Record Highs Are Not the Risk Most Investors Think They Are

7 hrs ago

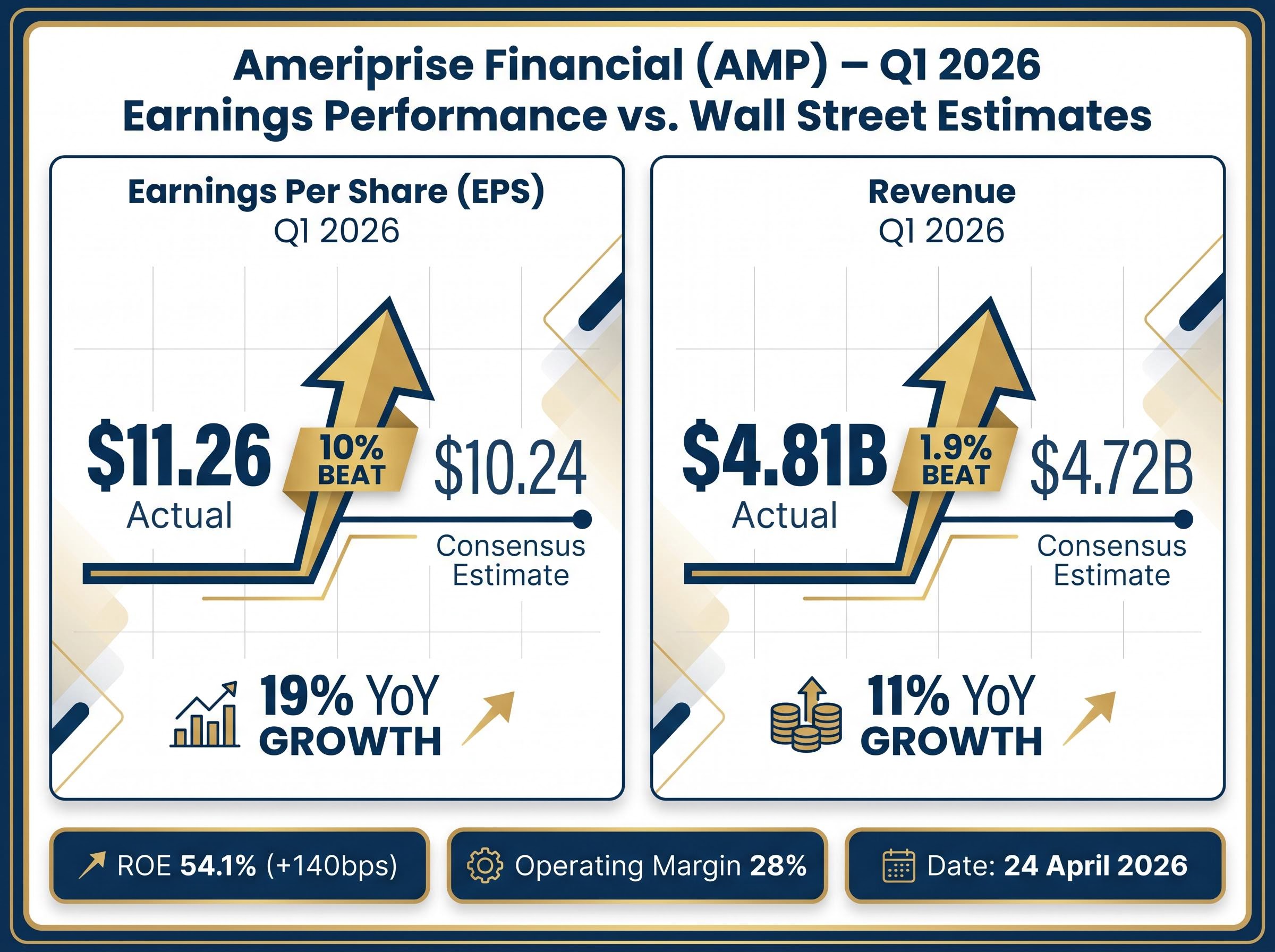

Ameriprise Financial delivered record adjusted operating earnings per share of $11.26 in Q1 2026, beating Wall Street estimates by roughly 10% and marking a 19% year-over-year surge. The diversified financial services firm’s results arrived amid volatile markets and an intensely competitive advisor recruiting environment, yet demonstrated the resilience of its wealth management-led model. This article breaks down the key drivers behind the earnings beat, the strategic implications of a major banking partnership shift, and what forward guidance signals for investors tracking the stock.

The headline numbers established the scope of the beat on 24 April 2026. Adjusted operating EPS of $11.26 came in 10% above the consensus estimate of $10.24, whilst revenue reached $4.81 billion against expectations of $4.72 billion, a 1.9% beat. Year-over-year revenue climbed 11% to $4.8 billion.

The performance was structural rather than event-driven. Return on equity expanded 140 basis points to 54.1%, and the operating margin held at 28%. Management attributed the quarter’s strength to operational discipline across the diversified business model, with wealth management leading but supported by asset management and retirement segments.

Record Performance Adjusted operating EPS of $11.26 represents a company record, up 19% year-over-year, signalling strengthening earnings quality alongside growth.

The magnitude of the EPS beat and the ROE expansion signal that Ameriprise’s earnings quality is strengthening, not just growing. For investors assessing valuation multiples, the combination of record profitability and margin stability matters as much as the top-line revenue figure.

Ameriprise’s 19% EPS growth and 11% revenue expansion demonstrate the kind of operational leverage that KPI-based earnings analysis identifies before consensus reprices the stock, with record advisor productivity and segment margin expansion revealing performance quality beyond headline EPS.

Wealth management was the primary engine of the earnings beat. Segment adjusted operating net revenues climbed 14% to $3.2 billion, whilst pre-tax adjusted operating earnings grew 20% to $951 million. The segment margin improved to 30% from 28% a year earlier.

Advisor productivity reached an all-time high of $1.2 million per advisor, up 10% year-over-year. Fee-based and transaction revenues rose 17%, supported by transactional activity growth of 10%. Total client assets expanded 12% to $1.1 trillion, with wrap assets growing 16% to $664 billion.

| Metric | Q1 2026 Figure | Year-over-Year Change |

|---|---|---|

| Segment Revenue | $3.2 billion | +14% |

| Pre-Tax Operating Earnings | $951 million | +20% |

| Segment Margin | 30% | +2 percentage points |

| Advisor Productivity | $1.2 million | +10% |

| Total Client Assets | $1.1 trillion | +12% |

| Wrap Assets | $664 billion | +16% |

Record advisor productivity and margin expansion suggest the firm is extracting more value from its existing advisor base, a critical metric as industry-wide recruiting costs escalate. The 20% earnings growth against 14% revenue growth indicates operating leverage is working in Ameriprise’s favour, positioning the division as the most profitable segment within the broader business mix.

The wealth management segment’s 20% earnings growth against 14% revenue growth creates operating leverage comparable to what custody banking earnings models demonstrate when asset-servicing firms extract incremental profitability from existing client relationships without proportional cost increases.

Ameriprise executed a strategic pivot in its banking partnership portfolio during the quarter. Comerica Bank terminated its advisory services agreement early, triggering a $25 million one-time make-whole payment booked in Q1 results. Approximately $18 billion of Comerica assets are expected to flow out by the end of Q3 2026.

The replacement arrived ahead of the exit. Huntington Bank signed a 10-year partnership agreement bringing roughly 260 advisors and $28 billion in client assets to Ameriprise. Most Huntington onboarding is targeted for Q4 2026, with growth potential built into the contract structure.

The Huntington Bank agreement’s 10-year contractual structure and $28 billion asset contribution exemplify capital-light wealth partnership models that generate immediate recurring revenue without acquisition premiums, a structure that diversified financial firms increasingly prefer over outright purchases when expanding their advisory footprints.

Partnership Transition The Huntington Bank agreement brings $28 billion in client assets and 260 advisors under a 10-year contract, exceeding the $18 billion in Comerica outflows expected by Q3 2026.

The net positioning favours Ameriprise rather than disrupts it. Replacing $18 billion in outflows with $28 billion in inflows, alongside a decade-long contractual commitment, suggests the partnership shift is accretive to the wealth management segment’s asset base. The timeline concentrates the Comerica outflows in Q2 and Q3 whilst deferring most Huntington onboarding to Q4, creating a temporary asset compression before the replacement arrives.

Return on equity measures how efficiently a financial firm generates profit from shareholder equity. Calculated as net income divided by shareholder equity, ROE tells investors how much profit the company produces per dollar of capital deployed. For financial services firms, elevated ROE signals effective capital allocation and operational efficiency.

The CFA Institute financial analysis techniques covering return on equity calculation establish ROE as net income divided by shareholder equity, the standard methodology that financial analysts use to assess capital efficiency across diversified financial services firms.

Ameriprise’s 54.1% ROE, up 140 basis points year-over-year, sits well above the industry median. The firm returned $936 million to shareholders in Q1, representing 88% of operating earnings. Share repurchases covered 1.6 million shares, whilst the quarterly dividend rose 6%. Excess capital stood at $2.3 billion, with $3.6 billion returned to shareholders over the trailing twelve months.

Understanding ROE helps investors assess whether a financial firm is efficiently deploying capital. Ameriprise’s elevated ROE combined with aggressive buybacks signals management confidence in the stock’s valuation. The capital return policy, targeting 85-90% of operating earnings with a stated bias toward the higher end, positions the stock as an income and capital return play rather than a growth reinvestment story.

Ameriprise’s $936 million capital return in Q1, representing 88% of operating earnings with 1.6 million shares repurchased, positions the stock within a cohort of aggressive share buyback programmes where management signals conviction that current valuations materially understate intrinsic value, a thesis that can produce significant stock price reactions when market perception eventually converges with management’s view.

Asset management contributed meaningful earnings growth outside the wealth management division. Operating earnings rose 13% to $273 million, whilst the segment margin reached 44%, above the targeted 35-39% range. Total assets under management and advisement reached $706 billion, up 8% year-over-year.

Net outflows improved significantly to $5.9 billion, a material deceleration from worse prior-year figures. Investment performance remained strong, with over 70% of funds performing above peer median across 1, 3, and 5-year periods. The improved flow trends and sustained investment performance suggest the worst of the industry-wide outflow cycle may be passing for Ameriprise’s asset management business.

The retirement and protection segment generated pre-tax adjusted operating earnings of $190 million in Q1. Management expects annual earnings to remain near $800 million over time, providing stable contribution to the diversified earnings mix. Annuity and variable universal life sales showed strength during the quarter, supporting the segment’s outlook.

Diversified earnings streams provide stability if any single segment faces headwinds. Asset management’s improving flows and margin strength, combined with the retirement segment’s steady contribution, reduce reliance on wealth management alone to drive consolidated performance.

Management provided forward earnings guidance alongside the Q1 beat. Projected EPS for Q2 2026 stands at $10.87, with full-year 2027 EPS forecast at $44.91. The guidance implies sustained profitability and continued operating leverage across the business.

Shares fell 1.9% in after-hours trading to $467.92 despite the earnings beat and forward guidance. The stock’s 52-week trading range spans from $422.37 to $550.18, placing the after-hours price near the midpoint of the annual range.

Forward Guidance Management projects Q2 2026 EPS of $10.87 and full-year 2027 EPS of $44.91, sustaining the profitability momentum demonstrated in Q1 results.

The divergence between strong guidance and a negative stock reaction suggests the market may be pricing in broader macro concerns rather than company-specific weakness. Key risks include market volatility affecting client asset values and the competitive recruiting environment pressuring advisor retention costs. For investors focused on fundamentals, the gap between earnings performance and stock response creates a potential opportunity if the macro headwinds prove temporary.

Ameriprise’s Q1 2026 results demonstrate the strength of its wealth management-led model, with record EPS, expanding margins, and a strategically favourable partnership transition offsetting near-term flow headwinds. The Huntington onboarding in Q4 and continued capital returns should provide catalysts for investors tracking the stock through year-end. Watch for Q2 results and Huntington integration updates to gauge whether the earnings momentum sustains.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Ameriprise reported record adjusted operating EPS of $11.26 in Q1 2026, beating the consensus estimate of $10.24 by approximately 10% and rising 19% year-over-year, with total revenue reaching $4.81 billion against expectations of $4.72 billion.

Despite the earnings beat and positive forward guidance, Ameriprise shares fell 1.9% in after-hours trading to $467.92, a move analysts attribute to broader macro concerns rather than any company-specific weakness in the results.

Huntington Bank signed a 10-year partnership agreement with Ameriprise bringing approximately 260 advisors and $28 billion in client assets, more than replacing the $18 billion in outflows expected from the early termination of the Comerica Bank agreement by Q3 2026.

Ameriprise returned $936 million to shareholders in Q1 2026, representing 88% of operating earnings, including repurchases of 1.6 million shares and a 6% increase in the quarterly dividend, with excess capital standing at $2.3 billion.

Management projected Q2 2026 EPS of $10.87 and full-year 2027 EPS of $44.91, signalling continued profitability momentum and sustained operating leverage across the diversified business.