Momentum or Value? Analysing 2 Canadian Defensive Stocks

Key Takeaways

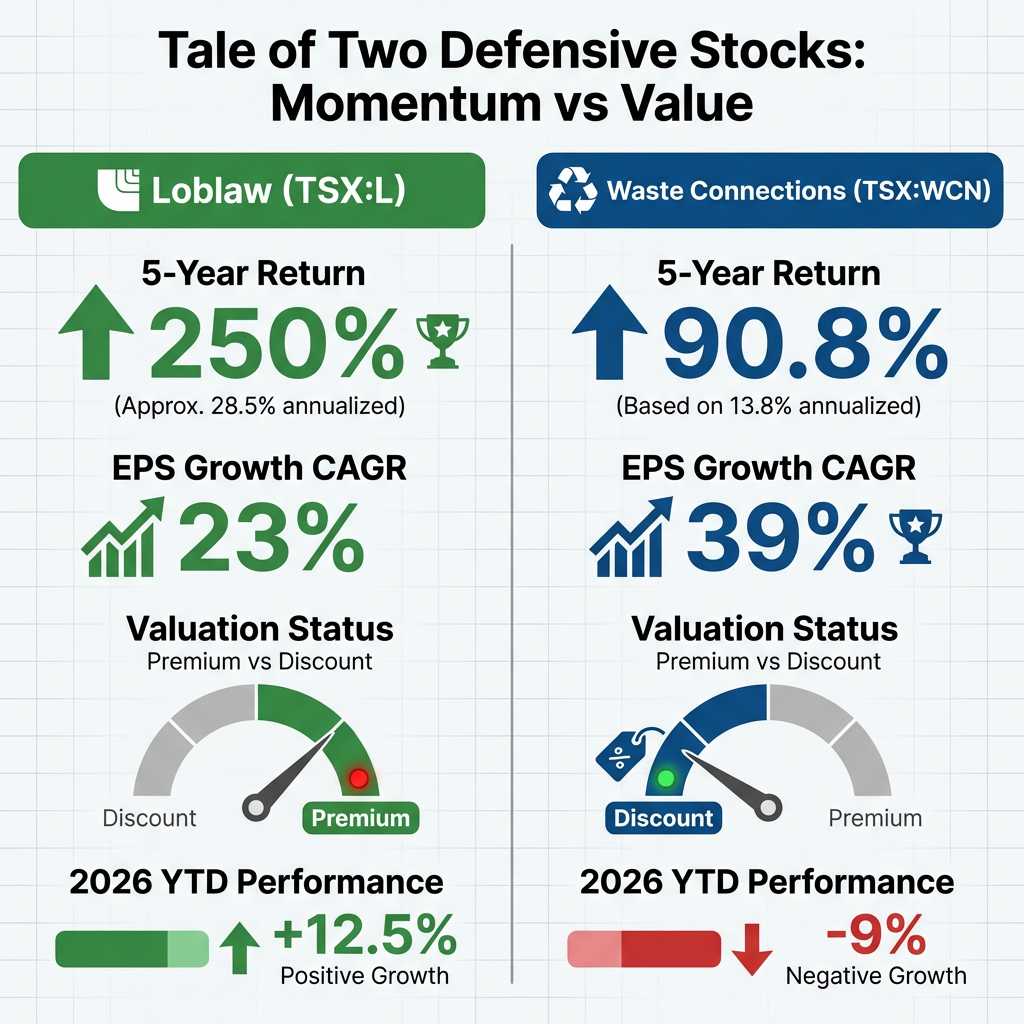

- Loblaw Companies (TSX:L) has delivered a 250% five-year price return with 23% EPS compounding, supported by a Moderate Buy analyst consensus and an average 12-month price target of C$92.63.

- Loblaw's current P/E of approximately 30 is substantially above its decade average of roughly 17, meaning investors are paying a significant premium for its defensive quality and growth trajectory.

- Waste Connections (TSX:WCN) has compounded earnings at 39% annually over five years and generated 13.8% annualised returns over a decade, but a California landfill remediation issue has driven a roughly 9% year-to-date decline in 2026, bringing its P/E near five-year lows.

- Loblaw's next earnings release is scheduled for 1 May 2026, while progress updates on Waste Connections' California landfill resolution represent the key near-term catalyst for that stock.

- Both stocks fulfil defensive portfolio roles through different mechanisms: Loblaw offers essential consumer goods exposure with current momentum, while Waste Connections presents a contrarian value opportunity in essential services.

Market turbulence in 2026 has intensified investor focus on stability. Canadian defensive stocks, anchored by essential services and consistent earnings, have emerged as portfolio protection vehicles amid elevated volatility. This analysis examines two prominent defensive options: Loblaw Companies (TSX:L), Canada’s grocery and pharmacy leader, and Waste Connections (TSX:WCN), an essential services provider navigating near-term headwinds.

Understanding defensive stocks and their market role

Defensive stocks provide goods or services with inelastic demand, meaning consumers purchase them regardless of economic conditions. Grocery retailers, waste management firms, utilities, and healthcare providers typically fall into this category because their revenue streams remain stable during recessions. These companies often deliver consistent dividends and exhibit lower price volatility than growth-oriented equities, though they may carry premium valuations during uncertain periods.

Key characteristics that define quality defensive holdings include:

- Essential service provision: Companies operate in sectors where demand persists through economic cycles (food retail, waste collection, energy distribution)

- Pricing power: Ability to pass input cost increases to customers without significant demand destruction

- Competitive moats: Structural advantages such as regulatory barriers, distribution networks, or market dominance that protect margins

- Dividend reliability: Track record of maintaining or growing distributions through downturns

- Stable revenue growth: Consistent top-line expansion driven by population growth, inflation, or market share gains rather than cyclical demand

Investors accept potentially higher valuations for defensive stocks during volatile periods because predictable cash flows and lower downside risk justify premium multiples. However, this premium can compress when market conditions stabilise and risk appetite returns.

Understanding broader strategies for navigating volatile markets can help investors position defensive stocks within a comprehensive portfolio approach that addresses both downside protection and opportunity capture.

When big ASX news breaks, our subscribers know first

Loblaw Companies (TSX:L): Canada’s grocery and pharmacy leader

Loblaw Companies dominates Canadian food retail and pharmacy operations, providing essential consumer goods that create inherent revenue stability. The grocery business offers partial inflation protection, as rising food prices flow through to revenues whilst volumes remain relatively resilient. Loblaw’s scale advantage, brand portfolio spanning discount to premium formats, and PC Optimum loyalty programme (Canada’s largest) reinforce competitive positioning.

The company’s financial performance demonstrates the defensive thesis in practice. Shares have delivered exceptional returns despite economic uncertainty.

| Metric | Value | Context |

|---|---|---|

| Market Capitalisation | $74.3B – $75.1B | Major Canadian equity |

| 5-Year Price Return | 250% | Significantly outpaced TSX Composite |

| EPS Growth (5-Year CAGR) | 23% | Earnings compounding well above inflation |

| Current P/E Ratio | ~30.2 | Trailing twelve months |

| Historical Average P/E | ~17 | Decade average for comparison |

| Dividend Yield | 0.89% | Modest yield reflects buyback focus |

Q4 2025 results, released 25 February 2026, highlighted continued momentum. Adjusted diluted net earnings per share reached C$0.67, whilst quarterly revenue hit C$15.70B with comparable sales advancing 3.5%. For the full 2025 fiscal year, total revenue climbed to C$63.90B (up 6.3%), and EPS surged to C$2.22 (up 26.7%). Management’s next earnings report is scheduled for 1 May 2026, providing updated guidance on Q1 2026 performance.

As detailed in the Financial Post’s coverage of Loblaw’s Q4 2025 results released 25 February 2026, adjusted diluted net earnings per share reached C$0.67, whilst quarterly revenue hit C$15.70B with comparable sales advancing 3.5%.

Loblaw’s competitive advantages extend beyond scale:

- Operational scale: Largest grocery and pharmacy network in Canada creates purchasing power and distribution efficiency

- Format diversity: Portfolio spans discount (No Frills), conventional (Loblaws), and premium (Fortinos) banners, capturing multiple customer segments

- Loyalty ecosystem: PC Optimum programme drives customer retention and provides valuable purchasing data

- Pricing leverage: Market position enables competitive pricing whilst maintaining margin discipline

- Geographic reach: National footprint limits regional economic exposure

Valuation presents a nuanced consideration for new investors. The current P/E ratio of approximately 30 sits substantially above the decade average of roughly 17, reflecting market recognition of quality and growth trajectory. This premium may limit multiple expansion opportunities, as further valuation increases would require sustained earnings growth to avoid appearing stretched. Analyst consensus remains Moderate Buy with an average 12-month price target of C$92.63, suggesting confidence in fundamental strength despite elevated multiples. The company allocates capital primarily to share buybacks (approximately 3.5% of shares repurchased annually since 2021) rather than aggressive dividend growth, which suits investors prioritising total return over income.

Investors seeking to assess whether Loblaw’s P/E ratio of approximately 30 versus its decade average of 17 represents excessive premium or justified quality may benefit from exploring valuation assessment frameworks for premium multiples used to evaluate market-leading companies.

Waste Connections (TSX:WCN): essential services with recovery potential

Waste Connections operates across the waste collection, transfer, disposal, and recycling value chain, providing services that maintain consistent demand regardless of economic conditions. Residential garbage collection continues during recessions, and commercial volumes exhibit relative stability compared to discretionary sectors. The company has historically combined organic growth with disciplined acquisitions, building a continent-wide platform with significant barriers to entry stemming from regulatory permits, landfill assets, and route density.

The investment thesis has delivered strong historical results, though 2026 has introduced near-term challenges.

| Metric | Value |

|---|---|

| Market Capitalisation | ~$56B |

| 10-Year Annualised Return | 13.8% |

| 5-Year Revenue CAGR | 11.7% |

| 5-Year EPS CAGR | 39% |

| 2026 YTD Performance | -9% (approximate) |

The California landfill environmental remediation issue has weighed on financial results for approximately two years, creating uncertainty around cost containment and resolution timelines. This operational headwind has pressured the share price despite the underlying defensive characteristics of the waste management business model. Resolution of the landfill matter would remove a significant overhang and could restore the historical growth trajectory that powered 39% annual EPS compounding over the past five years.

The California landfill environmental remediation issue, detailed in the California Environmental Protection Agency’s enforcement documentation, has weighed on financial results for approximately two years, creating uncertainty around cost containment and resolution timelines.

> Valuation Opportunity

> The approximately 9% year-to-date decline in 2026 has brought Waste Connections’ P/E ratio near five-year lows, potentially creating an attractive entry point for long-term investors willing to look through near-term operational challenges. The contrarian opportunity exists within a high-quality defensive name with proven compounding ability.

Investors evaluating Waste Connections must weigh the established track record (a decade of 13.8% annualised returns) against the uncertainty surrounding California landfill remediation costs and timing. The depressed valuation relative to historical norms suggests the market has priced in considerable pessimism, which could reverse if the company demonstrates progress toward resolution.

The next major ASX story will hit our subscribers first

Comparing Loblaw and Waste Connections for defensive exposure

| Criterion | Loblaw (TSX:L) | Waste Connections (TSX:WCN) |

|---|---|---|

| Current Momentum | Strong price appreciation, positive analyst revisions | YTD decline of ~9%, technical weakness |

| Valuation Status | P/E ~30 vs decade average ~17 (premium) | P/E near 5-year lows (discount) |

| Growth Trajectory | 23% EPS CAGR, accelerating earnings | Historical 39% EPS CAGR, near-term headwinds |

| Dividend Yield | 0.89% (buyback-focused capital allocation) | Data unavailable |

| Near-Term Catalysts | Q1 2026 earnings (1 May), analyst target ~C$92.63 | California landfill resolution progress |

| Risk Factors | Elevated valuation may limit multiple expansion | Remediation cost uncertainty, execution risk |

Momentum-oriented investors may gravitate toward Loblaw’s current strength, backed by analyst support and visible earnings growth. The stock offers exposure to defensive characteristics (essential food retail) whilst participating in a positive fundamental trajectory. However, the valuation premium means new investors are paying substantially more than historical norms, requiring confidence that 23% annual EPS growth can continue justifying elevated multiples.

Value-focused investors might find Waste Connections’ pullback attractive, particularly if they believe the California landfill issue represents a temporary rather than structural challenge. The ~9% year-to-date decline has created a potential entry point at depressed valuations for a company that compounded earnings at 39% annually over five years. This approach requires tolerance for near-term uncertainty and conviction that the defensive waste management model remains intact beneath operational noise.

Both stocks serve defensive portfolio allocation purposes through different mechanisms. Loblaw provides stability via essential consumer goods exposure with current momentum, whilst Waste Connections offers essential services exposure with contrarian value characteristics. Risk tolerance, investment timeline, and preference for momentum versus value positioning determine suitability.

Investment considerations and risk factors

Defensive stocks are not immune to market forces or company-specific challenges. Several risk factors warrant consideration when building defensive portfolio allocations:

- Valuation compression risk: Premium multiples paid during volatile periods can compress when market conditions stabilise and investors rotate toward growth or cyclical sectors. Loblaw’s P/E of approximately 30 versus a decade average near 17 illustrates this dynamic.

- Company-specific operational issues: Even defensive business models face execution challenges, as demonstrated by Waste Connections’ California landfill remediation costs impacting results for roughly two years.

- Interest rate sensitivity: Defensive stocks paying dividends can face pressure when bond yields rise, as fixed-income alternatives become more attractive. Rising rates also increase discount rates applied to future cash flows.

- Sector concentration risk: Overweighting defensive sectors creates portfolio imbalances that may underperform during economic expansions when cyclical stocks lead market gains.

- Currency exposure: For non-Canadian investors, exchange rate movements between the Canadian dollar and their home currency introduce additional volatility to returns.

Canadian investors focused on domestic defensive stocks may also benefit from understanding geographic diversification considerations, particularly as international equities have shown distinct performance patterns in 2025 and 2026.

Ongoing evaluation remains essential. Defensive positioning requires monitoring whether the stability premium justifies current valuations and whether company-specific fundamentals support the defensive thesis.

Canadian defensive stocks serve an important portfolio function during the volatile conditions characterising 2026. Loblaw Companies has delivered exceptional shareholder returns (250% over five years) through consistent execution in essential food retail, supported by analyst consensus ratings of Moderate Buy and an average price target of C$92.63. Waste Connections offers a decade of 13.8% annualised compounding with current valuation near five-year lows, creating potential opportunity for investors willing to navigate near-term landfill remediation uncertainty. Investment decisions should align with individual risk tolerance, time horizon, and portfolio context. Upcoming catalysts include Loblaw’s 1 May 2026 earnings release and progress updates on Waste Connections’ California landfill resolution, both warranting close monitoring.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What are Canadian defensive stocks and why do investors buy them?

Canadian defensive stocks are shares in companies providing essential goods or services with inelastic demand, such as grocery retail and waste management, that maintain stable revenues regardless of economic conditions. Investors buy them during volatile periods because predictable cash flows and lower price swings offer downside protection relative to growth or cyclical equities.

Is Loblaw Companies (TSX:L) a good defensive stock to buy in 2026?

Loblaw has delivered a 250% five-year price return and 23% EPS compounding, with analyst consensus rated Moderate Buy and an average 12-month price target of C$92.63. However, its current P/E of approximately 30 sits well above its decade average of roughly 17, meaning new investors are paying a significant premium for the quality.

What is the California landfill issue affecting Waste Connections (TSX:WCN)?

Waste Connections has faced an environmental remediation issue at a California landfill for approximately two years, creating uncertainty around cost containment and resolution timelines that has weighed on financial results and contributed to a roughly 9% year-to-date share price decline in 2026. Resolution of this matter could remove a significant overhang and potentially restore the company's historical growth trajectory.

How do I choose between Loblaw and Waste Connections for defensive exposure?

Loblaw suits momentum-oriented investors who prioritise current earnings strength and analyst support, while Waste Connections appeals to value-focused investors willing to tolerate near-term uncertainty in exchange for a potential entry point near five-year valuation lows. The right choice depends on individual risk tolerance, investment timeline, and preference for momentum versus contrarian value positioning.

What are the main risks of investing in defensive stocks?

Key risks include valuation compression when market conditions stabilise and investors rotate back to growth sectors, company-specific operational challenges such as environmental remediation costs, interest rate sensitivity that makes dividend-paying stocks less attractive when bond yields rise, and sector concentration that may cause defensive-heavy portfolios to underperform during economic expansions.