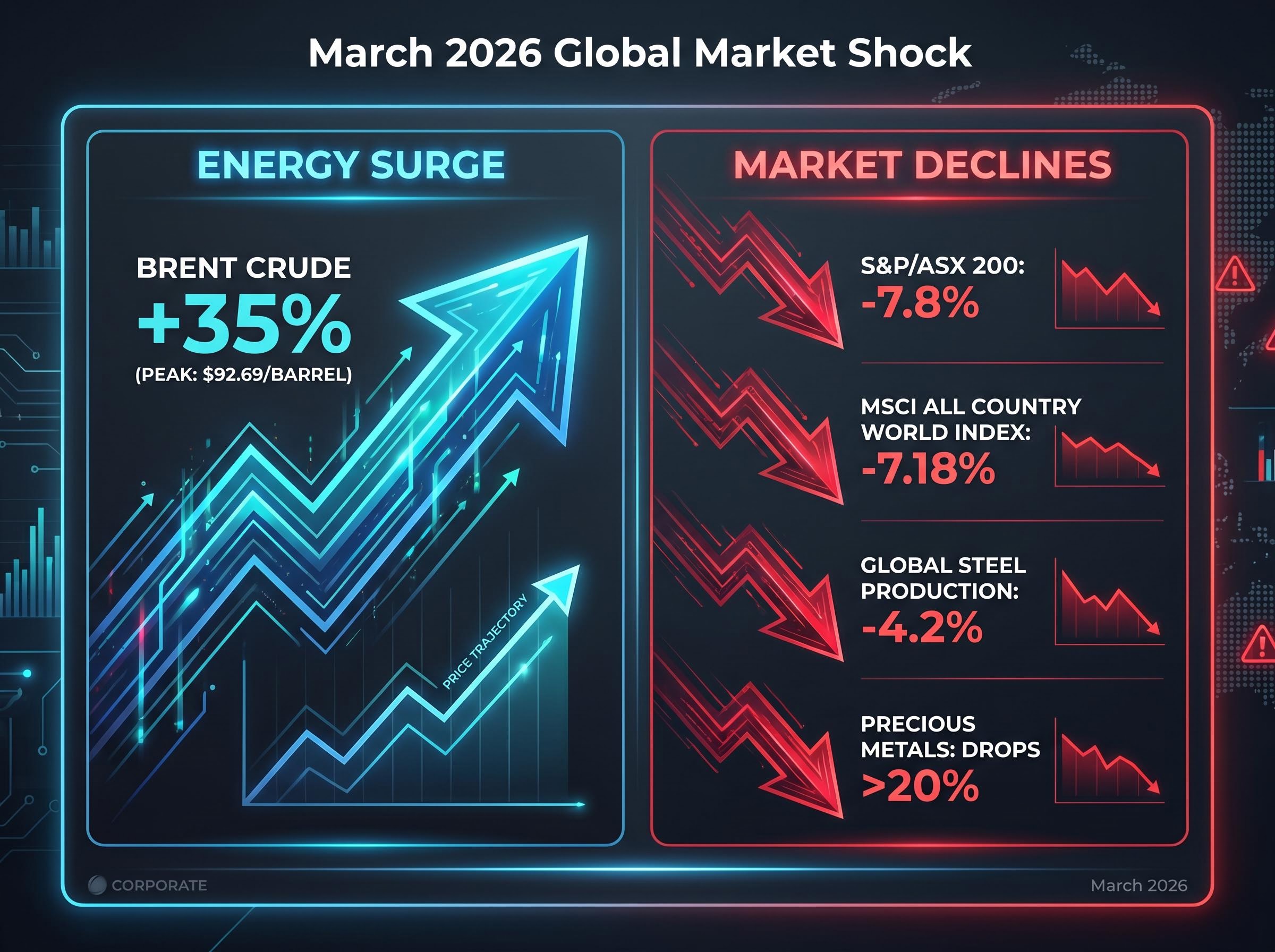

The extreme market volatility of early March 2026 forced a rapid reassessment of every major asset allocation strategy across the Australian market. Brent crude oil surged by 35%, dragging the S&P/ASX 200 down by 7.8% in a matter of weeks as supply chain fears gripped financial centres. As of late April 2026, the Reserve Bank of Australia (RBA) continues holding the cash rate steady at 4.10% amid the ongoing conflict in Iran and the heavily restricted Strait of Hormuz blockade. These compounding pressures leave many investors questioning how to position their capital safely. This guide cuts through the noise of geopolitical panic to help investors build a resilient, forward-looking portfolio. By evaluating current fixed income opportunities, understanding structural deflationary forces, and applying systematic equity approaches, market participants can navigate the complex crosscurrents effectively.

The Geopolitical Energy Shock and Global Volatility

The immediate catalyst for recent market instability stems from physical supply constraints in the Middle East. The blockade of the Strait of Hormuz severely muted global petroleum traffic, trapping millions of barrels away from international markets. When proposed ceasefire negotiations foundered in early April 2026, deep uncertainty permeated the fragile geopolitical environment, validating the intense anxiety felt across equity and commodity markets.

The sudden surge in crude prices is forcing a reassessment of global inflation trajectories, particularly as central banks demonstrate increasing policy divergence in response to persistent commodity supply constraints.

Brent crude peaked at $92.69 per barrel during the early March surge, driving severe operational challenges across the broader economy. Elevated energy costs cascaded through supply chains globally, forcing manufacturers to pass costs onto consumers or absorb margin compression. Consequently, global equities dropped 7.18% on the MSCI All Country World Index in March, while global steel production declined by 4.2% as heavy industries curtailed output.

These equity selloffs represent a natural reaction to rapid resource constraints rather than a permanent structural decline in corporate earnings power. Understanding the exact mechanisms behind these market drops helps separate temporary geopolitical panic from long-term fundamental weakness. This context prevents emotional selling at the bottom of a shock cycle.

The fallout created distinct pressure points across different investment categories:

Broad Australian Equities: Suffered heavily from the initial shock, reflecting the immediate repricing of energy inputs across major industrial and logistics sectors. Precious Metals: Entered a temporary bear market with drops exceeding 20% in some cases, as liquidity crunches forced broad asset sell-offs to cover margin calls. * The Mining Sector: Faced immediate operational margin compression due to an intense reliance on diesel fuels for heavy extraction machinery and transport.

Sector-Specific Impacts on the ASX

The resource-heavy Australian market absorbed the energy shock unevenly across its constituent companies. While large-cap diversified miners possessed the balance sheets to manage the immediate diesel price spike, smaller operators faced severe cash flow projections. Junior mining stocks fell particularly fast alongside the broader market pullback, reflecting their heightened sensitivity to short-term operational costs and limited hedging capabilities.

When big ASX news breaks, our subscribers know first

Why Artificial Intelligence and Structural Shifts Counter the Inflation Panic

While the Middle East conflict dominates immediate inflation concerns, powerful structural deflationary forces are operating quietly behind the headlines. Emerging technologies and shifting global supply chains indicate that the current inflation spike is likely transient rather than permanent. Historical data shows that interest rate increases triggered by sudden petroleum shortages typically reverse.

Artificial intelligence integration is increasingly recognised by analysts as a major disruptor, driving unprecedented productivity gains and supply chain optimisations across the global economy. These technology-driven efficiency improvements introduce a profound disinflationary impact that commercial markets are already pricing into forward estimates. Furthermore, the systematic shift of low-cost manufacturing away from China to alternative destinations acts as a secondary mitigating factor against regional supply shocks.

Recent BlackRock research on AI-driven deflation suggests these technology-led productivity gains act as a powerful growth engine capable of reducing systemic cost pressures across major global industries.

Industry Forecast on Technological Deflation According to recent industry analysis, the current technology-driven productivity boom could act as a significant disinflationary force, potentially offsetting broader inflationary pressures within a matter of months if alternative supply chains are optimised rapidly.

This dynamic is visible in the petroleum market through a pricing structure known as backwardation. When near-term futures contracts price higher than longer-dated ones, it signals that commercial traders expect the current pricing spike to resolve shortly. Buyers are willing to pay a premium for immediate delivery, but long-term expectations remain anchored. Betting entirely on sustained runaway inflation ignores these massive technological shifts that protect long-term purchasing power.

Rethinking Portfolio Defence for Modern Markets

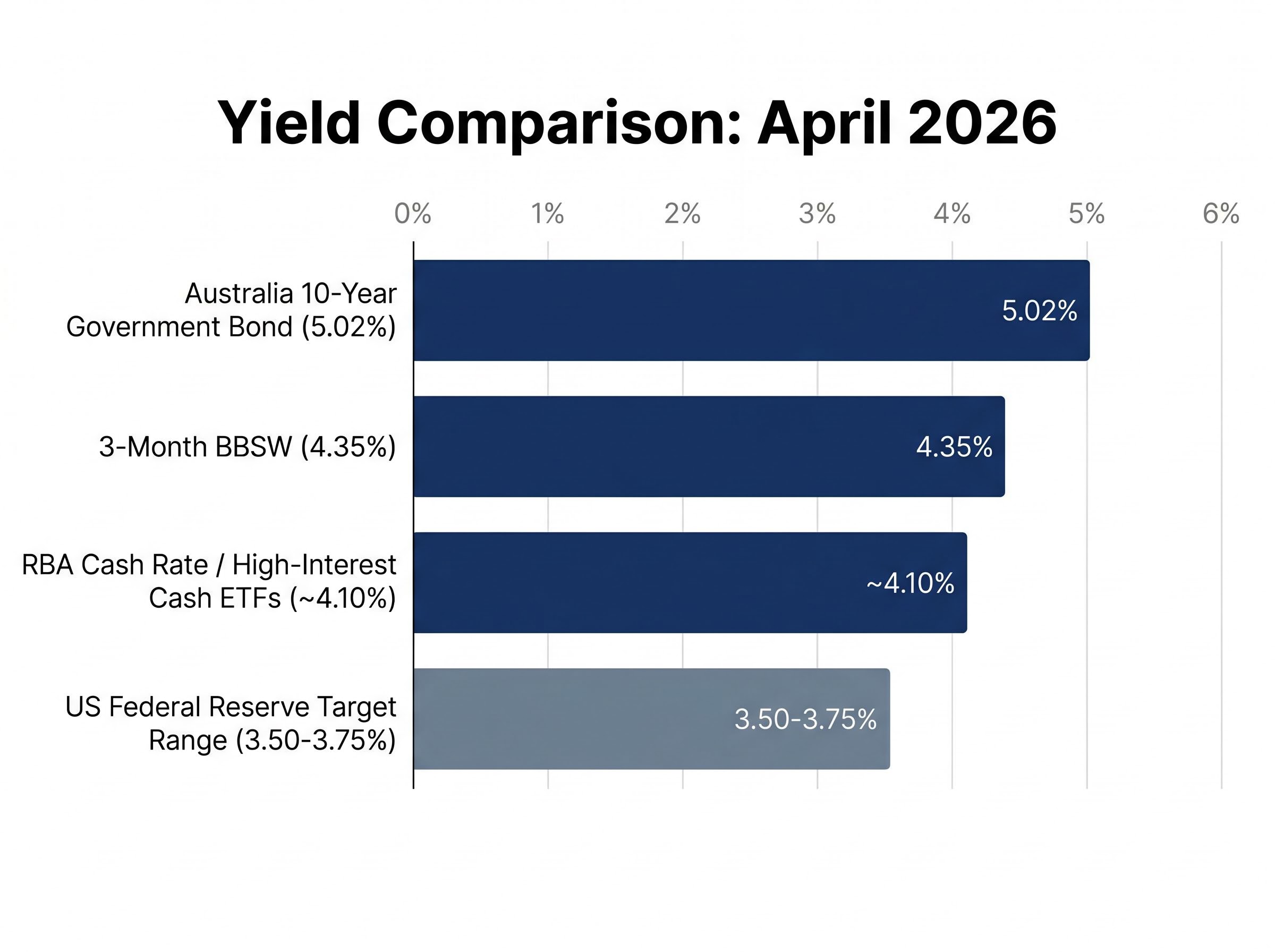

A resilient investment approach in 2026 requires abandoning outdated safe-haven assumptions. Historically, investors defaulted entirely to the US dollar during geopolitical crises. However, traditional defensive tactics are showing mixed effectiveness against the current macroeconomic crosscurrents, as the US Federal Reserve target range currently sits at 3.50-3.75%, notably lower than the RBA cash rate.

This interest rate differential fundamentally alters the cost of seeking safety in US assets, reducing the yield premium historically associated with holding dollars. Consequently, Australian wealth managers and superannuation funds are actively trimming their USD exposure in favour of alternative safe havens that offer better structural support. Central bank gold holdings now exceed USD reserves in total value globally, solidifying the precious metal’s status as a highly resilient asset amid rising government debt and geopolitical fragmentation.

Understanding why the old rules of safety no longer apply gives investors the confidence to restructure their own holdings systematically. Market resilience no longer means hiding entirely in cash; it means building a diversified allocation that can absorb shocks while continuing to compound over time. Modern market defence relies on a three-part framework designed for a rate-cut-starved environment:

- Securing Local Yield: Prioritise domestic fixed-income instruments that offer higher baseline returns than global alternatives, anchoring the portfolio with predictable income streams.

- Avoiding Emotional Timing: Maintain consistent market exposure rather than attempting to trade in and out of rapidly shifting geopolitical news cycles, which often results in missing sharp recovery days.

- Holding Productive Equities: Retain positions in companies demonstrating strong cash flows, pricing power, and the ability to pass on elevated input costs to consumers without destroying demand.

For investors wanting to translate these defensive principles into specific local allocations, our detailed coverage of ASX portfolio protection provides a clear framework for identifying companies with strong pricing power and executing risk-efficient rebalancing strategies during elevated inflation.

Capturing Australian Yield Through Cash and Fixed Income

Australian domestic yields remain highly attractive compared to global alternatives, providing a strong foundation for defensive capital. Moving from macroeconomic theory to specific yield-capturing tactics requires evaluating the exact returns available in the local market. The RBA has maintained a steady approach despite the external chaos, keeping the cash rate at 4.10% and providing a strong baseline for domestic fixed income investors.

Traditional government bonds offer compelling compensation for longer lock-up periods, with the Australia 10-Year Government Bond Yield sitting at approximately 5.02% as of late April 2026. This premium over the cash rate reflects the market pricing in extended inflation risks. For shorter-term allocations, the 3-month Bank Bill Swap Rate (BBSW) is tracking at 4.35%, serving as a critical benchmark for corporate lending. High-interest cash exchange-traded funds (ETFs) are also offering rates highly competitive with at-call bank deposits, generally hovering near the central bank benchmark.

Accessing AOFM Treasury Bond issuance data allows fixed-income investors to track the exact characteristics and outstanding volumes of these government securities when structuring long-term defensive allocations.

Preserving liquid capital in high-yielding accounts serves a dual purpose in the current environment. It generates returns above inflation while keeping funds readily accessible to deploy when major equity opportunities arise. Evaluate current bank deposits against these baseline metrics to verify if existing allocations are delivering competitive returns.

| Yield Instrument | Current Rate (April 2026) | Strategic Function |

|---|---|---|

| Australia 10-Year Government Bond | 5.02% | Long-term defensive anchor |

| 3-Month BBSW | 4.35% | Short-term corporate benchmark |

| RBA Cash Rate | 4.10% | Baseline risk-free reference |

| High-Interest Cash ETFs | ~4.10% | Liquid capital preservation |

Systematic Equity Investing Amid Market Dislocation

Approaching equity markets following the Q1 volatility requires a distinct shift from defensive hesitation to systematic opportunity capture. The Australian banking sector has demonstrated notable resilience as a domestic anchor against extreme energy price volatility. National Australia Bank (NAB) recently reported 15% higher cash earnings compared to the second half of 2025, highlighting the underlying operational strength of local financial institutions even as broader market sentiment sours.

Before the current geopolitical shock, international equities saw a massive 30% full-year return in 2025. The recent energy-driven volatility has compressed these valuations rapidly. Employing a dollar-cost averaging strategy allows investors to mechanically capture these market downturns. Systematically investing fixed amounts at regular intervals removes the emotional burden of trying to predict the exact bottom of the geopolitical news cycle.

Tracking exactly how global conflict reallocates capital reveals distinct sector rotation opportunities, as institutional money systematically shifts away from vulnerable consumer discretionary stocks and fortifies alternative energy infrastructure.

Capitalising on International Market Discounts

The Iran-driven derating has created distinct entry points in global markets that were previously trading at significant premiums. European and Emerging Markets now present notable valuation discounts, supported by favourable long-term fiscal spending and monetary easing backdrops.

Maintain broad geographic exposure through diversified funds rather than attempting to pick individual sovereign winners. The reassessment of the Middle East conflict continues to weigh heavily on specific sectors, but current institutional allocations generally assume no escalation into a wider global conflict. Drip-feeding capital into these discounted international markets safely captures the upside when the current geopolitical pressures eventually ease.

Executing Your 2026 Wealth Blueprint

Two opposing forces are currently shaping the financial environment: short-term geopolitical shocks driving immediate market volatility, and long-term technological deflation anchoring future pricing power. Navigating this dynamic requires a balanced approach that pairs protective domestic yield with growth-oriented equities. Doing nothing and holding zero-yielding assets remains the greatest risk to long-term purchasing power as inflation fluctuates.

Review current fixed income yields and equity diversification against the metrics provided in this guide to ensure alignment with current market realities. Adjust capital allocations to secure strong domestic fixed-income returns while systematically capturing discounted international equities to execute a resilient wealth plan.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.