How Social Security Spousal Benefits Can Boost Household Income

Key Takeaways

- Married individuals can receive up to 50% of their spouse's primary insurance amount in spousal benefits when claimed at full retirement age, making strategic timing critical to maximising household retirement income.

- Claiming spousal benefits before full retirement age results in permanent reductions — as steep as 35% less per month for those who claim at 62 with an FRA of 67.

- The 2015 Bipartisan Budget Act introduced deemed filing rules that eliminate the option to claim spousal benefits only for anyone born after January 1, 1954, closing off strategies many retirees still mistakenly plan around.

- Delaying the higher earner's Social Security claim beyond full retirement age increases their PIA by 8% per year until age 70, boosting both spousal and survivor benefits based on their record.

- The Government Pension Offset can reduce or eliminate spousal benefits for public sector workers, making it essential for former teachers, police officers, and firefighters to factor GPO rules into their retirement planning.

Understanding social security spousal benefits can significantly impact your household retirement income. These benefits allow married individuals to receive up to 50% of their spouse’s primary insurance amount (PIA) when claimed at full retirement age, providing crucial support for couples where one partner earned substantially less or didn’t work outside the home. With strategic planning, couples can optimise their combined Social Security income and maximise lifetime benefits.

What Are Social Security Spousal Benefits?

Social security spousal benefits provide a safety net for married couples by allowing the lower-earning spouse to claim retirement benefits based on their partner’s work record. This programme addresses income disparities that often exist when one spouse spent years caring for children, worked part-time, or earned significantly less throughout their career. The benefit calculation centres on the higher earner’s primary insurance amount, the monthly benefit a worker receives if they claim at full retirement age.

Three fundamental facts define how spousal benefits work:

- Maximum benefit equals 50% of your spouse’s primary insurance amount when you claim at full retirement age

- You may qualify even if you have no work history or limited Social Security credits

- Your spouse must have filed for their own retirement benefits before you can claim spousal benefits

The spousal benefit represents a separate calculation from your own retirement benefit. If you’ve earned Social Security credits through your own work, the Social Security Administration (SSA) compares both amounts and typically pays the higher of the two, plus any applicable spousal top-up.

Now that you understand what spousal benefits are, let’s examine exactly who qualifies and the specific requirements you must meet.

When big ASX news breaks, our subscribers know first

Who Is Eligible for Social Security Spousal Benefits?

Eligibility requirements for social security spousal benefits follow clear guidelines, though special circumstances can affect qualification. Most married individuals approaching retirement age need to verify they meet basic thresholds before claiming. Understanding these requirements helps couples plan their claiming strategy effectively.

Core eligibility criteria include:

- Age requirement: You must be at least 62 years old, OR be caring for a child under age 16 or a disabled child who receives Social Security benefits

- Marriage duration: You must have been married to your spouse for at least one continuous year

- Spouse’s filing status: Your spouse must have already filed for their own Social Security retirement benefits

- Caregiving exception: If you’re caring for a qualifying child, you can claim spousal benefits at any age and receive the full 50% with no reduction

Divorced spouses face different requirements but may still qualify for benefits based on their former partner’s work record. The marriage must have lasted at least 10 years, and you must currently be unmarried and at least 62 years old. Your former spouse doesn’t need to have filed for benefits, only be eligible to receive them. Importantly, claiming benefits on your ex-spouse’s record doesn’t affect their benefit amount or any benefits their current spouse may receive.

These eligibility rules apply uniformly across the United States. There are no state-by-state variations in spousal benefit requirements or calculation methods.

Meeting eligibility requirements is just the first step. Understanding how your benefit amount is calculated will help you make informed decisions about when to claim.

How Social Security Spousal Benefits Are Calculated

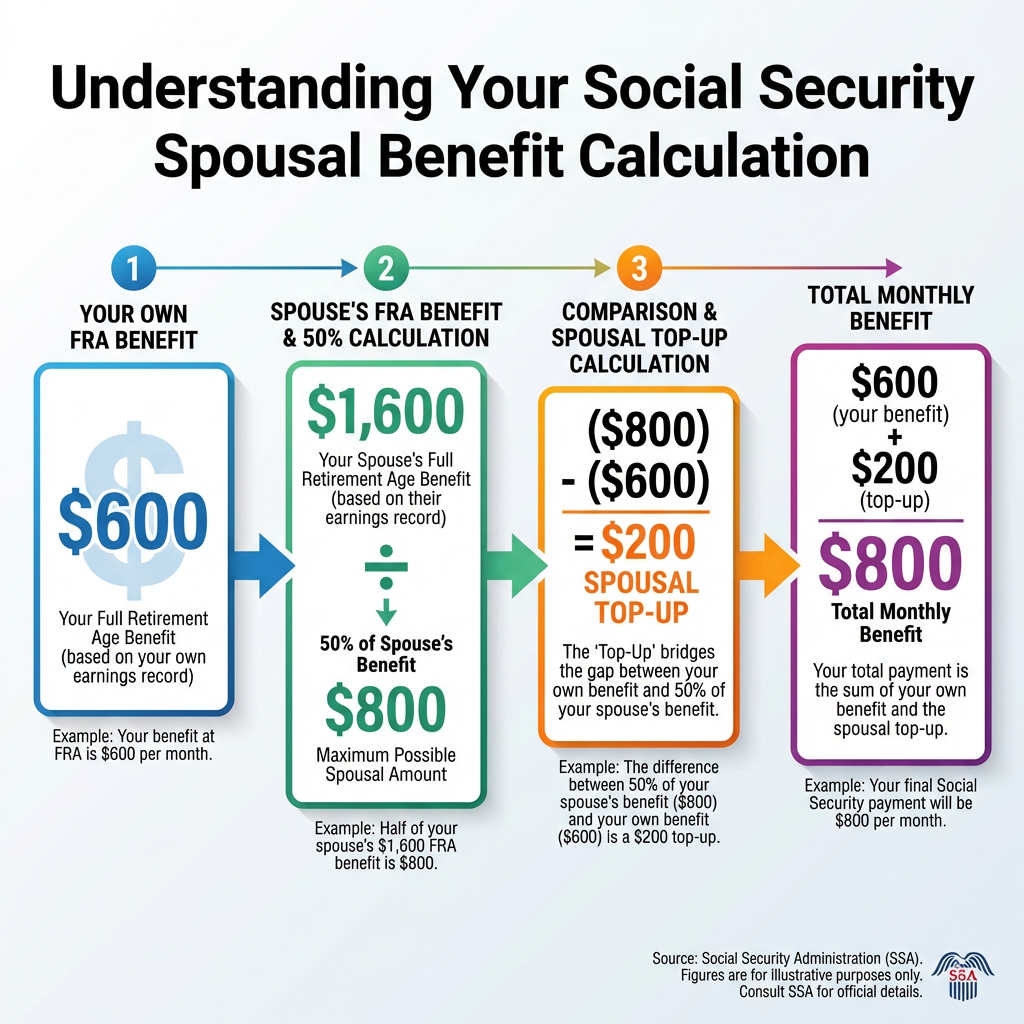

The calculation of social security spousal benefits involves specific formulas that determine your monthly payment. Your actual benefit depends on your claiming age and whether you’re entitled to retirement benefits based on your own work record. The Social Security Administration applies a spousal top-up formula to determine the final amount you receive.

The core formula works as follows: Your spousal benefit = (½ of spouse’s FRA benefit) – (Your own FRA benefit). If this calculation results in zero or a negative number, you receive only your own retirement benefit with no spousal supplement. This formula ensures you always receive the higher of the two benefit amounts.

> Key Concept: The spousal top-up formula means you first receive your own retirement benefit, then SSA adds any additional amount needed to bring your total up to the spousal benefit level. You cannot receive both benefits as separate, full payments.

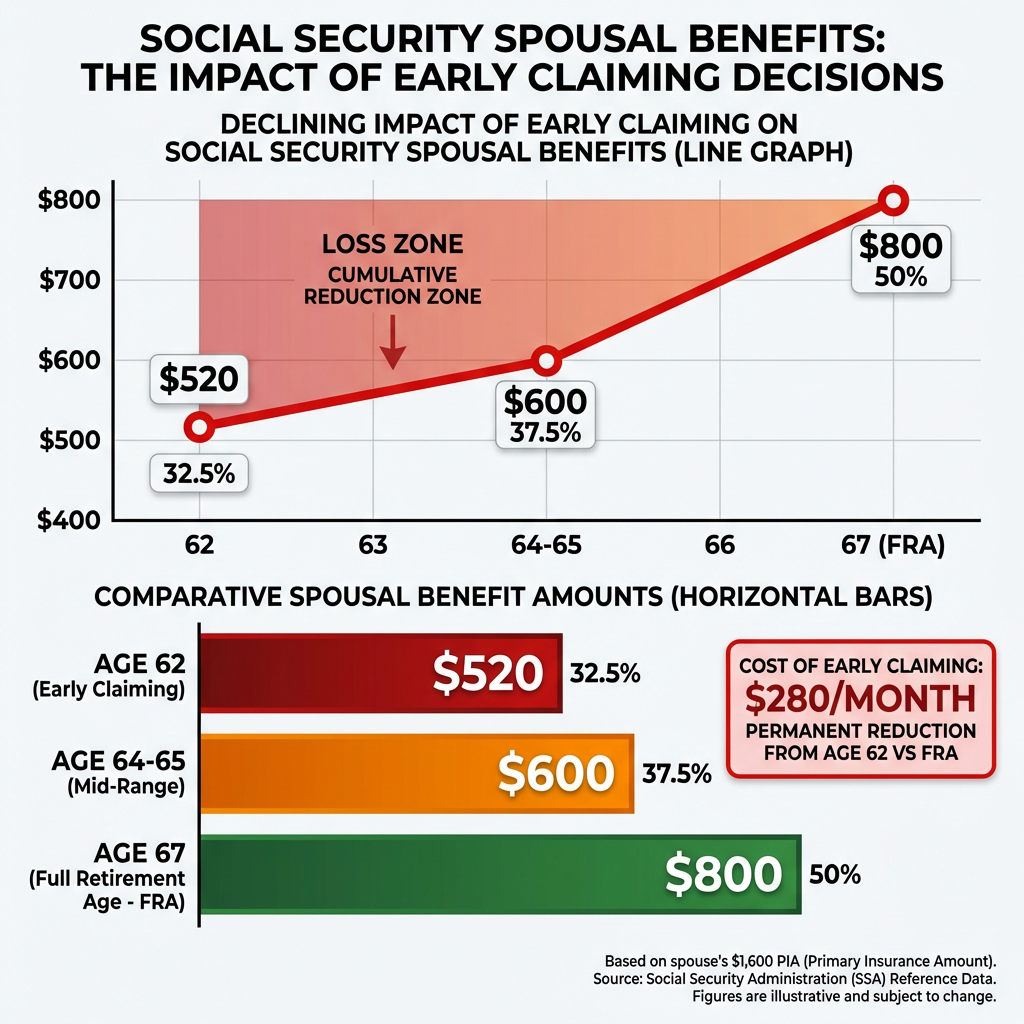

Claiming spousal benefits before your full retirement age permanently reduces the amount you receive. SSA applies reduction factors of 25/36 of 1% per month for the first 36 months before FRA (approximately 6.67% per year), then 5/12 of 1% per month for any additional early months (approximately 5% per year). These reductions compound, significantly lowering benefits for those who claim at 62.

The Social Security Administration provides detailed technical formulas for calculating early claiming reductions. SSA’s official spousal benefit reduction calculator shows precisely how the 25/36 of 1% monthly reduction applies for the first 36 months before FRA, followed by 5/12 of 1% for additional months.

| Claiming Age | Months Before FRA | Percentage of Spouse’s PIA | Monthly Benefit (on $1,600 PIA) |

|---|---|---|---|

| Full Retirement Age | 0 | 50% | $800 |

| 3 years before FRA | 36 | 37.5% | $600 |

| Age 62 (FRA 67) | 60 | 32.5% | $520 |

The table demonstrates the significant cost of early claiming. A spouse entitled to $800 monthly at full retirement age would receive only $520 if claiming at 62 with an FRA of 67, a permanent reduction of $280 per month or 35% of the full benefit.

The calculation becomes more complex when you’re eligible for both your own retirement benefit and spousal benefits simultaneously. That’s where deemed filing rules come into play.

Understanding Deemed Filing Rules: What Changed After 2016

Many individuals approaching retirement encounter outdated advice about claiming strategies that no longer apply. The 2015 Bipartisan Budget Act fundamentally changed how social security spousal benefits work for anyone born after January 1, 1954. These deemed filing rules eliminated the option to file a restricted application for spousal benefits only, preventing most couples from using strategies their parents may have employed.

Can I file for spousal benefits only and let my own benefit grow?

If you were born after January 1, 1954, no. Deemed filing means when you apply for any retirement benefit, SSA automatically considers you applying for all benefits you’re eligible for and pays the higher amount. You cannot strategically delay claiming one benefit type while collecting another. The system compares your own retirement benefit against any spousal benefit you qualify for, then pays the larger total amount automatically.

Key implications of deemed filing include:

- Applies to anyone born after January 1, 1954 (those who reached age 62 after 2016)

- Filing for your own retirement benefit automatically triggers a spousal benefit application if your spouse has already filed

- Filing for spousal benefits automatically triggers your own retirement benefit application

- SSA compares both benefits and pays you the higher amount (you don’t choose)

Only individuals born on or before January 1, 1954 retain the ability to file a restricted application for spousal benefits only upon reaching full retirement age. This allows them to claim spousal benefits whilst their own retirement benefit continues growing through delayed retirement credits until age 70. For everyone else, deemed filing applies universally.

With deemed filing in mind, let’s explore practical strategies couples can use to maximise their combined Social Security income.

Strategies to Maximise Your Spousal Benefits

Strategic claiming decisions significantly impact lifetime household benefits, even within the constraints of deemed filing rules. Couples with earnings disparities, age gaps, or specific cash flow needs can optimise their combined Social Security income through careful timing and coordination. The key lies in understanding how one spouse’s decisions affect the other’s benefits.

Actionable optimisation strategies include:

- Have the higher earner delay claiming: Each year past FRA increases their PIA by 8% until age 70, boosting both their benefit and any future spousal or survivor benefits based on their record

- Consider early claiming for the lower earner if needed: If the lower earner’s own benefit is small and cash flow is needed, claiming early may make sense (run the numbers using SSA calculators)

- Account for age gaps: If the higher earner is younger, the lower earner cannot claim spousal benefits until the higher earner files (or reaches FRA)

- Don’t delay spousal benefits past FRA: Unlike your own retirement benefit, spousal benefits don’t earn delayed retirement credits (the 50% maximum is reached at FRA)

A common scenario illustrates these principles in action. Consider a wife who claimed her own reduced retirement benefit at 62 whilst her younger, higher-earning husband continued working. When he files for his benefits at 67, she becomes eligible for a spousal top-up. Under deemed filing, she’s already locked into her reduced own benefit rate, but SSA will automatically add any spousal top-up she qualifies for based on the formula: (½ of husband’s FRA benefit) – (her own FRA benefit). If this calculation yields a positive number, her total monthly payment increases to reflect the spousal supplement.

The strategic value of delaying the higher earner’s claim extends beyond immediate spousal benefits. A larger PIA also increases the surviving spouse’s benefit in the event of death, potentially providing significantly more income security over a lifetime. According to financial planning research, this approach often maximises total household benefits for couples with substantial earnings gaps.

Implementing these strategies requires accurate information about your potential benefits. SSA provides several online tools specifically designed to help couples model their options.

Using SSA Tools to Calculate Your Spousal Benefits

The Social Security Administration provides free, accurate online calculators specifically designed for spousal benefit planning. Financial advisors recommend SSA’s my Social Security account for personalised estimates over third-party calculators, as it draws directly from your actual earnings record rather than relying on estimates or assumptions.

| SSA Tool | What It Does | Best Used For |

|---|---|---|

| my Social Security Spouse Estimates | Personalised estimates using your earnings record; enter spouse’s FRA benefit to see spousal amounts | Most accurate personal planning |

| Benefits for Spouses Calculator | Computes early retirement reductions as percentage of worker’s PIA | Understanding early claiming impact |

| Quick Calculator | Rough estimates for ages 62-70 with adjustable earnings | Initial planning and comparisons |

| Online Calculator | Precise projections using complete earnings history | Detailed retirement planning |

To use these tools effectively, create a my Social Security account at ssa.gov if you haven’t already. Once logged in, access your benefit estimates and use the spouse benefit feature by entering your spouse’s estimated FRA benefit amount. The system allows you to compare claiming at different ages, showing how early claiming reductions affect your monthly payment. Financial planners recommend running multiple scenarios, particularly testing what happens if the higher earner delays to 70 versus claiming at full retirement age.

Third-party calculators from providers like NerdWallet can supplement SSA’s tools but should not replace them for final planning decisions. SSA’s official calculators reflect current programme rules, including deemed filing requirements and the latest reduction formulas, ensuring your estimates align with what you’ll actually receive.

Beyond the standard rules, there are several special situations that can affect spousal benefits in unexpected ways.

The next major ASX story will hit our subscribers first

Special Situations: Divorce, Working While Collecting, and Government Pensions

Standard spousal benefit rules apply to most married couples approaching retirement, but several special circumstances require additional consideration. These situations won’t affect everyone but carry significant implications for those they impact. Understanding these exceptions helps avoid unexpected benefit reductions or missed claiming opportunities.

Three key special situations include:

- Divorced spouse benefits: Marriage must have lasted at least 10 years, you must be currently unmarried and age 62+, and your ex must be eligible for benefits (doesn’t need to have filed if divorced 2+ years)

- Working while collecting: If you claim before FRA and earn above the annual limit, benefits are temporarily reduced (but you get credit back after reaching FRA)

- Government Pension Offset (GPO): If you receive a pension from work not covered by Social Security (certain government jobs), your spousal benefit may be reduced by two-thirds of your pension amount

The Government Pension Offset particularly affects former teachers, firefighters, police officers, and other public employees whose positions weren’t covered by Social Security. If you receive a government pension of $1,500 monthly, SSA would reduce your spousal benefit by $1,000 (two-thirds of $1,500). This offset can eliminate spousal benefits entirely for those with substantial government pensions.

The Government Pension Offset rules can be complex, particularly regarding which specific government positions and pension types trigger the offset. SSA’s Government Pension Offset publication provides comprehensive regulatory details on how the two-thirds reduction formula applies across different categories of government employment.

Benefits are uniform nationwide. There are no state-by-state variations in spousal benefit rules, calculation methods, or amounts. This consistency simplifies planning for couples who may relocate in retirement or who have worked in multiple states throughout their careers.

Conclusion

Social security spousal benefits provide essential retirement income support for millions of American couples, offering up to 50% of the higher earner’s benefit when claimed strategically. Understanding eligibility requirements, calculation formulas, and deemed filing rules empowers you to make informed claiming decisions that maximise your household’s lifetime benefits. The spousal top-up formula, early claiming reductions, and coordination strategies all play crucial roles in optimising your retirement income.

Use SSA’s official online tools, particularly the my Social Security account, to model different claiming scenarios based on your actual earnings record. Consider consulting a qualified financial adviser to evaluate your specific situation, especially if you face special circumstances like divorce, government pensions, or significant age gaps. Strategic planning today can translate into thousands of additional dollars over your retirement years.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What are social security spousal benefits?

Social security spousal benefits allow a married individual to receive up to 50% of their spouse's primary insurance amount (PIA) when claimed at full retirement age, providing retirement income support for those who earned less or did not work outside the home.

How much will I receive in Social Security spousal benefits if I claim early?

Claiming spousal benefits before your full retirement age permanently reduces the amount — for example, claiming at age 62 with an FRA of 67 reduces your benefit to just 32.5% of your spouse's PIA, compared to the maximum 50% available at FRA.

Can I collect spousal benefits only and let my own Social Security benefit grow?

If you were born after January 1, 1954, deemed filing rules prevent this strategy — when you apply for any Social Security benefit, the SSA automatically applies you for all benefits you are eligible for and pays the higher amount.

Do divorced spouses qualify for Social Security spousal benefits?

Yes, divorced spouses may qualify if the marriage lasted at least 10 years, they are currently unmarried, at least 62 years old, and their former spouse is eligible for Social Security benefits — and claiming on an ex-spouse's record does not affect that person's benefit amount.

How does the Government Pension Offset affect spousal benefits?

If you receive a pension from a government job not covered by Social Security, the Government Pension Offset (GPO) reduces your spousal benefit by two-thirds of your pension amount, which can significantly reduce or even eliminate your spousal benefit entirely.