How Dual-Class Shares Put $24 Billion in Gulf Capital at Arm’s Length

22 hrs ago

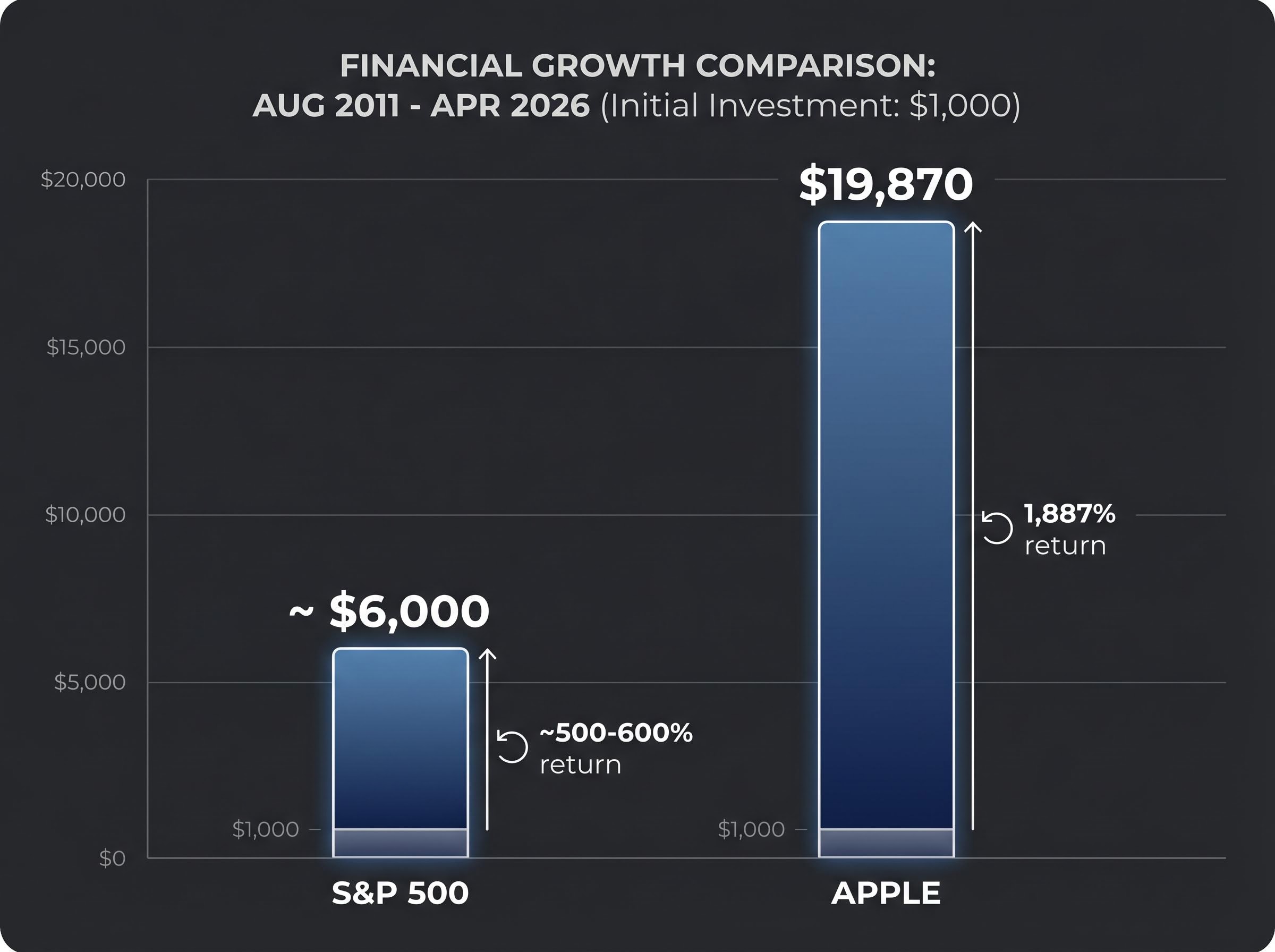

A $1,000 investment in Apple stock on the day Tim Cook became chief executive in August 2011 was worth approximately $19,870 by late April 2026. That is a price return of roughly 1,887%, excluding dividends. The same $1,000 allocated to the S&P 500 on the same date grew to an estimated $6,000 over the identical window.

Cook’s announced departure, scheduled for 1 September 2026 with John Ternus named as successor, has prompted a wave of reflection among retail investors who owned Apple shares at some point during his tenure. Their outcomes diverged sharply, not primarily because of when they bought, but because of how long they stayed. What follows is an examination of why holding period is often the single most consequential variable in long-term equity returns, and what that principle means for how American investors approach the buy and hold strategy today.

Apple’s split-adjusted closing price on 24 August 2011 was approximately $13.435, according to historical data from Yahoo Finance and Macrotrends. By 27 April 2026, the stock had reached approximately $266.93, representing a compound annual growth rate (CAGR) of roughly 22% per year over 14.67 years.

A $1,000 investment in Apple at the start of Tim Cook’s tenure grew to approximately $19,870 by April 2026. The equivalent position in the S&P 500 grew to roughly $6,000 over the same period.

That gap, more than three times the index return on the same starting capital, is not a modelling exercise. It is what actually happened to invested dollars over a decade and a half.

A discussion on Reddit’s r/Money forum surfaced real shareholder accounts that put the data in human terms:

Several participants in the thread reported wishing they had held more shares, or exited later than they did. The same stock, the same starting price, produced radically different outcomes depending on how long each person stayed.

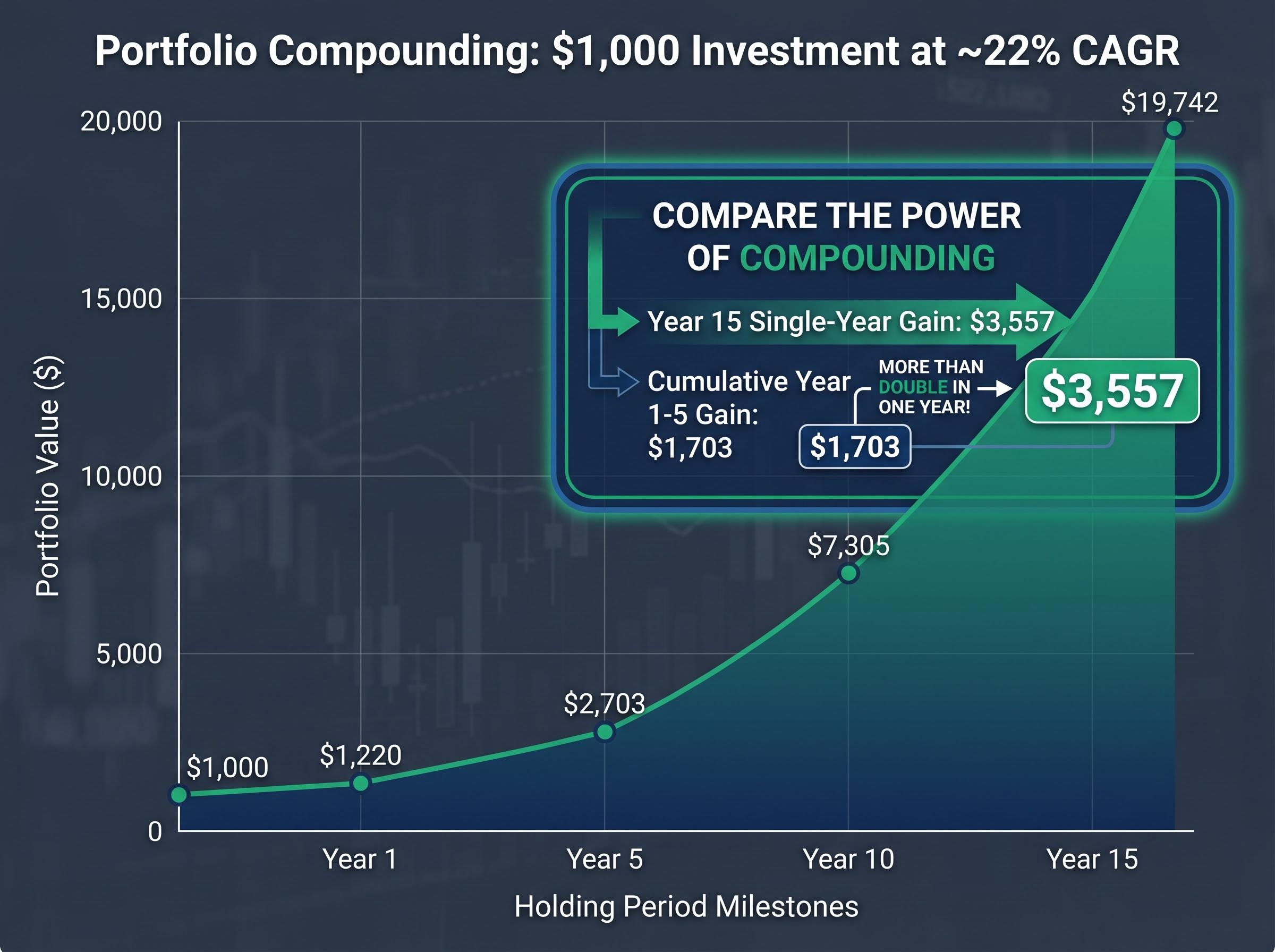

A 22% annual growth rate sounds consistent from year to year. In percentage terms, it is. In dollar terms, it is not, and the distinction is where the real wealth creation sits.

Compounding is nonlinear. A 22% return on a $1,000 base produces $220 in the first year. That same 22% applied to a base that has already grown to $8,000 by year ten produces $1,760 in a single year, eight times the dollar gain of year one despite the identical percentage rate. The absolute dollar gain accelerates as the base compounds, meaning the majority of the terminal value is generated in the final years of a long holding period, not the early ones.

The table below illustrates this effect using Apple’s approximate 22% CAGR on a $1,000 starting investment:

| Year | Approximate Portfolio Value | Dollar Gain That Year (Illustrative) | Cumulative Gain |

|---|---|---|---|

| 1 | $1,220 | $220 | $220 |

| 3 | $1,816 | $327 | $816 |

| 5 | $2,703 | $487 | $1,703 |

| 7 | $4,023 | $725 | $3,023 |

| 10 | $7,305 | $1,316 | $6,305 |

| 12 | $10,872 | $1,959 | $9,872 |

| 15 | $19,742 | $3,557 | $18,742 |

By year five, the $1,000 stake has roughly doubled. By year fifteen, it has grown nearly twentyfold. The dollar gain in a single late year exceeds the entire cumulative gain of the first five years combined.

This is why early exits carry such a steep structural cost. Selling at 300% or even 500% feels like a win, and it is, but it represents a fraction of the terminal value. The S&P 500’s estimated 500-600% return over the same window offers a useful baseline: it shows what a solid long-term return looks like without the late-phase acceleration that individual compounders like Apple can deliver.

The mathematics of compounding are straightforward. The psychology is not.

A common pattern among retail investors runs something like this: a stock doubles, the gain feels real, the future feels uncertain, and the position gets sold. The profit is tangible. The foregone compounding is invisible. Behavioural finance identifies this as loss aversion operating in reverse; the fear of losing existing gains overrides the potential for larger future ones.

Odean’s disposition effect research in the Journal of Finance established through large-scale brokerage data that retail investors systematically sell winning positions too early while holding losing ones too long, a pattern driven by the same asymmetry between tangible realised gains and invisible foregone compounding that the Apple case illustrates in dollar terms.

In the Reddit discussion, several Apple shareholders explicitly expressed regret over exiting before continued appreciation, noting that what felt like a reasonable decision at the time left substantial returns on the table.

The Apple case makes the cost of early exits visible in specific terms. An investor who sold in 2015 or 2016 would have missed three compounding catalysts that drove the bulk of the stock’s late-tenure appreciation:

The asymmetry is worth stating plainly. The downside of holding a quality company through volatility is a temporary drawdown. The downside of selling early is permanent foregone compounding. Both carry costs, but only one of them is recoverable.

The phrase “buy and hold” sounds passive. In practice, it is one of the more demanding disciplines an investor can adopt.

Holding through a 30-40% drawdown requires conviction that most investors overestimate on paper and underestimate in real time. Apple experienced significant corrections within the Cook tenure window, including the 2018 rate-driven selloff and the early 2020 pandemic shock. Both episodes tested shareholders’ resolve, and both preceded substantial further appreciation.

The strategy also requires honest self-assessment about position quality. Apple’s market capitalisation grew from approximately $350 billion in August 2011 to roughly $3.92 trillion by 27 April 2026, according to data from StockAnalysis and CompaniesMarketCap. The $700 billion-plus in cumulative buybacks served as a structural quality indicator, a signal that management was consistently returning capital while the business continued to grow.

There is a meaningful difference between holding a quality business through volatility (an intentional decision) and holding a deteriorating position out of inertia (a different risk entirely). Buy and hold works best when three conditions are met:

Some investors in the Reddit discussion offered a useful counterpoint: fixating on the maximum possible gain can obscure the fact that realising profits for personal financial goals is also a legitimate outcome. Diversification remains the structural safeguard. Apple as a case study illustrates the power of patient holding; it does not argue for single-stock concentration.

Diversification remains the structural safeguard the article raises here, and for U.S. investors building a long-term equity position, that principle now extends beyond sectors. Diversification across geographies as a structural portfolio safeguard has become more consequential in 2026, with the S&P 500 CAPE ratio near 40.66 and international developed markets trading at roughly half that multiple, creating a valuation gap that affects the long-run return potential of a domestically concentrated portfolio.

Apple’s roughly 1,887% price return is exceptional in magnitude. The underlying principle, that long holding periods in quality equities tend to outperform strategies built around timing entry and exit, applies far more broadly.

$1,000 invested in the S&P 500 in August 2011 grew to approximately $6,000 by April 2026. The same $1,000 in Apple grew to roughly $19,870. Both positions required the same discipline: staying invested.

The index return itself, an estimated 500-600% over 15 years, exceeds what most active trading strategies deliver after accounting for the structural headwinds that compound against frequent traders:

Journal of Finance research on individual investor trading performance, drawn from the trading records of more than 66,000 households, found that the most active traders underperformed a passive buy-and-hold approach by several percentage points annually, with transaction costs and mistimed entries accounting for the bulk of the gap.

Apple’s outperformance versus the index serves as a quantified illustration of what compounding can achieve in a single high-quality equity. It is not a prediction for other individual stocks. The holding-period lesson, however, transfers across portfolio approaches, including index-fund investing, where the same patience produces the same structural advantage.

Apple’s investor outcomes over the Cook era diverged not because shareholders bought at different prices, but because they held for different lengths of time. The compounding mechanics that turned $1,000 into nearly $20,000 are not specific to Apple; they are a function of time, quality, and the discipline to stay invested through periods when selling feels like the safer choice.

The counterpoint deserves acknowledgement. Selling to fund a home, secure retirement, or meet a personal financial goal is not a failure of strategy. It is the point of investing. The lesson is not to hold forever in all circumstances. It is to understand, in specific dollar terms, what is being given up when an exit happens early.

As Cook’s era ends and market narratives shift, the durable finding from Apple’s 15-year run may be the simplest one: compounding does its most powerful work in the years most investors never stay for.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The buy and hold strategy involves purchasing shares in a quality company and holding them for years or decades, allowing compounding returns to accumulate rather than attempting to time the market through frequent buying and selling.

A $1,000 investment in Apple on the day Tim Cook became CEO in August 2011 grew to approximately $19,870 by late April 2026, representing a price return of roughly 1,887% excluding dividends.

Compounding accelerates over time, meaning the largest dollar gains occur in the later years of a holding period; an investor who sold Apple in 2015 or 2016, for example, would have missed the wearables growth, pandemic-era demand surge, and over $700 billion in cumulative share buybacks that drove the bulk of its late-tenure appreciation.

Research published in the Journal of Finance found that the most active traders underperformed a passive buy-and-hold approach by several percentage points annually, with transaction costs, short-term capital gains taxes, and mistimed entries accounting for the bulk of the gap.

The buy and hold strategy works best when the business has a durable competitive position, the investor can tolerate significant drawdowns without panic-selling, and the time horizon is genuinely long, measured in years or decades rather than quarters.