Barclays Warns of Prolonged Market Volatility Under New Fed Reality

Jun 27, 2026

Recent Middle Eastern tensions have pushed WTI crude oil near $100 per barrel, colliding simultaneously with unprecedented deflationary waves driven by artificial intelligence productivity gains. Global financial markets in April 2026 are caught in a complex tug of war between immediate supply shock inflation and long-term structural deflation. This tension forces wealth accumulators to completely rethink their portfolio allocations to preserve purchasing power.

Implementing an effective inflation investing strategy requires bridging macroeconomic theory with practical capital deployment. Readers will master the foundational mechanics of monetary policy within this guide. The framework outlines how to strategically position wealth to capture elevated yields and acquire discounted global securities during periods of economic volatility.

Capital allocators must first evaluate the foundational drivers of cost escalation before adjusting portfolio weights. The optimal annual price appreciation objective for advanced nations sits near 2%. Moderate price appreciation encourages commercial expansion, whereas excessive escalation destroys economic output.

Primary triggers for upward cost adjustments include:

When input costs erode purchasing power, nominal returns can mask negative real wealth generation. The psychological component is particularly dangerous for economic stability. Anticipating future price hikes creates a self-perpetuating cycle where workers demand higher compensation, forcing businesses to raise prices further.

According to International Monetary Fund documentation, whenever cost growth exceeds target levels within developed jurisdictions, each incremental hike correlates with a contraction in inflation-adjusted gross domestic product.

This foundational knowledge prevents capital erosion during rapid economic shifts. Investors who understand these mechanics can recognise when their nominal returns are actually losing value in real terms.

For readers wanting to establish a stronger baseline, our full explainer on how inflation erodes household wealth details the exact mechanisms central banks use to suppress demand and the historical precedents that define modern policy trade-offs.

National monetary authorities adjust benchmark lending rates to either suppress societal consumption or stimulate financial liquidity. These adjustments act as blunt instruments, making borrowing more expensive to cool heated markets. Stabilising prices often requires inflicting deliberate economic pain on corporations and consumers alike.

To determine exactly how aggressively they must hike rates, central banks rely on mathematical frameworks. The most prominent of these frameworks dictates the precise relationship between cost escalation and interest rate responses.

According to economic theory, the Taylor Rule specifies elevating benchmark lending costs by roughly 1.5% for each 1% that actual cost growth exceeds designated targets.

Recent NBER research on the Taylor Rule validates this mathematical coefficient as the historical standard required to adequately cool overheated economies without triggering a disproportionate recession.

Understanding how central banks react to data empowers readers to anticipate interest rate movements. This foresight can provide a timing advantage before policy shifts are fully priced into the bond market.

Monetary authorities rely on historical data to shape their current interventions. According to historical records, during the early 1980s, United States monetary authorities compressed price growth from 14% down to 3%. This aggressive intervention achieved its primary objective but pushed domestic joblessness above 10%.

These historical lessons shaped the policy responses seen throughout 2022 and beyond. Modern central bankers understand that curing severe cost escalation inevitably causes collateral damage to the broader economy. Evaluating these precedents helps contextualise the tightrope global financial institutions walk today.

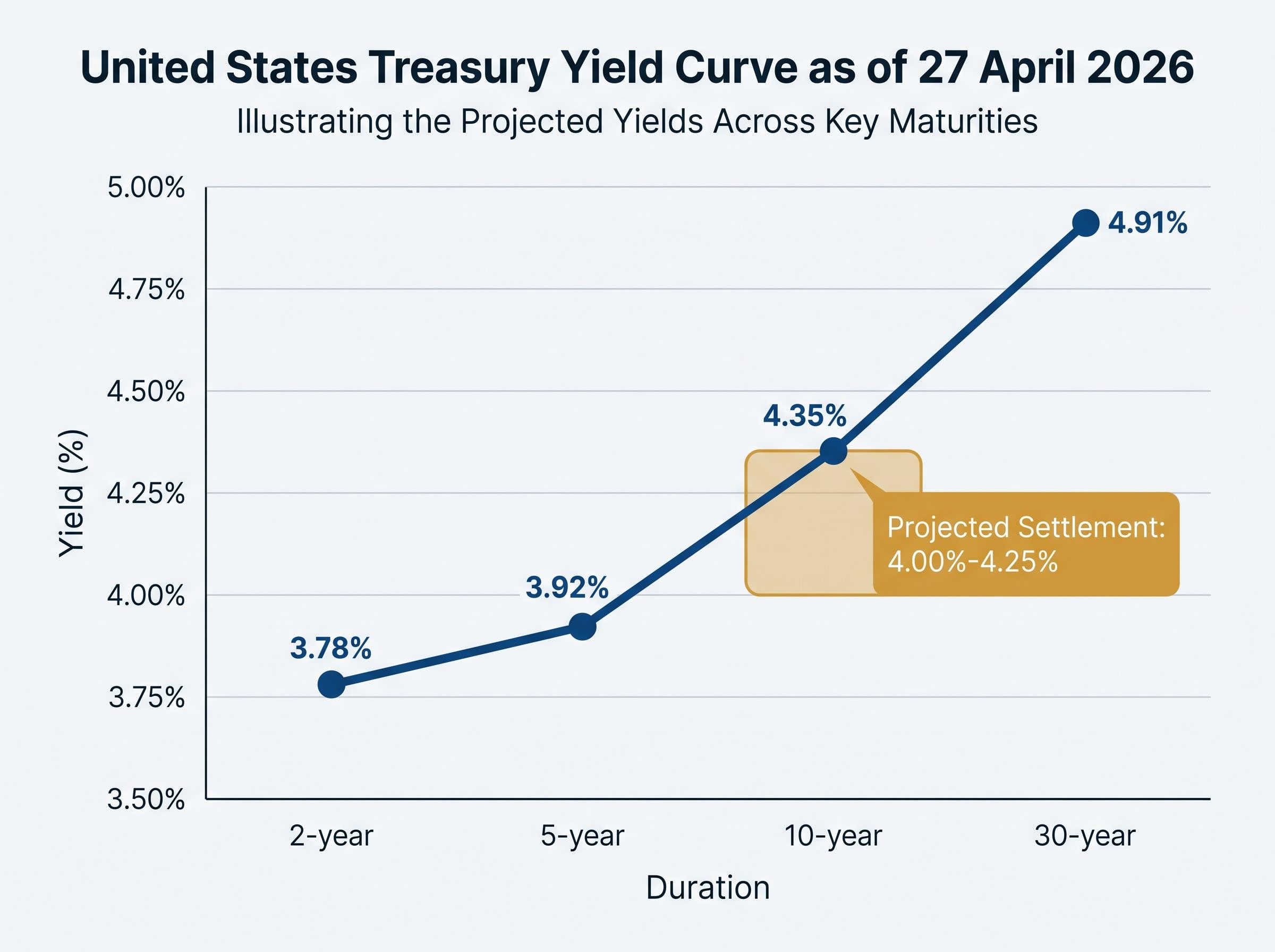

Late April 2026 Middle Eastern conflicts disrupted regional supply lines, driving energy shock severity significantly higher. WTI crude oil prices reached approximately $99.44 per barrel by 27 April 2026. This amplified energy pressure forced Treasury yields higher, overriding typical risk-off behaviours that usually accompany geopolitical stress.

The 10-year US Treasury yield increased to 4.35% in response to these commodity pressures. By grasping these opposing macroeconomic forces, investors can look past terrifying daily headlines to identify structural long-term trends that will dictate asset valuations into 2027.

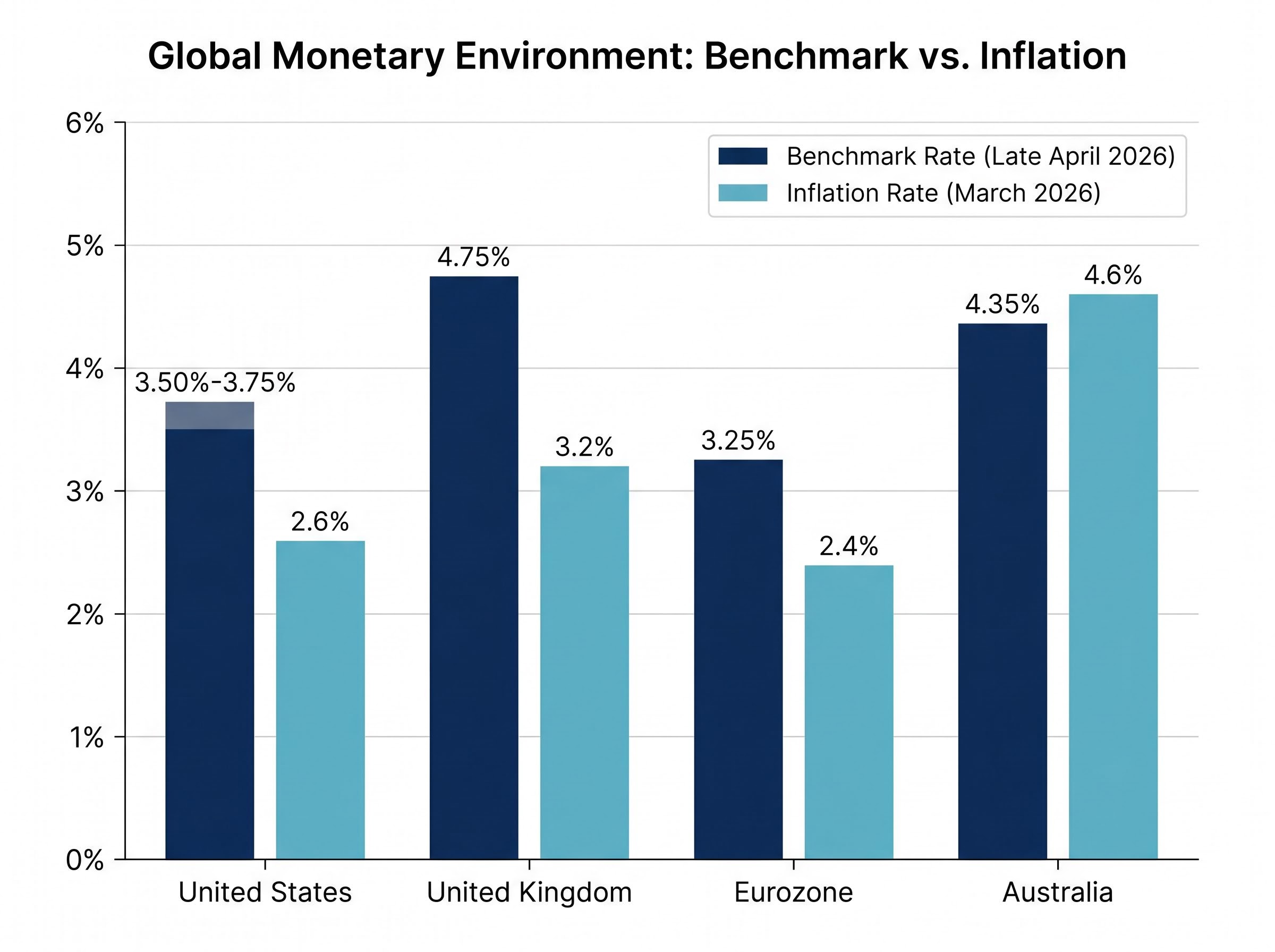

Major central banks are currently responding to these conflicting signals with varied benchmark rates. The global monetary environment remains fractured as different jurisdictions balance local inflation metrics against international pressures.

| Jurisdiction | Benchmark Rate (Late April 2026) | Inflation Rate (March 2026) |

|---|---|---|

| United States | **3.50%-3.75%** | **2.6%** (Core) |

| United Kingdom | **4.75%** | **3.2%** |

| Eurozone | **3.25%** | **2.4%** |

| Australia | **4.35%** | **4.6%** |

These immediate inflationary pressures collide directly with powerful deflationary forces. Massive productivity gains across sectors, driven by artificial intelligence, act as a structural deflationary counterbalance. Industry analyst Brian Stutland notes that these technological efficiencies are forcing economists to recalculate baseline growth models.

Recent Invesco analysis on tech-driven deflation suggests these automation tools could drastically reduce corporate labour expenses over the coming years, providing a persistent cap on aggregate price escalation.

Additionally, the International Monetary Fund’s April 2026 World Economic Outlook explicitly identifies the redirection of inexpensive Chinese manufacturing outputs as a deflationary crosscurrent. These efficiencies may eventually allow central banks to execute rate cuts once the immediate commodity pressures subside.

Fixed-income vehicles present increasingly appealing return profiles due to recent capital depreciation across the broader debt sector. When evaluating portfolios, readers must assess exactly where to find secure, elevated returns during periods of persistent rates. Higher yields offer a protective buffer against capital erosion while generating consistent portfolio income.

The United States yield curve currently offers distinct risk-reward propositions depending on the selected duration. As of 27 April 2026, the 2-year Treasury yields 3.78%, the 5-year yields 3.92%, the 10-year yields 4.35%, and the 30-year yields 4.91%. Financial forecasts project the 10-year Treasury will eventually settle in the 4.00%-4.25% range.

Concurrently, debt markets are pricing in 25 to 50 basis points of tightening for 2026 and 2027 in short-duration Treasuries and Canadian bonds. This pricing reflects lingering energy inflation risks.

Expert fixed-income positioning currently targets three primary areas:

Curve Strategy: The front end of the yield curve offers a superior risk-reward profile, while long-duration bonds carry elevated persistent inflation risks. Credit Opportunities: The intermediate segment features strong opportunities in higher-quality credit and securitised credit, with spreads projected to narrow over a 12-month horizon. * International Government Bonds: Select non-US government bonds from the United Kingdom, Australia, and New Zealand provide better value than US Treasuries, as those central banks possess more room for potential rate cuts.

Executing this fixed-income strategy provides vital stability when equity markets experience geopolitical turbulence.

Financial market turbulence presents strategic opportunities for disciplined wealth accumulators to acquire discounted securities. Volatility serves as a highly effective acquisition mechanism for investors targeting premium global assets. Transitioning from capital preservation to wealth generation requires purchasing highly rated equities when broad market anxiety suppresses their valuations.

However, identifying genuine discounts requires intense scrutiny when broader indices are mispricing geopolitical risk; some rapid market recoveries actively mask underlying fragilities in consumer spending and delayed supply chain inflation.

Selecting corporations with impeccable balance sheets and sufficient market dominance is critical during elevated cost environments. These dominant enterprises can pass elevated operational expenses directly to their customer base, protecting profit margins, while geographically distributed equity holdings diversify away from localised regional shocks.

The Vanguard MSCI Index International Shares ETF (VGS) demonstrates this defensive global posture by tracking premier global corporations. Vanguard reported a dividend yield of 1.6% for the fund in March 2026, with overall portfolio yields tracking around 2.50%. This income generation continues despite the fund’s daily total return year-to-date standing at a negative 2.41% amid global volatility.

A systematic wealth accumulation strategy requires structural discipline:

Applying this methodology helps portfolios acquire institutional-grade assets precisely when retail market participants are liquidating them.

The fundamental relationship between central bank interventions and commercial market performance will dictate capital returns over the coming decade. Geopolitical shocks, such as the April 2026 energy spike, generate intense immediate volatility and complicate monetary policy decisions. However, powerful structural deflationary forces offer genuine long-term hope for stabilised benchmark interest rates.

These volatile periods are rapidly reallocating investment capital across the economy, driving institutional funds toward discount retailers and technology infrastructure providers while punishing sectors burdened by volatile fuel margins.

Investors must look beyond temporary macroeconomic turbulence to construct genuinely resilient portfolios. Maintaining highly liquid capital reserves allows capital allocators to react strategically when exceptional market dislocations emerge. Readers should systematically accumulate diversified, high-quality fixed-income instruments and global equities regardless of short-term headline anxiety.

Balancing defensive yield generation with opportunistic equity acquisition creates a portfolio capable of absorbing inflation while capturing long-term growth.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Taylor Rule is an economic framework that guides central banks on how aggressively to adjust interest rates, typically suggesting a 1.5% rate hike for every 1% that inflation exceeds its target.

Investors can target the front end of the yield curve, seek opportunities in high-quality credit, and consider select non-US government bonds like those from the United Kingdom or Australia, which may offer better value for potential rate cuts.

Global markets in April 2026 are experiencing a conflict between immediate inflationary pressures, such as Middle Eastern geopolitical tensions driving oil prices, and long-term structural deflationary forces from artificial intelligence productivity gains.

AI-driven productivity gains are seen as deflationary because they can drastically reduce corporate labor expenses and improve operational efficiencies across various sectors, placing a persistent cap on aggregate price escalation.