Betashares ERTH ETF: Macro Tailwind Meets Real Volatility Risk

3 hrs ago

Australia’s inflation rate delivered a deceptive calm this week. The quarterly trimmed mean for Q1 2026 came in at 0.8%, a touch below the 0.9% that NAB and the broader consensus had forecast. On the surface, it looked like progress. But the number landed on 29 April 2026 into a market already reshaped by a fuel price shock that the quarterly data barely captured. Headline CPI has surged to 4.6% year-on-year, automotive fuel recorded its largest monthly jump since records began, and three of Australia’s four major banks now expect the Reserve Bank of Australia (RBA) to raise the cash rate again in May. What follows breaks down what the numbers actually show, why the quarterly result is less reassuring than it appears, and what a potential rate hike would mean for mortgages, rents, and household bills across Australia.

The Q1 2026 trimmed mean of 0.8% quarter-on-quarter brought the annual rate to 3.5% year-on-year. That quarterly reading sat 0.1 percentage points below the RBA’s February 2026 Statement on Monetary Policy (SoMP) forecast and below both NAB’s and the consensus call of 0.9%.

The undershoot, however, was not broad-based. It was concentrated in volatile components:

Roughly two-thirds of the CPI basket was still rising at an annualised rate above 3% during Q1 2026, a signal that inflation remains widespread despite the headline undershoot.

That breadth matters more than the quarterly print. A result dragged lower by airfares tells the RBA very little about whether rents, insurance, and services costs are moderating. On that count, the answer is: they are not.

The monthly CPI indicator for March 2026 accelerated to 4.6% year-on-year, up sharply from 3.7% in February 2026. The Middle East conflict involving Iran was the primary driver, sending fuel costs surging through the Australian economy faster than most forecasters anticipated.

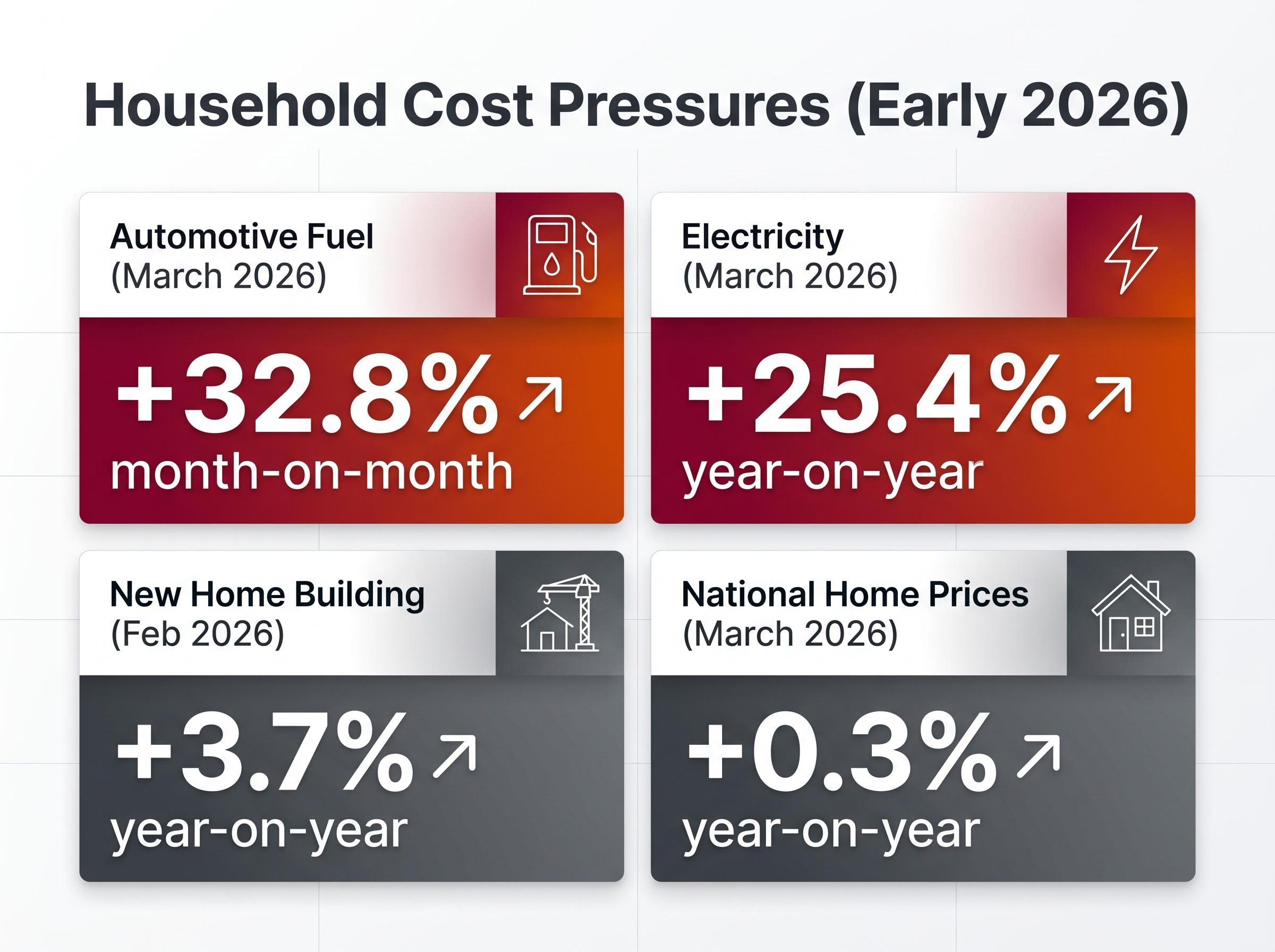

Automotive fuel rose 32.8% month-on-month in March, the largest monthly increase since the Australian Bureau of Statistics began tracking the series in 2017. That figure preceded the fuel excise relief that commenced in April.

The ASX sector repricing triggered by the oil shock extends well beyond the energy names; passive index investors carry concentrated exposure to financials and materials, two sectors facing distinct but material headwinds from higher rates and elevated freight costs respectively.

The monthly trimmed mean held at 3.3% year-on-year, in line with forecasts, though the monthly pace edged up to 0.3% from 0.2%. NAB had forecast a headline monthly reading of 4.7%; the broader consensus sat at 4.8%. The actual 4.6% came in marginally below both, but annualised underlying measures across one-month, three-month, and six-month windows all remained above 3%.

| Measure | February 2026 | March 2026 |

|---|---|---|

| Headline CPI (yoy) | 3.7% | 4.6% |

| Monthly trimmed mean (yoy) | 3.3% | 3.3% |

| Automotive fuel (mom) | — | 32.8% |

Fuel excise relief commenced in April 2026 and should lower Q2 headline CPI readings. Lower global oil prices may reinforce that moderation. But the pass-through of higher transport and energy costs into broader goods and services prices is already under way. Businesses have absorbed higher freight, packaging, and logistics costs over March, and those repricing decisions will not reverse because the excise has been reduced.

The headline CPI reads 4.6%. The trimmed mean reads 3.3%. The RBA pays closer attention to the second number. Understanding why requires knowing what the trimmed mean actually does.

Trimmed mean CPI removes the most extreme price movements from the basket, both the sharpest rises and the sharpest falls, to produce a cleaner reading of underlying price pressure. It strips out one-off distortions so policymakers can see whether inflation is broad and persistent or concentrated and temporary.

The RBA’s trimmed mean methodology removes the most extreme price movements from both ends of the CPI basket to isolate persistent underlying inflation, which is why the measure sits at the centre of the Board’s monetary policy deliberations rather than the more volatile headline figure.

The difference matters right now because of what each measure includes:

The RBA targets inflation of 2-3% year-on-year. At 3.3%, the trimmed mean sits above the top of that band. At 4.6%, headline CPI sits well above it. Both readings concern the central bank, but the trimmed mean is the more durable signal.

For readers wanting to build a firmer foundation before tracking the RBA’s next move, our dedicated guide to CPI and trimmed mean inflation walks through how the ABS constructs each measure, why the trimmed mean strips out volatile items like fuel, and what the RBA’s 2-3% target band actually requires in practice.

Core inflation was already tracking at approximately 3.5% before the oil price shock began, an unfavourable starting position for the RBA heading into the crisis, according to NAB analysis.

That pre-shock baseline is the detail that makes the quarterly undershoot less comforting than it appears. The RBA was not dealing with a controlled descent toward target; it was managing sticky domestic inflation that then absorbed an energy shock on top.

Three of Australia’s four major banks have converged on the same call: a 25 basis point increase at the RBA’s May 2026 meeting, lifting the cash rate from 4.10% to 4.35%. The current rate already reflects the 25bp hike delivered in March 2026.

| Bank | May 2026 forecast | Cash rate post-hike |

|---|---|---|

| CBA | 25bp hike | 4.35% |

| NAB | 25bp hike | 4.35% |

| Westpac | 25bp hike | 4.35% |

| ANZ | ~60% probability of hike | 4.35% (if hiked) |

CBA has described the May decision as finely balanced, reflecting the tension between elevated inflation and weakening consumer and business sentiment. NAB has flagged upside risk beyond May if secondary pass-through from energy prices proves broader than expected, forecasting rates on hold through mid-to-late 2027 after the hike. ANZ remains the outlier at approximately 60% probability, a less certain call that leaves meaningful room for a hold.

ASX 30 Day Interbank Cash Rate Futures, which derive an implied probability of rate changes from the pricing of short-term interest rate contracts, showed approximately 72% probability of a May hike as of late April 2026. That figure reflects the collective positioning of institutional traders and is a real-time gauge of market expectations. A 72% reading implies the market leans toward a hike but has not priced it as a certainty; incoming data between now and the meeting could shift that pricing in either direction.

A 25bp hike adds directly to the monthly repayment burden for every borrower on a variable-rate mortgage. On a $600,000 loan, the cumulative effect of the March and potential May increases would add several hundred dollars per month to repayments compared to the rate environment of late 2025.

Housing cost pressures extend well beyond mortgages:

Electricity prices rose 25.4% year-on-year in March 2026, the sharpest increase since the Energy Bill Relief Fund subsidies expired in January.

National home prices rose 0.3% in March 2026 according to PropTrack. For households navigating higher mortgage repayments, rent renewals, and energy bills simultaneously, the cumulative effect of these pressures is compounding faster than wage growth can offset.

Investors wanting to convert the household cost picture into concrete portfolio decisions will find our comprehensive walkthrough of ASX portfolio positioning during inflation, which covers cash ETFs such as ISEC and AAA that benefit directly from higher rates, quality equity selections with demonstrated pricing power, and the case against reactive selling when CPI headlines spike.

The Q1 data captured only the opening phase of the oil shock. The more complex, slower-moving effects are still working through the supply chain. Second-round pass-through follows a predictable pathway:

The RBA’s February 2026 SoMP projections did not incorporate the Middle East conflict escalation. That means the central bank’s own forecasting framework is operating with outdated assumptions. NAB has characterised the 3.5% core inflation reading prior to the shock as an unfavourable starting position, noting that broad and rapid secondary-round transmission poses particular risk in new dwelling construction, transport-dependent goods, and oil-derived product categories.

Counterbalancing the shock-driven upside are structural deflationary forces including AI-driven productivity gains, frozen global housing markets, and a wave of discounted Chinese manufactured goods, forces that commercial bank forecasts for the cash rate reaching 4.85% by August 2026 may not fully account for.

The April excise relief and lower global oil prices should moderate Q2 headline CPI readings. But the RBA focuses on trimmed mean inflation, which the excise cut will affect less directly. The question the Board will weigh in May is whether temporary headline relief is sufficient to offset the underlying momentum in core prices that were already running above target before the shock arrived. The research suggests the answer is no.

The quarterly trimmed mean came in below forecasts. In isolation, that would be welcome. In the context of a 4.6% headline reading, a fuel shock still transmitting through supply chains, and an RBA forecasting framework built before the conflict escalated, it offers limited reassurance.

Three of four major banks expect a hike. Market pricing leans the same way at 72%. The path ahead depends on whether second-round pass-through broadens or fades, and that answer will not arrive before the May meeting.

For borrowers and households, three practical steps are worth considering:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding RBA policy and inflation projections are subject to change based on incoming data and market developments.

Trimmed mean inflation removes the most extreme price movements from both ends of the CPI basket to produce a cleaner reading of underlying price pressure, stripping out one-off distortions like fuel spikes. The RBA targets this measure rather than headline CPI because it better reflects whether inflation is broad and persistent, and it currently sits at 3.3% year-on-year, above the RBA's 2-3% target band.

As of March 2026, Australia's headline CPI inflation rate is 4.6% year-on-year, up sharply from 3.7% in February 2026, driven largely by a 32.8% monthly surge in automotive fuel costs linked to Middle East conflict. The trimmed mean, which the RBA monitors most closely, sits at 3.3% year-on-year.

Three of Australia's four major banks, CBA, NAB, and Westpac, are forecasting a 25 basis point rate hike at the May 2026 RBA meeting, which would lift the cash rate from 4.10% to 4.35%. ASX 30 Day Interbank Cash Rate Futures showed approximately 72% probability of a hike as of late April 2026, with ANZ the only major bank assigning less certainty at around 60%.

A 25 basis point hike would increase monthly repayments on a variable-rate mortgage, and on a $600,000 loan the cumulative effect of both the March and potential May increases would add several hundred dollars per month compared to the rate environment of late 2025. Borrowers are advised to review whether a variable or fixed rate structure best suits their current exposure.

The Q1 2026 trimmed mean came in at 0.8% quarter-on-quarter, just below the 0.9% consensus forecast, but the undershoot was concentrated in volatile items like airfares rather than reflecting broad easing across the basket. Roughly two-thirds of the CPI basket was still rising at an annualised rate above 3%, and core inflation was already tracking around 3.5% before the oil price shock began.