Lululemon Fundamental Analysis: the Price of Brand Dilution

2 hrs ago

The evaluation of eVTOL stocks has shifted dramatically in early 2026, moving from speculative technological forecasts to rigorous commercial analysis. As the sector transitions from theoretical testing to live passenger flights, major electric aviation companies are posting significant year-to-date gains. Performance data from late April 2026 highlights this momentum, with Beta Technologies up 44.88% and Joby Aviation returning 37.43%.

Investors are bracing for the imminent May 2026 first-quarter earnings reports. The financial stakes are underpinned by massive global market projections. Industry forecasts suggest the sector will surge from $5.13 billion in 2026 to $216.02 billion by 2035.

Market participants must look beyond the novelty of flying vehicles to understand the underlying balance sheets. What follows is a comparative framework to evaluate which operational strategy offers the most viable path to profitability.

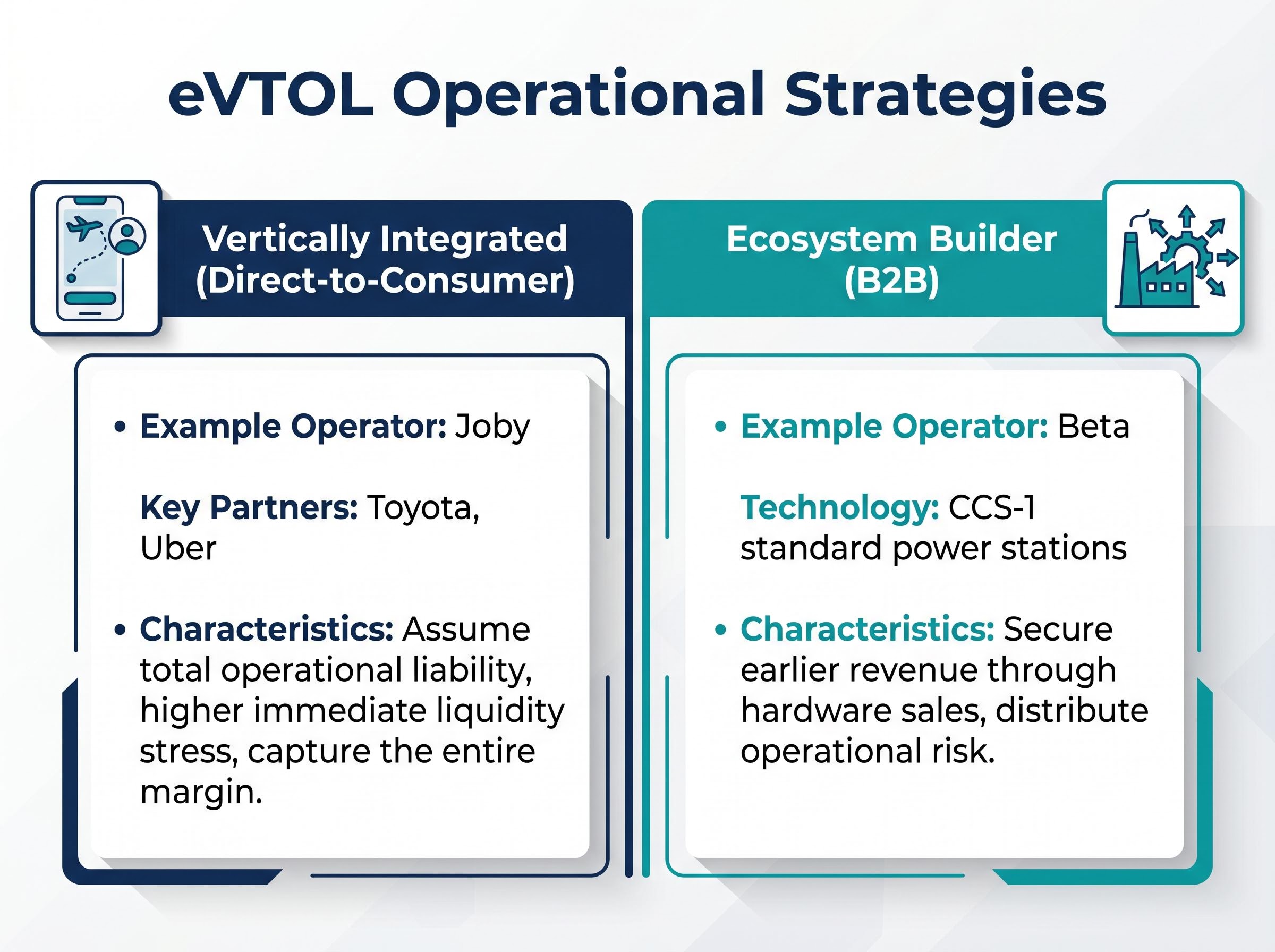

The commercial viability of electric vertical takeoff and landing companies rests entirely on their foundational business models. Two distinct operational strategies have emerged, dictating long-term capital requirements and certification timelines. Investors must grasp these differences before committing capital to the sector.

The vertically integrated, direct-to-consumer approach requires companies to control the entire value chain. These entities manufacture the aircraft, build the consumer application, and operate the ride-sharing network themselves. Joby exemplifies this strategy, building proprietary components utilising Toyota manufacturing expertise while establishing a dedicated mobility network alongside Uber.

Conversely, the ecosystem builder model focuses on business-to-business transactions. These manufacturers operate as traditional aerospace suppliers, selling hardware and infrastructure to third-party operators. Beta operates under this framework, constructing universal power stations that utilise CCS-1 standards to accommodate multiple aircraft brands.

These foundational choices drastically alter cash burn rates, regulatory pathways, and timeline risk. The core distinctions between the two models include:

Direct-to-consumer operators: Assume total operational liability and face higher immediate liquidity stress, but capture the entire margin of the end-user fare. Business-to-business manufacturers: Secure earlier revenue through hardware sales, distribute operational risk to established partners, and avoid the massive overhead of managing public flight networks.

For readers wanting to model these specific financial pressures, our full explainer on eVTOL cash runways examines recent sector capital raises and details how varying strategic frameworks directly alter certification timeline risk.

Vertically integrated operators currently dominate the United States market and maintain a significant regulatory lead. Capturing the highest market valuations, these companies offer massive upside if they can successfully execute their end-to-end vision. Joby currently leads this cohort with a market capitalisation of approximately $8.95 billion.

This ambition carries a heavy immediate liquidity stress. Funding simultaneous aircraft certification and consumer network deployment requires tremendous capital expenditure. Joby has demonstrated operational progress, achieving Federal Aviation Administration testing under Type Inspection Authorization in early 2026.

The company also completed a successful flight of its conforming aircraft on 11 March 2026.

This crucial phase of Joby’s FAA-conforming aircraft flight testing generates the empirical safety data required by regulators before approving final commercial deployment.

Variations on this integrated model are emerging to eventually lower operating overhead. Boeing and its Wisk subsidiary serve as a prime example of an autonomous operational framework, pursuing pilotless vehicles to reduce long-term personnel costs. However, achieving these savings requires even greater upfront capital to secure autonomous regulatory approval.

Investors holding these integrated operators face substantial dilution risk if additional capital raises are required before sustained revenue generation.

Wall Street Analyst Consensus on Sector Liquidity “Vertically integrated business-to-consumer models face higher immediate cash burn and elevated sector-wide liquidity stress. The capital-intensive nature of launching direct operations and independently navigating complex certification hurdles creates severe short-term financial pressure compared to hardware-only peers.”

The collaborative ecosystem model serves as the defensive investment play within the electric aviation sector. Business-to-business manufacturers reduce their cash burn by partnering with legacy aerospace suppliers and traditional logistics companies. This approach distributes capital requirements and mitigates early commercialisation risks.

Generating revenue through ancillary services creates a more stable financial foundation while passenger certification remains pending. Beta demonstrates the strength of this model, maintaining a $3.55-$3.57 billion market capitalisation through diverse income sources like propulsion mechanism sales. Strategic backing from established aerospace giants provides these newer entities with both credibility and shared engineering resources.

Similar diversification strategies are proving successful across broader electric mobility networks, where manufacturers leveraging last mile delivery partnerships and service-based models have achieved substantial annual sales growth.

Eve Air Mobility integrates third-party technologies from BAE Systems alongside its Vector airspace management platform. Backed heavily by Embraer, the company leverages traditional manufacturing infrastructure to reduce its proprietary research costs. Archer Aviation pursues a similar hardware acquisition strategy, purchasing critical flight components from legacy suppliers like Honeywell.

Diversified revenue streams protect share value during lengthy regulatory certification delays. The table below maps the three primary ecosystem operators against their corporate structures.

| Operator | Primary Revenue Stream | Key Legacy Partners | Market Capitalisation |

|---|---|---|---|

| Beta Technologies | Propulsion sales and logistics | Undisclosed logistics firms | $3.55B – $3.57B |

| Archer Aviation | Hardware integration | Honeywell | $4.35B – $4.38B |

| Eve Air Mobility | Vector airspace software | BAE Systems, Embraer | $0.96B – $0.99B |

Theoretical business models are now meeting the reality of live commercial operations. While North American regulatory hurdles command significant media attention, proactive commercial launches are occurring immediately across the Middle East and Asia. These regional markets are providing the earliest proof of concept for the underlying equities.

Specific timelines for infrastructure development are translating into inaugural passenger flights. Joby confirmed its operational progress in Dubai during late April, noting that initial routes from Dubai International Airport were active by February 2026. Archer is similarly preparing for its impending 2026 commercial launch in Abu Dhabi, with regional infrastructure actively under construction.

The Asian marketplace has already initiated operational consumer flights, led successfully by eHang in the Chinese market. This geographic shift forces investors to track where real-world revenue generation is happening first.

Operational execution in new territories carries novel forms of risk. International expansion introduces complexities entirely outside of domestic regulatory control. External variables can heavily impact deployment schedules, making regional stability a primary factor for revenue projections.

The push into these emerging international territories coincides with rapid technological advancements in the broader autonomous drone market, where companies are acquiring alternative navigation systems to maintain operations in structurally complex or geopolitically unstable environments.

Market analysts must price these geographical risks into current valuations. Regional instability poses a potential geopolitical threat to Middle Eastern launch schedules, reminding investors that crossing the regulatory finish line is only the first hurdle in global commercialisation.

The ultimate metric for sector success is surviving until 2030 without subjecting shareholders to severe dilution. As the upcoming May earnings reports approach, fundamental balance sheet strength remains the critical lens for evaluating these manufacturers. Recent share price divergence highlights how the market is actively penalising companies with opaque funding pathways.

Archer has experienced a recent three-month performance decline of 26.3%, contrasting sharply with the broader sector momentum. Conversely, strong cash projections are supporting the valuations of newly public entities. Analyst projections for Beta following its late 2025 initial public offering forecast liquid reserves by the end of 2026.

This projected cash buffer creates a resilient path to self-sustainability, allowing the company to aggressively expand its universal charging network while competitor aircraft face tighter financial constraints.

This strong capital position suggests Beta maintains adequate funding to avoid secondary stock offerings until achieving positive cash flow by 2030. Other operators are managing their cash runways against specific regulatory timelines. Vertical Aerospace has established a strict target to finalise initial British and European regulatory authorisations.

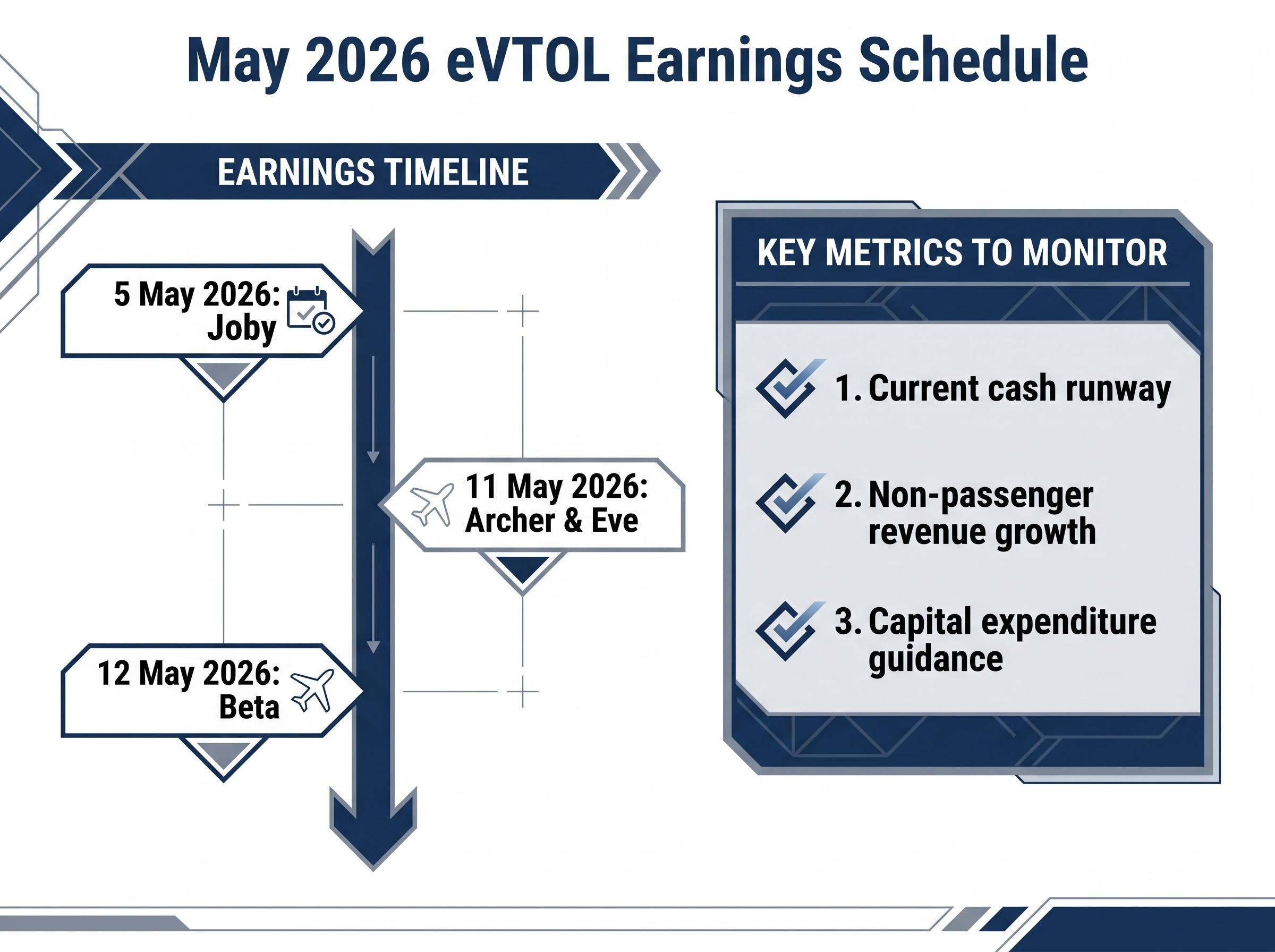

To manage a portfolio containing electric aviation equities over the next four years, investors should monitor three key financial metrics during the early May earnings calls:

The electric aviation market remains defined by the central tension between the high-reward vertically integrated model and the defensively diversified ecosystem approach. Immediate commercial success in the Middle East during 2026 will heavily influence market sentiment and dictate near-term valuations across the entire sector.

Investors must scrutinise the upcoming first-quarter liquidity figures as the ultimate indicator of operational sustainability. The release schedule demands immediate attention, with Joby reporting on 5 May 2026, Archer and Eve following on 11 May 2026, and Beta concluding on 12 May 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The two main models are vertically integrated, where companies control the entire value chain like manufacturing and operations, and ecosystem builders, who focus on business-to-business hardware and infrastructure sales.

Vertically integrated companies incur higher immediate cash burn and liquidity stress due to controlling the entire value chain, while ecosystem builders reduce cash burn and distribute risk by partnering with third parties.

Investors should monitor current cash runway, non-passenger revenue growth from hardware or logistics, and capital expenditure guidance, focusing on manufacturing versus research and development.

In early 2026, Beta Technologies was up 44.88% and Joby Aviation returned 37.43%, reflecting significant momentum in the sector.