Lululemon Fundamental Analysis: the Price of Brand Dilution

2 hrs ago

Any comprehensive Beta Technologies analysis must begin by confronting the stark contrast between the company’s ambitious November 2025 initial public offering and its current market reality. As of April 28, 2026, shares trade at $15.54, representing a severe contraction from their debut valuation. The electric aviation sector currently faces significant downward pressure on valuations as capital markets reassess the timeline for commercial air taxis.

However, surface-level stock performance often obscures fundamentally different underlying business models. This evaluation examines the specific commercial strategy that insulates this electric aviation operator from the high-burn passenger network race.

Investors tracking the broader mobility transition frequently misjudge the timeline required to achieve regulatory approval for human flight. This analysis explores how a pivot toward freight logistics, physical charging infrastructure, and component supply provides a distinct, quantifiable advantage. Understanding these core pillars offers clarity on how the company plans to survive the current market compression.

The public market debut of the manufacturer executed smoothly on November 5, 2025, capturing aggressive investor appetite. The company sold 34,330,882 shares at $34.00, raising $1.16 billion before standard underwriting discounts. Yet the subsequent stock trajectory leading into early 2026 reflects a broader recalibration of sector risk.

The current market capitalisation sits at $3.6 billion, a figure that demands close scrutiny against the company’s actual balance sheet. Investors assessing bankruptcy risk must look past the share price decline and focus on liquid asset reserves. Early market entrants in the electric aviation space typically require continuous capital injections to survive developmental phases.

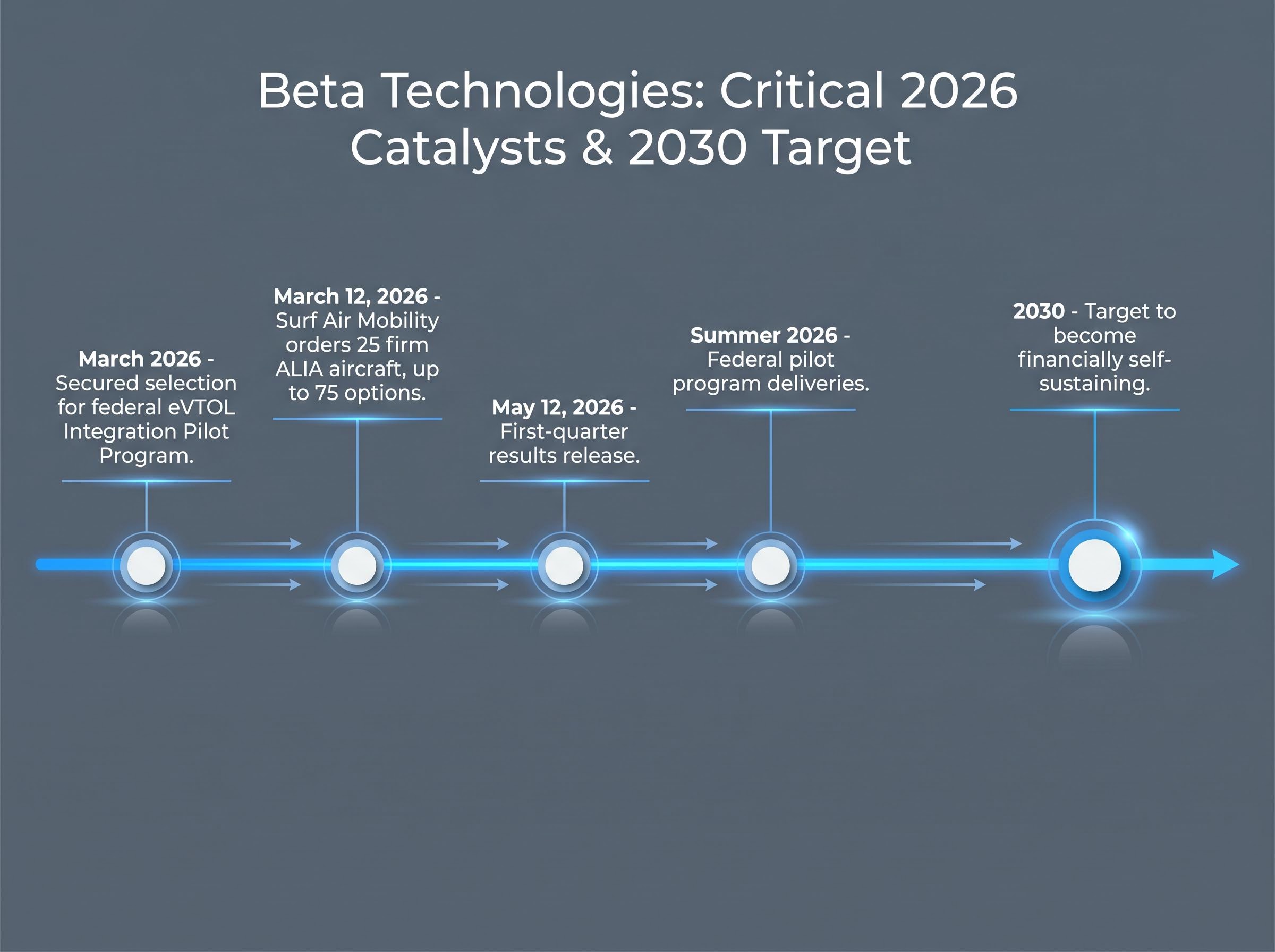

The company retains a $971 million cash buffer in available liquid assets, providing a fully funded operational runway through 2026. This reserve is the ultimate metric of survival in a capital-starved environment. Market attention now shifts toward the upcoming May 12, 2026 release of first-quarter results.

These figures will test whether the falling market capitalisation accurately prices the fundamental business or merely reflects macroeconomic sector pressure.

| Financial Metric | November 2025 (IPO) | April 2026 (Current) |

|---|---|---|

| Share Price | $34.00 | $15.54 |

| Market Capitalisation | $6.57 billion to $7.40 billion | $3.60 billion |

| Capital Raised / Cash Buffer | $1.16 billion (Gross Proceeds) | $971 million (Liquid Assets) |

Commercial analysts evaluating electric vertical takeoff and landing aircraft frequently make the error of treating all sector stocks equally. The electric aviation industry encompasses entirely different operational playbooks, and differentiating a consumer passenger play from a business-to-business logistics operation is strictly necessary for accurately pricing regulatory risk.

Comprehensive passenger networks: Vertically integrated companies building aircraft to operate their own consumer air taxi services. Pure equipment fabricators: Manufacturers selling aircraft directly to existing airlines or logistics operators. Diversified component makers: Firms supplying core propulsion or battery mechanisms to competitor aircraft programs. Self-navigating software plays: Technology companies focused purely on the autonomous flight systems required for future pilotless travel.

Competitors like Joby Aviation and Archer Aviation are building vertically integrated passenger networks. In contrast, the strategic focus here remains firmly on established cargo operators. This deliberate pivot away from consumer flying taxis offers a significantly faster and more reliable path to structural revenue.

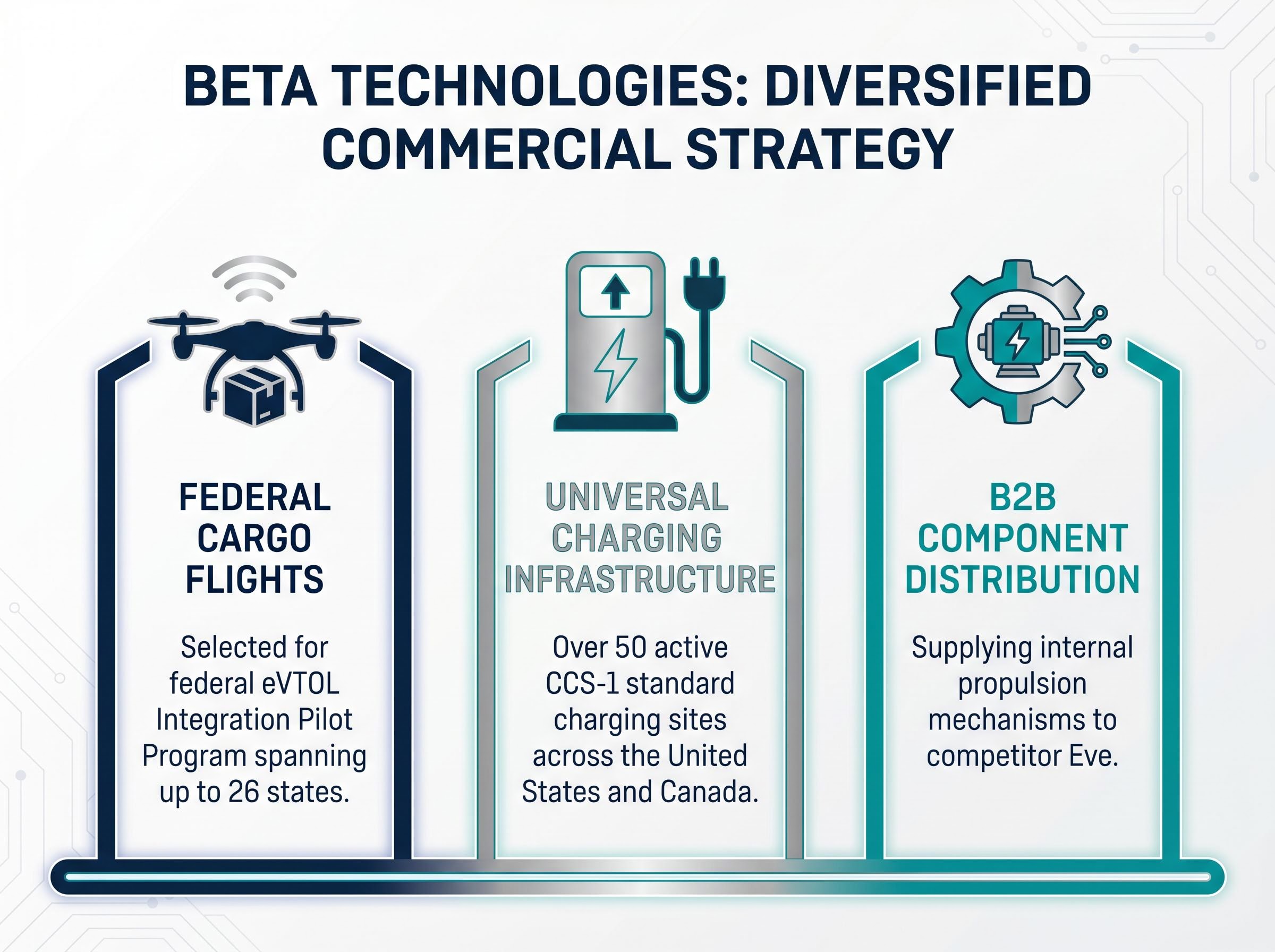

The Federal Aviation Administration presents a fundamentally lower barrier to entry for uncrewed or cargo flights compared to the rigorous standards required for commercial human passenger operations. This regulatory reality materialised in March 2026, when the company secured selection for the federal eVTOL Integration Pilot Program. The selection spans up to 26 states, granting immediate federal backing for tangible medical and logistics transport operations rather than speculative consumer routes.

The official FAA Advanced Air Mobility framework establishes specific certification pathways for both aircraft and operators, shaping the timeline expectations for early cargo deployment compared to human transport.

The most resilient element of the company’s commercial strategy exists entirely on the ground. The rapid expansion of an electric aircraft charging network across North America creates a recurring revenue stream that operates independently of airframe sales. Installations nearly doubled throughout 2024 to reach 46 sites across 22 states prior to the public offering.

By early 2026, that footprint has expanded to over 50 active sites online across the United States and Canada. The strategic brilliance of this rollout lies in the deliberate adoption of the universally compatible CCS-1 charging standard. Rather than building a proprietary walled network that only services their own aircraft, the company has built physical infrastructure that competing manufacturers will eventually need to utilise.

This creates a distinct commercial moat that generates profit even if competitors dominate the final aircraft manufacturing race.

For investors exploring how heavy transport operators are solving similar power requirements, our dedicated guide to grid-integrated charging infrastructure examines commercial models that combine battery swapping with renewable energy capture.

Transitioning from building whole aircraft to supplying internal propulsion mechanisms to direct competitors demonstrates a sophisticated maturation of the business model. According to company data, the company currently distributes internal propulsion mechanisms to competitor Eve, a subsidiary of the aerospace giant Embraer. These business-to-business sales validate the underlying technology stack in the eyes of the broader market.

This specific Eve component supply agreement involves the provision of electric pusher motors for conforming prototypes, establishing a direct commercial channel that monetises core intellectual property before full aircraft certification.

Supplying components to rivals effectively creates a hedged bet on the broader sector’s success, generating revenue regardless of which specific aircraft operator captures the majority of the market share.

The company announced a major aircraft purchase agreement with Surf Air Mobility on March 12, 2026. This deal includes a firm order for 25 all-electric ALIA aircraft, alongside structured options for up to 75 additional units. While this specific order focuses heavily on passenger operations, it perfectly feeds into the broader component and infrastructure strategy.

Every passenger aircraft delivered expands the required utilisation of the company’s universal charging network. This mechanism reinforces the recurring revenue loop that defines their diversified playbook.

The defining question for any commercial evaluation in the electric aviation sector is whether an operator will exhaust its capital before achieving profitable scale. Synthesising the diverse revenue channels against the current cash burn rate reveals a structurally sound financial timeline extending through the end of the decade. Historical revenue for the first half of 2025 sat at $15.6 million, doubling the performance of the prior year.

Full-year projections for 2025 indicated revenue landing between $29 million and $33 million, paired with a substantial free cash flow loss of $414.5 million. While a capital burn rate of that magnitude appears alarming in isolation, it aligns with the intensive manufacturing scale-up required for federal aviation programs.

Developers working on next-generation drone battery retention technology face similar capital-intensive development cycles before their silicon components can achieve commercial certification.

The combination of income from cargo flights, expanding charging networks, and component distribution steadily offsets this expenditure. According to company data, management maintains a stated corporate target to become financially self-sustaining during 2030 without requiring further equity dilution.

Financial Runway Target According to company data, “The combination of diversified commercial income and our existing $971 million liquid asset reserve provides the exact mathematical runway required to reach self-sustaining profitability by 2030,” company projections indicate.

This projection heavily relies on the precise execution of near-term logistics contracts. However, the existing $971 million capital reserve provides a credible mathematical path to achieving that milestone.

The structural combination of dedicated freight platforms, universal physical infrastructure, and component distribution creates a significantly more resilient business model than pure passenger aviation plays. While stock prices in the electric aviation sector may remain highly volatile throughout 2026, the underlying cash position comprehensively supports this long-term commercial strategy.

The company is fully capitalised to execute its immediate operational milestones. Readiness to capitalise on the upcoming summer 2026 federal pilot program deliveries will serve as the next major catalyst for fundamental valuation reassessment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Beta Technologies focuses on freight logistics, physical charging infrastructure, and component supply, differentiating itself from companies building consumer passenger air taxi networks.

Beta Technologies retains a $971 million cash buffer, which management projects provides a fully funded operational runway through 2026 and a credible path to self-sustaining profitability by 2030.

Focusing on cargo operations allows Beta Technologies to pursue a significantly faster and more reliable path to structural revenue, facing lower regulatory barriers than commercial human passenger flights.

Beta Technologies' CCS-1 charging network uses a universally compatible standard, creating a distinct commercial moat that generates recurring revenue even if competitors dominate aircraft manufacturing, as rival manufacturers will need to utilize it.