Helloworld Travel Cuts FY26 Guidance as Middle East Conflict Slashes Flights

Helloworld Travel revises FY26 guidance as Middle East conflict disrupts flight routes

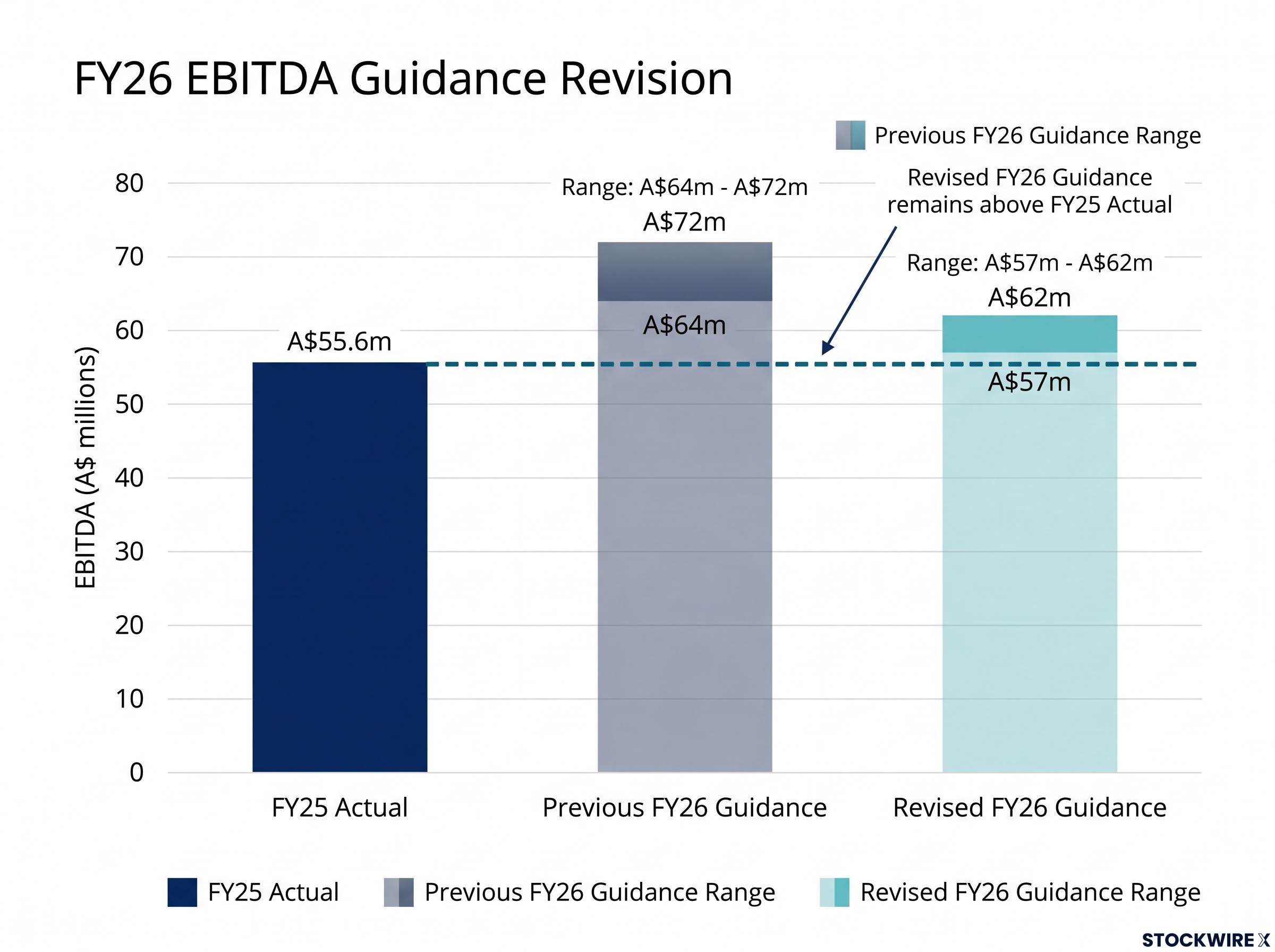

Helloworld Travel (ASX: HLO) has lowered its FY26 earnings guidance to $57 to $62 million EBITDA, down from the previous range of $64 to $72 million, as ongoing Middle Eastern conflict disrupts international flight routes and customer bookings. Despite the downgrade, the revised guidance still positions the company to exceed its $55.6 million actual EBITDA result from FY25. The travel distributor reported that weekly flights from major Middle Eastern carriers—Emirates, Qatar, and Etihad—dropped from 150 per week to nil in March 2026, recovering to approximately 82 per week at present, forcing significant rebookings through alternative Asian carriers and compressing commission margins.

The announcement, released on 5 June 2026, marks the second time the company has adjusted market expectations this financial year. Helloworld initially provided guidance on 23 October 2025 and reaffirmed the range when releasing half-year results on 25 February 2026. Management attributed the revision to protracted uncertainty from the conflict, which has caused flight cancellations and constrained airline capacity, particularly through March and April. Higher jet fuel prices have also led to increased ticket pricing, dampening new travel demand across both Australian and New Zealand markets.

When big ASX news breaks, our subscribers know first

What caused the earnings impact?

The scale of the booking trajectory shift illustrates the extent of disruption. Prior to the commencement of the Middle East conflict, Helloworld’s forward air sales ticketed to depart in Q4 FY26 were tracking 29% above the prior corresponding period in Australia and 16% above in New Zealand. However, high levels of cancellations and rebookings have reversed this momentum, with Q4 FY26 now tracking approximately 4% below prior corresponding period for both markets.

The earnings impact stems primarily from a shift in override income—volume-based commission bonuses travel companies earn from airlines—away from higher-yielding Middle Eastern carrier partners to lower-yielding deals with smaller Asian carrier partners. When capacity constraints force customers to rebook onto alternative routes, Helloworld services the same booking effort but earns reduced commission rates, directly compressing margins.

| Metric | Pre-Conflict | Current |

|---|---|---|

| Q4 FY26 vs pcp (Australia) | +29% | -4% |

| Q4 FY26 vs pcp (New Zealand) | +16% | -4% |

| Middle Eastern carrier flights/week | 150 | ~82 |

How airline disruptions affect travel company earnings

Override income represents a crucial revenue stream for travel distributors. Airlines provide volume-based commission bonuses to agents who deliver high booking numbers, rewarding scale and loyalty. Middle Eastern carriers operate high-margin long-haul routes connecting Australia and New Zealand to Europe and the UK—routes that typically command premium fares and generate higher commission rates for travel companies.

When geopolitical events force capacity to shift from these premium routes to alternative pathways through Asian hubs, the economic equation changes. Smaller Asian carriers operating these substitute routes typically offer lower commission structures. The travel company performs the same booking and customer service work but earns less revenue per transaction. This structural shift in carrier mix explains how total booking volumes can remain similar while earnings compress—the margin per booking has declined due to the enforced change in airline partners.

Recovery outlook and forward bookings signal resilience

Management has indicated that demand typically recovers within 60 to 90 days of conflict resolution, based on the company’s previous experience with geopolitical disruptions. Forward bookings from July onwards are already tracking above the prior year, suggesting customer intent to travel remains intact despite near-term volatility. The company continues to identify opportunities to manage its cost base while maintaining the infrastructure required to service its agent and broker networks when demand rebounds.

CEO and Managing Director Andrew Burnes and CFO Mike Smith will host an investor phone call on Tuesday, 9 June 2026 at 11:00am AEST to discuss the trading update. The call provides an opportunity for investors to gain further detail on recovery expectations and operational responses to the current environment.

Despite the Middle East conflict, leisure travel demand is very resilient and travel is firmly entrenched as a non-discretionary item in households that make up the majority of Helloworld’s market demographic.

Premium travel and product mix provide margin support

While carrier-related margin compression presents near-term headwinds, structural improvements in product mix partially offset the impact. Premium seat sales—premium, business and first-class cabins—now represent approximately 53% of air sales in Australia and 50% in New Zealand (year-to-date FY26), compared to 50% and 46% respectively in the prior corresponding period. This shift toward higher-value bookings provides natural margin support as premium cabin commissions typically exceed economy rates.

Non-air sales, including land packages, cruise bookings, insurance, and car hire, represent 37% of Australian retail sales (up from 34% in the prior corresponding period) and 29% in New Zealand (up from 19%). This diversification away from pure air ticketing reduces exposure to airline commission volatility and taps higher-margin ancillary products. Management noted that complex multi-destination itineraries favour travel agent expertise, reinforcing the value proposition of professional travel services in an increasingly fragmented distribution environment.

- Premium cabin sales growing as share of total air revenue

- Non-air products gaining share, providing margin diversification

- Complex itineraries involving multiple destinations and experiences support agent value proposition

Due to the geographic location of Australia and New Zealand, travel bookings are often complex and include multiple destinations and experiences. Customers want the services of a travel professional to ensure planning is executed correctly and to provide support if disruptions occur.

Dividend and investment portfolio update

The company anticipates paying an FY26 final dividend similar to the FY26 interim dividend paid in March 2026, subject to finalisation of the financial statements and final determination by the Board of Directors. At Helloworld’s closing share price of $1.40 on 4 June 2026, this represents a fully franked yield of approximately 7% per annum.

Helloworld currently holds 78,250,205 ordinary shares in Webjet Group Limited (ASX: WJL), representing 20.118% of voting power when adjusted for WJL’s share buybacks. As WJL’s largest shareholder, Helloworld continues to monitor the performance of the business and assess its options with respect to the investment. The strategic holding provides optionality around capital allocation and potential value realisation as market conditions evolve.

The next major ASX story will hit our subscribers first

What this means for investors

The revised guidance reflects the tangible impact of an external geopolitical event rather than structural weakness in the business model. Forward bookings recovering from July onwards, combined with improving product mix toward premium and non-air categories, suggest the company’s market positioning remains intact. The anticipated dividend of approximately 7% fully franked yield remains subject to finalisation of the FY26 financial statements and final determination by the Board of Directors.

Investors should note that the revised EBITDA range of $57 to $62 million still represents year-on-year growth from the $55.6 million achieved in FY25. The upcoming investor call on 9 June 2026 provides an opportunity for further detail on recovery expectations, cost management initiatives, and strategic responses to the carrier mix shift. The key question for investors is whether management’s 60 to 90 day recovery timeline proves accurate once the Middle Eastern conflict resolves, and whether the structural improvements in premium travel and non-air sales can accelerate margin recovery beyond pre-conflict levels.

The Peter Costello board appointment in June 2026 added further governance weight to the leadership team overseeing the recovery, with the former Treasurer and Future Fund founder bringing deep ASX-listed commercial board experience at a pivotal moment for the business.

Stay Ahead on Travel Sector News

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to receive real-time alerts the moment market-moving announcements hit the ASX.