What Domino’s Q1 Results Reveal About the Consumer Spending Slowdown

15 hrs ago

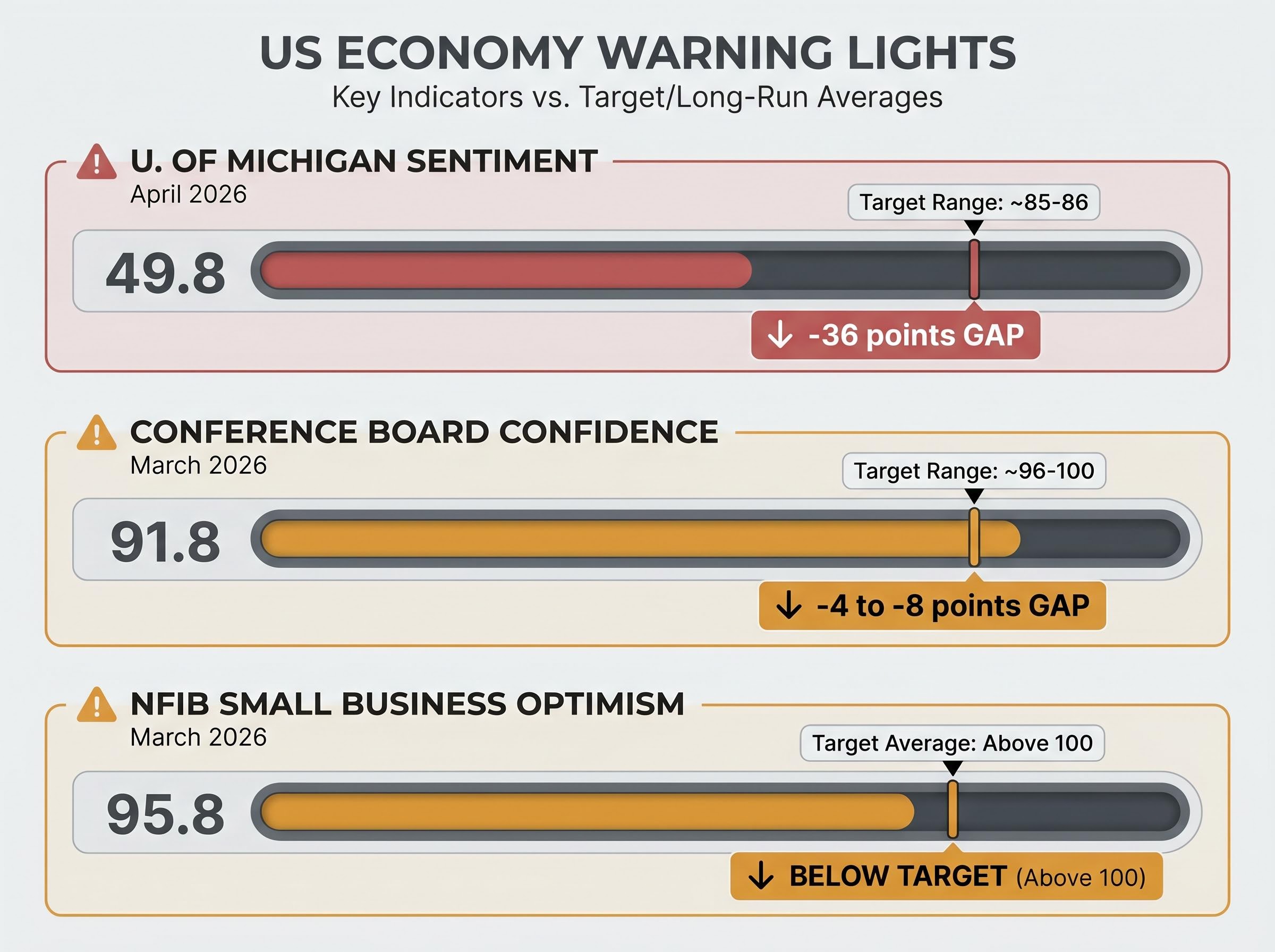

“`json { “fact_checked_full_article”: “The University of Michigan Consumer Sentiment Index fell to 49.8 in April 2026, its lowest reading on record. The S&P 500, in the same month, sat near 7,165, carrying a year-to-date gain of 5.05% after returning 25% in 2024 and ~18% in 2025. The stock market and economic confidence are telling two different stories, and the gap between them is wider than at any point in recent memory.\n\nMarkets and sentiment have historically moved in rough alignment. When one races ahead of the other by this magnitude, investors face a genuine interpretive problem: is the market pricing in a recovery that confidence surveys cannot yet detect, or are equity valuations running on borrowed conviction while the ground beneath them softens? What follows is a close reading of the specific data driving that divergence, the historical pattern of how these gaps have resolved, and a framework for holding both signals at once without dismissing either.\n\n## The divergence by the numbers: record equities, record-low confidence\n\nThe simplest way to see the gap is to place the numbers side by side.\n\n> Record low. The University of Michigan Consumer Sentiment Index printed at 49.8 in April 2026, the lowest reading in the survey’s history dating back to 1978.\n\nThe S&P 500’s 5.05% gain in 2026 alone extends a run that has delivered cumulative returns north of 47% since the start of 2024. Consumer confidence, by every available measure, has moved in the opposite direction.\n\n

| Indicator | Most Recent Reading | Long-Run Average | Gap from Average |

|---|---|---|---|

| S&P 500 YTD Return | +5.05% (April 2026) | ~+8-10% annual | On pace or above |

| U. of Michigan Sentiment | 49.8 (April 2026) | ~85-86 | -36 points |

| Conference Board Confidence | 91.8 (March 2026) | ~96-100 | -4 to -8 points |

| NFIB Small Business Optimism | 95.8 (March 2026) | Above 100 (historical norm) | Below optimism threshold |

\n

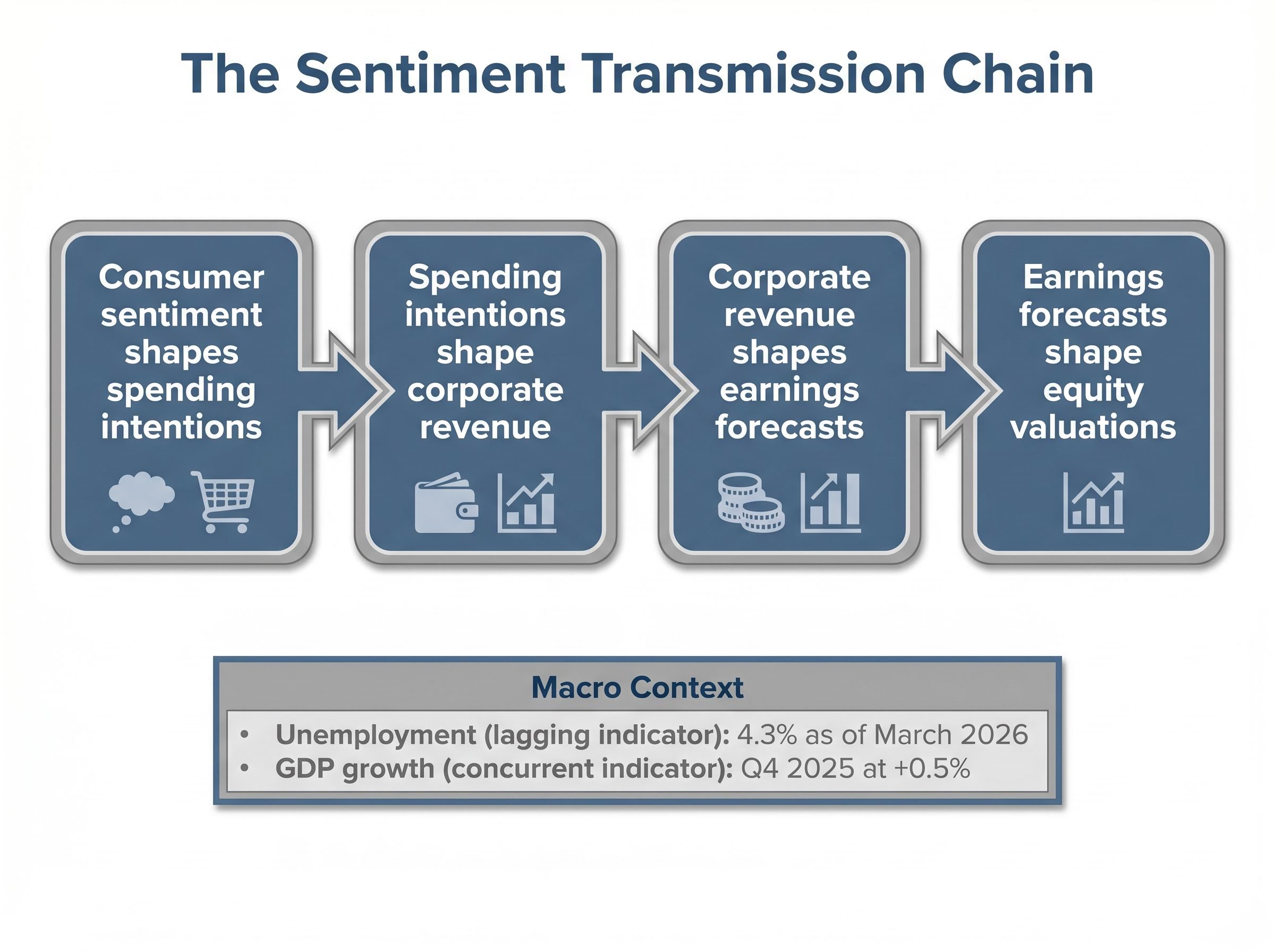

\n\nThe Michigan reading is the most striking: 36 points below its long-run average. The Conference Board and NFIB readings confirm that the pessimism extends beyond households into the small business sector. Investors relying solely on index levels to gauge economic health are reading one instrument on a dashboard with several warning lights active.\n\n## Why soft data matters when hard data looks stable\n\nA common response to collapsing sentiment is to dismiss it as mood, not mechanism. The hard data, after all, looks serviceable: unemployment at 4.3% as of March 2026 remains low by historical standards. Hiring continues. The economy has not contracted.\n\nThat framing misses the transmission chain. Consumer sentiment shapes spending intentions. Spending intentions shape corporate revenue. Corporate revenue shapes earnings forecasts. Earnings forecasts shape equity valuations. Each link in that chain operates with a lag, which means by the time sentiment deterioration appears in GDP or unemployment, the damage is already well advanced.\n\nThe distinction between indicator types matters here:\n\n- Employment (lagging indicator): Unemployment at 4.3% reflects hiring decisions made months ago. It tells investors where the economy has been, not where it is going.\n- Inflation expectations (leading indicator): Year-ahead inflation expectations of 4.7-4.8% from the University of Michigan’s April 2026 survey signal that households expect purchasing power to erode further, a direct headwind to discretionary spending.\n- GDP growth (concurrent indicator): Q4 2025 annualised growth came in at just +0.5%, according to Bureau of Economic Analysis data, suggesting momentum was already fading before sentiment hit its record low.\n\n### The mixed macro picture investors are navigating\n\nThe coexistence of low unemployment and record-low sentiment is not a paradox. It is a signal that inflation is eroding real purchasing power even as headline employment holds. In a typical cycle, low unemployment lifts confidence because workers feel secure and wages grow. That stabilising dynamic breaks down when inflation outpaces wage gains, leaving households employed but financially squeezed.\n\nGoldman Sachs has flagged that US consumers face challenging months ahead due to inflation pressures, a view consistent with sentiment readings that show households feeling worse despite remaining employed. Q1 2026 GDP data was not yet available at the time of writing, making the next print a particularly meaningful signal for whether the soft data has begun infecting the hard numbers.\n\n## What consumer sentiment and business confidence actually measure\n\nThese indices are not opinion polls. Each one surveys a specific set of economic behaviours and expectations, and understanding their construction changes how investors interpret new readings.\n\n- University of Michigan Consumer Sentiment Index: A monthly telephone survey covering five sub-components that measure both current financial conditions and forward expectations for personal finances, business conditions, and buying conditions. Published monthly since 1978, with a long-run average of approximately 85-86. Considered a leading economic indicator because it captures spending intentions before they appear in retail sales or GDP data.\n- Conference Board Consumer Confidence Index: A monthly mail survey with particular emphasis on labour market conditions, asking respondents to assess whether jobs are plentiful or hard to find. Published since 1967, with a long-run average of approximately 96-100. Its labour market focus makes it a useful complement to the Michigan index’s broader financial conditions lens.\n- NFIB Small Business Optimism Index: A monthly survey of small business owners covering hiring plans, capital expenditure intentions, sales expectations, and inventory investment. Small business capex intentions are a forward signal for broader economic investment because small firms account for a significant share of US employment and output.\n\nThe current Michigan reading of 49.8 sits approximately 36 points below its long-run average, one of the widest gaps on record. Investors who understand what these surveys measure can assess whether a given print represents a genuine forward signal or temporary noise, and calibrate their response accordingly.\n\n## Historical patterns: what happens when this gap has appeared before\n\nThe historical record on sentiment troughs and subsequent equity performance tells a story that cuts both ways.\n\n> According to Zacks Investment Research commentary, the lowest consumer sentiment readings have historically preceded 12-month S&P 500 returns averaging approximately 24-25%, functioning as a contrarian signal.\n\nThat pattern is well established. When households are most pessimistic, equity markets have tended to deliver their strongest forward returns. The logic is intuitive: by the time sentiment reaches extreme lows, much of the bad news is already reflected in consumer behaviour and, to some degree, in equity pricing. The subsequent recovery in both spending and confidence drives a rally.\n\nThe counter-pattern is equally instructive. Sentiment peaks have historically preceded more modest forward returns, suggesting that elevated confidence correlates with markets that have already priced in the good news.\n\nTwo competing interpretations emerge:\n\n1. Contrarian buy signal: Record-low sentiment may indicate that pessimism has overshot, and equities purchased at sentiment troughs have historically outperformed over the following 12 months.\n2. Genuine leading warning: The current sentiment decline is more extreme and more sustained than most prior trough episodes. The April 2026 reading of 49.8 versus a long-run average of 85-86 represents a gap wider than in several prior cycles, which complicates the assumption that this trough will resolve the same way previous ones have.\n\nNo institutional source currently resolves which interpretation applies to the present cycle. The depth and duration of this particular decline sit outside the comfortable range of historical analogies.\n\n## The broader stress picture: commercial real estate and regional bank exposure\n\nThe sentiment-equity divergence is not the only fault line. Credit markets carry their own set of stress signals that have yet to appear fully in broader equity pricing.\n\nCMBS delinquency rates on office and multifamily properties have risen sharply in recent quarters, reflecting a commercial real estate market under sustained pressure from remote work adoption, higher interest rates, and weakening demand. Specific current delinquency figures were not available at the time of writing; investors can consult the Trepp CMBS Delinquency Report for the latest data.\n\nThree stress indicators warrant monitoring:\n\n- CMBS delinquency rates: Rising delinquencies on office and multifamily loans signal that property-level cash flows are deteriorating, a precursor to broader CRE repricing.\n- Regional bank CRE concentration: Approximately 45% of regional bank loan portfolios are concentrated in commercial real estate, a level that turns sector-specific stress into a potential systemic lending concern.\n- Credit loss provisions: Forward-looking reserves set aside by banks against expected loan losses; rising provisions indicate that bank management teams are preparing for deterioration rather than merely reporting it.\n\n### Why regional bank concentration in CRE amplifies the risk\n\nThe 45% concentration figure is the mechanism that connects CRE stress to the broader economy. When nearly half of a bank’s lending book sits in a single sector experiencing rising delinquencies, the pressure on capital ratios and lending capacity extends well beyond commercial property. Credit tightening by regional banks flows into small business lending, construction financing, and local economic activity.\n\nCredit loss provisions in upcoming regional bank quarterly earnings will be the forward-looking balance sheet signal worth tracking. Rising provisions would indicate that CRE stress is migrating from property markets into bank earnings, a potential second-order channel through which ground-level economic weakness could eventually reach equity valuations.\n\n## Holding two signals at once: a framework for investors\n\nThe S&P 500 near 7,165 and Michigan Sentiment at 49.8 present contradictory information. The instinct is to choose one signal over the other. The more disciplined approach is to monitor the data that would settle the debate, and to know in advance what change in that data would update one’s view.\n\nThe risk of the single-signal error runs in both directions. Ignoring sentiment and watching only equity levels means missing early warnings that have historically preceded economic deterioration. Acting solely on sentiment and exiting equities means potentially missing the contrarian recovery rally that has followed prior troughs.\n\nA practical monitoring framework centres on five specific data releases, in priority order:\n\n1. University of Michigan Consumer Sentiment monthly release: The April 2026 reading of 49.8 is the baseline. Any further decline, or a sustained failure to recover, would strengthen the case that sentiment deterioration is structural rather than transient.\n2. Conference Board Consumer Confidence monthly release: The labour market focus provides a cross-check on whether employment conditions are beginning to reflect the weakness sentiment surveys have flagged.\n3. NFIB Small Business Optimism monthly data: Capex intentions and hiring plans are the forward signals for business investment; deterioration here would suggest the sentiment drag is broadening beyond households.\n4. Q1 2026 GDP advance estimate (when available): This release will be the first meaningful test of whether weak Q4 2025 growth of +0.5% was a soft patch or the beginning of a trend. The data was not yet available at the time of writing.\n5. Regional bank quarterly earnings, specifically credit loss provisions: Rising provisions would signal that CRE stress is transmitting into the banking system, a development with implications for credit availability and broader economic activity.\n\nInvestors tracking the forward price-to-earnings ratio as a supplementary valuation check can consult FactSet or Bloomberg for current consensus estimates, as verified data was not available at the time of this analysis.\n\nThe goal is not to resolve the debate in advance. It is to identify the specific data points that would resolve it, and to watch for the moment when soft sentiment begins appearing in hard economic output.\n\n## Conclusion\n\nThe S&P 500 near 7,165 and the University of Michigan Consumer Sentiment Index at a record low of 49.8 represent the most extreme divergence between market performance and economic confidence in the survey’s history. History cuts both ways: the contrarian case for equities purchased at sentiment troughs is real, supported by average 12-month returns of approximately 24-25% following prior lows. The depth and duration of this particular decline, however, sit well outside the range of most historical precedents.\n\nThe more disciplined approach is not to pick a side but to track the transmission mechanism. Sentiment flows into spending, spending flows into earnings, earnings flow into valuations. The next Michigan Sentiment release and the Q1 2026 GDP advance estimate will be the first meaningful tests of whether the soft data has begun infecting the hard numbers.\n\nInvestors who monitor that chain, rather than waiting for a single data point to settle the question, will be better positioned regardless of which signal proves correct.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements regarding economic indicators and market performance are subject to change based on evolving conditions.\n\n—” } “`

Valuation context adds another layer to this picture: the Buffett Indicator at 228% of GDP currently exceeds both the dot-com peak and the pre-2008 reading, a stretched reading that can persist for years without triggering a correction but that historically narrows the margin for error when leading indicators are simultaneously deteriorating.

The Federal Reserve’s shift to rate holds through year-end 2026 removes a mechanism that prior research identified as critical to sustaining elevated valuations during low-sentiment phases; without the expectation of future easing, the discount rate assumption embedded in current equity pricing rests on a narrower base of support.

The Trepp CMBS Delinquency Report for March 2026 documented a sharp jump in delinquency rates across office and lodging segments, providing the property-level data that substantiates the broader CRE stress picture the article outlines and giving investors a current benchmark against which to track further deterioration.

The Bureau of Economic Analysis GDP second estimate for Q4 2025 placed annualised real growth at just 0.5%, confirming that economic momentum was already fading before consumer sentiment reached its record low in April 2026.

The University of Michigan Consumer Sentiment Index is a monthly survey measuring household views on current financial conditions and forward expectations for personal finances, business conditions, and buying conditions. It is a leading economic indicator because it captures spending intentions before they appear in retail sales or GDP data, making it a useful early warning tool for investors monitoring economic momentum.

The S&P 500 has continued climbing on the back of cumulative gains exceeding 47% since the start of 2024, while the University of Michigan Consumer Sentiment Index hit a record low of 49.8 in April 2026, reflecting household anxiety about inflation eroding purchasing power despite low unemployment. Markets may be pricing in a future recovery that confidence surveys cannot yet detect, or equity valuations may be running ahead of deteriorating economic fundamentals.

According to Zacks Investment Research commentary cited in the article, the lowest consumer sentiment readings have historically preceded 12-month S&P 500 returns averaging approximately 24-25%, functioning as a contrarian signal. However, the April 2026 reading of 49.8 is more extreme and more sustained than most prior trough episodes, which complicates direct comparisons to historical precedents.

The article identifies five priority data releases: the monthly University of Michigan Consumer Sentiment release, the Conference Board Consumer Confidence Index, the NFIB Small Business Optimism Index, the Q1 2026 GDP advance estimate, and regional bank quarterly earnings with a focus on credit loss provisions. Together these releases trace the transmission chain from household sentiment through to corporate earnings and equity valuations.

Regional banks hold approximately 45% of their loan portfolios in commercial real estate, and CMBS delinquency rates on office and multifamily properties have risen sharply, as confirmed by the Trepp CMBS Delinquency Report for March 2026. If credit loss provisions rise in upcoming bank earnings, CRE stress could tighten credit availability for small businesses and local economies, creating a second-order channel through which property market weakness reaches broader equity valuations.