Infratil Ltd CDC Stake Rises A$1.76B as Contracted Capacity Tops 1GW

CDC valuation jumps 23.6% to A$18.5 billion on data centre demand surge

Infratil Limited has disclosed the independent valuation of CDC as at 30 June 2026, revealing a 23.6% increase during the quarter to a mid-point of A$18.5 billion. The uplift represents a A$3.5 billion rise from the prior 31 March 2026 valuation.

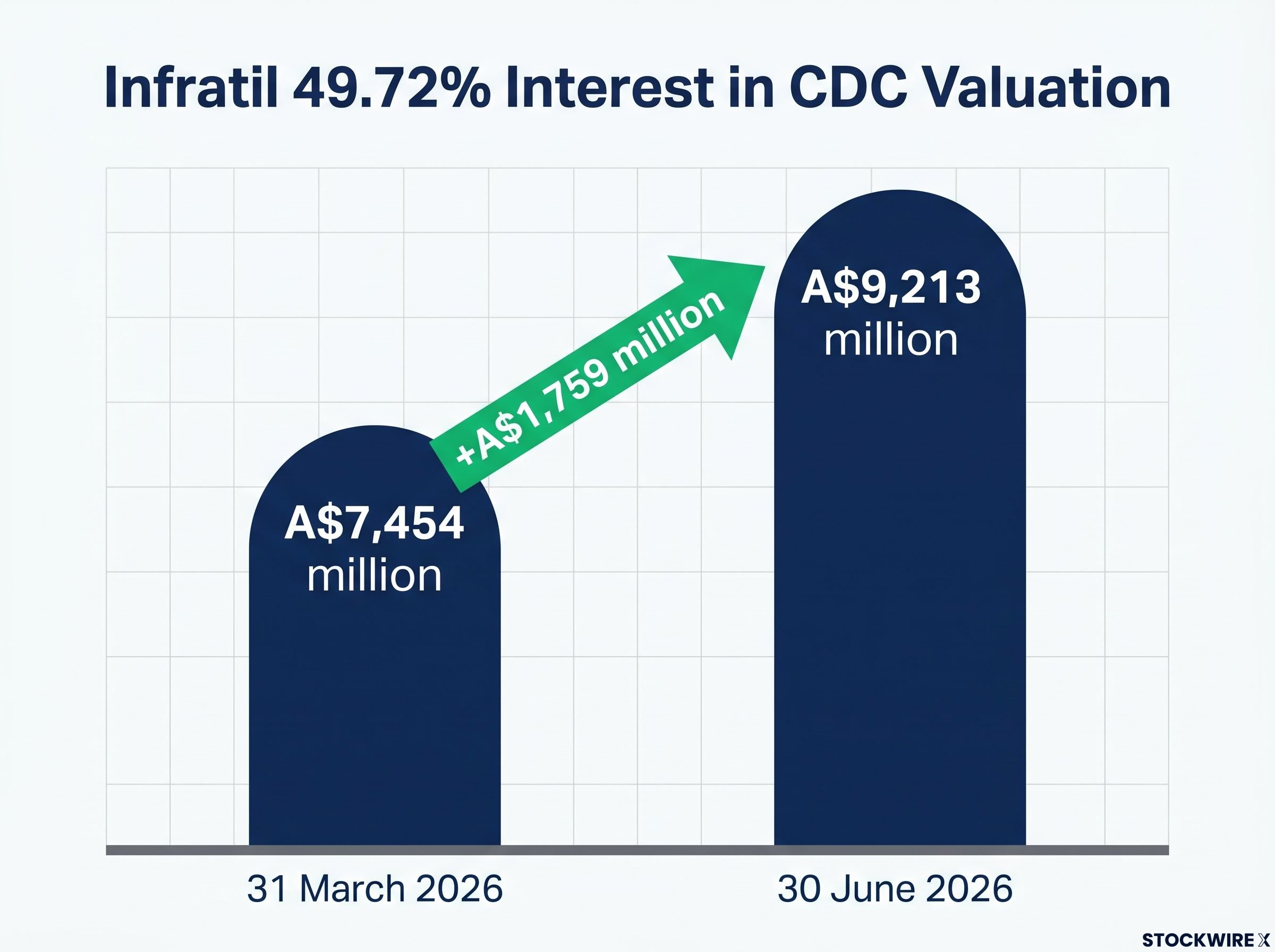

On this basis, Infratil’s 49.72% interest in CDC is now valued at A$9,213 million, up A$1,759 million from A$7,454 million at 31 March 2026.

The update attributed the movement to three primary drivers: contracted capacity growing to more than 1GW, an accelerated build programme, and expansion of CDC’s total pipeline to 3.9GW of leasable capacity. These signals point to demand from data centre customers rather than a purely financial re-rating.

When big ASX news breaks, our subscribers know first

What drove the A$3.5 billion valuation increase

The independent valuation was assessed within a range of A$17.5 billion to A$19.7 billion, with the mid-point of A$18.5 billion underpinning the reported figures. The quarter’s key positive value movements were driven by capacity and pipeline growth across CDC’s Australian and New Zealand operations.

- Contracted capacity increased to more than 1GW, including the 555MW contract announced in May plus a further 14MW of contracted capacity in New Zealand.

The 555MW contract announced in May was signed with a US investment-grade customer on a 30-year term, representing the largest single data centre deal in Australian history and the primary catalyst that pushed CDC’s total contracted capacity above 1GW.

-

Leasable operating capacity rose 90MW to 550MW.

-

Leasable capacity under construction doubled to 810MW.

-

Total reported pipeline increased 1.9GW to 3.9GW of leasable capacity.

These positive cash flow movements were partly offset by the valuation’s assessment of a 25 basis point increase in the long-term risk-free rate. This lifted the long-term forward yield curve, raised assumed interest costs, and increased the cost of equity.

Valuation assumptions at a glance

The independent valuation retained its established methodology, allowing a direct comparison of the key metrics between the two reporting dates.

| Metric | 30 June 2026 | 31 March 2026 |

|---|---|---|

| Enterprise value | A$24,504m | A$20,019m |

| Equity value | A$18,528m | A$14,991m |

| Equity value (Infratil 49.72%) | A$9,213m | A$7,454m |

| Net debt | A$5,976m | A$5,028m |

| Risk-free rate | 4.25% (+0.25%) | 4.00% |

| Cost of equity (blended) | 12.45% (+0.61%) | 11.84% |

| Long-term EBITDA margin | 83% (2055) | 83% (2055) |

The methodology remained unchanged. The valuation applied a discounted cash flow (DCF) approach using free cash flow to equity (FCFE), a terminal year of 2055, and an asset beta held steady at 0.575.

The rise in the blended cost of equity from 11.84% to 12.45% reflected the 25bps increase in the risk-free rate, alongside a higher forecast gearing ratio from CDC’s debt-funded construction activity. The asset-specific risk premium remained largely unchanged, with de-risking from increased contracted capacity offset by the addition of future build capacity.

Understanding data centre valuations: why capacity and contracts matter

A data centre “pipeline” refers to the total capacity a developer expects to build and bring online over a defined period. That capacity typically falls into three categories: operating (live and generating revenue), under construction (development commenced but not yet in service), and future build (planned developments expected to be delivered later).

CDC defines leasable capacity as “primary ICT capacity that is contractable or revenue generating.” This measure focuses on the portion of a facility that can actually be sold to customers, rather than total infrastructure capacity.

Why does contracted capacity matter to a valuation? Signed contracts convert future potential into revenue certainty. When a large portion of operating and under-construction capacity is already contracted, the cash flows underpinning the valuation carry less risk.

A disclosure change accompanied this update. Pipeline and capacity metrics are now reported on a leasable capacity basis, whereas previous disclosures used a built capacity basis. The disclosure horizon was also extended from FY34 to FY40. Importantly, this is a disclosure change and not a change in the valuation approach, so the reclassification alone does not imply underlying growth.

Strong customer signals for additional large scale data centre demand continue to underpin the capacity metrics assessed in the valuation.

The development pipeline: 3.9GW to FY40

CDC’s pipeline growth during the quarter reflected both new development activity and the recognition of additional future capacity.

-

Operating capacity increased 90MW as data centres became operational at the Eastern Creek (NSW) and Hume (ACT) campuses.

-

Under construction capacity doubled to 810MW as development commenced at the Marsden Park (NSW) and Laverton (VIC) campuses.

-

Future build capacity increased from 1.7GW to 2.6GW, including 1.3GW of additional future build capacity recognised to meet strong customer demand.

The 1.9GW total pipeline increase comprised 550MW previously assumed for FY34 to FY40 development, plus 1.3GW of newly recognised capacity planned across key Australian markets. The following table sets out operating leasable capacity by region.

| Region | Operating capacity (June 2026) | Operating capacity (March 2026) |

|---|---|---|

| ACT | 120MW | 100MW |

| NSW | 220MW | 150MW |

| VIC | 130MW | 130MW |

| NZ | 80MW | 80MW |

| Total | 550MW | 460MW |

Funding the build programme

Net debt increased over the period, primarily reflecting the acceleration of CDC’s debt-funded build programme across key sites to support contracted capacity growth and future contracting discussions.

Following the assignment of its public Moody’s Baa2 (Stable) credit rating, CDC continued to diversify its funding sources. This included the issuance of a A$1 billion hybrid capital bond across floating and fixed-rate tranches at a blended margin of 250bps.

The Moody’s Baa2 (Stable) credit rating, assigned in April 2026, was underpinned by CDC’s weighted average lease expiry of 28.4 years and a customer base where more than 90% of revenue comes from investment-grade counterparties, giving institutional debt markets the confidence to participate in CDC’s funding programme.

The next major ASX story will hit our subscribers first

What it means for Infratil investors

The uplift is material for Infratil shareholders. The value of the CDC stake gained A$1,759 million in a single quarter, driven by real demand signals such as contracted capacity growth and pipeline expansion, rather than financial re-rating alone.

Contracted capacity now accounts for a significant portion of CDC’s operating and under-construction capacity, with the pipeline runway extended to FY40 to capture ongoing customer demand. CDC’s build programme is targeting delivery of the contracted capacity by the end of FY29.

The increase was driven by strong growth in CDC’s contracted capacity to more than 1GW, the acceleration of CDC’s build programme to support this demand, and the expansion of CDC’s total pipeline to FY40 from 2.6GW to 3.9GW of leasable capacity to support future growth.

The valuation update was authorised for release by Matthew Ross, Infratil Chief Financial Officer. The announcement did not contain forward projections beyond the disclosed capacity, contracting, and funding milestones, with delivery of the accelerated build programme dependent on execution against the stated FY29 and FY40 timeframes.

Don’t Miss the Next ASX Tech and Infrastructure Breakout

Big News Blast delivers FREE breaking ASX news straight to your inbox within minutes of release, complete with in-depth analysis already done for you. Join 20,000+ investors who stay ahead of the market on tech, infrastructure, and beyond. Click the “Free Alerts” button at StockWire X to start receiving alerts the moment news breaks.