A 3-Layer Portfolio Strategy for Volatile ASX Markets

1 min ago

Celsius Holdings delivered 117% consolidated revenue growth in Q4 2025, yet the stock sits near its 52-week low. Dutch Bros grew revenue 29% the same quarter and trades up roughly 13% year-to-date in 2026. That divergence, where the faster-growing company is the worse-performing stock, is precisely what makes the comparison between these two consumer growth names worth unpacking.

Both CELH and BROS are growth-stage consumer plays commanding multi-billion-dollar market caps in a market that has selectively rewarded beverage and quick-service brands. But they are structured differently, growing differently, and priced differently. A side-by-side scan of headline multiples does not capture what is actually happening inside each business. This analysis breaks down what is driving performance at each company as of 30 April 2026, where the valuation maths stands, and which stock presents the more compelling risk-adjusted opportunity for investors with a two-to-three year horizon.

On the surface, the resemblance is close enough to invite comparison. Celsius Holdings carries a market capitalisation of approximately US$8.4 billion at a share price near US$33-35. Dutch Bros sits at approximately US$9.43 billion with shares at roughly US$55.62. Both companies crossed or are approaching the US$2 billion revenue threshold. Both are growth-stage names in the consumer space.

The similarity ends there.

| Metric | Celsius (CELH) | Dutch Bros (BROS) |

|---|---|---|

| Market Cap | ~US$8.4B | ~US$9.43B |

| Current Price | ~US$33-35 | ~US$55.62 |

| 52-Week Range | US$32.30-$66.74 | N/A |

| YTD / 1-Year Return | ~-6.6% (1-year) | ~+13% (YTD 2026) |

| Revenue Scale (TTM) | ~US$2.52B | Guiding US$2.0B-$2.03B for 2026 |

Celsius is a branded consumer packaged goods (CPG) play. It sells canned energy drinks through grocery, convenience, and distribution channels. Its value is concentrated in brand equity, shelf-space positioning, and the direct store delivery (DSD) networks that get product onto shelves.

Dutch Bros is a physical footprint expansion story. It monetises drive-through coffee locations and depends on customer frequency, same-store sales growth, and disciplined unit economics as the store count scales. Every metric that follows should be read through this structural distinction.

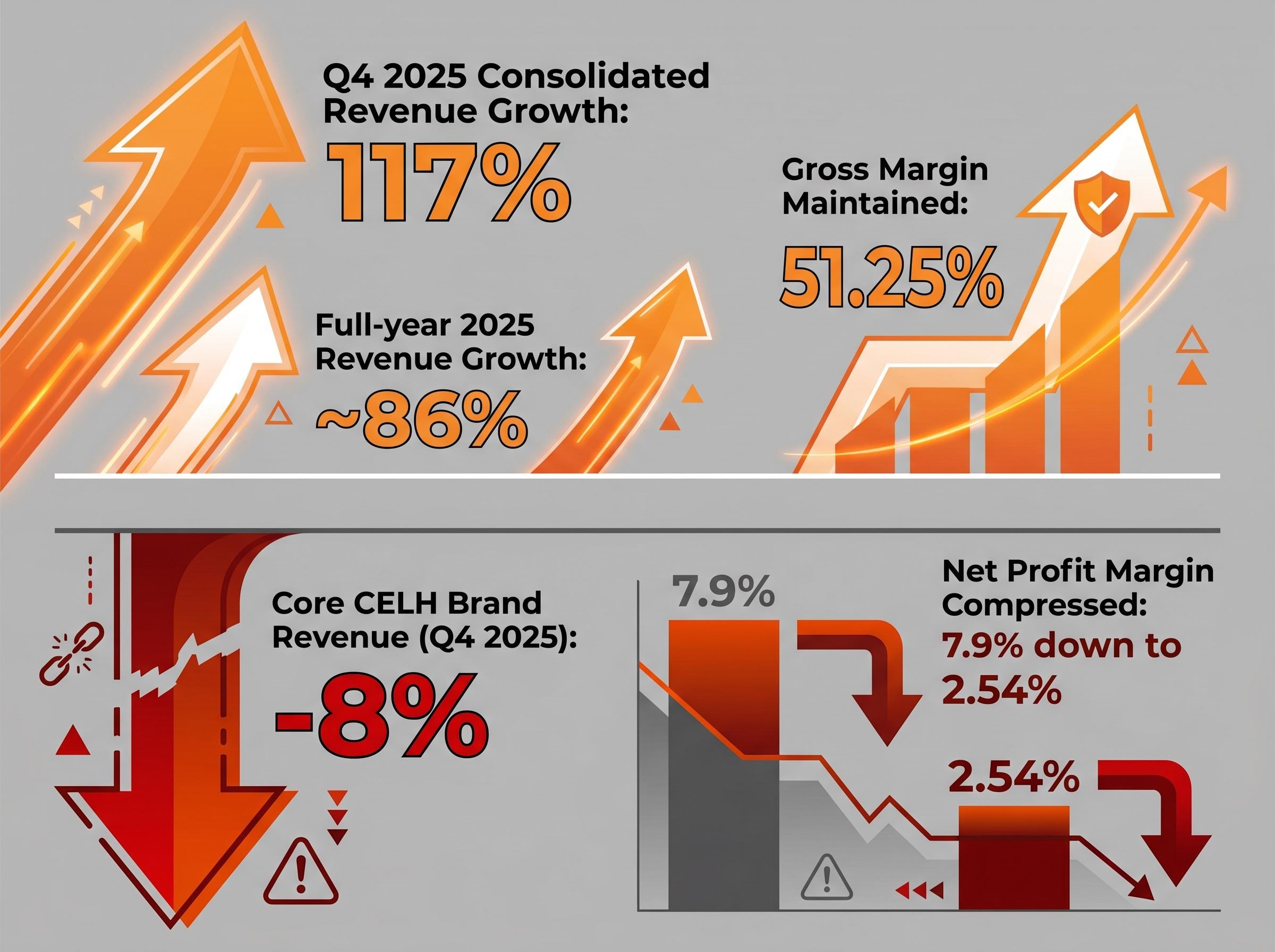

The headline number demands attention: 117% consolidated revenue growth in Q4 2025. Full-year 2025 revenue rose approximately 86%, pushing trailing twelve-month revenue to roughly US$2.52 billion. Q4 earnings per share came in at US$0.26, beating analyst estimates of US$0.21.

Then the decomposition arrives.

The growth was driven overwhelmingly by the Alani Nu acquisition, a fitness-oriented beverage brand Celsius acquired in 2025 that expanded the combined portfolio’s energy drink market share to approximately 20%. The three components of the 86% full-year growth story break down as follows:

The Celsius Holdings Alani Nu acquisition announcement, published at deal close in April 2025, confirmed a net purchase price of approximately US$1.65 billion, paid through a mix of cash and stock, with the stated strategic rationale of combining two complementary brands to capture a larger share of the functional beverage category.

The core Celsius brand, the original thesis, saw revenue fall roughly 8% in Q4 2025. The headline growth rate and the underlying brand trajectory are moving in opposite directions.

That gap is the single most important question a CELH investor must answer. An investor who cannot separate the acquisition-driven headline from the underlying brand performance is flying blind on the most material risk in the thesis.

Net profit margin compressed from 7.9% to 2.54% following the acquisition, reflecting integration costs, DSD transition expenses, and one-off items. Gross margin held at 51.25%, which suggests the underlying unit economics remain intact even as the bottom line absorbed acquisition-related friction.

Gross margin held at 51.25%, which suggests the underlying unit economics remain intact, but the Alani Nu integration costs absorbed at the net margin level reflect a pattern common to acquisitive CPG growth strategies: headline gross economics look clean while below-the-line friction obscures the true run-rate earnings picture until integration is complete.

Wall Street’s consensus projection of approximately 55% EPS growth from 2026 to 2028 assumes margin recovery, integration completion, and DSD leverage kicking in as one-off costs roll off. Medium-term earnings growth is forecast at approximately 29.55% annually. The bull case requires all three assumptions to hold simultaneously.

Functional beverages occupy a structurally attractive but concentration-prone category. For investors less familiar with consumer staples dynamics, the competitive mechanics here explain why distribution infrastructure can matter more than brand alone.

Three structural features define the category:

Celsius holds approximately 25.8% dollar share by some measurement methodologies, behind Monster but ahead of Red Bull at roughly 19.1%. The company is expanding into Australasia and European territories as an international growth vector, while product diversification into zero-sugar, still beverages, and new flavours serves as both a defensive and offensive strategy.

C-Store Dive energy drink market share data, citing a Goldman Sachs report from April 2026, places Celsius at approximately 25.8% dollar share and Red Bull at 19.1%, figures that situate Celsius as the number two player in a category where Monster retains the leading position.

In the five years preceding its peak, CELH stock appreciated approximately 7,330%. The stock now trades near its 52-week low of US$32.30, a reminder that backward-looking performance tells investors nothing about the path forward.

The Dutch Bros growth story reads as a clean compounding machine. Q4 2025 revenue grew 29% year-over-year, entirely organic. Full-year 2025 same-shop sales rose 5.6% system-wide and 7.4% at company-operated locations, marking 11 consecutive quarters of positive same-store sales comps. Net income grew approximately 76% year-over-year.

The store count trajectory is the structural engine. From 671 locations three years ago to approximately 1,136 today, Dutch Bros is targeting at least 181 new openings in 2026, with a medium-term goal of 2,029 stores by 2029 and a long-term domestic ceiling estimated at 7,000 shops.

The unit-level economics underpinning that store count trajectory have shifted materially over the past two years: Dutch Bros reduced its average capital expenditure per shop to approximately US$1.3 million by Q4 2025, with a long-term target of US$1.25 million, and its build-to-suit real estate model limits upfront cash drag while maintaining a 28.9% company-operated contribution margin.

| Year | Store Count | Milestone |

|---|---|---|

| ~2023 | 671 | Baseline |

| Current (2026) | ~1,136 | 181+ new openings targeted in 2026 |

| 2029 Target | 2,029 | Medium-term expansion goal |

| Long-Term Ceiling | ~7,000 | Estimated domestic saturation |

Three near-term revenue catalysts support the guidance of US$2.0 billion-$2.03 billion for 2026:

The cleanliness of this story commands a premium. BROS trades at approximately 35x forward earnings, and the analyst consensus target of US$75.52 implies roughly 36% upside from the current price, with a Moderate Buy rating. The question is whether that premium leaves enough margin for error if same-store sales decelerate below the guided range.

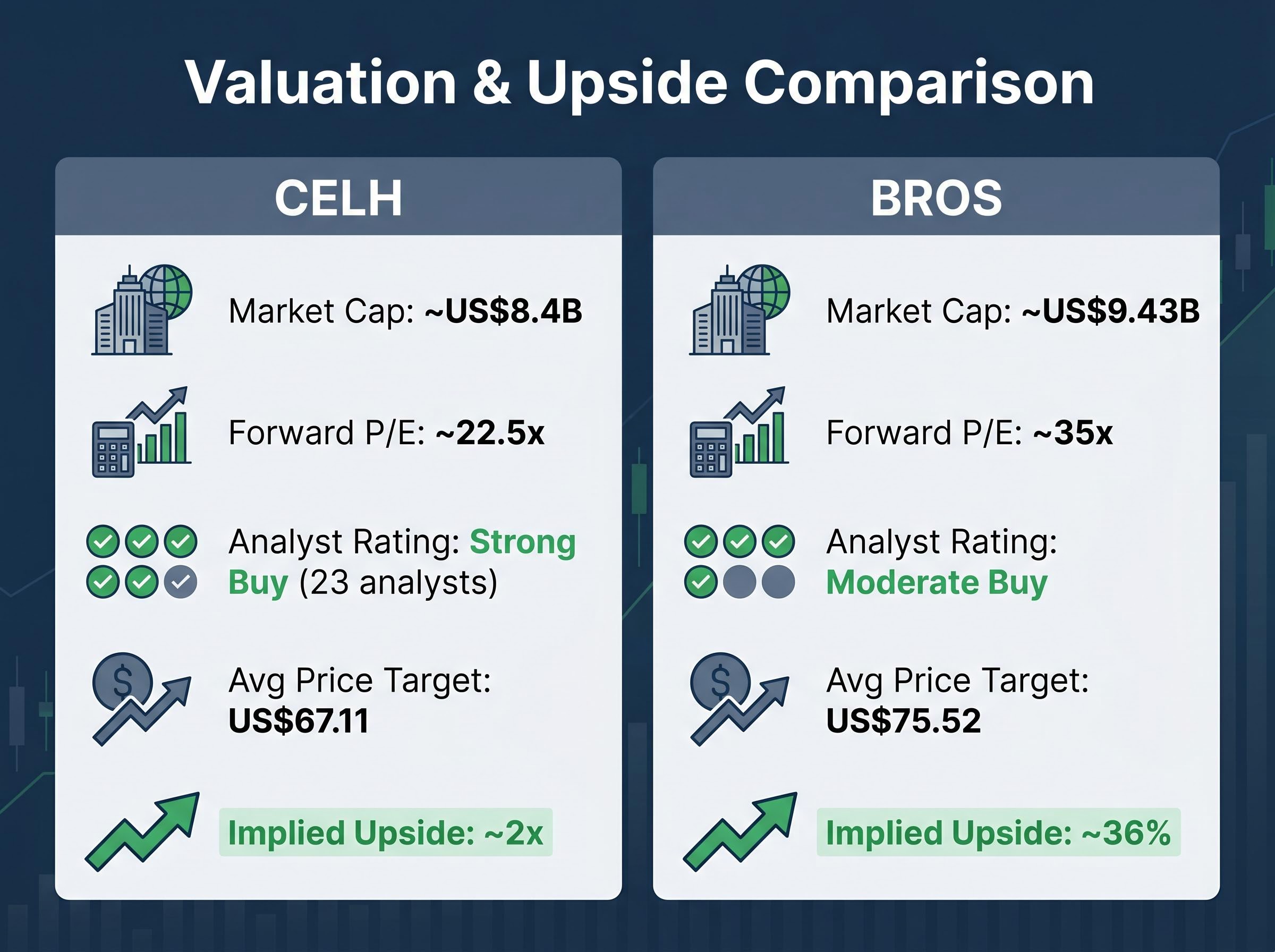

The forward price-to-earnings gap frames the entire decision. CELH trades at approximately 22.5x forward earnings. BROS trades at approximately 35x. That 12.5-turn spread reflects a specific market judgement: investors are willing to pay a substantial premium for Dutch Bros’s execution predictability, while Celsius is discounted for the margin recovery optionality that has not yet been demonstrated post-acquisition.

| Metric | CELH | BROS |

|---|---|---|

| Forward P/E | ~22.5x | ~35x |

| Analyst Rating | Strong Buy (23 analysts) | Moderate Buy |

| Avg Price Target | US$67.11 | US$75.52 |

| Implied Upside | ~2x from current price | ~36% |

| Key Valuation Risk | Margin recovery must materialise | Premium demands sustained comps |

The 23-analyst consensus price target of US$67.11 for Celsius implies the stock could roughly double from its current level near US$33-35. Simply Wall St estimates CELH trades approximately 63.3% below fair value on forward earnings growth assumptions. That gap captures how much pessimism is priced in, and how much has to go right for the market to close it.

The trailing P/E tells the other side. At approximately 131.3x trailing earnings, CELH is not cheap by any backward-looking measure. The entire bull case is a forward earnings recovery story. Investors choosing Celsius over Dutch Bros are betting on a compression of that trailing-to-forward P/E gap, which requires the 55% EPS growth consensus to materialise on schedule.

The EPS growth consensus of approximately 55% from 2026 to 2028 embeds aggressive synergy realisation assumptions across both the core Celsius brand and the Alani Nu portfolio, and the degree to which those synergies are back-loaded versus front-loaded materially changes the year-by-year earnings path that investors are actually paying for at today’s multiple.

The comparison sharpens when framed not as “which stock is better” but as “what does each stock need to be true.”

The CELH bull case requires four conditions:

The BROS bull case requires three conditions:

Celsius offers the greater analyst-implied upside, roughly 2x to the consensus target versus 36% for Dutch Bros. But the CELH thesis demands more variables to resolve correctly, and the stock’s -6.6% one-year return against a +29.1% broader US market suggests the market is not yet convinced those variables will break favourably.

Dutch Bros is the higher-conviction execution story. Eleven consecutive quarters of positive same-store sales comps, a disciplined expansion cadence, and improving margins present a cleaner operational track record. The trade-off is a 35x forward multiple that leaves less room for error if comps disappoint or the expansion encounters friction.

Neither stock is a straightforward allocation at current prices without a clear view on the specific risk conditions above.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The analytical tension is durable, not resolvable with a single verdict. Celsius is the cheaper stock on forward multiples with substantially more analyst-implied upside, but the thesis requires a clean execution cycle that has not yet been demonstrated since the Alani Nu acquisition closed. Dutch Bros is the more expensive stock with the cleaner operational track record and a more legible compounding path.

The specific data points to monitor heading into mid-2026 earnings season:

Celsius (CELH):

Dutch Bros (BROS):

The right choice between these two stocks depends less on which company is “better” and more on which set of risks an investor is willing to underwrite at the price the market is offering today.

Celsius Holdings is a branded consumer packaged goods company selling energy drinks through retail distribution channels, while Dutch Bros is a physical drive-through coffee chain growing through store count expansion. The two businesses have fundamentally different growth mechanics, cost structures, and valuation profiles.

The 117% revenue growth in Q4 2025 was driven primarily by the Alani Nu acquisition rather than organic brand performance; the core Celsius brand actually declined approximately 8% in Q4 2025. Investors are discounting the stock for margin compression and execution risk tied to the integration, not the headline growth figure.

Celsius carries a 23-analyst consensus price target of US$67.11, implying roughly 2x upside from its current price near US$33-35, while Dutch Bros has a consensus target of US$75.52, implying approximately 36% upside. Celsius offers greater implied upside but also requires more execution variables to resolve correctly.

Dutch Bros is targeting at least 181 new store openings in 2026, aiming to reach 2,029 locations by 2029 from approximately 1,136 today, with a long-term domestic ceiling estimated at around 7,000 shops. The company has reduced its average capital expenditure per new shop to approximately US$1.3 million to support this expansion.

The CELH bull case requires core brand volume to stabilise after the Q4 2025 decline, successful integration of Alani Nu without further margin deterioration, net margin recovery as one-off acquisition costs roll off, and meaningful contribution from international expansion into Australasia and Europe by 2027-2028.