Finfluencer Rules Won’t Work Until the Penalty Beats the Profit

2 hrs ago

Most ASX biotech stocks sit years from any regulatory inflection point. Dimerix (ASX: DXB) and Paradigm Biopharma (ASX: PAR) do not. Both companies carry binary catalysts with defined 2026 timelines, and analyst consensus implies up to 579% upside for DXB alone. In a sector defined by pre-revenue balance sheets, capital-intensive trial programmes, and the kind of catastrophic outcomes that erased Opthea’s workforce and shareholder value after a Phase 3 failure in March 2025, the distinction matters. This article profiles both companies in detail, explains the regulatory mechanics that make each case distinctive, and provides a framework for assessing late-stage biotech risk before any capital decision.

Clinical-stage biotech outcomes cluster at the extremes. A successful Phase 3 trial can deliver returns that reprice a company by multiples of its current valuation. A failed one can destroy the majority of invested capital within days. There is very little middle ground, and that asymmetry is the defining feature of the sector for investors.

Late-stage programmes differ from earlier-stage ones across three dimensions:

ASX small-to-mid-cap biotechs range in market capitalisation from below A$100 million up to approximately A$1 billion, and most remain in early clinical stages. Both DXB and PAR have cleared early futility hurdles, placing them in a narrower cohort with near-term data events.

Phase 3 failure can erase more than 80% of a company’s workforce and the vast majority of shareholder value within weeks, as Opthea’s COAST trial outcome in March 2025 demonstrated.

That risk does not disappear at the late stage. It concentrates. Surrogate endpoints and interim analyses, two features relevant to both companies profiled below, can bring forward the moment of truth in a trial. They reduce the waiting period but not the underlying binary nature of the outcome.

The Opthea outcome is one data point in a broader pattern of compounding pressures on the sector; investors wanting the full picture on ASX healthcare sector risk, including FDA instability under the current US administration and its effect on the discount rate applied to pre-approval pipeline assets, will find our full explainer walks through how structural US policy shifts are repricing valuations across device makers and biotech companies in ways that have no natural cyclical reversal point.

Dimerix is developing DMX-200 for focal segmental glomerulosclerosis (FSGS), a rare kidney disease that affects more than 40,000 patients in the United States alone and typically progresses to kidney failure within five years. No therapies are currently approved specifically for FSGS globally, creating the kind of measurable unmet need that shapes the Food and Drug Administration’s (FDA) willingness to consider accelerated pathways.

The FDA workshop on proteinuria endpoints for FSGS concluded that available data support complete remission of proteinuria as a surrogate endpoint for progression to kidney failure, providing the scientific foundation that makes the accelerated approval pathway available to DMX-200.

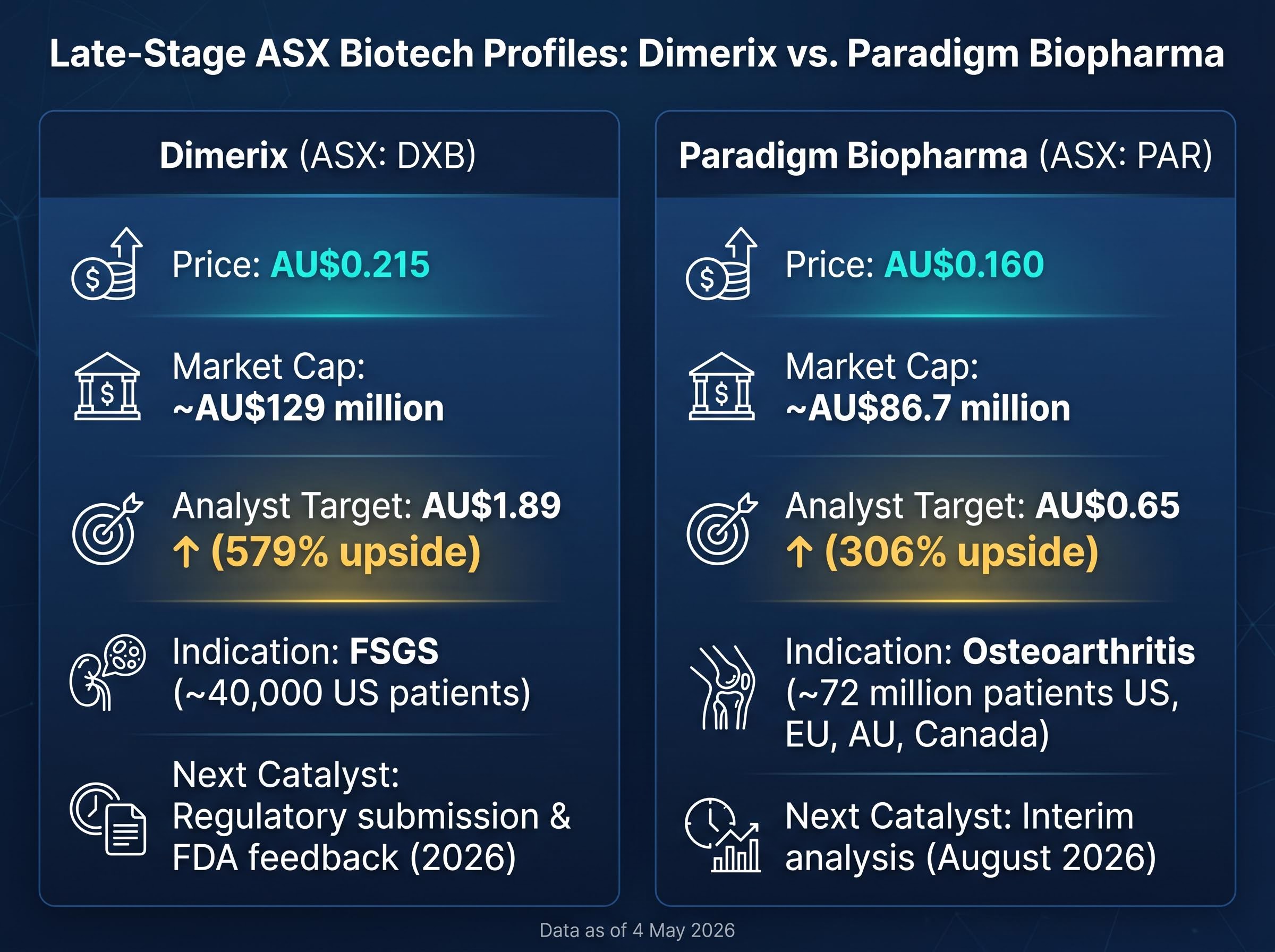

As of 4 May 2026, DXB trades at AU$0.215 with a market capitalisation of approximately AU$129 million. Analyst consensus rates the stock a Moderate Buy with an average 12-month price target of AU$1.89.

The AU$1.89 average analyst target against a AU$0.215 share price implies approximately 579% upside, a gap that reflects the market pricing in a low probability of approval success rather than analyst overconfidence.

The ACTION3 Phase 3 trial has completed full adult enrolment at 286 patients, with dosing completed by the end of 2025. Retention into the open-label extension stands at 94%. An earlier interim efficacy analysis, using the first 72 patients on the proteinuria endpoint, passed successfully.

The statistical review was completed on 28 April 2026. The company’s focus has shifted to regulatory submissions and FDA feedback on the approval pathway.

The FDA’s recognition of proteinuria reduction as a surrogate endpoint for DMX-200 is the structural differentiator in this case. Accelerated approval allows the FDA to approve a drug based on a surrogate endpoint, a measurable outcome reasonably likely to predict clinical benefit, with post-market confirmatory trials required after approval. This is not a standard feature of kidney disease trials; it is a company-specific concession that opens a faster regulatory pathway.

On 14 April 2026, the FDA approved sparsentan for reducing proteinuria in FSGS. This approval is a directly relevant regulatory precedent: it validates proteinuria as an accepted surrogate endpoint for FSGS therapies and strengthens the framework within which DMX-200 could pursue accelerated approval. The FDA also updated its surrogate endpoint table within weeks of May 2026, further reflecting the evolving regulatory environment for kidney disease.

Orphan drug designations across the US, Europe, Japan, and the UK provide up to 10 years of market exclusivity, a significant commercial protection for a company of this size.

| Metric | Detail | Significance to Investors | Source/Date |

|---|---|---|---|

| Disease indication | FSGS (no approved therapies globally) | Unmet need supports accelerated regulatory pathways | Company filings |

| Trial enrolment status | 286 adult patients; dosing complete | Enrolment risk eliminated; trial in data phase | Q1 2026 quarterly report |

| Regulatory pathway | FDA surrogate endpoint (proteinuria) recognised | Opens accelerated approval; sparsentan precedent set April 2026 | FDA records, April 2026 |

| Analyst price target | AU$1.89 (Moderate Buy consensus) | Implies 579% upside from AU$0.215 | Analyst consensus, May 2026 |

| Key 2026 milestone | Statistical review completed 28 April 2026 | Company now in regulatory submission preparation phase | ASX announcement, 28 April 2026 |

The addressable population for a disease-modifying osteoarthritis treatment spans approximately 72 million eligible patients across the US, EU, Australia, and Canada. No currently approved therapy modifies the underlying disease; existing treatments manage symptoms only. If Zilosul succeeds, Paradigm Biopharma would enter a market with no direct competitive analogue.

An estimated 72 million patients across four major markets have no access to a disease-modifying osteoarthritis therapy, making this one of the largest unmet treatment needs in musculoskeletal medicine.

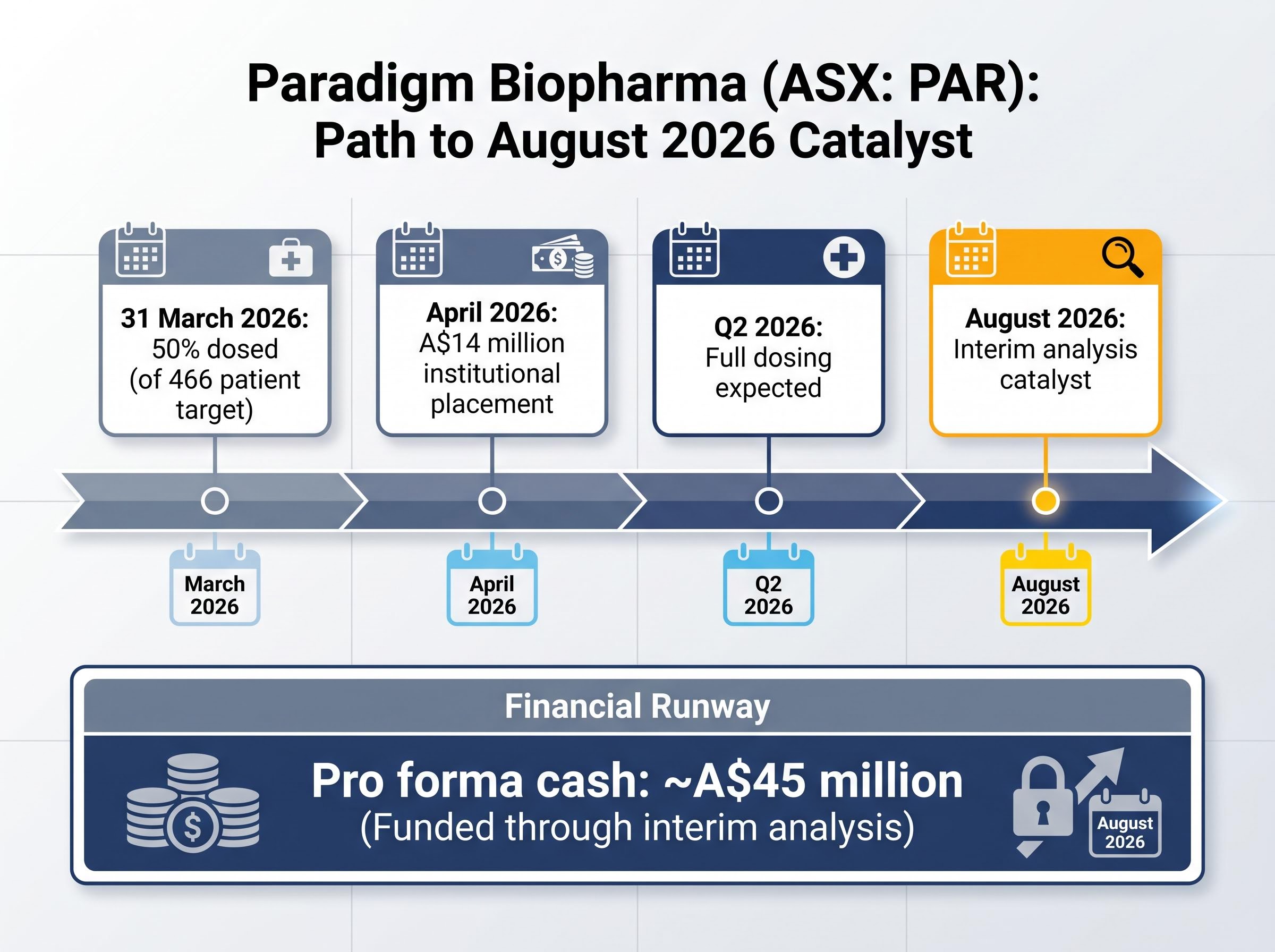

As of 4 May 2026, PAR trades at AU$0.160 with a market capitalisation of approximately AU$86.7 million. The analyst consensus price target sits at AU$0.65, implying approximately 306% upside from the current price.

The PARA_OA_012 Phase 3 trial targets enrolment of 466 patients. As of 31 March 2026, 50% of patients had been dosed, with full dosing expected in Q2 2026. The interim analysis is confirmed for August 2026.

The August 2026 interim analysis is prespecified in the trial protocol. This is a structural credibility marker: it was designed into the trial from the outset rather than added as an ad hoc management decision. At 50% enrolment, the enrolled cohort reaches the threshold required for the prespecified interim review. This design is common in adaptive trials because it allows early stopping for efficacy or futility before the full trial cost is incurred.

In April 2026, Paradigm completed an upsized A$14 million institutional placement, bringing pro forma cash to approximately A$45 million. This figure is the operative number for assessing whether the company can reach its interim catalyst without dilutive emergency funding. The placement extends financial runway through the Q3 2026 interim analysis, removing one of the most common pre-catalyst risks for small-cap biotechs.

A positive interim result could attract licensing or acquisition interest from larger pharmaceutical companies with established rheumatology commercial infrastructure. The converse risk is equally real: interim analyses can be stopped for futility, which would represent a severe adverse outcome for shareholders.

Investors wanting to understand the scientific foundation that makes the August 2026 interim credible should read our deep-dive into Paradigm’s Phase 2 biomarker results, which covers the OARSI Congress presentation data showing up to 74% reductions in synovial ARGS versus placebo, the correlation between those biomarker changes and patient-reported WOMAC outcomes, and why the trial design team used this evidence to inform the PARA_OA_012 Phase 3 protocol.

| Metric | Detail | Significance to Investors | Source/Date |

|---|---|---|---|

| Disease indication | Osteoarthritis (no disease-modifying treatment approved) | 72 million eligible patients; first-mover potential | Industry data |

| Trial enrolment status | 50% dosed (of 466 target) as of 31 March 2026 | Enrolment on track; full dosing expected Q2 2026 | ASX quarterly report, March 2026 |

| Interim analysis date | August 2026 (Q3 CY2026) | Most precisely dated binary catalyst among profiled ASX biotechs | Company filings |

| Funding runway | Pro forma cash ~A$45 million | Funded through interim analysis; dilution risk reduced | April 2026 placement announcement |

| Analyst price target | AU$0.65 | Implies 306% upside from AU$0.160 | Analyst consensus, May 2026 |

Both companies sit closer to regulatory inflection points than most ASX biotechs, but the nature of each opportunity differs in ways that matter for portfolio construction.

| Evaluation Dimension | Dimerix (DXB) | Paradigm Biopharma (PAR) |

|---|---|---|

| Stage of evidence | Adult enrolment complete; statistical review done | 50% dosed; full dosing expected Q2 2026 |

| Regulatory pathway | FDA surrogate endpoint recognised; accelerated approval pathway | No specific FDA interaction publicly disclosed |

| Next catalyst | Regulatory submission and FDA feedback (2026) | Interim analysis confirmed August 2026 |

| Funding to catalyst | Funded through regulatory phase | ~A$45M pro forma cash; funded through interim |

| Addressable market | ~40,000 US patients (orphan indication) | ~72 million patients across US, EU, AU, Canada |

| Analyst upside target | 579% (AU$0.215 to AU$1.89) | 306% (AU$0.160 to AU$0.65) |

Analyst price targets reflect probability-weighted outcomes, not guarantees. The gap between current prices and targets reflects the market’s estimate of approval probability. Opthea’s Phase 3 failure, which arrived with no clear warning from earlier data, remains a reminder that late-stage evidence can still disappoint.

Single-trial NDA pathways for orphan indications have become a recurring feature of FDA engagement for ASX biotechs in 2026, with PYC Therapeutics securing agreement on a registrational design that uses a primary endpoint threshold while preserving a totality-of-evidence fallback, a structure that illustrates how the agency balances statistical rigour against the practical constraints of rare disease development.

For investors considering exposure to either or both names, three principles apply to position sizing in late-stage biotech:

What separates DXB and PAR from the broader ASX biotech cohort is specificity. Both companies have completed or confirmed the milestones that most small-cap biotechs are still working toward: full or majority enrolment, cleared futility hurdles, defined regulatory engagement, and funded runways to their respective catalysts.

The 28 April 2026 Dimerix statistical review completion and the August 2026 Paradigm interim analysis are the two calendar anchors for the sector this year. Most ASX biotechs remain years from any comparable inflection point.

The irreducible risk remains. The most rigorous trial design and the most supportive regulatory environment cannot eliminate the possibility that a drug fails to demonstrate efficacy. Phase 3 is where most drug candidates fail, regardless of how promising earlier data appeared.

Phase 3 safety milestones function differently from efficacy readouts in how they move a development programme forward; Telix Pharmaceuticals’ ProstACT Global Part 1 results, which confirmed an acceptable tolerability profile across all three treatment cohorts without triggering any new safety signals, demonstrate how a cleared safety threshold resets investor focus onto the larger randomised expansion and the subsequent FDA engagement required to open US enrolment.

Investors monitoring both positions should track:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. These forward-looking statements are speculative and subject to change based on market developments and company performance.

Dimerix (ASX: DXB) and Paradigm Biopharma (ASX: PAR) are among the most advanced ASX biotech stocks with defined 2026 catalysts, including DXB's FDA regulatory submission phase and PAR's prespecified interim analysis confirmed for August 2026.

A surrogate endpoint is a measurable outcome, such as proteinuria reduction, that the FDA accepts as reasonably likely to predict clinical benefit, allowing accelerated drug approval before full long-term data is available. For Dimerix, the FDA's recognition of proteinuria as a surrogate endpoint for FSGS opens a faster approval pathway for DMX-200.

As of May 2026, analyst consensus implies approximately 579% upside for Dimerix (DXB) from AU$0.215 to a target of AU$1.89, and approximately 306% upside for Paradigm Biopharma (PAR) from AU$0.160 to a target of AU$0.65.

Yes. Following an upsized A$14 million institutional placement in April 2026, Paradigm Biopharma held pro forma cash of approximately A$45 million, which the company states is sufficient to fund operations through the Q3 2026 interim analysis.

Late-stage biotech investing carries binary risk: a successful Phase 3 trial or regulatory approval can multiply a company's valuation, while a failure can erase the majority of shareholder value within days, as demonstrated by Opthea's Phase 3 failure in March 2025 which decimated its share price and led to significant workforce reductions.