Domino’s Falls 9.6% to 52-Week Low After Q1 Miss on All Metrics

11 hrs ago

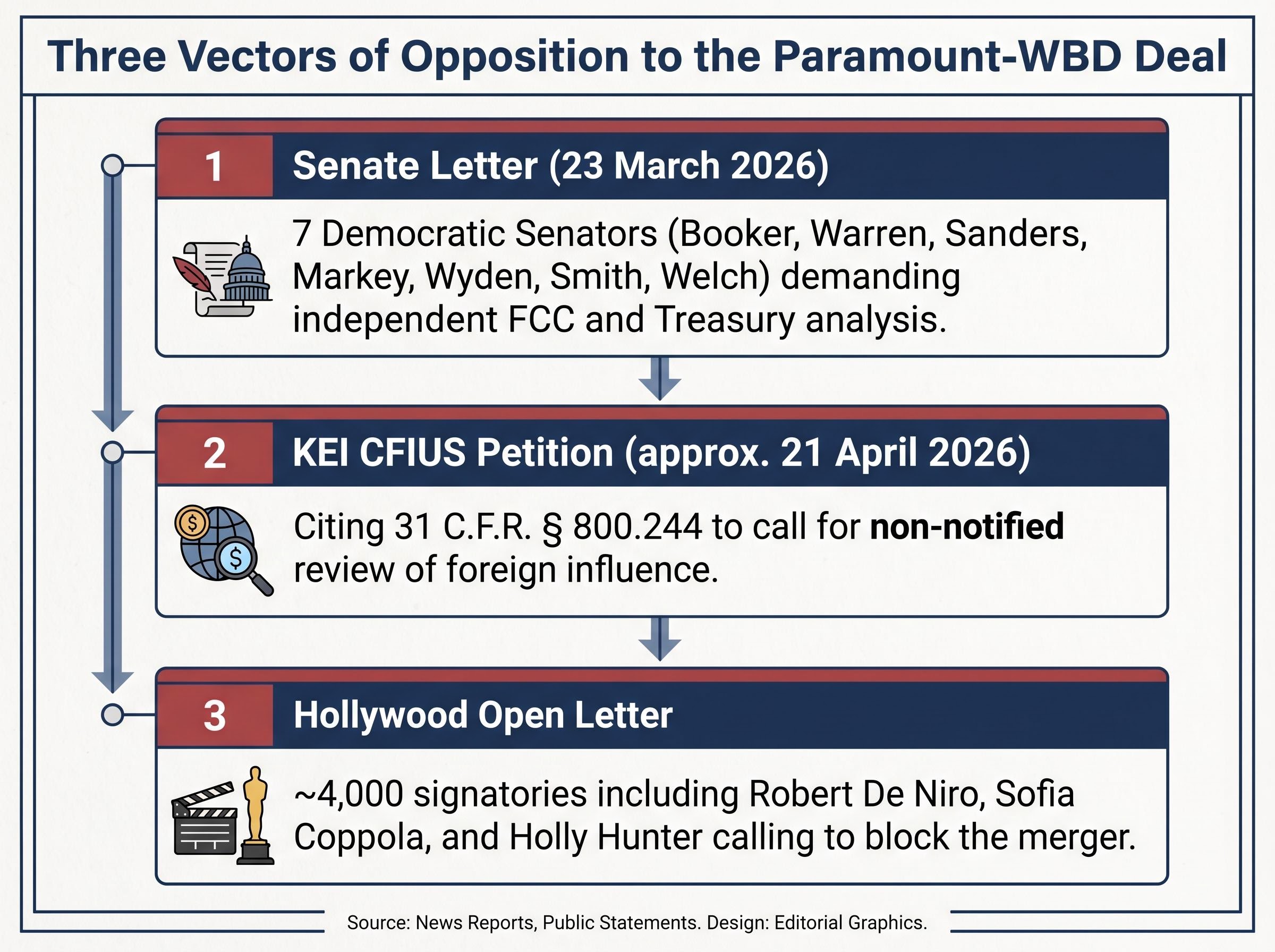

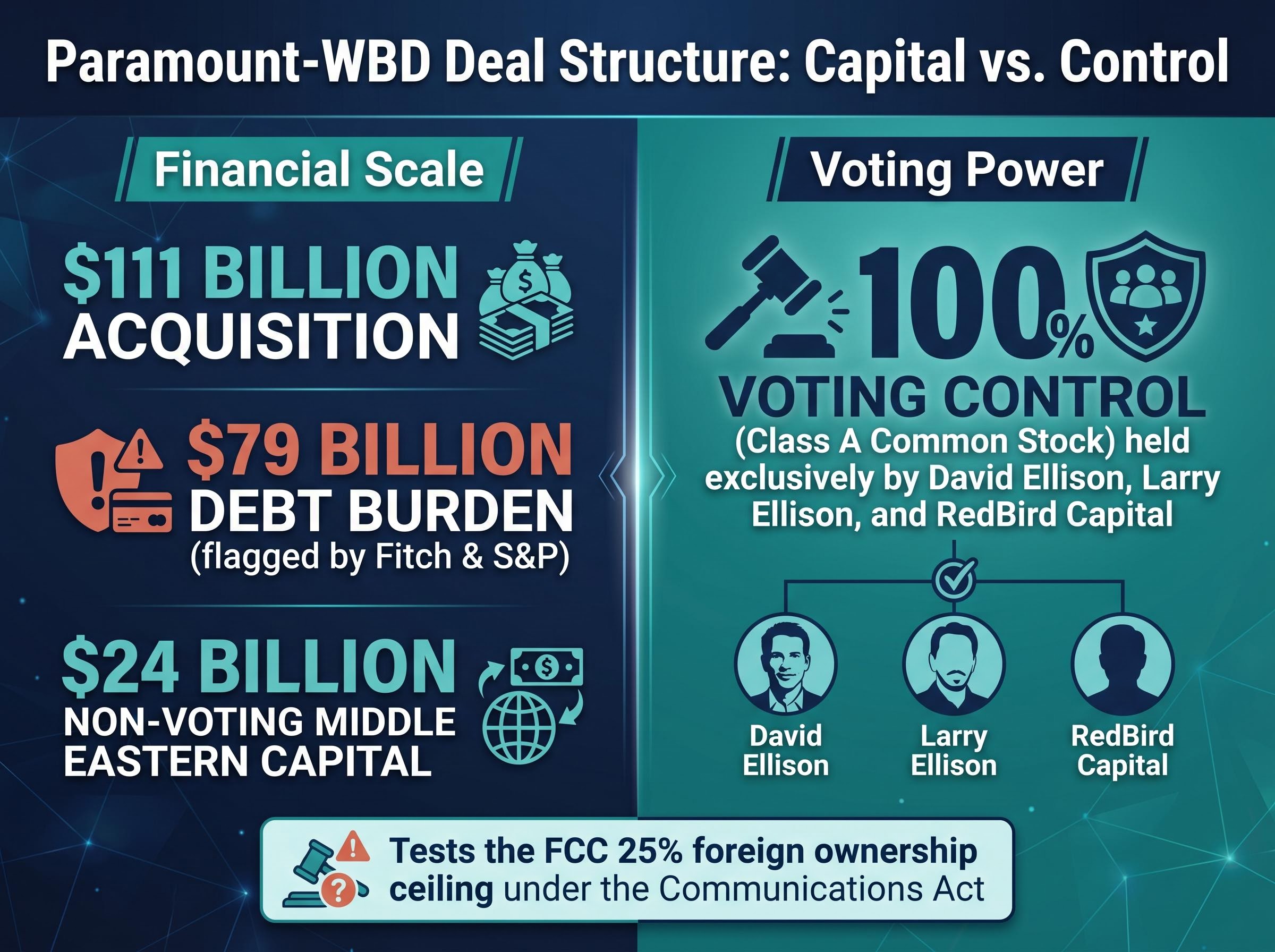

“`json { “fact_checked_full_article”: “Paramount has petitioned the Federal Communications Commission (FCC) to authorise $24 billion in Middle Eastern sovereign wealth fund capital as part of the approximately $111 billion acquisition of Warner Bros. Discovery, formally opening a regulatory process that will test the limits of U.S. broadcast ownership law. The petition, a declaratory ruling request signed by Paramount chief legal officer Makan Delrahim and addressed to FCC Chair Brendan Carr, arrives one week after WBD shareholders approved the transaction. What follows is an examination of what Paramount filed on 27 April 2026, who the foreign investors are, why the FCC’s 25% foreign ownership threshold is at the centre of the regulatory debate, and what organised opposition from senators, national security advocates, and the entertainment industry means for the deal’s path forward.\n\n## Understanding the FCC’s 25% foreign ownership rule and why this deal tests it\n\nThe U.S. Communications Act caps foreign equity and voting interests in entities holding FCC broadcast licences, such as CBS stations owned by Paramount, at 25%. Any transaction that would push foreign participation above that threshold requires explicit FCC authorisation through a declaratory ruling petition, which is the precise instrument Paramount filed today.\n\nThe deal’s architects argue the threshold is not triggered. All three sovereign wealth fund investments are structured as non-voting equity, meaning the foreign holders possess no voting control, no board seats, and no governance rights. Under this reading, the 25% cap applies only to voting interests, and the non-voting structure keeps the transaction compliant.\n\nCritics reject that interpretation. Knowledge Economy International (KEI), in a petition filed approximately 21 April 2026, argued that non-voting equity does not automatically escape scrutiny if the investment affords influence over a U.S. business, citing 31 C.F.R. § 800.211 in the Committee on Foreign Investment in the United States (CFIUS) context. The regulation specifies that passive, non-voting stakes may still fall within CFIUS oversight where such stakes confer meaningful influence over the target’s operations. Democratic senators have made a parallel argument under the Communications Act’s equity prong, contending that the statute’s language covers equity broadly, not only voting shares.\n\n> The FCC filing projects total indirect foreign ownership at nearly double the statutory 25% ceiling, a gap that explains why this petition exists and why its outcome is not a formality.\n\nTo secure approval, Paramount must satisfy a two-step test:\n\n1. Demonstrate that the non-voting structure does not confer prohibited influence over FCC-licensed broadcast operations\n2. Show that the foreign investment serves the public interest in those broadcast operations\n\nThe FCC has also tightened foreign ownership transparency disclosure requirements in recent years, adding a further layer of procedural scrutiny to any filing of this scale.\n\n## What Paramount filed with the FCC today, and why it matters\n\nThe petition is a formal request for a declaratory ruling, the mechanism by which broadcast licensees seek FCC authorisation for foreign equity participation above the statutory threshold. It was filed on 27 April 2026, signed by Makan Delrahim, and directed to FCC Chair Brendan Carr.\n\nParamount has characterised the filing as a standard procedural step rather than a precondition for deal closing. Simultaneously, the company submitted responses to Team Telecom, the interagency body that advises the FCC on national security and law enforcement concerns related to foreign participation in U.S. telecommunications.\n\nThe scope of the request is where the filing’s significance sharpens. Paramount is seeking authorisation permitting up to 100% of equity or voting shares to be held by foreign parties, a breadth the company describes as routine in declaratory ruling petitions but one that would grant the FCC-licensed entity maximum structural flexibility for foreign capital.\n\nThe three sovereign wealth funds contributing the $24 billion are:\n\n- Saudi Arabia’s Public Investment Fund (PIF), the kingdom’s primary sovereign investment vehicle\n- Abu Dhabi’s L’Imad, a newly consolidated sovereign wealth entity formed in January 2026 with approximately $300 billion in assets under management\n- Qatar Investment Authority (QIA), Qatar’s sovereign wealth fund\n\nAll three stakes are characterised as non-voting in the filing.\n\n> Makan Delrahim argued in the petition that reducing barriers to foreign investment would enable Paramount to expand and preserve its broadcast television operations, framing the sovereign wealth capital as supportive of the public interest.\n\n## The three sovereign wealth funds and how the ownership structure works\n\nThe $24 billion in foreign capital is distributed across three Gulf state sovereign wealth funds, each taking a non-voting equity position in the combined entity.\n\n

| Fund Name | Country | Voting Rights | AUM |

|---|---|---|---|

| Public Investment Fund (PIF) | Saudi Arabia | Non-voting | Not disclosed |

| L’Imad | Abu Dhabi (UAE) | Non-voting | ~$300 billion |

| Qatar Investment Authority (QIA) | Qatar | Non-voting | Not disclosed |

\n

\n\nL’Imad is the newest of the three, formed in January 2026 through a consolidation of Abu Dhabi sovereign wealth assets, including the absorption of peer fund ADQ. Its approximately $300 billion in assets under management makes it one of the largest sovereign wealth vehicles in the Gulf.\n\nThe FCC filing projects total indirect foreign ownership across all foreign holders, including passive investors in RedBird Capital funds and SEC Form 13F filers, at a level reportedly nearly double the statutory 25% ceiling, though this figure remains unverified pending primary source documentation. The three Gulf funds collectively represent the largest single bloc of foreign equity in the deal.\n\n### Who controls the votes\n\nVoting power sits entirely outside the sovereign wealth fund structure. Class A Common Stock, representing 100% of voting power, will be held exclusively by David Ellison, Larry Ellison, and RedBird Capital. No sovereign wealth fund receives board representation, governance rights, or any mechanism to influence corporate decision-making through the formal ownership structure.\n\nThe remaining foreign equity holders beyond the three Gulf funds are passive investors in RedBird funds and institutional holders identified through Form 13F filings, none of whom hold an active governance role.\n\nThis non-voting architecture is Paramount’s primary legal argument for why $24 billion in foreign capital does not breach the Communications Act’s 25% ceiling. It is also the argument that critics and regulators are most actively contesting.\n\n## Senate opposition and the national security challenge building around the deal\n\nOpposition to the deal is not confined to a single institution or argument. It is arriving from Congress, from national security policy organisations, and from the entertainment industry, each with a distinct legal or policy basis.\n\nA group of seven Democratic senators wrote to FCC Chair Brendan Carr on 23 March 2026, calling for a thorough, independent FCC review to be completed before any approval could be granted. The signatories:\n\n- Cory Booker\n- Elizabeth Warren\n- Bernie Sanders\n- Ed Markey\n- Ron Wyden\n- Tina Smith\n- Peter Welch\n\nTheir core demands included scrutiny of the $24 billion in Gulf capital, transparency about whether additional undisclosed foreign capital is involved, and an explicit rejection of what they characterised as fast-tracking with limited oversight. The senators also wrote separately to the U.S. Treasury, pressing CFIUS to open its own independent review of the transaction.\n\nThree distinct opposition vectors have now formalised:\n\n- Senate letter (23 March 2026): Demanded independent FCC analysis and questioned whether the non-voting structure genuinely insulates broadcast operations from foreign influence\n- KEI CFIUS petition (approximately 21 April 2026): Contended that the transaction amounts to a foreign government-controlled investment within the meaning of 31 C.F.R. § 800.244 and called on CFIUS to open a non-notified review\n- Hollywood open letter: Approximately 4,000 signatories, including Robert De Niro, Sofia Coppola, and Holly Hunter, called for the merger to be blocked, per Variety\n\nIn March 2026, FCC Chair Carr described the deal as \”cleaner\” relative to earlier media transactions and indicated approval was expected to come \”quickly.\” As of 27 April 2026, no public response from the FCC, CFIUS, or the White House to any of the opposition filings had been confirmed.\n\n### The CFIUS dimension: when \”non-voting\” may not be enough\n\nThe reach of CFIUS authority is not limited to voting equity stakes. The regulation at 31 C.F.R. § 800.211 makes clear that non-voting investments can remain subject to review where the foreign party retains the ability to influence the operations of a U.S. business. KEI’s petition argues that sovereign wealth fund participation in a company controlling CBS News and CNN meets precisely this threshold.\n\nA parallel letter sent by the senators to the U.S. Treasury pressed CFIUS to proceed on its own track, separate from whatever the FCC decides. As of 27 April 2026, no CFIUS review had been publicly announced or confirmed.\n\nThe accumulation of opposition from multiple independent directions, congressional, regulatory, and cultural, suggests the regulatory path for this deal is more contested than the FCC Chair’s public framing indicates.\n\n## What comes next for the Paramount FCC petition\n\nParamount’s 27 April petition formally opens the regulatory clock on foreign ownership review for the $111 billion Warner Bros. Discovery acquisition. The non-voting equity structure remains the legal linchpin: if accepted, it clears the 25% foreign ownership threshold; if challenged successfully, the $24 billion capital structure may require restructuring or conditions.\n\nThe milestones to watch are the FCC’s formal response to the declaratory ruling petition, any CFIUS action prompted by the KEI petition or the Senate Treasury letter, and whether the deal’s debt burden (approximately $79 billion, flagged by Fitch and S&P) adds further complexity to the regulatory timeline. As of 27 April 2026, neither Paramount, Warner Bros. Discovery, nor the Trump administration has publicly responded to any of the opposition filings.\n\nInvestors and industry observers tracking the transaction’s regulatory progress can monitor FCC Electronic Comment Filing System (ECFS) docket filings and CFIUS public notices for the next formal developments.\n\n> This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.\n\n> Forward-looking statements regarding regulatory outcomes, deal timelines, and approval prospects are speculative and subject to change based on regulatory decisions, political developments, and market conditions.\n\n—\n\n—” } “`

Team Telecom’s national security review window carries a statutory ceiling of 120 days with a possible 30-day extension, making it a longer and less predictable clock than the FCC’s own deliberation on the declaratory ruling petition, and the interagency body’s conclusions on the Gulf funds could impose conditions that reshape the ownership structure regardless of what the Commission decides on the foreign equity question.

The public interest case Paramount has built around the foreign capital goes beyond governance arguments: the company has tied its petition directly to the structural decline in linear television revenue, pointing to cable subscriber counts falling from roughly 105 million in 2010 to approximately 68.7 million in 2026 as evidence that sovereign wealth capital is necessary to sustain broadcast investment.

The 31 C.F.R. Part 800 regulations governing CFIUS covered investments define the scope of Treasury review authority, including the provisions under Section 800.211 that extend oversight to non-voting or passive equity positions where the foreign party retains any access to material non-public information or the ability to influence operational decisions of the U.S. business.

The 47 CFR Part 1 Subpart T foreign ownership rules for broadcast licensees codify both the 25% statutory ceiling under Section 310(b)(4) of the Communications Act and the declaratory ruling petition mechanism that broadcast licensees must use when seeking FCC authorisation to exceed that threshold, making them the precise regulatory framework within which Paramount’s filing operates.

Paramount FCC approval refers to the declaratory ruling the Federal Communications Commission must grant before foreign equity exceeding the statutory 25% threshold can be held in entities controlling FCC broadcast licences such as CBS. Without this ruling, the $111 billion acquisition of Warner Bros. Discovery cannot proceed with its current $24 billion Gulf sovereign wealth fund capital structure intact.

Three Gulf state sovereign wealth funds are contributing the $24 billion in foreign equity: Saudi Arabia's Public Investment Fund (PIF), Abu Dhabi's L'Imad (formed in January 2026 with approximately $300 billion in assets under management), and Qatar's Qatar Investment Authority (QIA). All three stakes are structured as non-voting equity with no board seats or governance rights.

The U.S. Communications Act caps foreign equity and voting interests in broadcast licence holders at 25%, and any transaction pushing foreign participation above that level requires explicit FCC authorisation via a declaratory ruling petition. Paramount argues its non-voting structure keeps the deal compliant, but critics and Democratic senators contend the statute's equity prong covers non-voting shares as well.

Seven Democratic senators, including Cory Booker, Elizabeth Warren, Bernie Sanders, Ed Markey, Ron Wyden, Tina Smith, and Peter Welch, wrote to FCC Chair Brendan Carr on 23 March 2026 demanding independent review and transparency around the Gulf capital. They also separately pressed CFIUS at the U.S. Treasury to open its own review of the transaction.

Investors should monitor FCC Electronic Comment Filing System (ECFS) docket filings for the Commission's formal response to Paramount's declaratory ruling petition, any CFIUS action triggered by the KEI petition or the Senate Treasury letter, and whether the deal's approximately $79 billion debt burden flagged by Fitch and S&P adds further complexity to the regulatory timeline.