Australia’s headline inflation rate reached 4.6% in the March 2026 quarter, well above the Reserve Bank of Australia’s (RBA) 2-3% target band. The RBA has already raised the cash rate twice this year in response. Yet most people reading those headlines have only a vague sense of what inflation actually is, why it keeps climbing, and what rate hikes are supposed to do about it.

Inflation is one of the most consequential forces in any economy, shaping mortgage repayments, grocery bills, wage negotiations, and investment returns simultaneously. With Australia navigating a re-acceleration of price pressures driven by both domestic demand and an external oil shock from the 2026 Iran conflict, understanding the mechanics behind the headlines has rarely been more practically useful. This guide explains what inflation is and what causes it, how Australia measures and targets it, why central banks find it so difficult to manage, and what the current environment means for everyday Australians.

What inflation actually is, and why the number on your screen matters

A year ago, the weekly grocery shop cost less. So did filling the car. The dollar amount on the receipt has changed, but the items in the basket have not. That gap between what money used to buy and what it buys now is inflation at its most tangible: a sustained rise in the general price level that makes each dollar worth progressively less over time.

The distinction between a genuine inflationary trend and a one-off price jump matters more than most headlines suggest.

- What inflation is: A broad, persistent increase in prices across the basket of goods and services an economy consumes, sustained over multiple quarters or years.

- What inflation is not: A one-off spike in a single category (a cyclone destroying banana crops), a seasonal price swing (airfares over school holidays), or a relative price shift where one good becomes more expensive while another falls.

Moderate, stable inflation is not a failure of economic management. Virtually all advanced economies target approximately 2% annual inflation as the optimal rate, because mild price growth encourages spending and investment rather than hoarding cash, supports wage adjustments, and gives central banks room to cut rates during downturns. The RBA’s 2-3% target band has been in place since 1993, formalised in the 1996 Statement on the Conduct of Monetary Policy.

Research from the International Monetary Fund indicates that each additional percentage point of inflation above 3% in a developed economy typically reduces real GDP growth by roughly 0.1-0.2 percentage points.

Understanding why the target is 2-3% rather than zero is the conceptual foundation for everything that follows. Zero inflation carries its own risks: it discourages borrowing, delays consumption, and leaves central banks with fewer tools in a recession. The policy objective is always a balancing act, not simply a campaign to minimise prices.

When big ASX news breaks, our subscribers know first

Three forces that push prices up: demand, supply, and expectations

Not all inflation arrives the same way, and the cause determines whether the standard policy response will work.

Demand-pull inflation occurs when spending outpaces an economy’s productive capacity. Consumers and businesses compete for a limited pool of goods and services, and prices rise to ration what is available. Australia’s current environment fits this pattern in part: strong private demand and a tight labour market have kept spending elevated. The RBA has characterised the economy as “further from balance” due to demand running ahead of supply.

Cost-push inflation operates from the supply side. When the cost of producing goods rises, whether through energy prices, raw materials, or wages, businesses pass those costs through to consumers. The 2026 Iran conflict has pushed oil prices above $150 per barrel, contributing directly to the acceleration in headline Consumer Price Index (CPI) from 3.6% in the December 2025 quarter to 4.6% in the March 2026 quarter. This is cost-push pressure operating in real time.

A fourth channel worth noting is currency depreciation, which raises the cost of imports for a trade-exposed economy like Australia, amplifying cost-push dynamics.

The Iran conflict’s oil shock is recalibrating global inflation expectations well beyond Australia, with central banks across advanced economies reassessing rate paths as energy costs filter through logistics, manufacturing, and retail price-setting in ways that domestic monetary policy cannot directly address.

| Type | Cause | Current Australian example | Policy effectiveness |

|---|---|---|---|

| Demand-pull | Spending exceeds productive capacity | Strong private demand, tight labour market | High: rate hikes directly cool demand |

| Cost-push | Rising input costs passed to consumers | Oil above $150/barrel from Iran conflict | Low: rate hikes do not reduce oil prices |

| Built-in (expectations) | Wage-price spiral from entrenched expectations | RBA concern over persistent services inflation | Moderate: depends on credibility of central bank commitment |

The distinction between demand-pull and cost-push matters enormously. Interest rate increases are a precise tool against demand-side inflation; they are a blunt and painful tool against supply-side shocks, because higher rates cannot produce more oil or repair disrupted supply chains. Knowing which type Australia is facing helps in evaluating whether the RBA’s current tightening is well-targeted or risks overtightening into a supply problem.

When expectations become the problem

The third force, built-in inflation, is the one central bankers fear most. The mechanism is self-reinforcing: workers anticipate further price rises, negotiate higher wages to protect their purchasing power, businesses absorb those wage costs and pass them through as higher prices, and the cycle repeats.

This is why central banks act early and decisively. Once inflation expectations become unanchored, as they did during the 1970s oil supply shocks, a second wave of inflation becomes nearly unavoidable without a severe policy response. The RBA has explicitly flagged tight labour markets and persistent services inflation as risks of this dynamic developing in Australia through 2026.

How Australia measures inflation, and what the RBA is actually targeting

The inflation figures that appear in headlines are the product of a specific institutional process. Understanding that process makes the numbers far more interpretable.

The Australian Bureau of Statistics (ABS) compiles the CPI by tracking price changes across a weighted basket of goods and services designed to reflect typical household spending. Categories include housing, food, transport, health, education, recreation, and more, with the basket periodically updated to reflect evolving spending patterns. The CPI is published quarterly.

Two versions of this data shape policy decisions:

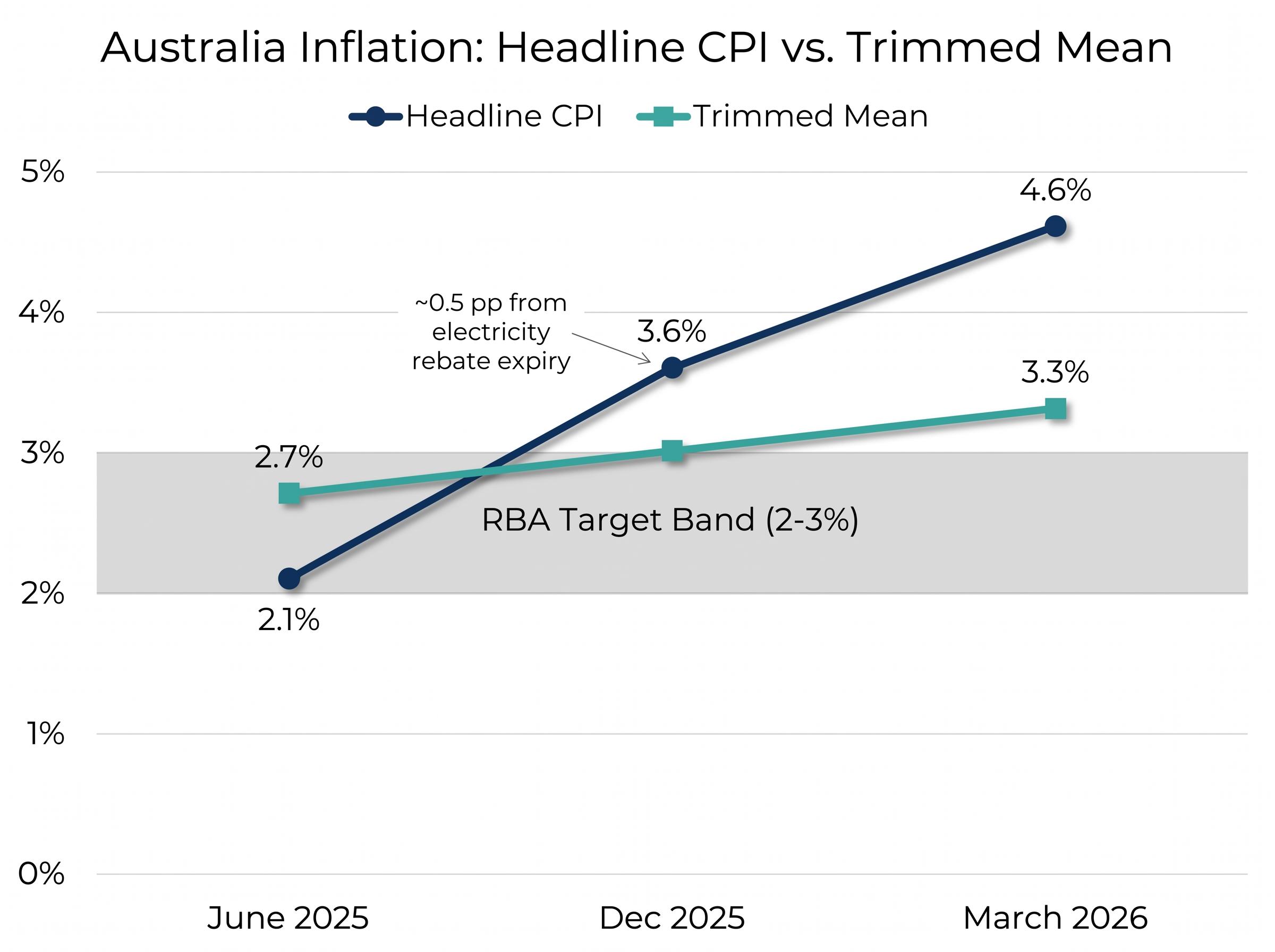

- Headline CPI captures price changes across the full basket, including volatile items such as fuel, fruit, and vegetables. It reflects what households actually experience at the checkout.

- Trimmed mean (underlying inflation) strips out the most volatile price movements at both ends of the distribution, removing the statistical noise of one-off spikes and dips to reveal the persistent, underlying trend in prices. This is the measure the RBA watches most closely for policy decisions, because it filters out temporary disruptions that would distort the signal.

The ABS methodology for underlying inflation measures explains how the trimmed mean is constructed by removing a fixed proportion of price changes at both extremes of the distribution each quarter, a process designed to isolate the persistent component of inflation from transitory shocks like fuel or fruit price spikes.

The practical difference matters right now. In the March 2026 quarter, headline CPI hit 4.6% year-ended while trimmed mean sat at 3.3%. The gap reflects the outsized contribution of fuel prices (driven by the Iran conflict) to the headline figure, a volatile item that the trimmed mean process partially strips out. For contrast, in the June 2025 quarter, headline CPI was just 2.1% while trimmed mean was 2.7%, both within or near the target band. The December 2025 quarter also illustrated this dynamic: approximately 0.5 percentage points of the headline CPI acceleration came from the expiry of electricity rebates, a one-off policy effect the RBA looks through when setting rates.

The RBA’s 2-3% inflation target, in place since 1993, is a band rather than a point. “Over time” means the RBA does not sacrifice employment to hit the midpoint immediately. The institution’s dual mandate encompasses both price stability and full employment.

Australians who understand the difference between headline and underlying inflation will not misread a temporary fuel-price surge as evidence of entrenched inflation, and will better interpret RBA communications about when and why it expects to ease policy.

Why managing inflation is harder than it looks: the central bank tightrope

The RBA’s primary tool for managing inflation is the cash rate. The transmission mechanism operates through a chain of consequences:

- The RBA raises the cash rate.

- Commercial borrowing costs rise across the economy (mortgages, business loans, credit cards).

- Higher borrowing costs discourage spending and investment.

- Reduced demand eases pressure on prices.

- Inflation gradually falls.

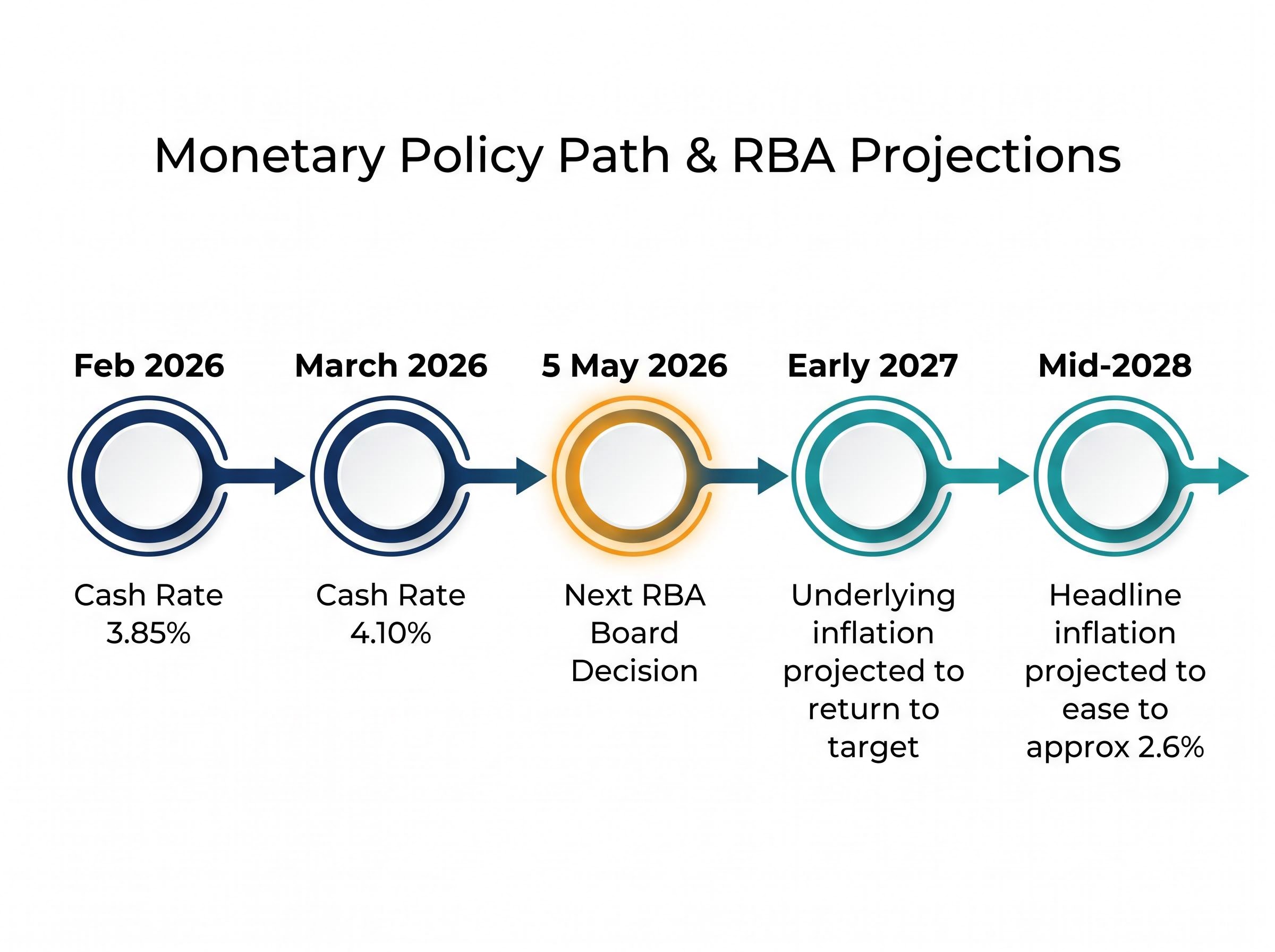

Each step involves a lag. Monetary policy operates with a delay of 12-18 months, meaning the RBA is always making decisions based on conditions that have already passed and forecasts that may prove wrong. The rate is currently at 4.10%, effective since the March 2026 board meeting, the second increase of the year following a move to 3.85% in February 2026.

The Taylor Rule, a widely referenced framework in monetary economics, suggests that central banks must raise rates by approximately 1.5 percentage points for every 1 percentage point of inflation above target to genuinely tighten financial conditions. Below that threshold, the rate increase is not restrictive enough to slow demand.

Peer-reviewed monetary policy rules research on rate-setting thresholds formalises the 1.5x coefficient, confirming that central banks must raise nominal rates by more than the inflation overshoot itself to achieve genuinely restrictive financial conditions, a principle that sits at the core of debates about whether the RBA’s current tightening pace is sufficient.

The historical record makes the difficulty vivid. Between 1980 and 1982, the US Federal Reserve under Paul Volcker raised rates aggressively to break entrenched inflation. It worked: inflation fell from approximately 14% to around 3%. The cost was severe. Unemployment exceeded 10%, and the economy endured a deep recession. The inflation was defeated, but the collateral damage was enormous.

The rare soft landing and why it is so hard to repeat

A soft landing describes the outcome where inflation returns to target without triggering a recession or a significant spike in unemployment. The 1990s US expansion is the benchmark example, achieved through gradual rate normalisation and a fortunate supply-side tailwind from technology-driven productivity gains.

Soft landings are historically rare. Australia’s current conditions make one harder to engineer: the RBA is managing an unusual combination of demand-side pressure (strong private spending, tight labour markets) and a supply-side shock (the oil price surge). The February 2026 Statement on Monetary Policy’s characterisation of “more persistent economy-wide capacity pressures” tempers optimism. The RBA is walking the narrow path between sustained above-target inflation and undermining economic growth.

How persistent inflation reshapes household finances for Australians

The macro statistics translate into specific financial pressures for Australian households. With headline CPI at 4.6% year-ended in the March 2026 quarter, the real-world effects are already visible across several channels:

- Purchasing power: Wages must rise at least as fast as prices to prevent a decline in living standards. When inflation runs at 4.6% and wage growth trails that figure, every pay cheque buys less in real terms.

- Mortgage costs: RBA rate increases directly raise variable mortgage repayments for the approximately one-third of Australian households carrying a mortgage. At a cash rate of 4.10%, repayment burdens are materially higher than they were a year ago.

- Fuel and energy: The Iran war oil shock, with prices above $150 per barrel, has pushed up fuel and transport costs. These expenses disproportionately burden lower-income households, who spend a larger share of income on transport and utilities.

- Savings erosion: Inflation reduces the real value of cash holdings and fixed-income payments such as pensions or benefits. A savings account earning 3% while inflation runs at 4.6% is losing purchasing power in real terms.

- Employment risk: Higher input costs squeeze business margins, potentially leading to reduced hiring, fewer hours, or deferred investment, creating a secondary link between inflation and labour market outcomes.

The practical mechanism of inflation wealth erosion is most visible in fixed-income holdings: a term deposit earning 3% annually loses real value at an accelerating rate when CPI runs at 4.6%, quietly compounding the gap between nominal and real returns across every quarter the rate differential persists.

The RBA’s February 2026 Statement on Monetary Policy projects underlying inflation remaining above the 2-3% target until early 2027, with headline inflation easing to approximately 2.6% by mid-2028. The next RBA board decision is scheduled for 5 May 2026.

Translating these projections into household terms: the period of above-average price growth is not expected to resolve quickly. Wage growth, mortgage structure, and savings allocation all warrant review in this context.

Navigating ahead: what comes after a period of high inflation

Supply-driven oil price shocks have a characteristic shape in the historical record. They tend to lift inflation and interest rates sharply in the short term, but growth concerns typically dominate within 6-12 months as higher energy costs cool household and business spending. Rate reversals have historically followed within that timeframe.

Several disinflationary forces are already operating in the background alongside the current inflationary pressures:

- AI-driven productivity gains, which could reduce unit labour costs across service industries over time.

- Softening wage growth in some sectors, as higher rates begin to cool demand for labour.

- Chinese export price competition, redirecting lower-cost manufactured goods into global markets and applying downward pressure on traded goods prices.

Oil futures are currently in backwardation, meaning near-term contracts are priced above longer-dated ones. This structure signals that market participants view the current supply disruption as temporary rather than structural, a reading with direct implications for how long cost-push inflation persists.

The RBA has adopted explicitly “data-dependent” language from its March 2026 board decision, signalling that the policy path from here will be determined by incoming data rather than a pre-set trajectory. The 5 May 2026 board meeting is the next observable checkpoint.

The February 2026 Statement on Monetary Policy projects underlying inflation above the 2-3% target until early 2027. That timeline could compress if the oil shock proves shorter than feared, or extend if expectations begin to drift upward. Understanding that inflation episodes have characteristic shapes and typical resolution timelines helps in distinguishing between short-term volatility and structural shifts.

Negative real returns on cash are not a theoretical concern in the current environment: with the RBA cash rate at 4.10% and headline CPI at 4.6%, even competitive savings accounts are delivering a loss in purchasing power terms, a gap that compounds meaningfully across the 12-18 month window the RBA projects before inflation returns to the target band.

The tightrope does not break often, but the stakes are real

Inflation is not one thing but a set of interacting forces, and the RBA’s cash rate is a blunt instrument applied to a complex system. Australia is managing an unusual combination of demand-side and supply-side pressure simultaneously, with the inflation return to target pushed out to early 2027 at the earliest for underlying measures and mid-2028 for the headline figure.

Knowing the mechanics behind the headlines, what CPI and trimmed mean actually measure, why demand-pull and cost-push inflation require different responses, and why soft landings are rare, equips readers to interpret future RBA decisions, inflation data releases, and cost-of-living changes with more confidence and less noise.

The next observable data points to watch are the RBA board decision on 5 May 2026 and the quarterly CPI releases from the ABS. Both will shape the trajectory of rates, prices, and the cost of living for the remainder of the year.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Financial projections referenced in this article, including RBA forecasts, are subject to market conditions and various risk factors. Past performance does not guarantee future results.