Lululemon Fundamental Analysis: the Price of Brand Dilution

2 hrs ago

The contrast in global advanced air mobility is striking this week. In China, eHang recently executed a 16-aircraft formation flight to mark the Spring Festival, while final pre-launch preparations for passenger transit are actively underway in Dubai. As of late April 2026, the sector has decisively transitioned from theoretical engineering to live commercial operations and complex regulatory finalisation. Evaluating the commercial viability of leading electric vertical takeoff and landing stocks requires looking past the prototype phase to assess the mechanics of entering commercial airspace. These eVTOL stocks represent a highly capital-intensive sector where the gap between a successful test flight and a profitable transit network is measured in billions of dollars. Investors must break down operational timelines, specific revenue models, and fundamental financial health to identify the aerospace developers capable of surviving the regulatory gauntlet.

The commercial reality of advanced air mobility is materialising first outside the United States. Showing where operations are actively commencing helps investors separate companies generating real-world flight data from those still confined to domestic testing facilities. Leading American players have strategically targeted the Middle East for their first revenue flights, seeking supportive regulatory environments to prove their operational models. Localised geopolitical risks in the region could still impact these planned 2026 launch schedules, forcing operators to maintain flexible deployment strategies. The distinct operational status across key global markets reveals a clear geographic divide in early adoption.

China: eHang secured its Production Certificate in 2024 and its Air Operator Certificate in 2025, which cleared the EH216-S for tourist flights. The company executed a highly publicised 16-aircraft formation flight during the Q1 2026 Spring Festival, successfully establishing active commercial tourist operations. Dubai: Joby Aviation is in the final stages of launching imminent commercial passenger transit. The launch is considered weeks away as of early April 2026, positioning the company to capture first-mover advantage in the region. * Abu Dhabi: Archer Aviation has achieved 100% Federal Aviation Administration (FAA) compliance for its planned regional operations. The company is heavily targeting 2026 for its inaugural revenue flights in the United Arab Emirates.

The CAAC issuance of Air Operator Certificates established a critical regulatory precedent for civil human-carrying pilotless vehicles, providing a blueprint for other international aviation authorities evaluating autonomous flight models.

The global race to launch is only one component of sector viability. Companies are competing with fundamentally different business models that directly dictate their cash burn rates and paths to positive cash flow. This structural distinction provides the specific commercial framework investors need to evaluate which corporate strategy offers the most resilient path to long-term profitability. Understanding how these companies plan to generate revenue separates vertically integrated operators from pure-play manufacturers.

Some developers are building direct-to-consumer operational frameworks, attempting to control both the vehicle manufacturing and the consumer ride-sharing network. Others function as traditional vehicle manufacturers, relying on legacy aerospace suppliers to build aircraft for third-party logistics operators. Furthermore, diversified income streams from charging infrastructure and logistics networks provide alternative paths to profitability for companies unwilling to rely entirely on passenger transit. A company’s chosen structural model determines its capital requirements over the next decade.

Advancements in commercial drone edge-AI chips are also reshaping these supply chains, as manufacturers look to integrate highly efficient silicon that dramatically extends battery endurance for autonomous cargo delivery.

| Company | Core Manufacturing Approach | Primary Revenue Model | Strategic Partners |

|---|---|---|---|

| Joby Aviation | Proprietary manufacturing | Direct-to-consumer mobility network | |

| Beta Technologies | Diversified systems | Cargo logistics, CCS-1 universal power stations | Undisclosed private backers |

| Eve Holding | Third-party integration | Aircraft sales, Vector airspace management |

Regulatory approval represents the ultimate binary hurdle for this emerging sector. Walk through aviation certification friction points and the gap between test flight optimism and strict safety mandates becomes immediately clear. Understanding exact certification timelines allows investors to accurately gauge when domestic commercial revenue can actually begin in Western markets. The stark reality is that no United States manufacturer holds full FAA Type Certification as of late April 2026.

Market leaders pushed through significant late-stage testing barriers early this year, but the regulatory backlog remains substantial. Early 2026 estimates assigned only a 20% to 30% probability of developers remaining on their initial schedules. Industry consensus now points to mid-2027 as the most realistic target for final FAA certification, requiring companies to fund an additional year of pre-revenue operations.

Key regulatory milestones achieved in the first quarter of 2026 highlight the gradual pace of progression:

Highlighting past failures protects portfolios from engineering hype. Without exceptional capital reserves, even the most promising aerospace engineering cannot survive the prolonged certification timeline. The high cost of entry fundamentally altered the industry structure through massive financial attrition during 2024 and 2025.

The collapse of major European developers effectively consolidated global market share for the surviving American and Chinese firms. Volocopter filed for insolvency in December 2024, ceasing operations despite remaining initially bullish on achieving a 2025 certification. Similarly, Lilium shut down entirely in February 2025 after failing to secure a critical financial rescue package from government and private backers. These high-profile bankruptcies underscore the necessity of massive cash reserves to bridge the multi-year gap between prototype testing and commercial operations.

Market Consolidation Insight Capital markets tightened strictly around clear certification winners in 2025, effectively starving mid-tier developers of the funds required to reach commercialisation and forcing widespread industry consolidation.

Surviving developers must demonstrate fortified balance sheets to weather the regulatory waiting period. Joby maintained a strong liquidity position of approximately $1.4 billion at the end of 2025. This war chest provides the necessary runway to absorb ongoing certification delays without requiring immediate, highly dilutive capital raises.

For readers wanting to compare the specific liquidity buffers across the sector, our deep-dive into eVTOL stock cash runways examines how vertically integrated networks and specialized fabricators are managing their capital burn profiles ahead of certification.

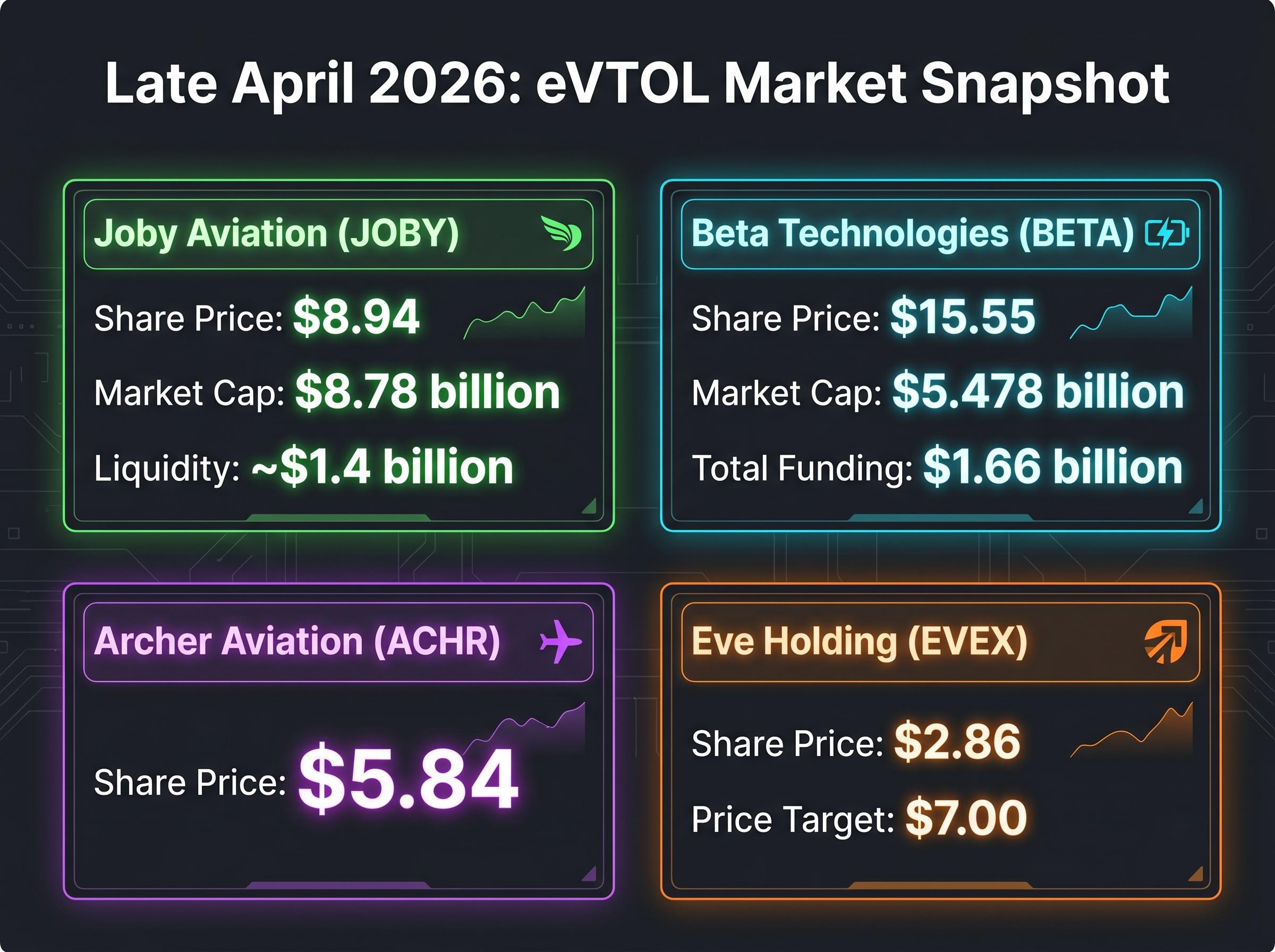

Translating operational and regulatory realities into actionable commercial intelligence requires examining the raw financial metrics. Comparing the current market capitalisations and share prices of the dominant publicly traded developers reveals how the market is pricing survival probability. Investors must evaluate these leaders side by side to understand where institutional capital is flowing.

Beta Technologies made a highly successful transition to public markets following massive private funding rounds. The company is currently trading at $15.55 with a $5.478 billion market capitalisation, supported by total funding of $1.66 billion. This strong debut demonstrates that institutional capital remains available for developers with diversified business models and sufficient runway. Conversely, earlier-stage developers without confirmed cash buffers are experiencing significant downward pressure on their valuations.

The company’s unique cargo logistics strategy significantly lowers its early reliance on passenger transit regulations; this diversified business model is a key reason institutional investors continue to back their long-term vision.

| Company | Late April 2026 Share Price | Market Capitalisation | Liquidity Position |

|---|---|---|---|

| Joby Aviation (JOBY) | $8.94 | $8.78 billion | ~$1.4 billion |

| Beta Technologies (BETA) | $15.55 | $5.478 billion | Not disclosed |

| Archer Aviation (ACHR) | $5.84 | Not disclosed | Not disclosed |

| Eve Holding (EVEX) | $2.86 | Not disclosed | Not disclosed |

Wall Street sentiment shows a clear preference for companies demonstrating strong balance sheets and advanced certification progress. Analysts widely favour Joby over Archer for the 2026 fiscal year due to its superior cash reserves and domestic regulatory lead. This institutional preference is reflected in the historical stock performance, with Joby being viewed as the superior pick after realising 330% gains since 2023.

Broader sector momentum was also visible early in the year, with a pronounced January Effect boosting stocks across the board. Joby saw a 20% increase at the beginning of 2026, while Archer gained 14% during the same period. Eve Holding also maintains positive analyst coverage, holding a $7.00 price target aggregated from multiple institutional analysts, indicating continued support for developers partnered with legacy aerospace manufacturers.

The intersection of imminent Middle Eastern commercial launches and ongoing FAA progress defines the 2026 landscape for electric aviation. While international operations provide vital early revenue, the domestic American market remains gated by strict certification timelines that will likely extend into 2027. Capital survival will ultimately separate the commercial winners from the engineering prototypes, as the cost of compliance continues to drain mid-tier competitors.

Investors should approach this sector defensively, prioritising companies with the billion-dollar balance sheets required to outlast regulatory delays while capturing the long-term upside of urban mobility.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Investors must assess operational timelines, specific revenue models, and the fundamental financial health of aerospace developers, moving beyond the prototype phase to commercial viability.

Commercial operations are materializing first in regions like China and the Middle East due to more supportive regulatory environments, allowing companies to prove operational models and gather real-world flight data.

No US manufacturer holds full FAA Type Certification as of April 2026, with industry consensus pointing to mid-2027 for final approval, requiring companies to fund additional years of pre-revenue operations.

Joby Aviation maintains a strong liquidity position of approximately $1.4 billion at the end of 2025, providing the necessary capital to absorb ongoing certification delays without requiring immediate, dilutive raises.