Managing Money as a Couple: Systems That Stop the Arguments

2 mins ago

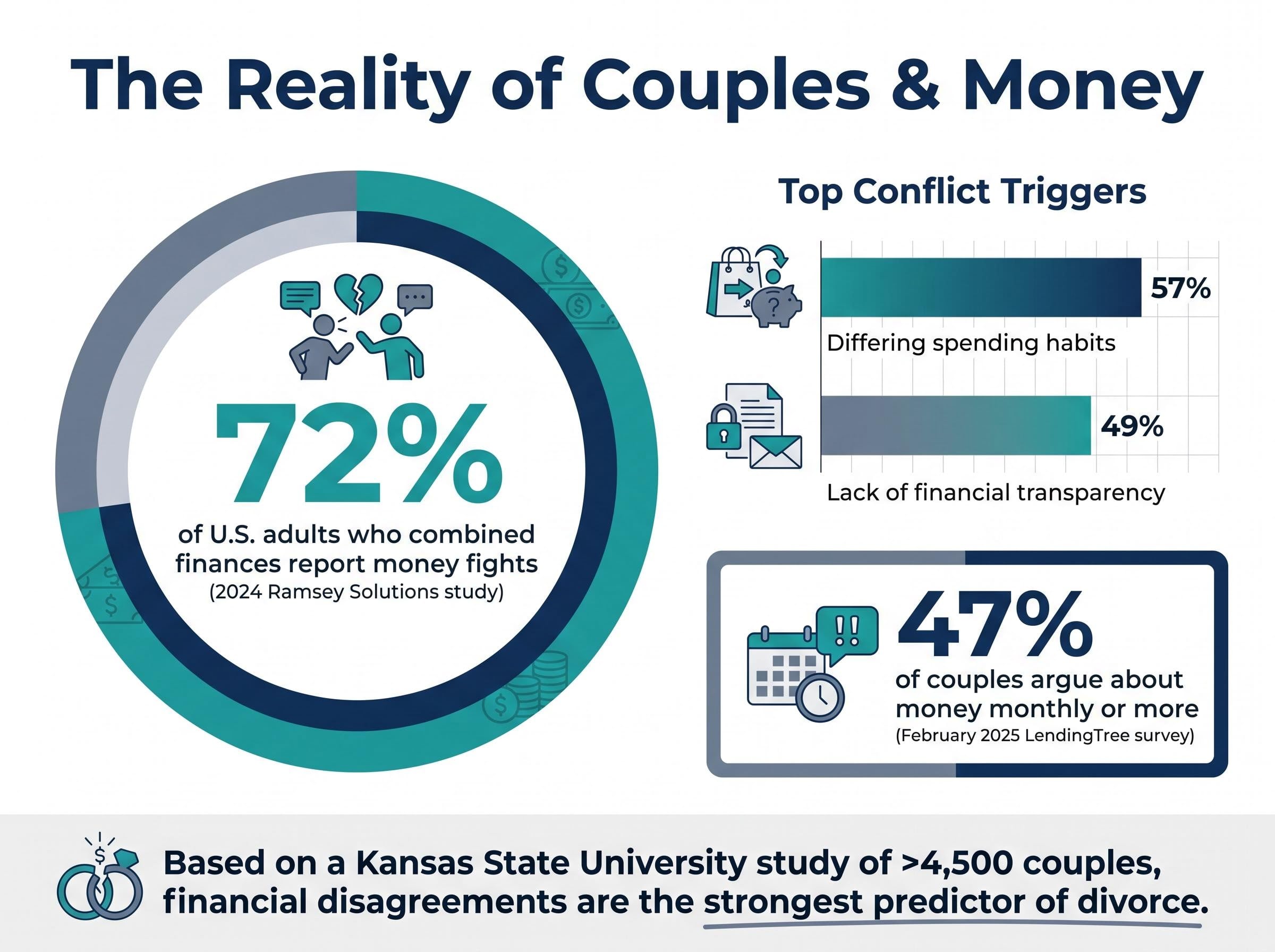

A Kansas State University study of more than 4,500 couples identified financial disagreements as the single strongest predictor of divorce, ranking above conflicts about children or extended family. The source of those disagreements, in most cases, is not the money itself. It is the absence of a shared system: couples where only one partner builds the budget, where spending remains opaque, or where there is no regular check-in are structurally vulnerable to resentment and drift regardless of income level. Rising grocery costs and persistent inflation on discretionary spending have only amplified pre-existing tension. This guide delivers a replicable monthly reset framework covering how to run a joint financial check-in, how to choose a structure that suits both partners, and how to use a low-spend month as a deliberate recovery tool when spending gets away from them.

The assumption is that financial conflict comes from not having enough. The research tells a different story.

A 2024 Ramsey Solutions study found that 72% of U.S. adults who combined finances with a partner reported money fights. The most commonly cited triggers were not income shortfalls but differing spending habits (57%) and lack of financial transparency (49%). A LendingTree survey from February 2025 reinforced the pattern: 47% of couples argue about money monthly or more, up from 2023 levels.

The Kansas State University research on financial disagreements and divorce, published in the peer-reviewed journal Family Relations, drew on longitudinal data from more than 4,500 couples and found that financial arguments were the strongest predictor of marital dissolution, outranking disputes about children, sex, or in-laws in both frequency and predictive power.

Kansas State University research found that financial disagreements are a stronger predictor of divorce than conflicts about children, in-laws, or household responsibilities.

The deeper fault line is what financial therapists call “money scripts,” the subconscious beliefs about money formed in childhood. One partner may operate from a scarcity script (save everything, spend nothing without anxiety), while the other spends for comfort or connection. Neither is wrong. Both feel entirely rational to the person holding them.

The structural dimension matters just as much. When only one partner builds the budget or controls financial visibility, the other can feel they need permission to access their own money. That dynamic breeds resentment even in financially comfortable households.

The most common couples’ money conflict triggers include:

Recognising these triggers reframes the problem. Financial conflict is not a character flaw; it is a system failure that responds to structure.

The macroeconomic backdrop matters here: record household debt levels and a US personal savings rate that fell to 4.00% in early 2026 mean couples are navigating genuine structural pressure, not just lifestyle drift, making the case for a repeatable shared system more urgent than it was even two years ago.

No single expense-splitting model works for every couple, and the most effective arrangement is whichever both partners perceive as equitable. The real risk is not picking the wrong model; it is never explicitly naming one at all.

| Structure | How It Works | Best Suited For | Watch Out For |

|---|---|---|---|

| 50/50 equal split | Both partners contribute the same dollar amount to shared expenses | Couples with comparable incomes who value simplicity | Can create genuine financial hardship when earnings diverge significantly |

| Proportional split | Each partner contributes a percentage of their income to shared costs | Couples with unequal incomes who want fairness relative to earning capacity | Requires regular recalibration as incomes change (promotions, job transitions, parental leave) |

| Full pooling with personal allocations | All income goes into a joint pool; each partner receives a defined personal spending amount | Couples seeking full financial integration while preserving individual autonomy | Requires high trust and transparent tracking to prevent one partner feeling monitored |

Research on couples’ financial health highlights full pooling with preserved individual “no-questions-asked” spending allocations as particularly effective at reducing routine justification friction.

Couples typically move through several arrangements across relationship milestones: moving in together, marriage, income changes, children. Revisiting the structure periodically is healthy, not a sign of failure. The conversation itself, naming the model both partners are currently operating under, often reveals that each person has been working from different unspoken assumptions.

A monthly money date does not require a perfect moment. It requires 30-60 minutes, a simple agenda, and enough consistency that both partners stop dreading it.

The communication principles that keep these sessions productive rather than contentious:

Starting with appreciations is recommended across financial therapy literature as a tension-reduction technique. The format matters less than the habit. A monthly check-in done consistently, even imperfectly, is the single most recommended intervention for reducing financial conflict frequency.

Apps with visual dashboards (charts, trend lines, goal trackers) make abstract numbers less emotionally charged and easier to discuss during a money date.

Choose based on tech comfort and whether the couple wants automation or manual discipline, not brand recognition.

Financial resentment often comes not from what is spent but from the requirement to justify it. A personal spending allocation removes that dynamic without undermining shared accountability.

The concept is straightforward. Each partner receives a defined monthly amount, agreed on together, that they spend without needing to explain or justify to the other. This is not a loophole in the budget. It is a deliberate structural feature.

Examples of what a personal spending allocation might cover:

Removing the need to justify everyday personal purchases reduces routine disagreements and the guilt spiral that often follows them. According to Ramsey Solutions research, lack of financial transparency ranks among the top conflict triggers for couples, but transparency works best as a systemic feature (shared visibility into joint spending categories) rather than surveillance of personal spending.

The most effective financial arrangement is whichever both partners perceive as equitable, regardless of structure.

The allocation amount should be revisited at the monthly check-in as circumstances change, keeping it connected to the shared system rather than floating independently. This mechanism works within all three splitting models outlined earlier: the 50/50 couple, the proportional-split couple, and the full-pooling couple all benefit from ring-fencing personal autonomy.

Overspending months happen to every couple. The productive response is a structured low-spend month the following month, not guilt or recrimination. Framed correctly, a spending reset is an act of agency rather than austerity.

Experts caution that overly strict no-spend months can trigger rebound spending: deprivation often leads to outsized splurges once the challenge ends.

The distinction matters. A strict no-spend challenge (everything beyond fixed bills stops) risks that rebound cycle. A low-spend or flex-spend approach, covering essentials plus a small discretionary buffer of roughly 10% of normal discretionary spending, is more sustainable and produces more durable results.

Categories that low-spend months most commonly target:

A practical implementation sequence for couples:

Low-spend challenges work best when they are short (2-4 weeks), specific (one category or one goal), and immediately followed by a money date to review results. Google search interest in no-spend challenges typically spikes post-holidays and post-overspend periods, confirming this is a widely used recovery tool. Community discussion on platforms like Reddit’s r/personalfinance reflects that framing the challenge as a team effort, rather than a restriction imposed by one partner on the other, is the difference between a challenge that sticks and one that breeds resentment.

The monthly check-in framework only reaches its potential when three foundational conversations have happened first. These do not need to be resolved in a single sitting.

These conversations are globally relevant. According to the World Economic Forum’s 2025 global financial inclusion report, 52% of European couples cite debt as a top financial stressor and 60% of Asian couples surveyed report emergency savings shortfalls. Shared savings goals address both pressures regardless of region.

Revisiting these three agreements at annual financial reviews, or at milestones like a new job, a child, or a move, is part of healthy financial practice. Once the foundations are explicit, the monthly 30-60 minute session becomes a progress review rather than a negotiation from scratch each time.

The monthly reset framework works not because it requires financial perfection but because it builds a repeatable structure that holds when spending drifts. The toolkit assembled here has three components: a monthly check-in agenda that takes under an hour, a personal spending autonomy mechanism that prevents justification fatigue, and a low-spend recovery month that functions as a financial pressure valve when a high-spend period arrives.

None of it requires agreement on every purchase. None of it requires matching money scripts. It requires one shared calendar entry and a willingness to sit down together.

The next step is specific: schedule a 30-minute money date within the next seven days. Choose a time, agree on the basic three-block agenda, and sit down. The first one will not be perfect. It does not need to be.

This article is for informational purposes only and should not be considered financial advice. Readers should conduct their own research and consult with financial professionals before making decisions about household financial management.

A money date is a monthly 30-60 minute structured financial check-in where both partners review spending, update savings goals, and plan for the month ahead using a simple three-block agenda designed to reduce conflict and build shared accountability.

There is no single best method; the most effective structure is whichever both partners perceive as equitable, with options including a 50/50 equal split, a proportional split based on income, or full pooling with individual personal spending allocations.

Research points to shared financial systems as the primary solution: establishing a named expense-splitting model, holding regular monthly check-ins, and giving each partner a defined personal spending allocation removes the justification friction that drives most routine money arguments.

A low-spend month is a structured 2-4 week period where couples agree to restrict specific discretionary categories, such as dining out or clothing, while maintaining a small buffer of around 10% of normal discretionary spending, used as a recovery tool after a high-spend period rather than as a strict no-spend challenge.

A Kansas State University study of more than 4,500 couples found that financial arguments were the strongest predictor of marital dissolution, outranking disputes about children, sex, or in-laws, largely because financial conflict reflects deeper system failures around transparency and shared decision-making rather than income levels alone.