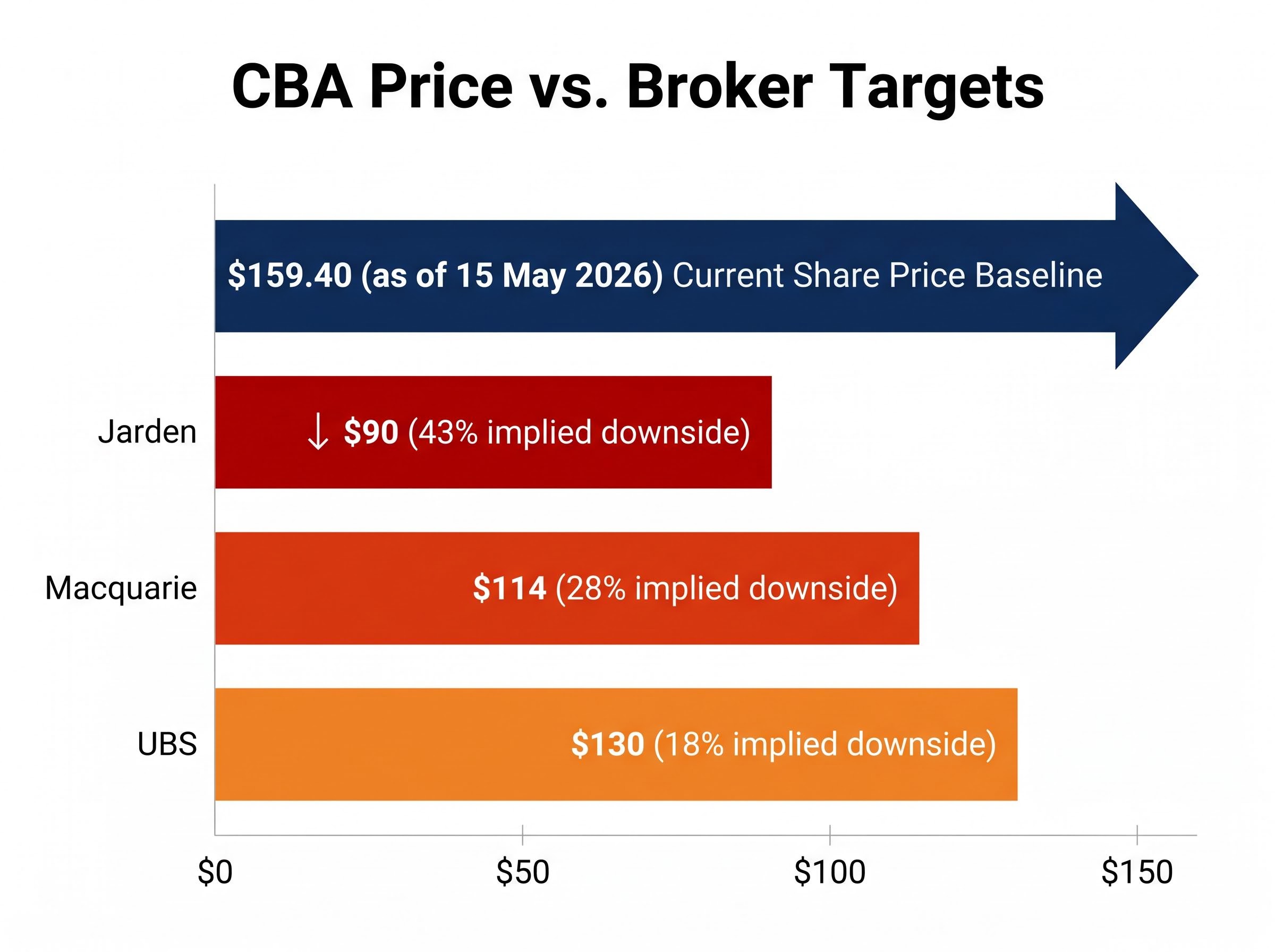

Every major broker covering Commonwealth Bank of Australia (CBA) holds a sell rating on the stock. Not one. All four. CBA shares closed at $159.40 on 15 May 2026, sitting anywhere from 18% to 43% above the highest and lowest analyst price targets in the market.

This disconnect is not new, but it sharpened considerably this week. Q3 FY2026 results landed as a slight miss, the stock recorded its steepest single-day fall since the bank’s 1991 listing, and the Federal Budget introduced a policy change targeting the precise lending segment where CBA dominates Australian banking. The confluence of these events makes the bearish case worth understanding with precision, not simply noting in passing.

What follows is a structural argument, not a results-week reaction. This analysis explains what four independent broker teams are actually arguing about the CBA share price, why the bank’s competitive strengths do not resolve the valuation problem, and why the negative gearing policy shift carries asymmetric risk for this bank specifically.

The gap between CBA’s price and every analyst’s target

The numbers speak before any interpretation is required.

| Broker | Rating | Price target | Implied downside from $159.40 |

|---|---|---|---|

| Jarden | Sell | $90 | ~43% |

| UBS | Sell | $130 | ~18% |

| Macquarie | Underperform | $114 | ~28% |

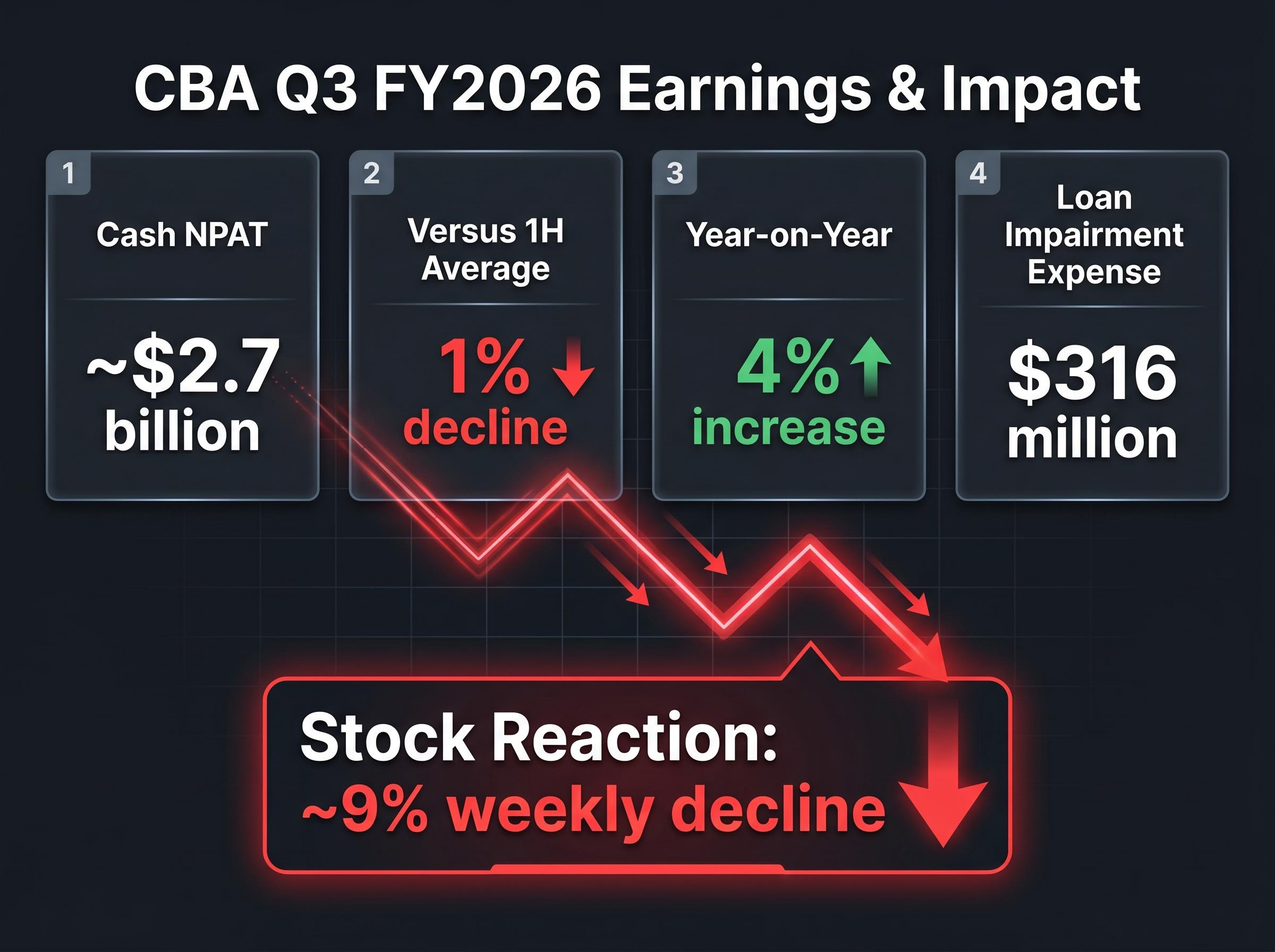

All four ratings were reaffirmed in the immediate post-Q3 results window, meaning each team had access to the latest earnings data when confirming its stance. Q3 FY2026 cash net profit after tax came in at approximately $2.7 billion, a 1% decline versus the first-half average and a 4% increase year-on-year. Sector-wide quarterly revenue declined approximately 3% quarter-on-quarter, according to Macquarie.

Jarden’s $90 price target implies that CBA shares would need to fall by roughly 43% to reach the firm’s assessed valuation, the widest gap of any major-bank broker target on the ASX.

If this were a single contrarian call, it could be set aside. Four independent teams reaching the same directional conclusion from the same post-results data is harder to dismiss.

When big ASX news breaks, our subscribers know first

What CBA genuinely does better than its peers

The bearish case is not built on the claim that CBA is a bad bank. It is built on the claim that a good bank at the wrong price is still a poor investment. Understanding the quality argument matters, because the brokers themselves acknowledge it.

CBA’s competitive advantages are real and well-documented:

- Highest return on equity (ROE) among domestic banking peers

- Lowest cost of capital in the sector

- Leading technology platform relative to ANZ, NAB, and Westpac

- Largest deposit base among the majors, skewed toward household and transaction accounts

- Largest share of the Australian residential mortgage market

- Superior asset quality within the investor home loan segment, characterised by interest-only structures and wider spreads

Jarden reached the same conclusion from a wider valuation gap.

The investor lending book

CBA’s dominance in investor home lending is structurally distinct. Its investor loan segment carries interest-only structures, wider net interest margins, and what the bank internally describes as its lowest-risk portfolio among the majors. These characteristics make investor lending the highest-quality revenue stream in CBA’s mortgage book, a point that becomes directly relevant when assessing the budget’s policy changes.

Understanding price-to-earnings premiums and why they create valuation risk

A stock trading above every analyst’s assessed value is not necessarily overpriced. It may reflect earnings growth expectations that have not yet been captured in formal models, or it may reflect demand factors (index weighting, institutional mandates, retail investor loyalty) that sustain a price premium independent of earnings.

The distinction matters because a premium supported by earnings trajectory can survive bad quarters. A premium sustained by sentiment and structural demand is vulnerable the moment the earnings narrative softens.

PE ratios in ASX bank stocks can mislead when NIM trajectories are shifting, because a multiple that appears stable on trailing earnings may already embed margin compression that has not yet flowed through reported profit, a dynamic particularly relevant when assessing whether CBA’s premium reflects genuine earnings durability or a lag in analyst model updates.

CBA’s Q3 results tightened that narrative. Cash net profit declined 1% against the first-half average. Loan impairment expense rose to $316 million, with elevated collective provisions attributed to geopolitical and macroeconomic uncertainty. The stock fell approximately 9% over the week, its steepest decline since CBA’s 1991 listing, reversing all gains accumulated since mid-February.

Morgans framed the valuation problem directly: medium-term return potential is insufficient at current elevated multiples. The question is not whether CBA earns well. The question is whether the price already assumes it will earn better, and what happens when that assumption weakens.

When a stock trades 43% above one broker’s target and 18% above another’s, the premium itself becomes the risk. Every quarter must deliver enough to justify what the market has already priced in.

Why the budget’s negative gearing changes land hardest on CBA

The policy mechanics

The Federal Budget, announced on 12 May 2026, restricts negative gearing for established residential investment properties purchased after 7:30pm AEST on that date. The restriction means losses on newly acquired established investment properties can only be offset against other residential property income, not broader taxable income. Changes take effect 1 July 2027.

The Federal Budget negative gearing factsheet confirms that losses on newly acquired established investment properties purchased after 7:30pm AEST on 12 May 2026 can only be offset against other residential property income, with new builds fully exempt and all existing holdings grandfathered under prior treatment.

New builds are fully exempt. Negative gearing treatment for new residential construction remains unchanged. All existing investment property holdings are grandfathered regardless of when they were purchased.

| Property type | Previous treatment | New treatment (post-1 July 2027) |

|---|---|---|

| Established (new purchases) | Losses offset against all taxable income | Losses offset only against residential property income |

| New builds | Losses offset against all taxable income | Unchanged |

| Existing holdings (pre-announcement) | Losses offset against all taxable income | Fully grandfathered; unchanged |

Why CBA carries outsized exposure

The policy creates a structural disincentive for new investor purchases of established residential property. CBA leads the major banks in investor home lending and derives structurally superior economics from that segment: wider spreads, interest-only structures, and higher asset quality relative to owner-occupier lending.

Jarden specifically flagged CBA’s investor lending dominance as the basis for its outsized exposure argument. The RBA Financial Stability Review from March 2026 noted that high debt-to-income (DTI) investor lending had been increasing, though remaining below APRA limits, providing macroprudential context for the policy’s timing.

The bank valuation transmission from the negative gearing reform runs through credit growth assumptions rather than capital adequacy, with the Parliamentary Budget Office modelling a 1-4% national property price impact that is sufficient to compress forward earnings multiples without triggering a solvency event, and CBA’s 25x forward PE amplifies that compression relative to peers trading at lower starting multiples.

Why grandfathering does not neutralise the risk

Grandfathering protects the credit quality of CBA’s existing investor loan book. No current borrower faces changed terms. The risk sits elsewhere: origination volume. New investor demand for established properties faces a direct structural disincentive from 1 July 2027, and origination volume is what drives revenue growth in a mortgage book. A dampener on new investor demand for established property compresses CBA’s forward lending pipeline precisely in the segment where its economics are strongest.

What the new build carve-out means for CBA’s lending pipeline

The exemption of new builds from the negative gearing restriction is a genuine partial offset. If investor demand migrates from established properties toward new construction, CBA would participate in that lending activity.

The offset is partial, however, because the economics differ. Established property investor lending and construction or new-build lending carry different characteristics:

- Spread profile: Established investor loans typically carry wider net interest margins than construction lending

- Loan structure: Interest-only arrangements dominate established investor lending; construction loans involve staged drawdowns

- Asset quality: Established property lending carries lower loss rates than construction exposure

- Borrower profile: Established property investors tend to be repeat borrowers with existing portfolios; new-build investors may include first-time property investors with different risk characteristics

The RBA’s March 2026 observation that household indebtedness remains a domestic vulnerability adds context. If the policy successfully redirects investor activity toward new builds, CBA would retain some investor lending volume, but likely at compressed margins relative to its current established property book.

The implementation date of 1 July 2027 gives the market approximately 13 months of lead time to price the impact. The brokers’ current targets already reflect the headwind scenario, not the catastrophe scenario. The distinction matters for investors assessing whether the sell ratings have overreacted or merely arrived early.

The bear case does not need CBA to fail; it just needs the premium to compress

Two forces now press on CBA’s valuation premium simultaneously: near-term earnings softness confirmed in Q3 results, and a forward policy risk to the bank’s highest-quality lending segment beginning 1 July 2027.

The bearish consensus does not require CBA to report losses or face a credit event. It requires only that the premium multiple normalises toward peers. If that happens, significant downside follows even in a scenario where CBA continues to report solid earnings.

Passive index flows had previously provided a structural support mechanism for CBA’s premium by making it the ASX’s largest company by market capitalisation and attracting mandatory buying from index-tracking funds, but the post-sell-off market capitalisation falling below BHP’s removes that mechanical tailwind precisely when the earnings narrative is softening.

Investors holding for approximately one year are marginally underwater. The weekly decline of roughly 9% reversed all gains since mid-February, and loan impairment expense of $316 million with elevated provisions signals management itself is preparing for a less benign environment.

The three-part structural argument underpinning every broker’s sell rating is specific:

- Valuation premium: CBA trades 18% to 43% above the full range of analyst targets, a gap sustained by sentiment rather than earnings trajectory

- Near-term earnings softness: Q3 cash net profit declined 1% versus the first-half average, tightening the growth narrative that supports the premium

- Forward policy headwind: The negative gearing restriction on established properties, effective 1 July 2027, directly compresses future origination volumes in CBA’s strongest lending segment

The consensus does not demand that investors sell immediately. It does demand a clear thesis for why the stock should appreciate from $159.40 despite these headwinds. The broker target range of $90 (Jarden) to $130 (UBS) represents that challenge in numerical terms.

Where this leaves CBA in the portfolio conversation

CBA’s quality is not in dispute. The question is whether quality at this price, at this point in the policy cycle, offers adequate forward return. Three conditions would challenge the bearish consensus:

- A meaningful re-acceleration of earnings growth sufficient to justify a sustained premium over peers

- Policy reversal or significant dilution of the negative gearing changes before the 1 July 2027 implementation date

- A compression of peer bank multiples that makes CBA’s relative premium appear less extreme

Long-term holders with low cost bases face a different calculus than new buyers evaluating entry at $159.40. The grandfathering provision protects existing investor property loans, and the RBA’s March 2026 observation that rising high-DTI investor lending was a vulnerability suggests the policy may simultaneously reduce a systemic risk the regulator had flagged.

For investors wanting to understand how the bearish case extends across all four major banks rather than CBA alone, our full explainer on Morgans’ sector-wide sell thesis covers the provisioning forecasts, earnings downgrade trajectory, and per-bank implied total return estimates that informed the simultaneous sell ratings on ANZ, CBA, NAB, and Westpac ahead of the May 2026 reporting season.

The forward question the market will answer over the next 13 months is whether CBA’s investor lending volumes hold up in the window before the policy takes effect, and whether that pre-implementation period allows orderly re-pricing or concentrated adjustment. The brokers have made their assessment. Investors now make theirs.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding policy impacts and earnings trajectories are subject to change based on market developments and regulatory outcomes.