Baby Bunting Group Expects FY26 Profit Up 32 to 40 Percent Despite Q4 Slowdown

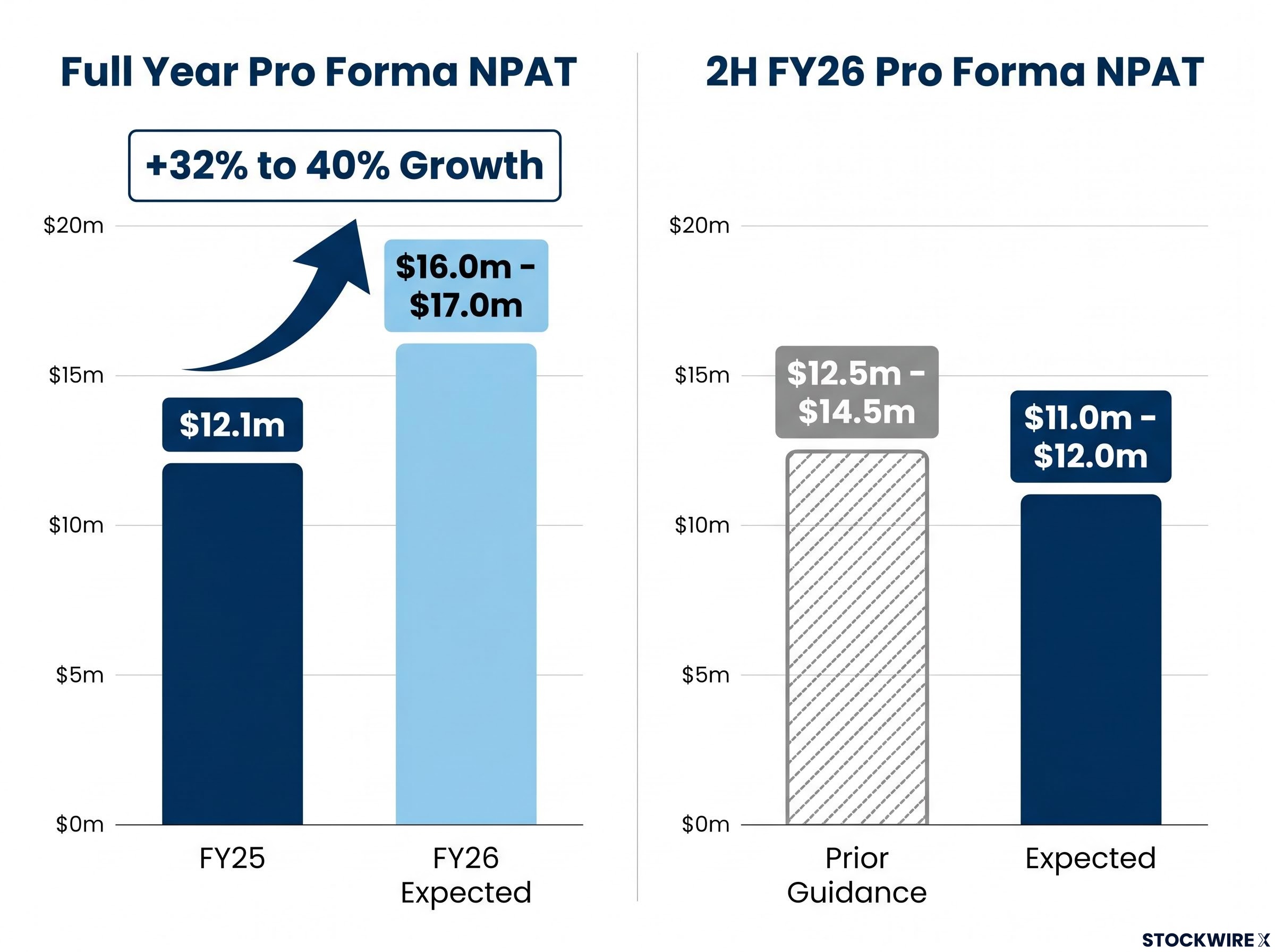

Baby Bunting Group expects FY26 pro forma net profit after tax (NPAT) of approximately $16.0m to $17.0m, up 32% to 40% on FY25’s $12.1m, in a trading update that pairs full-year profit growth with softer-than-expected fourth-quarter trading. The result remains subject to the final week of trade and the year-end audit.

The headline profit growth tells only part of the story. Baby Bunting Group (ASX: BBN) now expects second-half pro forma NPAT of $11.0m to $12.0m, below its previously guided 2H FY26 range of $12.5m to $14.5m.

For investors, the update presents a nuanced picture. Full-year profit growth and margin expansion held firm in a difficult consumer environment, yet a late-quarter slowdown saw the company miss its own prior second-half guidance.

Total sales are expected to land around $553m to $555m, up approximately 6.0% versus the prior corresponding period, with comparable store sales growth of approximately 3.5% for FY26.

A snapshot of FY26 performance

The following table summarises the key expected metrics for FY26 against the prior year where comparable figures are available.

| Metric | FY26 (Expected) | FY25 | Change |

|---|---|---|---|

| Pro forma NPAT | ~$16.0m–$17.0m | $12.1m | +32% to 40% |

| Total sales | ~$553m–$555m | — | +~6.0% |

| Comparable store sales | ~3.5% | — | — |

| Gross margin | Above 41% (~41.5% in 2H) | 40.2% | Expansion |

| Net debt | ~$20m | — | — |

The second-half detail provides further context on both the growth achieved and the shortfall against guidance:

-

2H pro forma NPAT of $11.0m to $12.0m, representing growth of 50% to 64% versus the prior corresponding period, but below the prior guidance range of $12.5m to $14.5m.

-

2H comparable store sales growth of approximately 3%, against the previous guidance assumption of 6% to 8%.

-

2H gross margin of approximately 41.5%.

When big ASX news breaks, our subscribers know first

What drove the Q4 softness

According to the company, trading conditions deteriorated through the fourth quarter, driven by macroeconomic pressures on consumer spending. Management cited three RBA cash rate rises in the second half, together with higher fuel prices, as factors that weighed on consumer spending and added to distribution costs.

Sales across the non-refurbished store network did not meet plan over the last seven weeks. The softness was concentrated in the prams and car safety categories relative to expectations, which lowered average transaction values.

Mark Teperson, CEO

“While trading softened through the fourth quarter, delivering pro forma NPAT growth of 32% to 40% for the full year and further gross margin expansion is a strong result in a difficult consumer environment.”

The framing positions the slowdown as macro-driven and category-specific rather than a structural issue within the business.

Strategic execution: where the business is winning

Beyond the headline guidance revision, several parts of the business continued to perform in line with or ahead of expectations, indicating the transformation strategy is delivering despite cyclical demand pressure.

-

Store of the Future: Sales growth of approximately 18% for FY26 (around 16% in 2H), in line with expectations, and including two of the company’s largest ever store openings in June.

-

Online channel: Sales growth of approximately 16% for FY26, representing double-digit growth.

-

New Zealand: Sales growth above 15% in the second half.

-

Cost and capital discipline: Group costs and capex investment remained in line with expectations, with net debt expected to finish at approximately $20m and a strong balance sheet maintained.

Understanding the “Store of the Future” program

Baby Bunting’s “Store of the Future” initiative applies this approach across its network.

Why does this matter to investors? Refurbished stores delivered approximately 18% for the full year and 16% in the second half growth while the broader network softened. That contrast suggests the programme is generating returns and providing a growth lever that operates somewhat independently of broader macroeconomic conditions.

This growth mechanism gives the company a degree of control over its sales trajectory, even when discretionary consumer spending comes under pressure.

The next major ASX story will hit our subscribers first

The investment case and the road to FY27

Management has expressed confidence in the underlying business despite the near-term consumer headwinds. The stated forward-looking growth levers include a new product pipeline in car safety, clear gross margin levers, and the ongoing refurbishment programme.

Mark Teperson, CEO

“The fundamentals of the business and the strategy we are executing remain strong. We have a great new product pipeline in car safety, clear gross margin levers and a refurbishment program that continues to deliver.”

For investors weighing the guidance revision against the structural growth drivers, the FY27 outlook rests on continued execution across refurbishments, margin, online and New Zealand, alongside the car safety product pipeline.

Key dates:

- FY26 full-year results: Friday, 14 August 2026.

The full-year results will provide investors with the audited figures and further detail on how the company intends to navigate the consumer environment through FY27.

Don’t Miss the Next Consumer Sector Winner

Big News Blast delivers FREE breaking ASX consumer sector news to your inbox within minutes of release, complete with in-depth analysis already done for you. Join 20,000+ investors who stay ahead of the market the moment announcements drop. Click the “Free Alerts” button at StockWire X to start receiving alerts today.