NobleOak Reports 9% Embedded Value Growth to $2.34 Per Share

NobleOak reports 9% embedded value growth to $2.34 per share

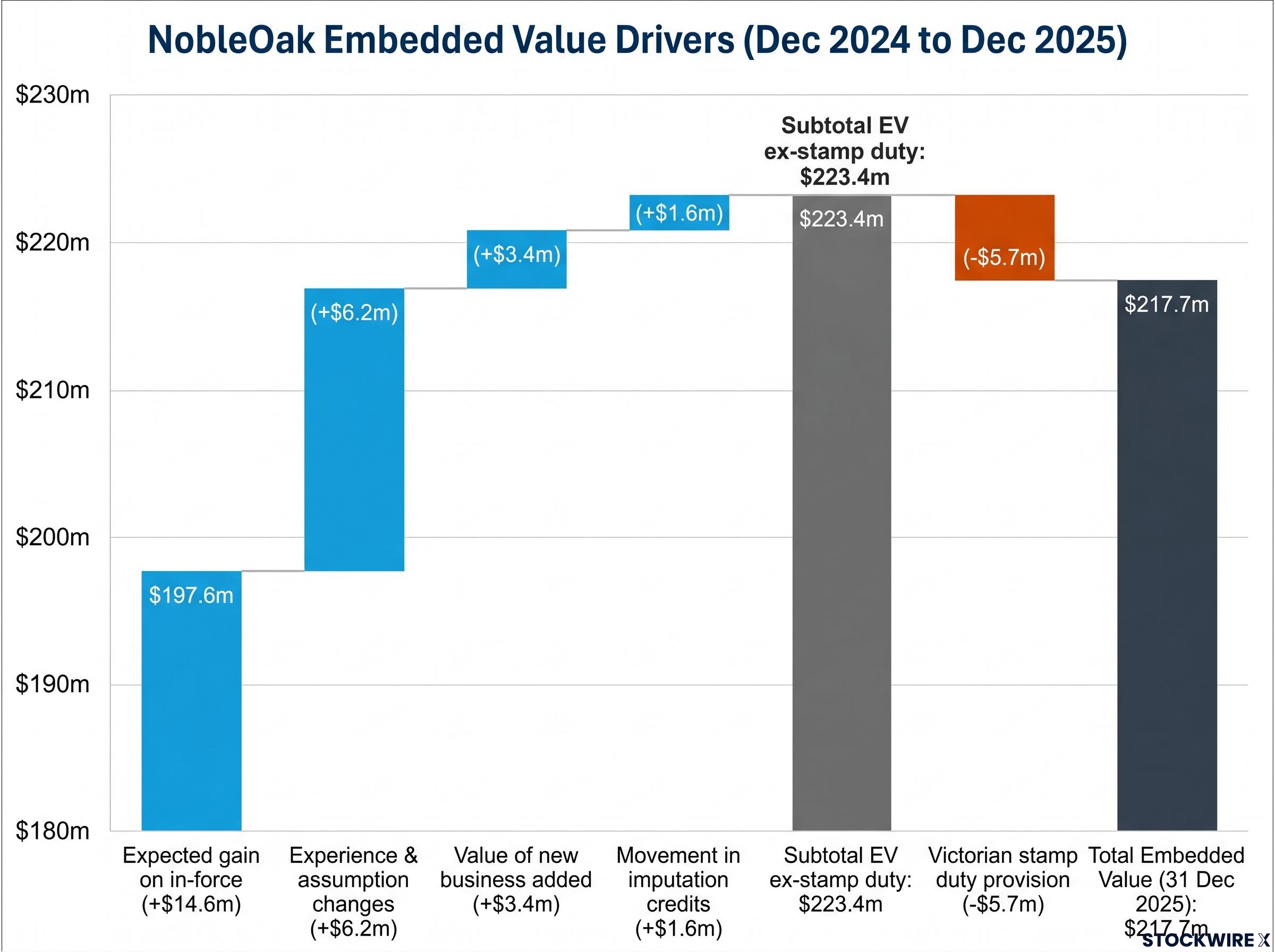

NobleOak Life has released its updated Embedded Value as at 31 December 2025, reporting 9% year-on-year growth to $2.34 per share, or $217.7 million in total. The valuation was calculated using an 8.5% discount rate and reflects continued market share gains and strong financial discipline.

Excluding the impact of the previously disclosed one-off Victorian stamp duty provision, Embedded Value growth would have been approximately 13% year-on-year.

Anthony Brown, Chief Executive Officer

“We are pleased to continue our strong and profitable growth trajectory, delivering 9% growth in Embedded Value over the last 12 months, and 16% in-force premium growth at 31 May 2026, achieving our FY26 in-force premium guidance. Our EV implies a significant premium to the Company’s current share price and reflects our continued market share gains and strong financial discipline supporting sustainable earnings growth.”

The Embedded Value metric estimates the present value of future profits distributable to shareholders from existing business. The valuation implies significant upside relative to NobleOak’s current trading price, particularly as it captures only the value of existing policies and does not account for future new business growth.

When big ASX news breaks, our subscribers know first

In-force premium growth hits 16%, achieving FY26 guidance

NobleOak’s in-force premiums reached $538 million as at 31 May 2026, representing 16% year-on-year growth. This result exceeds the company’s FY26 guidance target of greater than 15% in-force premium growth.

The company’s in-force market share reached 4.7% at December 2025, while new business market share stood at 14.1%. The gap between new business and in-force market share indicates the company is writing new policies at a rate significantly higher than its existing book, positioning it for continued expansion of its annuity-style recurring revenue base.

NobleOak crossed its $500 million in-force milestone in February 2026, with underlying NPAT climbing 11% and new business market share reaching 13.8%, already exceeding the company’s long-term target by 3.8 percentage points.

In-force premiums represent a predictable, annuity-style revenue stream for life insurers. As policyholders pay premiums over the life of their policies, this metric provides visibility into future revenue and cash flows.

| Period | In-force Premiums ($m) |

|---|---|

| FY21 | $182 |

| FY24 | $387 |

| FY25 | $464 |

| May-26 | $538 |

What is embedded value and why does it matter?

Embedded Value estimates the present value of future profits distributable to shareholders from existing business. It provides a framework for evaluating the long-term economic value of a life insurance company beyond statutory accounting metrics.

The Embedded Value calculation comprises three components: the Value of in-force business (VIF), Adjusted net worth, and the Value of imputation credits. The VIF component grew 11% to $191.2 million at the 8.5% discount rate, reflecting the expected profitability of NobleOak’s existing policy book.

Critically, Embedded Value captures only the value of business already written. It does not include any value from future new business growth. For a high-growth company like NobleOak, which is capturing market share at more than three times its in-force base, this implies significant upside beyond the current EV calculation.

The metric is sensitive to assumptions around claims experience, policy lapse rates, expense allocation, and the discount rate applied to future cash flows. Changes in these assumptions can materially affect the calculated value, which is why the company presents EV at multiple discount rates (ranging from 7.5% to 9.5%).

Key drivers behind the embedded value increase

The movement in Embedded Value from 31 December 2024 to 31 December 2025 can be broken down into several components:

-

Expected gain on in-force: +$14.6 million — This reflects the unwinding of the discount rate applied to the opening Embedded Value, representing the expected natural growth in value over the period.

-

Value of new business added: +$3.4 million — The positive value indicates that returns on new business written during the period exceeded the 8.5% discount rate. The company estimates the return on new business at approximately 10%.

-

Experience and assumption changes: +$6.2 million — Lower administration expense ratios drove +$4.1 million in value as the business benefited from economies of scale. This was partially offset by -$0.7 million from pricing updates and claims assumption adjustments.

-

Movement in imputation credits: +$1.6 million — This primarily reflects the overall movement in the Value of business in-force.

-

Victorian stamp duty provision: -$5.7 million — This one-off impact represents the estimated effect of the Victorian stamp duty provision recognised during the period.

The Victorian stamp duty provision arose after the State Revenue Office rejected NobleOak’s exemption claim under its Friendly Society structure, prompting the company to raise the provision to $6.5 million and implement pricing adjustments for Victorian policyholders to mitigate ongoing exposure.

Excluding the stamp duty provision, the subtotal Embedded Value reached $223.4 million, representing 13% growth from the prior year.

Strategic momentum and AI transformation

NobleOak’s business update presentation outlined several operational achievements underpinning the Embedded Value growth. The company has embedded its new Direct operating model, which is expected to drive profitable sales momentum in 2027, while strategic partner relationships with NEOS and PPS continue to deliver strong growth.

Early traction with the NEOS Futura product and nib partnership provides additional growth pathways. The company highlighted its AI strategy as moving from capability to competitive advantage, supporting scalable growth, margin expansion, and stronger Embedded Value through improvements in underwriting efficiency, client service, and actuarial modelling.

NobleOak has strengthened its senior leadership team with new hires, positioning the business to execute on its long-term target of $1 billion in in-force premiums. The company’s growth trajectory, combined with its focus on operational efficiency through technology, is designed to drive both top-line expansion and margin improvement.

Transition to Life Company structure

NobleOak is transitioning from a Friendly Society structure to a Life Company structure, involving the replacement of multiple benefit funds with a single statutory fund. The company expects a two-year implementation period with a total investment of $6 million and a payback period of 3-4 years.

Capital is likely to be retained and invested in the business during the transition period. Key benefits of the new structure include:

- Capital efficiency: More cost-effective capital structure to support growth

- Product flexibility: Greater speed to market with no APRA approval required for future product changes

- Industry alignment: Stronger alignment with industry practice, improving credibility with investors and stakeholders

- Enhanced governance: Improved governance and risk management under a single statutory framework

The transition positions NobleOak for more capital-efficient growth and greater flexibility to respond to market opportunities without regulatory approval delays for product modifications.

The next major ASX story will hit our subscribers first

What’s next for NobleOak investors

NobleOak will release its full year FY26 financial results on 28 August 2026, providing detailed profitability metrics and further insight into the company’s financial performance.

The investment case centres on the significant premium that the Embedded Value of $2.34 per share implies relative to the current share price. This valuation gap reflects the predictable cash flows from the existing in-force book, which provides an annuity-style revenue stream underpinning long-term earnings.

Continued market share gains, with new business share at 14.1% versus in-force share at 4.7%, position the company for sustained in-force premium growth. The AI and operating model investments are designed to drive margin expansion as the business scales, while the transition to Life Company structure will support capital-efficient growth towards the company’s $1 billion in-force premium target.

Don’t Miss the Next Financial Services Winner

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to start receiving alerts the moment market-moving announcements break across financials, healthcare, tech, and beyond.