Southern Cross Media Targets $150M Cost Cuts Amid Weak TV Advertising Market

Southern Cross Media announces $150 million cost reduction program amid challenging advertising market

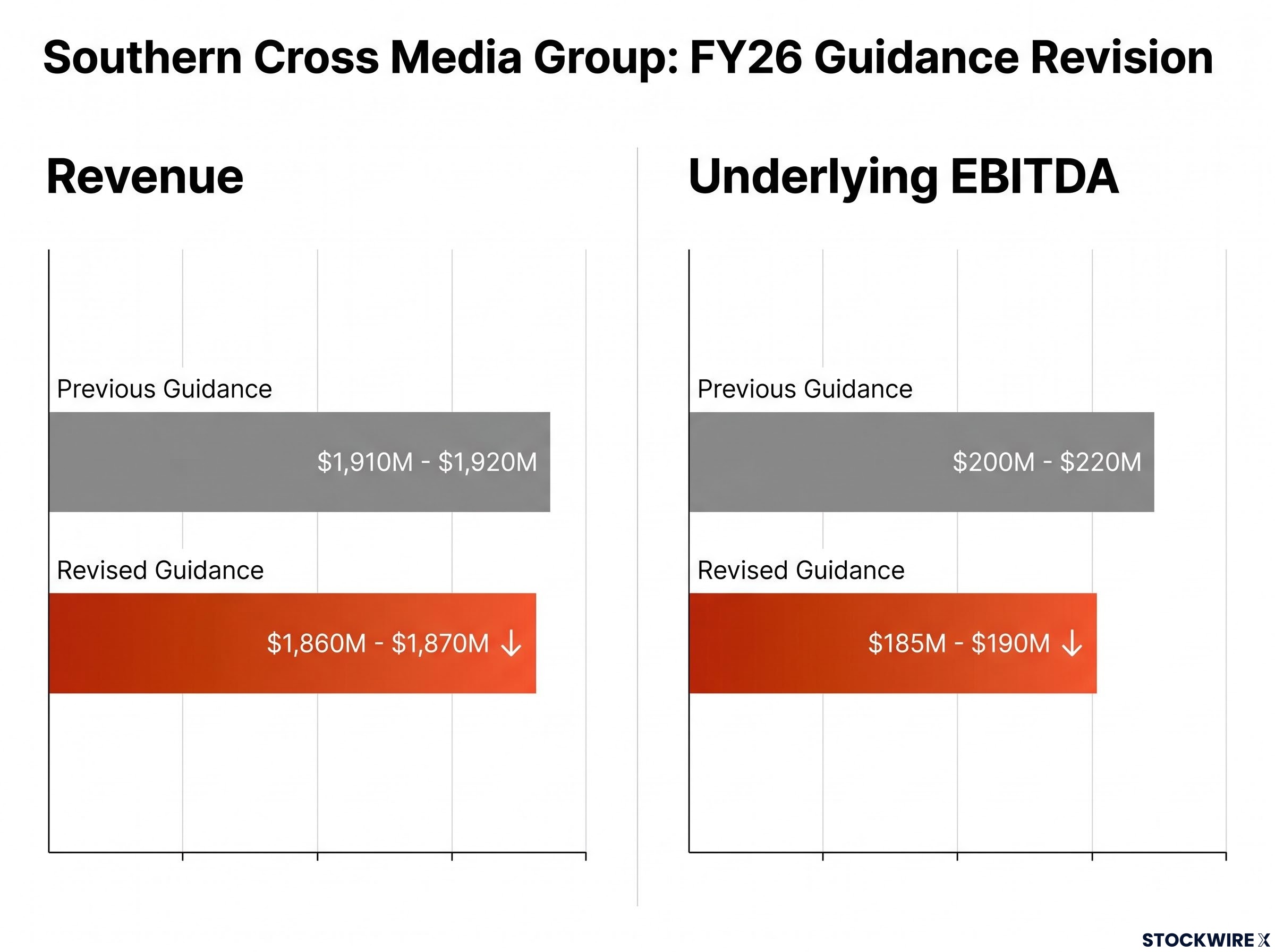

Southern Cross Media Group has launched a major cost reduction program targeting annual savings of $145 to $150 million while revising its FY26 financial guidance downward following a material deterioration in advertising market conditions through the fourth quarter. The Group now expects FY26 revenue of $1,860 to $1,870 million versus previous guidance of $1,910 to $1,920 million, with underlying EBITDA guidance revised to $185 to $190 million from $200 to $220 million. Reported EBITDA is expected at $190 to $195 million after accounting adjustments.

The dual announcement represents management taking decisive action to reset the business for current market conditions rather than waiting for recovery. Market softness has been particularly pronounced in the TV segment through Q4 FY26, with the revenue shortfall of approximately 2.5% below the guidance range reflecting broader macroeconomic pressures affecting advertiser spending. The cost reduction program builds on merger synergies already delivered and aims to create a leaner, more flexible cost base capable of competing for the structural shift toward premium, trusted local content.

Proactive cost management has partially mitigated the revenue impact, with operating costs now expected at $1,670 to $1,680 million, around 1.5% lower than previous guidance and down 3% from $1,728 million in FY25 despite estimated cost inflation of up to 4%.

When big ASX news breaks, our subscribers know first

What is an onerous contract provision?

An onerous contract provision is an accounting treatment required when the unavoidable costs of fulfilling a contract exceed the economic benefits expected from it. This is a non-cash accounting adjustment that does not represent money leaving the business, but rather recognises on the balance sheet that certain contractual obligations have become uneconomical.

Media companies face this issue when legacy content deals signed during different market conditions become unprofitable as advertising revenues decline. If a broadcaster commits to paying $50 million for programming rights but can only generate $40 million in advertising revenue from that content, accounting standards require the $10 million shortfall to be recognised as a provision. The provision affects reported earnings but does not change the company’s cash position or alter the underlying contract terms.

Under AASB 3 Business Combinations, provisions identified in the period following a merger are recognised through purchase price accounting from the acquisition date. For Southern Cross Media, this means the onerous contract provision will be recognised with effect from the 7 January 2026 merger date of SCA and Seven West Media, lifting reported EBITDA in FY26 and FY27 as the provision is utilised against contract costs.

Investors should distinguish between this accounting treatment and operational performance. While the provision signals management’s revised assessment of content value, the cash cost of the contracts was already committed regardless of the accounting entry.

Cost reduction program targets $145 to $150 million in annual savings

The expanded cost reduction program is expected to deliver annual run-rate benefits of $145 to $150 million upon conclusion, building on merger synergies that have already achieved $30 million in run-rate savings in line with target and earlier than the previously estimated FY27 delivery date. The program will result in 250 to 300 FTE leaving the Group before 30 June 2026, subject to finalising consultation processes, with an associated FY26 restructuring charge of approximately $20 million.

The $30 million in merger synergy targets delivered ahead of schedule builds on the audio division’s strong H1 FY26 result, where underlying EBITDA grew 28% to $40 million even as metro radio advertising markets declined 7%.

The program focuses on several key areas designed to remove duplication and improve operational efficiency:

- Removing duplication across the merged business

- Streamlining and automating processes

- Focusing content acquisition on higher-value programming

- Leveraging management infrastructure and procurement scale across the enlarged Group

Implementation primarily impacts mid and back office functions, corporate staff, and non-labour costs. Management has emphasised that the program is being carefully managed to limit disruption to clients, audiences, and continuing employees, with communications conducted in accordance with industrial and legal obligations.

| Metric | Figure |

|---|---|

| Target annual run-rate savings | $145-$150 million |

| Merger synergies already delivered | $30 million |

| FTE reductions before 30 June 2026 | 250-300 |

| FY26 restructuring charge | ~$20 million |

The expanded program aims to offset future cost inflation and fund targeted growth investments, creating a leaner, more flexible cost base positioned to compete in markets increasingly favouring premium, trusted local content. The annual savings will improve earnings through offsetting ongoing cost inflation while providing capacity for limited investment in building growth capability.

CEO Rohan Lund acknowledged the difficult decisions required:

Rohan Lund, Managing Director and CEO

“We must reset our cost base to meet current market conditions and capture the full benefits of scale across our trusted platforms for our audiences and advertisers, now and into the future. Unfortunately, this means saying goodbye to some talented colleagues who have helped build our business. We are deeply grateful for their contributions, and we are committed to supporting them through this transition.”

Strong audience performance despite revenue headwinds

The Group’s operational performance remains strong despite advertising market softness, with audience metrics across television, audio, and publishing demonstrating positive momentum. The company has achieved revenue share gains in both TV and Audio segments, supported by merger synergies that are combining content, sales, and operations activities across the portfolio.

Key audience achievements for the financial year to date through May 2026:

- Total TV audience share up 1.1 percentage points financial year to date through May 2026

- HIT network: number one for people 25-54 (19% share) and women 25-54 (21% share)

- Triple M: leading network for men 25-54 (22% share)

- West Australian brand group: average unique monthly audience of 3.36 million

- The Nightly: average monthly audience of 3 million

The audience strength across platforms positions the Group well for market recovery, with the company delivering the premium, trusted local content that structural market changes are increasingly favouring. Revenue share gains in both TV and Audio have partially offset weaker market conditions, demonstrating that the business is performing well relative to the broader advertising market.

The combination of strong audience performance and cost discipline provides a foundation for the business to capture market opportunities when advertising conditions improve. Management’s ability to deliver revenue share gains despite challenging market conditions validates the strategic rationale for the SCA and Seven West Media merger.

Onerous contract provision to boost reported EBITDA in FY27

Southern Cross Media expects to recognise an onerous contract provision of $65 to $70 million relating to legacy TV content contracts, subject to finalising year-end audit procedures. The provision takes effect from the date of the SCA/Seven West Media merger on 7 January 2026 and will be recognised as part of the purchase price accounting process required under AASB 3 Business Combinations.

The reported EBITDA impact will flow through as the provision is utilised against contract costs:

- FY26: Approximately $5 million uplift to reported EBITDA

- FY27: Approximately $30 million uplift to reported EBITDA

This is a non-cash accounting adjustment that does not impact cash flows. The provision reflects management’s revised assessment of the direct and indirect benefits likely to be derived from a range of legacy content contracts, taking account of subdued trading conditions and structural changes in the TV advertising market.

The reassessment of content contract profitability is conducted each reporting period. Where unavoidable costs of meeting contractual obligations exceed the economic benefits expected from the content, accounting standards require an onerous contract provision. The provision effectively recognises that certain programming commitments made in different market conditions have become uneconomical under current advertising revenue levels.

While the provision reflects a challenging outlook for legacy TV content deals signed before market conditions deteriorated, the accounting treatment provides near-term earnings support. Investors should focus on the cash flow neutrality of this adjustment when evaluating the company’s financial performance, distinguishing between reported EBITDA (which benefits from the provision utilisation) and underlying operational cash generation.

FY26 cost performance ahead of guidance despite revenue miss

Southern Cross Media has demonstrated strong cost discipline despite the revenue shortfall, with operating costs expected at $1,670 to $1,680 million, around 1.5% lower than previous guidance. This performance is particularly notable given estimated cost inflation of up to 4% affecting the business, with total costs down 3% from $1,728 million in FY25.

Merger synergies are contributing to cost outperformance, with the Group having delivered cost synergies with an annualised benefit of $30 million to date, in line with the upwardly revised target announced in February and earlier than the previously estimated FY27 delivery date. The cost control capability demonstrated through FY26 supports confidence in management’s ability to execute the expanded $145 to $150 million cost reduction program.

The EBITDA revision is primarily revenue-driven rather than a cost blowout. The revenue shortfall of approximately 2.5% below the guidance range reflects weaker market conditions, particularly material deterioration in the TV segment through Q4 FY26. Proactive cost management partially mitigated the revenue impact, preventing a more significant EBITDA miss.

The cost performance validates the strategic focus on removing duplication, streamlining processes, and leveraging scale across the merged business. Management’s track record of delivering merger synergies ahead of schedule and below initial cost guidance provides credibility for the expanded cost reduction program targeting annual run-rate benefits of $145 to $150 million.

The next major ASX story will hit our subscribers first

What to watch for at the August results

Southern Cross Media Group has scheduled its full-year results presentation for 11 August 2026, which will provide critical insights into the company’s FY27 trajectory and the cost reduction program’s execution. The results will offer the first comprehensive view of the merged entity’s performance and management’s strategic response to challenging market conditions.

Key items investors should monitor at the August results:

- FY27 guidance: Management’s revenue and EBITDA outlook will signal whether market conditions are expected to stabilise or deteriorate further

- Progress on cost reduction program implementation: Updates on the 250 to 300 FTE departures and whether the $145 to $150 million annual savings target remains on track

- Final onerous contract provision figure post-audit: Confirmation of the $65 to $70 million provision range following completion of year-end audit procedures

- Update on merger integration and synergy realisation: Detail on the $30 million in merger synergies already delivered and any additional opportunities identified

- Advertising market outlook commentary: Management’s assessment of structural changes in the TV advertising market and recovery timeframes

The August results will clarify whether the cost reduction program is tracking to deliver the targeted savings and provide visibility on the company’s earnings trajectory once the program concludes. Investors should focus on management’s commentary around structural versus cyclical challenges in the TV advertising market, as this will determine whether the business requires further cost restructuring or is appropriately sized for current conditions.

The onerous contract provision’s final quantum will also be confirmed following year-end audit processes, providing certainty around the FY27 reported EBITDA uplift of approximately $30 million from provision utilisation.

Stay Ahead on Media Sector Shake-Ups

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to get media sector announcements delivered straight to your inbox the moment they hit the market.