Morgan Stanley Elevates Affirm to Top Pick, Sees 27% Upside

Key Takeaways

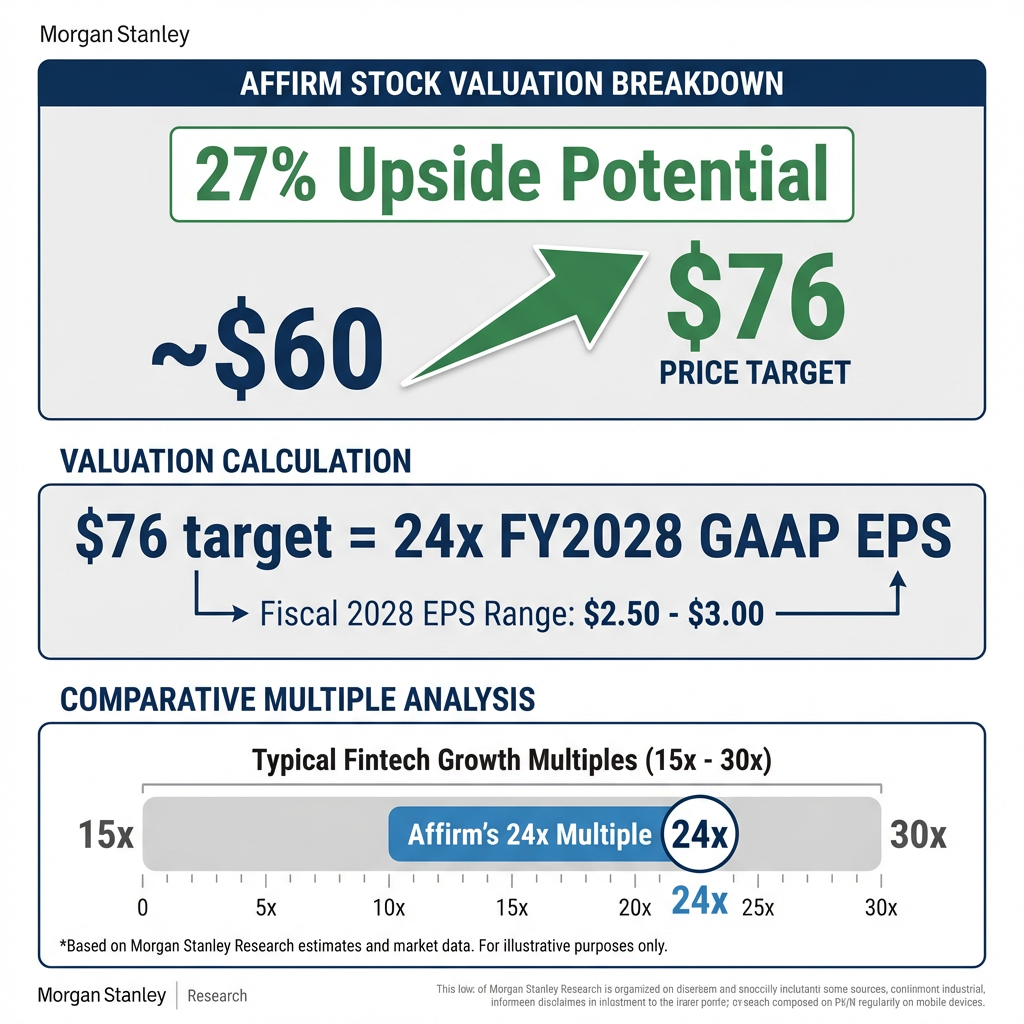

- Morgan Stanley elevated Affirm to Top Pick status on April 17, 2026, with a $76 price target implying approximately 27% upside from recent trading levels.

- Analyst James Faucette views private credit concerns as overdone, with improving ABS funding conditions and tightening spreads supporting Affirm's business model.

- Morgan Stanley expects Affirm to sustain GMV growth above 30% while achieving fiscal 2028 GAAP EPS of $2.50-$3.00, a target the firm considers conservative.

- The May 2026 Investor Forum is identified as the key near-term catalyst, where management disclosures on margins and growth could trigger broader analyst estimate revisions.

- Affirm shares rose 3.5% in premarket trading following the upgrade, reflecting the market's positive reaction to Morgan Stanley's highest conviction fintech call.

Affirm Holdings (AFRM) shares jumped 3.5% in premarket trading on Thursday, April 17, 2026, after Morgan Stanley elevated the buy-now-pay-later (BNPL) provider to Top Pick status with a $76 price target. The upgrade, issued by analyst James Faucette, signals the firm’s highest conviction call in the fintech sector and implies 27% upside from recent trading levels. This marks an escalation of Morgan Stanley’s bullish stance, following an earlier upgrade to Overweight in February 2026.

The Affirm stock upgrade reflects improving market conditions for BNPL operators and rising confidence in the company’s ability to sustain rapid growth whilst expanding profitability. Morgan Stanley’s move positions Affirm as a top investment idea ahead of a critical investor event in May 2026.

Morgan Stanley upgrades Affirm to Top Pick, shares jump

Morgan Stanley upgraded Affirm to Top Pick status on April 17, 2026, elevating the stock above its standard Overweight rating. Analyst James Faucette set a $76 price target, representing approximately 27% upside based on current trading levels. The target implies a valuation of roughly 24 times fiscal 2028 GAAP earnings per share, which the firm views as reasonable given Affirm’s growth trajectory and improving unit economics.

Morgan Stanley’s target implies a valuation of roughly 24 times fiscal 2028 GAAP earnings per share. To assess whether this premium is justified, investors should consider broader market valuation context, particularly given current rotation dynamics favoring profitable growth over pure expansion.

Shares rose 3.5% in premarket trading following the announcement. The upgrade comes as Morgan Stanley positions Affirm as its highest conviction idea within the BNPL and fintech sectors, reflecting optimism about the company’s funding environment and upcoming catalysts.

When big ASX news breaks, our subscribers know first

What a Top Pick rating means for investors

Morgan Stanley’s rating system includes Underweight, Equal-Weight, and Overweight as primary categories. Top Pick sits above Overweight as the firm’s highest conviction designation within a sector, reserved for stocks the analyst believes offer the best risk-reward profile among coverage. This signals stronger conviction than a standard Buy or Overweight call.

Morgan Stanley had previously upgraded Affirm from Equal-Weight to Overweight on February 3, 2026. The move to Top Pick represents an escalation of bullish sentiment rather than a fresh positive turn, indicating that the analyst sees improving fundamentals and near-term catalysts that could drive the stock significantly higher.

The bull case: why Morgan Stanley is betting big

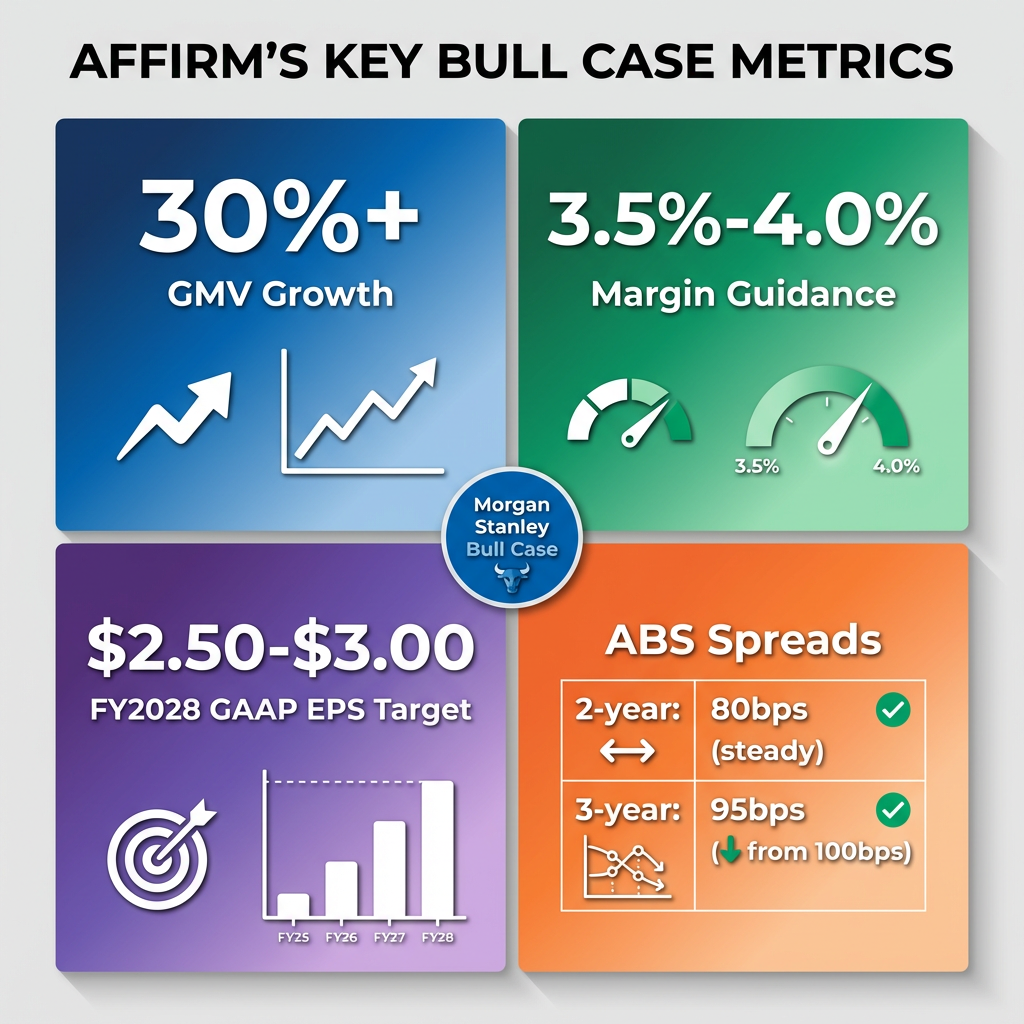

Faucette’s core thesis centres on the view that private credit concerns weighing on BNPL stocks are overdone. According to Morgan Stanley’s analysis, even weaker competitors successfully raised capital intra-quarter, suggesting healthy market conditions for quality operators. The firm expects Affirm to sustain 30% or higher gross merchandise value (GMV) growth whilst improving profitability metrics.

Key drivers supporting the bullish case include:

- Sustained GMV growth above 30%, demonstrating resilient consumer demand and merchant adoption

- Raised margin guidance for retained loan and transaction margins to the 3.5%-4.0% range

- Fiscal 2028 GAAP EPS target of $2.50-$3.00, which Morgan Stanley views as conservative and likely to be revised upwards

- Anticipated estimate revisions across the analyst community following improved disclosures

The $76 price target implies approximately 24 times fiscal 2028 GAAP EPS, a valuation Morgan Stanley considers reasonable given the combination of sustained high growth and expanding margins. The firm believes improving unit economics and favourable funding conditions position Affirm to exceed current market expectations.

Funding conditions show improvement

Funding conditions are critical for BNPL companies like Affirm, which rely on asset-backed security (ABS) markets and forward flow arrangements to finance loan portfolios. Spreads directly impact profitability, as tighter spreads translate to lower funding costs and better margins. Morgan Stanley’s analysis shows quantifiable improvement in the ABS funding environment.

The improving funding conditions Morgan Stanley cites are evident across global markets, with recent asset-backed security (ABS) markets showing record investor participation and tightening spreads for quality consumer lenders.

| ABS Tranche | Current Spread | Trend |

|---|---|---|

| Two-year | 80 basis points | Holding steady |

| Three-year | 95 basis points | Tightened from 100bps |

Morgan Stanley observed that peers with weaker credit performance still raised forward flow capital during the quarter, suggesting the market remains open and accessible. This contradicts concerns about private credit market stress posing existential risk to BNPL business models. The firm characterises the funding backdrop as constructive, with spreads moving in a favourable direction for quality operators like Affirm.

Market data shows US consumer lending ABS issuance reaching post-crisis highs according to Reuters, with strong investor appetite supporting the constructive funding environment Morgan Stanley referenced in its analysis.

The next major ASX story will hit our subscribers first

May investor forum could be the next catalyst

Morgan Stanley identifies Affirm’s May 2026 Investor Forum as the near-term catalyst that could validate the bullish thesis and trigger broader estimate revisions across Wall Street. The event is expected to provide critical updates on growth outlook, margin targets, and long-term profitability goals.

Expected topics at the forum include:

- GMV growth scenarios potentially ranging from below 20% to above 30%, with management likely confirming the higher end of the range

- Updated adjusted operating income (AOI) margin guidance, reflecting operational leverage and efficiency gains

- Raised retained loan and transaction margin targets to the 3.5%-4.0% range

- Potential introduction of fiscal 2028 GAAP EPS targets, possibly in the $2.50-$3.00 range or higher

Positive disclosures at the May forum could trigger broader analyst community upgrades and estimate revisions, amplifying the stock’s upward momentum. Morgan Stanley views the event as a key inflection point where management can demonstrate the sustainability of Affirm’s growth trajectory and profitability improvements.

What investors should watch

Morgan Stanley’s Affirm stock upgrade reflects confidence in the company’s execution and improving market conditions for BNPL operators. The May 2026 Investor Forum stands out as the key near-term date for investors to monitor, as management disclosures could confirm the bullish thesis and drive further upside.

Key factors for investors to track include:

The regulatory framework for buy-now-pay-later providers has evolved significantly, with the CFPB’s interpretive rule establishing BNPL lender compliance requirements under the Truth in Lending Act similar to traditional credit card issuers.

- ABS funding spreads for signs of stress or continued tightening, indicating favourable capital market conditions

- GMV growth sustainability above 30%, demonstrating resilient consumer demand and merchant adoption

- Margin expansion progress, particularly in retained loan and transaction margins moving towards the 3.5%-4.0% range

- Competitive dynamics in the BNPL space, including funding access and market share trends among peers

- Broader private credit market conditions, which could impact funding availability and cost

As competitive dynamics in the BNPL space evolve, emerging players are combining traditional instalment lending with DeFi yields and AI-driven financial guidance, potentially reshaping the competitive landscape Affirm operates within.

The upgrade positions Affirm as Morgan Stanley’s highest conviction idea in fintech, with the $76 price target representing 27% upside potential. Investors should assess whether they agree with the funding environment thesis and growth sustainability assumptions underpinning the bullish call.

> Disclaimer

> This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What does Morgan Stanley's Top Pick rating mean for Affirm stock?

Top Pick is Morgan Stanley's highest conviction designation within a sector, ranking above a standard Overweight rating and signalling the analyst believes Affirm offers the best risk-reward profile among fintech coverage.

What is the price target Morgan Stanley set for Affirm (AFRM)?

Morgan Stanley analyst James Faucette set a $76 price target for Affirm, implying approximately 27% upside from recent trading levels and a valuation of roughly 24 times fiscal 2028 GAAP earnings per share.

Why did Morgan Stanley upgrade Affirm to Top Pick in April 2026?

Morgan Stanley upgraded Affirm because it believes private credit concerns weighing on BNPL stocks are overdone, funding conditions are improving with tightening ABS spreads, and the company is on track to sustain over 30% GMV growth while expanding profitability margins.

What should investors watch ahead of Affirm's May 2026 Investor Forum?

Investors should monitor management guidance on GMV growth scenarios, updated adjusted operating income margin targets, raised retained loan and transaction margin guidance toward the 3.5%-4.0% range, and any introduction of fiscal 2028 GAAP EPS targets in the $2.50-$3.00 range or higher.

How do ABS funding conditions affect Affirm's profitability?

Affirm relies on asset-backed security markets to finance its loan portfolios, so tighter ABS spreads translate directly into lower funding costs and better margins; Morgan Stanley currently characterises the funding backdrop as constructive, with two-year spreads at 80 basis points and three-year spreads tightening to 95 basis points.