WTI Jumps 1.6% as Iran Strikes Shatter Hormuz Deal Hopes

2 hrs ago

The market reaction on April 29, 2026, presented a counterintuitive scenario for infrastructure and defence contractor Parsons Corporation. Shares traded higher pre-market and climbed intraday, despite the company reporting a year-on-year revenue contraction for the first quarter of 2026.

This divergence between headline figures and equity pricing highlights a reporting distortion caused by the roll-off of a confidential government agreement. Beneath this top-line noise, the company delivered a material beat in adjusted earnings and established historic momentum in its future contract pipeline.

A rigorous analysis of Parsons stock requires evaluating the underlying operational engine rather than these surface-level revenue drops. By focusing on critical leading indicators like bookings, adjusted organic growth, and backlog expansion, investors gain a precise framework for assessing the true health of the business. The underlying data reveals an enterprise actively converting structural government demand into tangible margin expansion.

The headline numbers from the Q1 2026 earnings report initially suggest a business in contraction. Parsons recorded a total revenue of $1.5 billion, representing a 4 percent annual drop from the previous year. Overall net income also fell.

The company’s published first quarter earnings release details these top-line financial metrics alongside broader segment performance data.

However, these figures carry a significant structural distortion. The decline is almost entirely attributable to the scheduled roll-off of an undisclosed secret government agreement, which artificially depressed the comparative year-on-year metrics. When analysts exclude the impact of this specific confidential project, the operational picture changes completely.

Stripping out the secret contract reveals actual total growth of 8 percent across the broader business. On an organic basis, the company expanded by 3 percent.

This underlying strength translated directly to the bottom line. This performance beat the Wall Street consensus, demonstrating how surface-level earnings reports can easily misdirect investors. Understanding these exact adjustments provides the necessary baseline to calculate the true operational trajectory of the stock.

| Metric | Q1 2026 Reported | Adjusted (Excluding Secret Contract) |

|---|---|---|

| Total Revenue Growth | -4% | +8% |

| Organic Growth | N/A | +3% |

Historical revenue only measures past execution, making it a lagging indicator of corporate health. For government defence and infrastructure equities, the ultimate leading indicators of future growth live within the order book. The most telling metric from the first quarter is the 1.4x book-to-bill ratio achieved across both of the company’s business segments.

A book-to-bill ratio measures the volume of new orders received against the amount of work actually billed during a specific period. It functions as a direct mathematical gauge of supply and demand for the company’s services.

Any number over 1.0 indicates a growing business, as the organisation is securing new contracts faster than it completes existing ones. A 1.4x ratio signifies aggressive pipeline expansion that will mathematically force future revenue upward.

This rapid order accumulation drove the total backlog to a record $9.3 billion. Within federal contracting, analysts differentiate between total backlog and funded backlog. Funded backlog represents the portion of contracts where government agencies have already appropriated and allocated the specific capital.

Parsons reported a record funded backlog of $6.6 billion. Furthermore, the company holds $11 billion in awarded contracts that are not yet officially booked, providing unprecedented visibility into long-term revenue streams. By mastering these specific metrics, investors can independently assess future earnings visibility.

For readers wanting to build a systematic portfolio allocation strategy in this sector, our dedicated guide to defense contractor investing details the methods for valuing funded pipelines and navigating the political risks inherent in federal budgets.

The $2.1 billion in new first-quarter bookings did not materialise in a vacuum. These orders connect directly to broader macroeconomic themes, specifically artificial intelligence integration and global electrification. Government and commercial clients are allocating massive capital pools to address these structural trends.

In the Critical Infrastructure segment, expansion is heavily tied to surging global energy requirements. Industry projections indicate a 40 percent rise in global electricity demand, forcing widespread infrastructure upgrades and grid modernisation projects. The company’s infrastructure divisions are positioned to capture government funding allocated for these exact resilience initiatives.

Simultaneously, the Federal Solutions segment is capturing significant value from the increasing militarisation of digital networks. U.S. defence agencies are actively reallocating capital toward the integration of AI-powered cyber defence technologies, directly benefiting specialised contractors.

This cybersecurity demand extends across the international defense ecosystem, as allied militaries increasingly mandate Zero Trust architectures to secure highly classified data sharing and multinational communications.

These geopolitical and technological trends translate directly into concrete federal appropriations. The first quarter featured multiple large-scale awards across both primary segments, proving the backlog rests on highly durable demand cycles.

The major contract wins include:

A $593 million extension for the Federal Aviation Administration (FAA) TSSC 5 transportation contract. A $500 million Joint Cyber Hunt Kit contract awarded by U.S. Cyber Command. * $145 million in GARDEM task orders to support advanced missile defence command and control technologies.

Winning lucrative contracts is only half the operational equation. The second half requires converting those awards into tangible profit and shareholder value. Despite the reported dip in net income, the company demonstrated exceptional financial efficiency and bottom-line improvement during the quarter.

Adjusted EBITDA reached a historic first-quarter high of $151 million, representing a 1 percent year-on-year increase. More importantly, profitability margins established a new company benchmark at 10.1 percent. This margin expansion provides clear evidence of strong executive execution and high operational leverage across the enterprise.

The organisation also executed a significant turnaround in cash generation. Operating cash utilisation improved, a favourable contrast against the amount utilised during the same period in 2025.

“Our first quarter results highlighted the resilience of our business and our team’s high level of execution, as we delivered our highest adjusted EBITDA margin ever, reached record levels for both total and funded backlog, achieved a robust book-to-bill ratio of 1.4x in both segments, and generated record first quarter cash flow,” said Carey Smith, Chief Executive Officer.

This disciplined cost control proves management can protect margins even while navigating complex contract transitions.

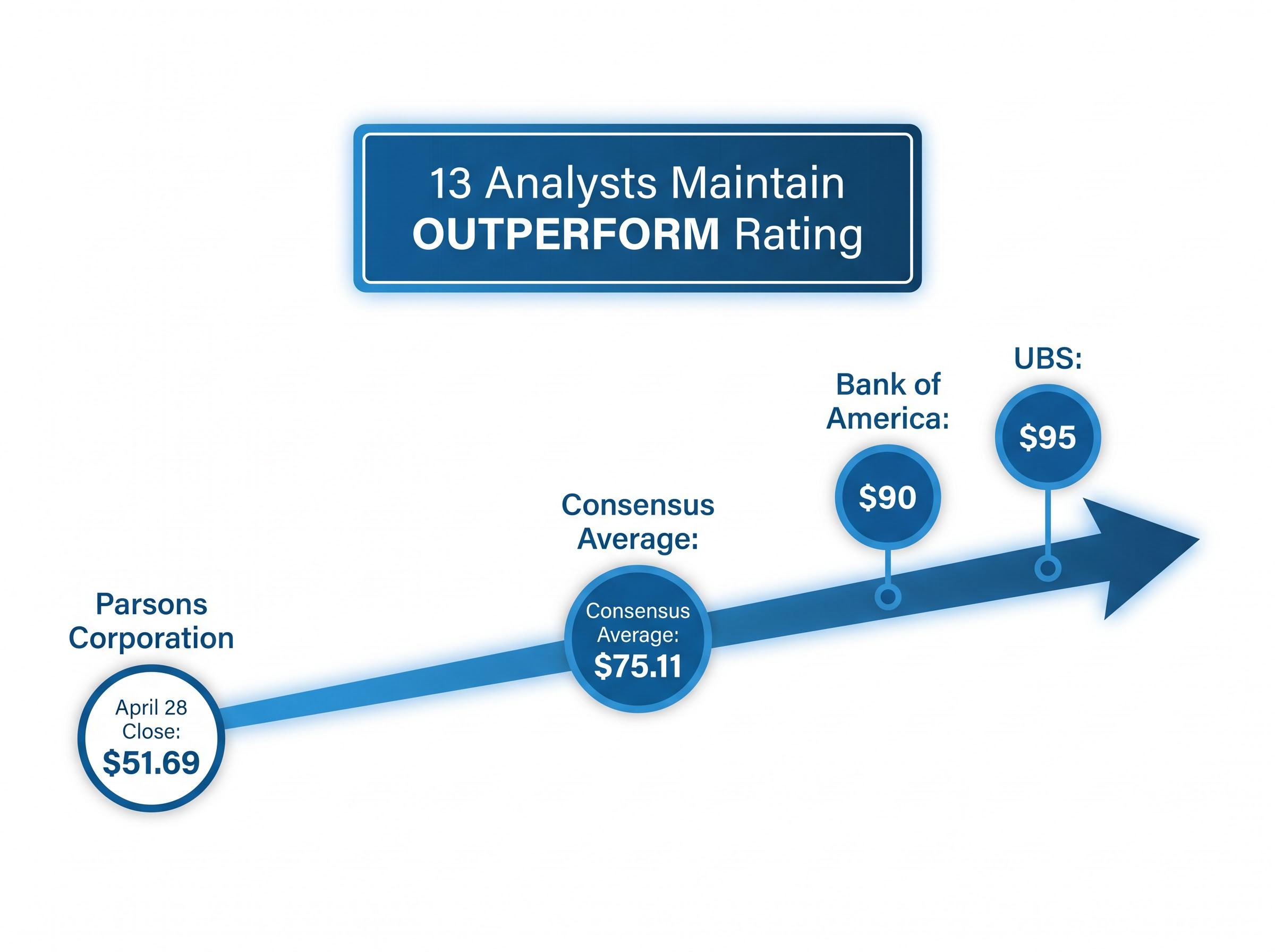

The combination of margin expansion and pipeline visibility explains why the market easily absorbed the headline revenue contraction. Ahead of the earnings release, the stock closed at $51.69 on April 28.

When equities absorb surface-level misses without significant downward pressure, analysing options market signals often reveals that institutional players had already accounted for the structural noise well before the earnings release.

As the underlying metrics became clear on earnings day, shares traded up as much as 3.75 percent intraday. Wall Street professionals maintain a highly favourable view of the stock’s trajectory, looking entirely past the temporary top-line noise. Analysts consistently highlight the growing backlog and improved margin profile as primary catalysts for future price appreciation.

A consensus of 13 Wall Street analysts maintains an OUTPERFORM rating on the equity. Management supported this institutional confidence by explicitly reaffirming full-year 2026 revenue guidance of $6.5 billion to $6.8 billion, aligning cleanly with broader market expectations.

Institutional targets suggest substantial upside from current trading levels. The most prominent analyst projections include:

This consensus view provides investors with the institutional context required to evaluate the stock’s forward momentum over the next 12 months.

The first quarter of 2026 functions as an exceptional case study in reading corporate financial statements. While the headline revenue contraction initially suggests weakness, the underlying leading indicators paint a highly bullish picture of an enterprise in aggressive expansion. The true health of the business lives within the record $9.3 billion backlog, the historic 10.1 percent profitability margin, and the powerful conversion of macroeconomic trends into funded federal contracts.

As the company moves deeper into fiscal 2026, its strategic positioning within the global defence and critical infrastructure markets remains exceptionally strong. Investors willing to look past temporary reporting distortions will find an operational engine accelerating into a multi-year growth cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The reported revenue contraction in Q1 2026 was primarily due to the scheduled roll-off of an undisclosed secret government agreement, which distorted year-on-year comparative metrics.

Excluding the impact of the secret contract, Parsons achieved an actual total growth of 8 percent across the broader business and 3 percent organic growth, surpassing Wall Street consensus.

Parsons' 1.4x book-to-bill ratio and record $9.3 billion total backlog, including $6.6 billion funded backlog, signify aggressive pipeline expansion and strong future revenue potential.

Yes, Parsons achieved its highest adjusted EBITDA margin ever at 10.1 percent, and adjusted EBITDA reached a historic first-quarter high of $151 million, demonstrating strong financial efficiency.

Wall Street analysts maintain a favorable view, with a consensus "OUTPERFORM" rating and an average price target of approximately $75.11, supported by the growing backlog and improved margin profile.