Charter Hall Long WALE REIT has completed a comprehensive $2.0 billion secured debt refinance, fully replacing all existing balance sheet debt including Medium-Term Notes previously issued in the Australian corporate bond market. The new platform diversifies debt across ten lending counterparties and marks a structural shift from unsecured to secured debt, delivering improved terms and enhanced financial flexibility for unitholders.

Charter Hall Long WALE REIT completes $2.0 billion secured debt platform

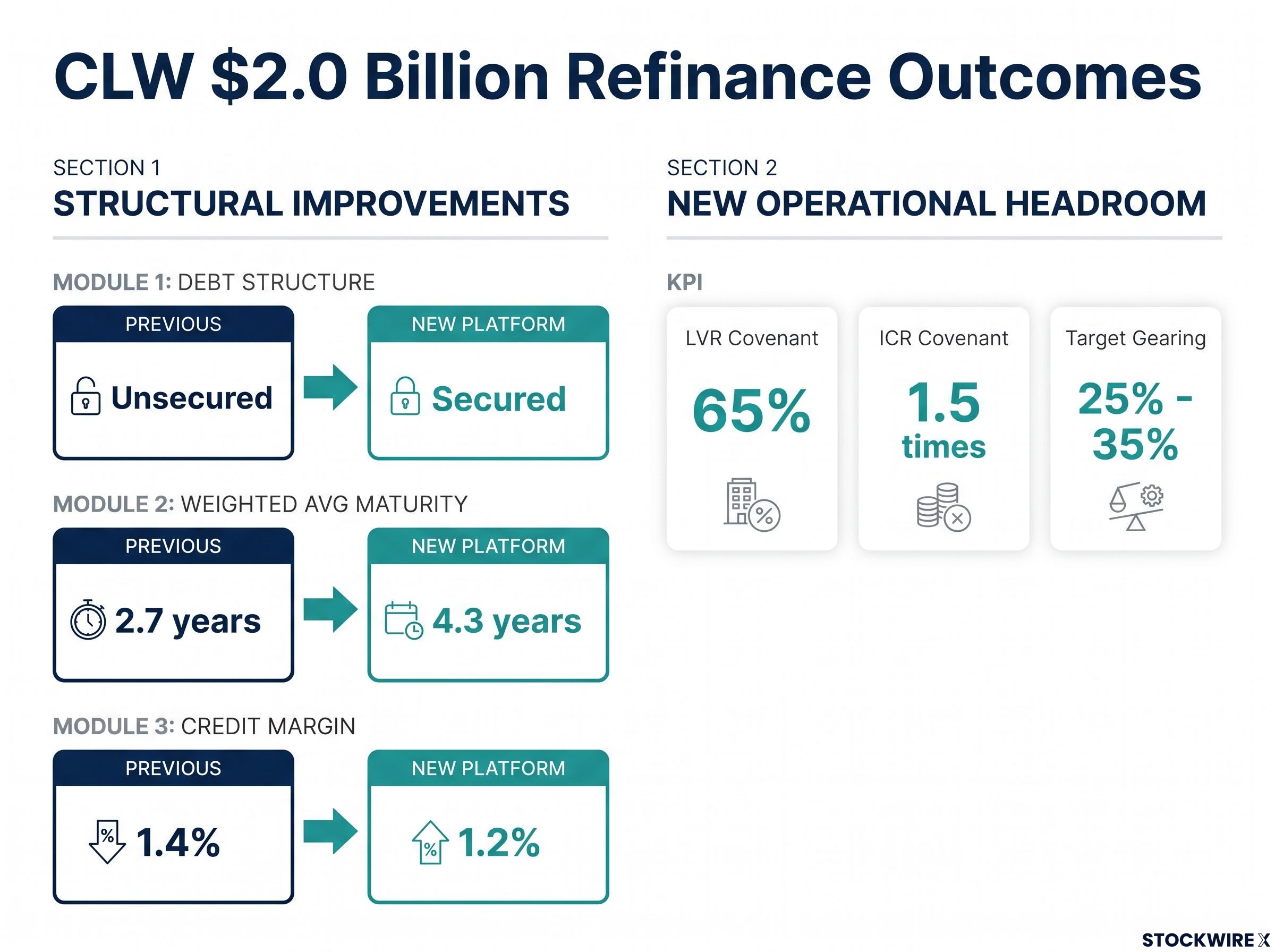

CLW announced the establishment of a new $2.0 billion secured debt platform, diversified across ten lending counterparties. This comprehensive refinance fully replaces all existing balance sheet debt, including the repayment of Medium-Term Notes previously issued in the Australian corporate bond market. The transaction represents a structural shift from unsecured to secured debt, positioning the REIT to access improved borrowing terms.

A diversified lender base reduces refinancing concentration risk while the shift to secured debt unlocks improved terms for unitholders. The platform provides CLW with greater financial flexibility across its balance sheet owned assets.

When big ASX news breaks, our subscribers know first

Debt maturity extended by 1.6 years with staggered repayment profile

The refinance extends CLW’s weighted average debt maturity from 2.7 years to 4.3 years, representing a 1.6-year extension. Maturities are staggered from FY29 through to FY32, reducing near-term refinancing pressure and providing management with greater optionality when approaching debt markets.

Staggered maturities across four financial years provide CLW with flexibility to refinance in favourable market conditions rather than facing a concentrated debt wall. This maturity profile reduces rollover risk and supports distribution sustainability over the medium term.

What is debt refinancing and why does it matter for REITs?

Debt refinancing involves replacing existing loans with new facilities, typically to secure better terms, extend maturities, or adjust debt structure. For property trusts, secured debt is backed by specific assets as collateral, while unsecured debt relies on the borrower’s general creditworthiness.

Weighted average debt maturity measures how far into the future a REIT’s debt obligations fall due. For REITs specifically, longer maturity profiles reduce rollover risk — the risk that debt cannot be refinanced at acceptable terms when it matures — and provide greater earnings visibility by locking in funding costs for extended periods.

For income-focused investors, understanding a REIT’s debt structure is critical because interest costs directly impact distributable earnings. A well-structured debt platform supports distribution sustainability and provides management with financial flexibility to pursue value-accretive opportunities.

Credit margin reduced by 20 basis points with enhanced covenant flexibility

The refinance delivers immediate financial benefits through a weighted average credit margin reduction of approximately 20 basis points, from 1.4% to 1.2%. The new covenant structure provides enhanced operational headroom with a balance sheet LVR covenant set at 65% and an ICR covenant at 1.5 times. CLW continues to target a balance sheet gearing range of 25% to 35%.

Lower credit margins flow directly to the bottom line, while increased covenant headroom provides a buffer during market volatility.

| Metric | Previous | New Platform |

|---|---|---|

| Debt Structure | Unsecured | Secured |

| Weighted Avg Maturity | 2.7 years | 4.3 years |

| Credit Margin | 1.4% | 1.2% |

| LVR Covenant | Not stated | 65% |

| ICR Covenant | Not stated | 1.5 times |

The new platform delivers:

- Credit margin reduction: ~20 basis points (1.4% → 1.2%)

- LVR covenant: 65%

- ICR covenant: 1.5 times

- Target gearing range: 25% to 35%

Management highlights CLW’s value proposition

Avi Anger, CLW’s Fund Manager and Charter Hall Diversified CEO, commented on the refinance: “The refinance of CLW’s existing debt arrangements maximises financial flexibility, significantly enhances covenant headroom, extends our debt maturity profile and concurrently reduces our credit margins.”

Anger also highlighted CLW’s current market positioning and portfolio quality characteristics:

CLW Market Positioning

“CLW is trading at a material discount to its last reported NTA per security and, as a result, offers investors an attractive 7.3% distribution yield. CLW is undervalued by the market particularly given the quality of its portfolio, long WALE with leases to blue chip tenants and strong annual rental growth, with over 52% of rent reviews linked to CPI.”

The REIT currently offers a 7.3% distribution yield based on FY26 DPS guidance of 25.5 cents per security and a security price of $3.48 as at 9 June 2026. Over 52% of rent reviews are linked to CPI, providing inflation protection for distributions.

FY26 earnings guidance reiterated at 25.5 cents per security

CLW reiterates FY26 EPS and DPS guidance of 25.5 cents per security, representing 2.0% growth on FY25. The REIT will report its full year financial results on 13 August 2026.

Reaffirming guidance alongside the refinance signals management confidence that the new debt platform supports distribution sustainability. The combination of reduced credit margins, extended maturities, and enhanced covenant flexibility positions CLW to maintain distributions while managing near-term market volatility.

Key takeaways for CLW investors

- $2.0 billion secured platform replaces all existing balance sheet debt

- Debt maturity extended by 1.6 years to 4.3 years weighted average

- Credit margin reduced by ~20 basis points

- Enhanced covenant headroom with 65% LVR and 1.5x ICR covenants

- FY26 distribution guidance of 25.5 cents per security maintained

- Over 52% of rent reviews linked to CPI providing inflation protection

- 7.3% distribution yield based on current security price and FY26 guidance

Want the Next REIT Move in Your Inbox?

Join 20,000+ investors getting FREE breaking ASX news delivered within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to start receiving real estate and REIT alerts the moment market-moving announcements break.