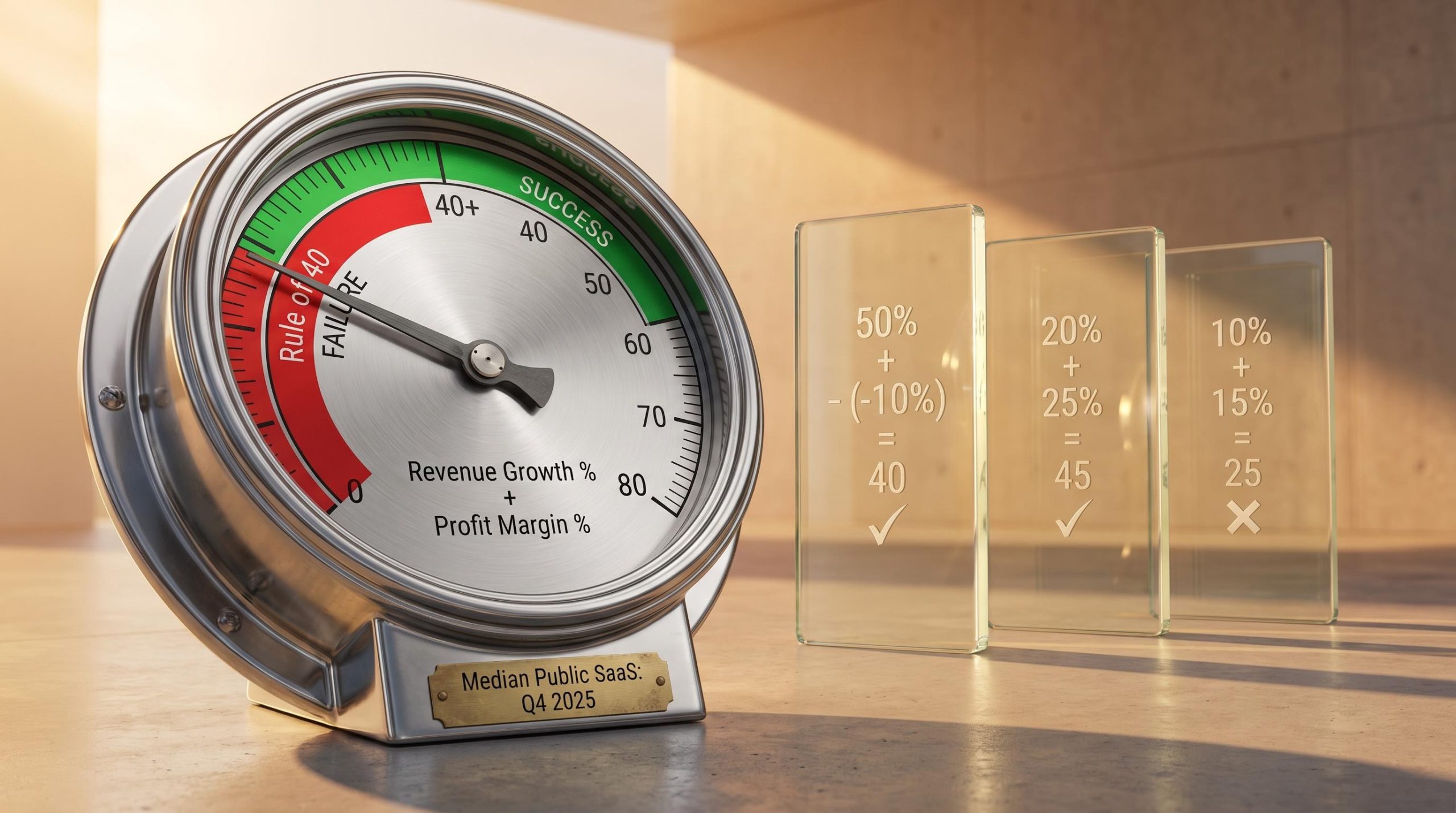

The median publicly traded SaaS company scores just 28 on the Rule of 40, meaning the typical listed software business fails the most widely cited health benchmark in the sector. That figure, drawn from Q4 2025 data, sits well below the 40-point threshold the metric was designed around. As SaaS revenue growth decelerated from 2022 onward without proportional margin recovery, investors needed a single lens to separate operationally disciplined businesses from those sacrificing sustainability for scale. The Rule of 40 became that lens, evolving from a practitioner shorthand into a near-universal valuation input. What follows explains what the Rule of 40 is, how to calculate it, how the growth-margin trade-off works through concrete scenarios, and how investors use it to assign valuation premiums or discounts. It also addresses the limitations and emerging criticisms that any serious analyst should understand.

What the Rule of 40 actually measures

SaaS businesses face a persistent tension: growing revenue fast typically requires spending aggressively on sales, marketing, and infrastructure, which compresses margins. Conversely, protecting margins usually means throttling the investment that drives growth. The Rule of 40 exists to reconcile these two competing forces into a single score, giving investors and operators a way to evaluate whether the overall balance is healthy regardless of which lever the business is pulling harder.

The formula is straightforward:

Rule of 40 Score = Revenue Growth Rate (%) + Profit Margin (%)

Revenue growth is measured year-over-year. The profit margin component is where practitioners diverge:

- EBITDA margin is the most widely used input and the standard benchmark in most SaaS analyses, as it captures operating profitability before non-cash charges.

- Free cash flow (FCF) margin is preferred by investors focused on cash generation durability, particularly when evaluating companies with high capital expenditure or stock-based compensation.

A score of 40 or above signals that a company has struck a healthy balance between growth and profitability. A score below 40 flags an imbalance: the business is neither growing fast enough nor generating sufficient margin to compensate. The metric is most meaningful for companies above $5-10M in annual recurring revenue (ARR), where operational patterns are stable enough to interpret.

When big ASX news breaks, our subscribers know first

How the growth-margin trade-off plays out in three scenarios

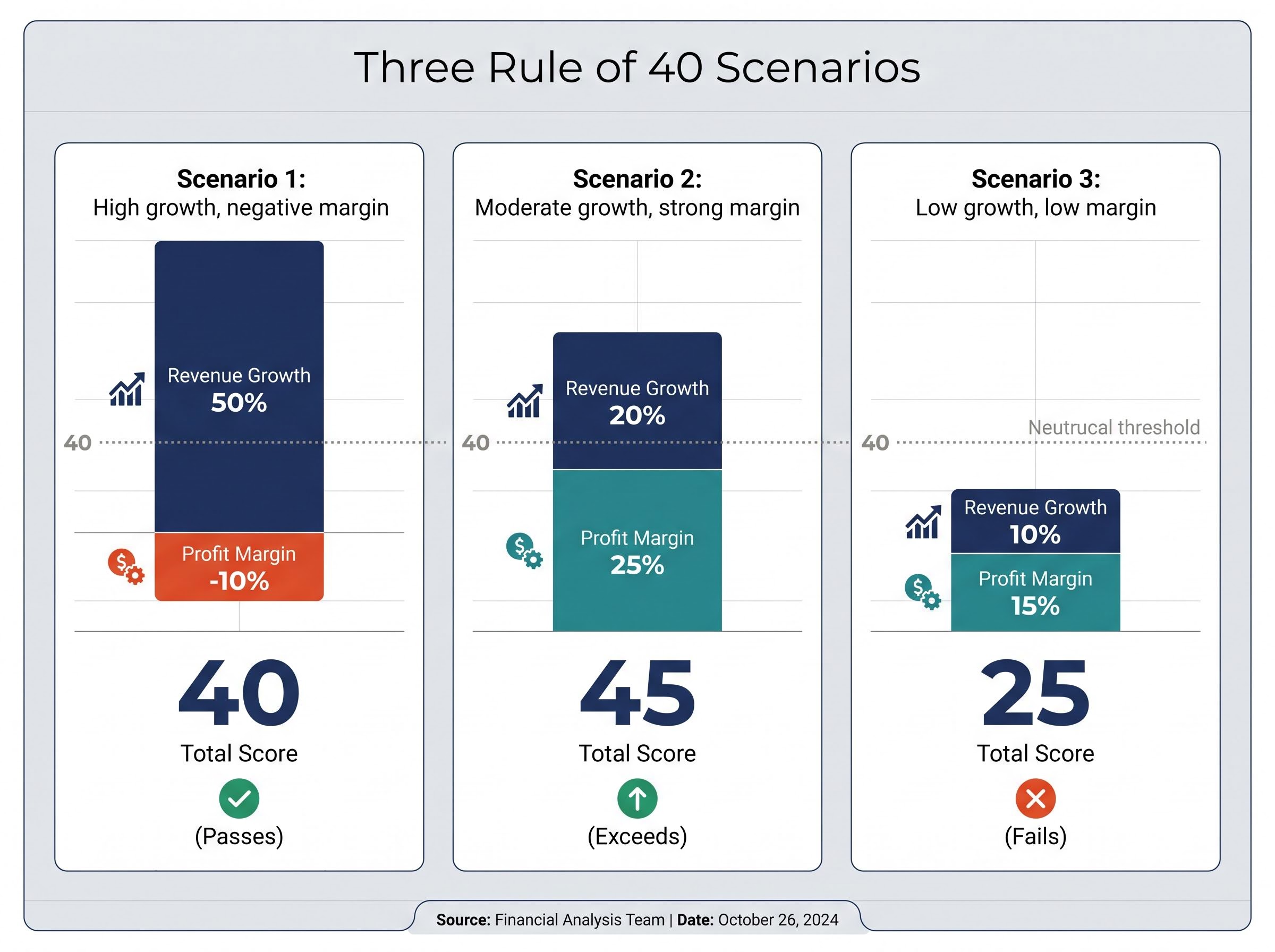

The number 40 is not the interesting part of the Rule of 40. The interesting part is that two companies with completely different financial profiles can reach the same score, and a third company that appears reasonable on both dimensions can still fail.

Consider a high-growth, early-stage SaaS business burning cash to capture market share. Revenue is expanding at 50% year-over-year, but aggressive spending produces a -10% profit margin. The sum is 40. The company passes.

Now consider a maturing SaaS business with moderate growth. Revenue growth has settled to 20%, but disciplined cost management delivers a 25% profit margin. The sum is 45. This company not only passes but exceeds the threshold.

A third company sits in a less comfortable position. Revenue growth has decelerated to 10%, and margins have only reached 15%. The sum is 25. Neither component is doing enough work to compensate for the other. This is the failure case the metric was designed to identify.

| Scenario | Revenue Growth Rate | Profit Margin | Rule of 40 Score | Interpretation |

|---|---|---|---|---|

| 1: High growth, negative margin | 50% | -10% | 40 | Passes; typical early-stage SaaS profile |

| 2: Moderate growth, strong margin | 20% | 25% | 45 | Exceeds; mature, profitable business |

| 3: Low growth, low margin | 10% | 15% | 25 | Fails; neither growth nor profitability compensates |

The contrast between Scenarios 1 and 2 is the metric’s core design feature. It does not prescribe a specific mix. A company burning cash is acceptable if it is growing fast enough; a slow-growing company is acceptable if its margins compensate. The Rule of 40 is not a profitability test or a growth test. It is a combined-efficiency test, and the weight given to each component should shift as a company matures.

Understanding the score tiers and what they mean for investors

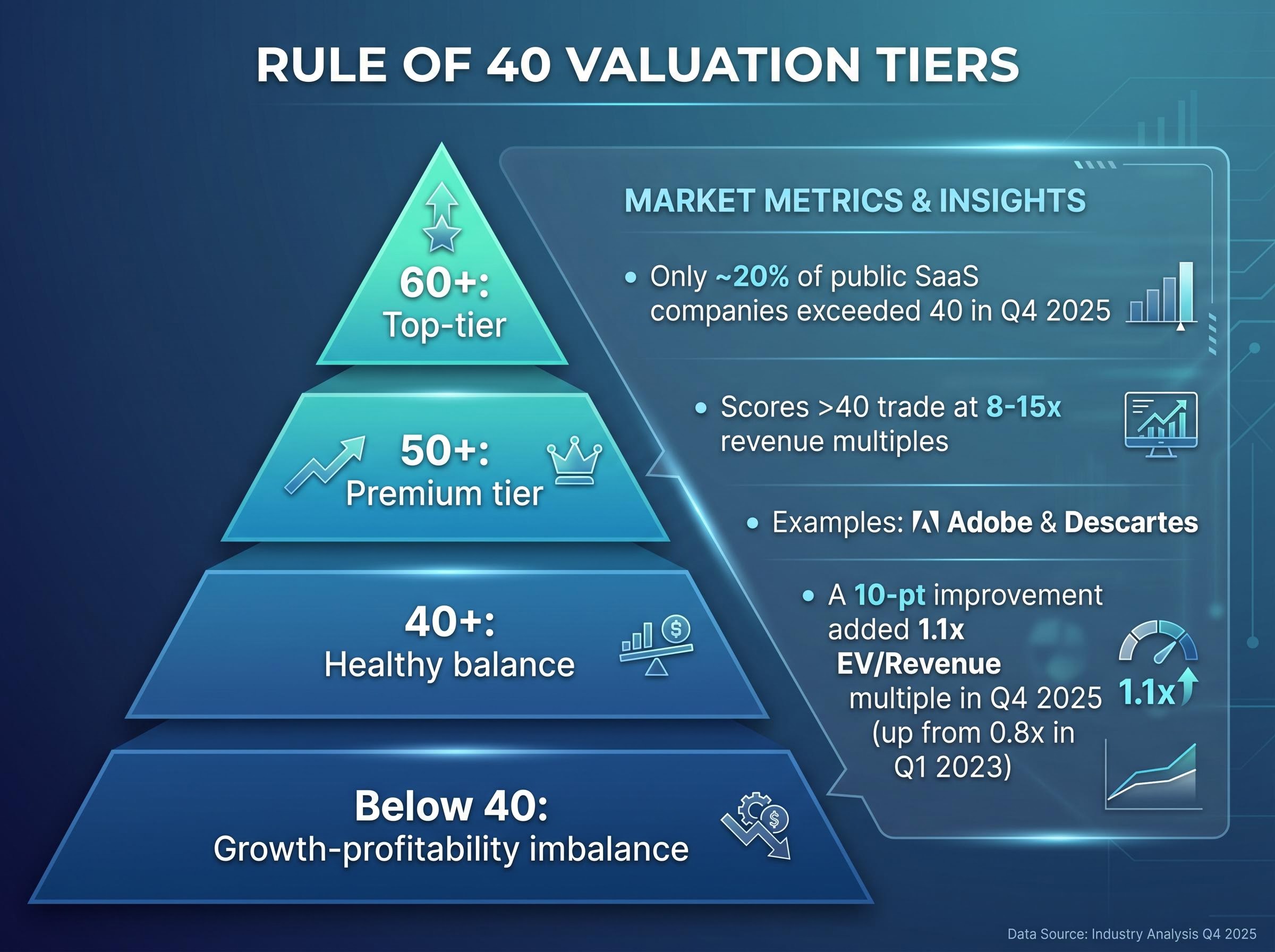

Passing the 40-point threshold is the baseline, but the investment implications sharpen at higher tiers. Practitioners generally interpret scores across four bands:

- Below 40: Growth-profitability imbalance. The business is neither scaling fast enough nor generating sufficient returns, which typically results in valuation discounts.

- 40+: Healthy balance. The company demonstrates operational discipline consistent with sustainable SaaS economics.

- 50+: Premium tier. Investors begin assigning materially higher revenue multiples at this level, reflecting confidence in both growth trajectory and margin structure.

- 60+: Top-tier. A small number of companies reach this band; they tend to command the highest valuations in the sector.

Only around 20% of tracked public SaaS companies exceeded the 40-point threshold as of Q4 2025. Adobe and Descartes are among the public companies consistently cited as comfortably surpassing it. Companies scoring above 40 generally trade at 8-15x revenue multiples, while those below face discounts.

The Catapult Sports Rule of 40 trajectory illustrates this progression in practice: the company recorded a score of 33 in the first half of FY26 and is guiding toward further improvement in the full-year result, driven by EBITDA expanding approximately 50% against ACV growth of 27-28%, the kind of margin-led score improvement the benchmark is designed to reward at scale.

Each 10-point improvement above 40 added 1.1x EV/Revenue multiple in Q4 2025, up from 0.8x in Q1 2023.

That sharpening of multiple sensitivity is not a coincidence. It reflects a structural repricing of what the market values.

Why multiple sensitivity has sharpened since 2022

The macro backdrop shifted materially from 2022 onward. Venture capital funding tightened. Interest rates rose. Revenue growth decelerated across the SaaS sector without offsetting margin recovery. In that environment, the Rule of 40 moved from a supplementary heuristic to a proxy for operational discipline, and investors began pricing the distinction more aggressively.

The median public SaaS company’s score remaining at approximately 28 reflects structural pressure across the sector, not isolated underperformance. The gap between the median score and the 40-point threshold captures the degree to which the broader industry has struggled to recalibrate after the growth-at-any-cost era.

Windsor Drake’s SaaS valuation multiples analysis for 2026 documents how EV/Revenue multiples repriced sharply after 2022 as interest rates rose and growth decelerated, providing the market context that explains why Rule of 40 score improvements now carry greater multiple sensitivity than in the prior decade.

How management teams use the Rule of 40 as a strategic tool

From an investor’s perspective, the Rule of 40 is a screening and valuation tool. From a management team’s perspective, it serves a different function: structuring the growth-versus-margin trade-off as an explicit strategic decision. Should the business prioritise accelerating revenue this period, or improving margins? The score provides a single reference point for that conversation.

The expected composition of the score changes as a company scales. An early-stage business at $10M ARR is expected to carry low or negative margins offset by high growth. A company at $100M+ ARR is expected to show score improvement driven increasingly by margin expansion rather than top-line acceleration.

KeyBanc KBCM survey data illustrates how benchmarks shift across ARR tiers:

| ARR Tier | Median Rule of 40 Score | 75th Percentile |

|---|---|---|

| Under $10M | 28-35 | 45+ |

| $10-25M | 33-40 | 50+ |

| $25-50M | 36-42 | 54+ |

| $50-100M | 38-45 | 58+ |

| $100M+ | 40-48 | 62+ |

The progression matters. A $15M ARR business with a score of 35 is tracking within its expected range. The same score at $100M ARR would signal underperformance relative to peers. Understanding that the benchmark shifts with company scale prevents management teams from benchmarking against the wrong cohort, a common analytical error that produces misleading strategic conclusions.

SaaS ARR growth benchmarks shift considerably as companies move through revenue tiers; OpenLearning’s 35% ARR growth to $3.19 million across 17 consecutive quarters, combined with rising average revenue per customer, reflects the kind of top-line momentum that can sustain a passing Rule of 40 score while margin structures are still maturing.

The limits of the Rule of 40: what the score cannot tell you

Four sections of exposition risk leaving the impression that the Rule of 40 captures everything an investor needs to know about a SaaS business. It does not. The metric carries three structural blind spots:

- Input variability: The same company’s score can differ materially depending on whether EBITDA margin or FCF margin is used, which undermines cross-company comparisons when the margin input is not disclosed or standardised.

- Early-stage unsuitability: Companies with inherent volatility in both revenue growth and margins (typically below $5-10M ARR) produce scores that fluctuate too widely to be directionally useful.

- Snapshot versus trajectory: The score captures a single period’s balance between growth and margin. It does not indicate whether a company’s score is improving, deteriorating, or oscillating, and a deteriorating 45 may be a worse signal than a rising 35.

Beyond these structural issues, a more recent critique has emerged. According to Bain and Company (April 2026), AI infrastructure costs are compressing margins across the SaaS sector even when revenue growth remains healthy.

Bain and Company’s analysis of AI and the Rule of 40 identifies the cost of AI infrastructure as a structural headwind that compresses margins even when revenue growth remains healthy, meaning the Rule of 40 treats this value-creating investment as indistinguishable from operational inefficiency.

Bain and Company (April 2026) identified AI infrastructure costs as a structural headwind creating margin compression across SaaS, a pressure the Rule of 40 does not disaggregate from other margin drivers.

The AI repricing of legacy software adds a structural dimension to this challenge: the $2 trillion in market capitalisation lost across US software markets in early 2026 reflected investor reassessment of per-user licensing models precisely because AI agents are displacing the human workflows those models were priced around, compressing both growth expectations and the margin projections that feed the Rule of 40.

AI simultaneously introduces tailwinds through productivity gains, but the net margin effect is compressing scores for many companies. The Rule of 40 treats all margin compression equally; it cannot distinguish between margin pressure from AI investment (potentially value-creating) and margin pressure from operational inefficiency (value-destroying).

Separately, investment analyst commentary from December 2025 questioned the metric’s predictive validity as a screening tool, citing poor performance as a filter in recent SaaS investment screens. This remains a minority view rather than a consensus shift, but it signals that practitioner confidence in the metric’s screening power is no longer universal.

The Rule of 40 is still the scorecard, but the game has changed

The Rule of 40 remains the dominant SaaS health benchmark heading into 2026. No competing metric has achieved comparable adoption among investors, operators, or analysts. Its strength lies in its simplicity: a single number that captures whether a SaaS business is generating enough combined value from growth and profitability to justify its operating posture.

The conditions under which that number is produced, however, have shifted materially since 2022. Capital is more expensive, growth rates have decelerated, AI infrastructure costs are introducing new margin pressure, and the market is pricing the metric’s output more aggressively than at any point in the prior decade. A 10-point improvement that once added 0.8x to a revenue multiple now adds 1.1x.

The practical takeaway: use the Rule of 40 as a first-pass filter and a strategic conversation-starter, not a definitive verdict. Always specify which margin input is being used. And recognise that a score of 40 earned through margin expansion in a capital-efficient environment carries different implications than the same score earned through aggressive growth in a zero-rate era. The era of growth at any cost is over. The Rule of 40 is the clearest single expression of what the market now demands.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.