Kelly Partners Walks Away From Eurofast Deal After Vendor Demands More Cash

Kelly Partners walks away from Eurofast partnership over pricing demands

Kelly Partners Group has elected not to proceed with its proposed partnership with Eurofast International Ltd, despite having a legally binding term sheet in place. The accounting network operator elected not to proceed with the transaction after the vendor requested a materially large additional upfront payment that did not meet KPG’s acquisition criteria.

The decision demonstrates rigorous acquisition discipline. Management noted that successful partnerships require cooperation and aligned views, stating that without these elements, execution becomes difficult. This marks a significant reversal given shareholder approval for financial assistance was already secured at the 8 May 2026 EGM.

Eurofast is a professional services firm headquartered in Nicosia, Cyprus, with operations and 6 major offices across 18 countries. The business had average annual revenue of approximately €10.2 million (net of client disbursements) and average EBITDA of approximately €3.7 million over the three financial years to 2025, representing an EBITDA margin of approximately 36.7%. These figures had not been audited.

When big ASX news breaks, our subscribers know first

What is acquisition discipline and why does it matter?

Acquisition discipline refers to the practice of maintaining strict deal criteria and walking away when terms shift unfavourably, even after significant time and resources have been invested. Companies that chase transactions at any cost risk destroying shareholder value through overpayment. Disciplined acquirers prioritise capital preservation over deal completion.

KPG’s decision illustrates this principle in action. Despite securing shareholder approval for financial assistance under Corporations Act sections 260A and 260B(2), management walked away when the vendor’s pricing demands breached internal investment thresholds. This suggests a focus on value preservation rather than empire-building.

Transaction timeline and what happened

The sequence of events highlights the complexity and resources invested before termination:

- 7 April 2026: KPG announced legally binding term sheet for potential Eurofast partnership

- 8 May 2026: Shareholder resolution passed at EGM approving financial assistance under Corporations Act sections 260A and 260B(2)

- 17 June 2026: KPG announces it will not proceed due to vendor requesting materially large additional upfront payment

Completion had been delayed due to the size and complexity of ongoing due diligence, including the need for a financial audit. The timeline demonstrates KPG invested considerable corporate resources before walking away, reinforcing the materiality of the pricing issue.

KPG’s growth track record continues

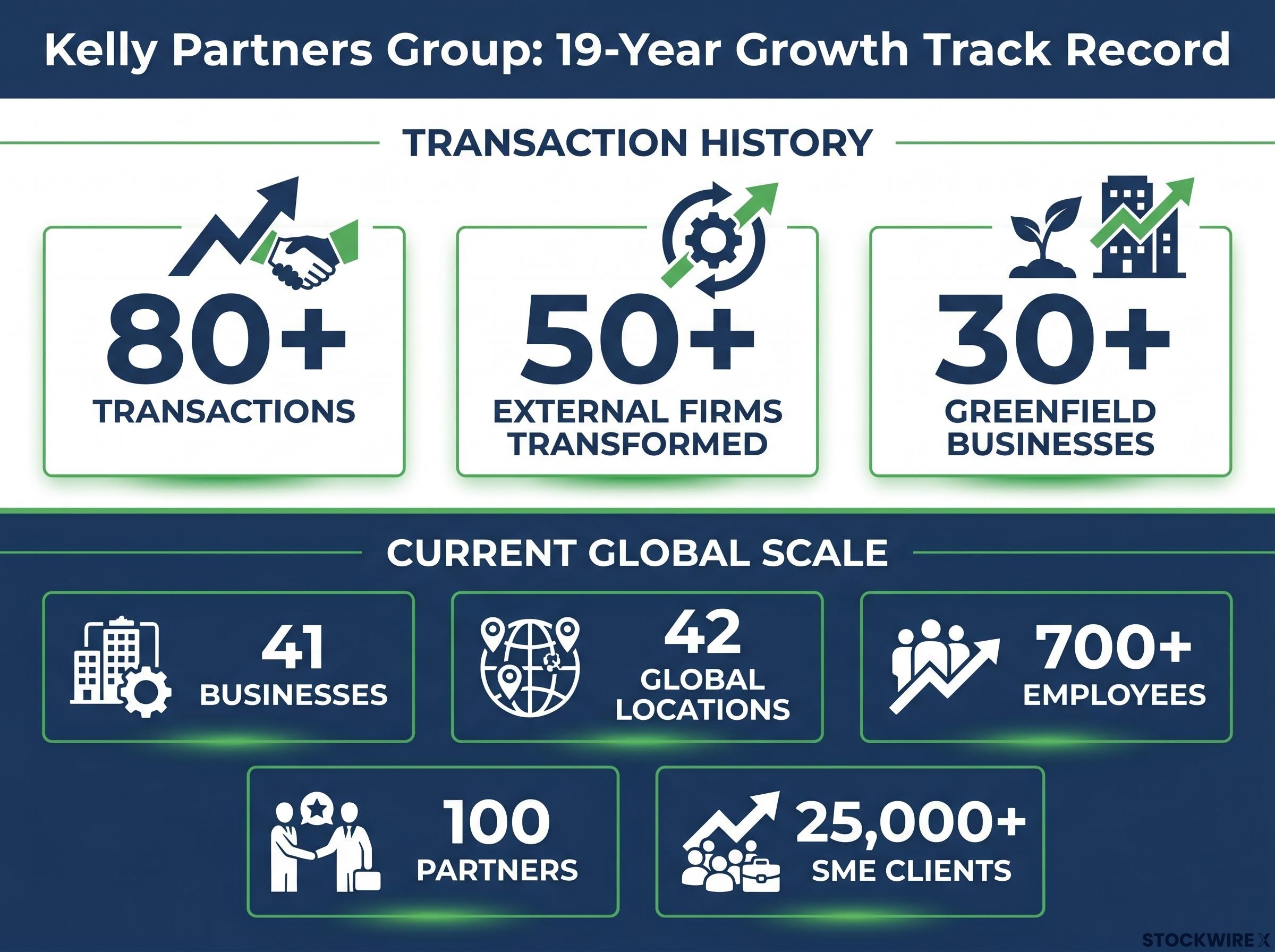

One abandoned transaction does not materially alter KPG’s established expansion strategy. The accounting network has completed 80+ individual transactions over 19 years to build its current platform, including the transformation of 50+ external firms and the launch of 30+ greenfield businesses.

The group now operates 41 businesses across 42 locations globally, employing more than 700 people including 100 partners who service over 25,000 SME clients. This scale demonstrates repeated ability to source and execute partnerships that meet investment criteria.

The Partner-Owner-Driver model and Hold Co structure that underpin this expansion remain unchanged. KPG’s FY26 run rate revenue trajectory, as shown in company materials, continues to track the long-term growth pattern established since 2006.

The Partner-Owner-Driver model has also been applied beyond traditional accounting practices, with the Kelly Partners Hello AI Partnership representing the first time the structure has been used to acquire a capability vertical rather than a conventional firm.

The next major ASX story will hit our subscribers first

What comes next for Kelly Partners

KPG’s core Australian operations and existing international platform remain intact. The company has elected not to proceed with the Eurofast transaction.

The Partner-Owner-Driver model and Hold Co ownership structure continue unchanged. No forward guidance was provided in the announcement regarding alternative EMEA opportunities or near-term acquisition targets.

Want the Next Accounting Sector Deal in Your Inbox?

Join 20,000+ investors getting FREE breaking ASX news delivered within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to receive market-moving announcements the moment they hit the ASX, with expert coverage already done for you.