Aussie Broadband Completes $115M AGL Deal to Become Australia’s Third-Largest NBN

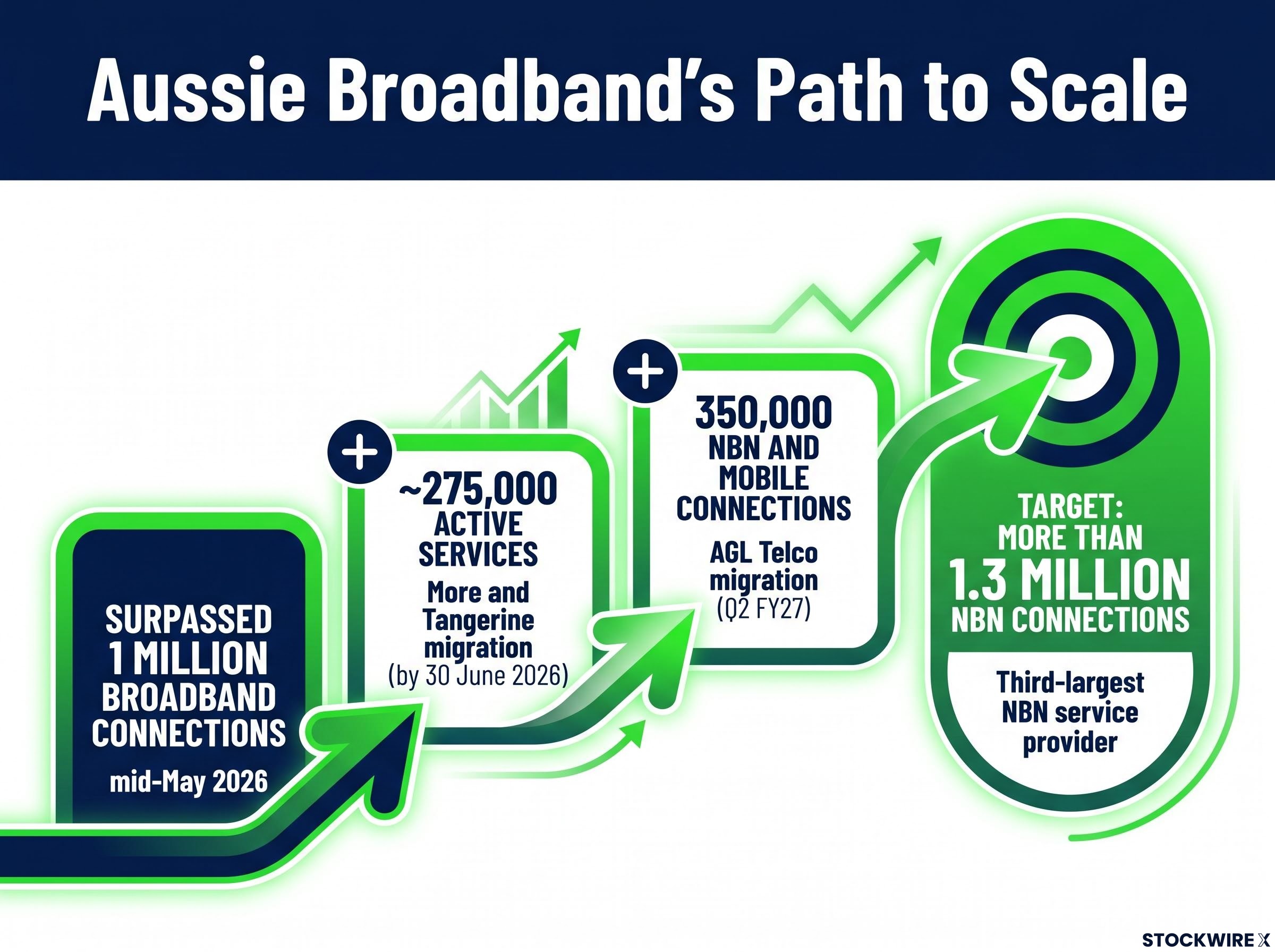

Aussie Broadband has completed the acquisition of AGL Energy’s telecommunications business, issuing $115 million in shares to AGL and providing a trading update that confirms the company surpassed 1 million broadband connections in mid-May 2026. The completion of AGL Telco, alongside three other strategic transactions in H2 FY26, positions the company to become Australia’s third-largest NBN service provider with more than 1.3 million NBN connections following migration completion in Q2 FY27.

Aussie Broadband completes AGL Telco acquisition, issues $115 million in shares

The AGL Telco acquisition completed on 15 June 2026, with AGL receiving $115 million in ABB shares under a Share Subscription Agreement. The transaction structure saw AGL issued approximately 22 million fully paid ordinary shares, representing approximately 7% of the company’s issued capital post-issuance. The share price was calculated using the 90-day volume-weighted average price (VWAP) to 9 February 2026.

The AGL Telco acquisition was structured as an all-scrip deal, with performance-linked incentives of up to $10 million in additional shares tied to net connection growth targets over the partnership term.

Migration of AGL’s combined 350,000 NBN and mobile connections will complete in Q2 FY27 (October-December 2026), delivering a step change in scale for the company’s network. The acquisition is expected to contribute $21 million in underlying EBITDA in the first 12 months post migration, with potential upside from further connection growth through AGL’s existing marketing channels and bundled energy offerings.

The strategic partnership provides exposure to AGL’s approximately 4.5 million customer base, with an ambition to grow telecommunications connections to 500,000 over time.

When big ASX news breaks, our subscribers know first

More and Tangerine migration on track for 30 June completion

Migration under the exclusive Wholesale Services Agreement with More Telecom — which includes the residential and business customers of both More and its jointly operated group company Tangerine Telecom — is on schedule for completion by the end of June 2026. Active services at 30 June 2026 are expected to be approximately 275,000, which is approximately 95% of the previously announced estimate.

The wholesale agreement is expected to deliver $12 million in annualised underlying EBITDA from FY27 before amortised incentives, or $7 million post incentives (amortised over the term of the contract). The company noted that the Buddy Telco brand and assets were divested to Tangerine during H2 FY26, but the connections will remain on the Aussie Broadband network under the Wholesale Services Agreement.

This wholesale arrangement delivers recurring revenue with limited execution risk, as the connections are migrating to ABB’s network infrastructure rather than being acquired outright as customer assets.

What a wholesale services agreement means for investors

A wholesale services agreement is a commercial arrangement where Aussie Broadband provides the underlying network infrastructure while the retail brand (in this case More and Tangerine) maintains the customer relationship and billing function. Under this model, ABB earns recurring wholesale fees for network access without incurring customer acquisition costs or retail overheads.

This capital-light structure is attractive because ABB does not acquire customer contracts or brands, reducing integration risk and upfront capital requirements. The company generates predictable wholesale revenue streams while the retail partner handles customer service, marketing, and retention activities.

This contrasts with the AGL Telco acquisition, where ABB is acquiring customer assets directly and will assume full responsibility for customer relationships, service delivery, and retention. Each model serves different strategic purposes: direct acquisition (AGL Telco) delivers higher per-customer economics and strategic partnership opportunities, while wholesale partnerships (More/Tangerine) provide rapid scale with minimal execution risk.

Four transactions completed in six months

Aussie Broadband completed four strategic transactions during H2 FY26, demonstrating execution capability across acquisition, divestment, and partnership structures. The table below summarises the transactions and their expected financial contributions:

| Transaction | Structure | Expected EBITDA Contribution | Completion |

|---|---|---|---|

| AGL Telco | Acquisition (share issuance) | $21m (12 months post migration) | 15 June 2026 |

| More/Tangerine | Wholesale Services Agreement | $12m annualised ($7m post incentives) | 30 June 2026 |

| Nexgen Investment Group | Acquisition | Not separately disclosed | H2 FY26 |

| Digital Sense Hosting | Divestment | N/A | H2 FY26 |

The volume of completed transactions demonstrates operational capability, though investors should note that EBITDA contributions from the Nexgen acquisition have not been separately disclosed. The divestment of Digital Sense Hosting represents a portfolio rationalisation, with the company focusing capital and management attention on core telecommunications infrastructure and services.

The Nexgen acquisition, completed earlier in H2 FY26, extended ABB’s SME unified communications suite and added Agentic AI capabilities at a 4.1x EBITDA multiple after synergies, funded from existing cash and debt facilities without shareholder dilution.

ABB surpasses 1 million broadband connections, targeting 1.3 million by Q2 FY27

Aussie Broadband surpassed 1 million broadband connections in mid-May 2026, a milestone driven by organic growth. The company delivered organic net connection growth of approximately 28,000 in the five months to 31 May 2026 and approximately 67,000 in FY26 to 31 May 2026 (including approximately 2,500 Buddy connections added in H1 FY26).

Following completion of the More and Tangerine migration by 30 June 2026 and the AGL Telco migration in Q2 FY27, ABB is on track to become the third-largest NBN service provider with more than 1.3 million NBN connections.

The organic growth trajectory demonstrates underlying business momentum independent of M&A activity. The company noted that competition remains strong but highlighted that its FY27 pricing plans, Australian-based customer service focus, and high-quality network performance position it well to continue winning customers migrating from legacy technologies and lower-speed services.

Balance sheet strength and capital flexibility

The company’s net debt to EBITDA ratio stood at 0.72x at the end of May 2026, reflecting a strong balance sheet position following the completion of four strategic transactions in H2 FY26. The AGL Telco acquisition was funded entirely through share issuance, preserving debt capacity and providing financial flexibility for future growth opportunities.

Management commentary highlighted the company’s “increasing flexibility to support future capital management initiatives alongside continued investment in growth opportunities,” reflecting the combination of low leverage, strong cashflow profile, and immediate earnings contributions from completed transactions. The transition to an increasingly capital-light operating model is expected to further enhance cash generation and balance sheet optionality.

While the announcement references future capital management flexibility, no specific actions such as share buybacks or dividend policy changes were disclosed. Investors should monitor future updates for clarity on how excess capital capacity will be deployed.

FY26 guidance reaffirmed; earnings expected at mid-range

Aussie Broadband expects to report FY26 underlying EBITDA in the middle of the previously announced guidance range of $162 million to $167 million. Capital expenditure is expected to come in at the upper end of the previously provided guidance range of $55 million to $60 million.

The company will release its financial results for the year ending 30 June 2026 on Monday 24 August 2026. Details of an investor webcast will be provided at a later date.

The mid-range EBITDA outcome with upper-end capital expenditure suggests slightly lower conversion to cash in FY26, though the company’s commentary on transitioning to an increasingly capital-light model indicates this should improve in FY27 and beyond as the acquired connections migrate and scale benefits materialise.

Look-to-28 strategic ambitions

Aussie Broadband outlined its upgraded Look-to-28 strategic ambitions in February 2026, which represent aspirational targets rather than formal earnings guidance. The strategic ambitions are:

- Group revenue: $1.5 billion

- Residential contribution: 40%

- EBITDA margin: 15%+

- NBN market share: 15% (excluding satellite)

- EPS growth: 15%+ (based on underlying NPATA in FY25)

The company explicitly stated that “these strategic ambitions do not constitute guidance and carry risks and uncertainties, including from events beyond Aussie Broadband’s control.” Investors should monitor progress against these targets over the next two financial years but should not treat them as committed forecasts or performance guarantees.

The completed transactions in H2 FY26 represent material progress toward these ambitions, particularly the NBN market share target of 15% (the company will hold more than 1.3 million NBN connections post-migration, representing a significant step toward this goal).

The next major ASX story will hit our subscribers first

CEO commentary

Brian Maher, Group Chief Executive

“I’m immensely proud of the effort delivered by the team. Completing one transaction is significant but completing four transactions within six months, while delivering the largest migration of connections on the NBN network to date and continuing to grow the business organically, is exceptional.

“These transactions are central to our upgraded Look-to-28 ambitions, repositioning the Company to deliver higher-quality and more sustainable earnings streams. While competition remains strong, our FY27 pricing plans, continued focus on Australian-based customer service, and high-quality network performance position us well to continue winning new customers, particularly those migrating from legacy technologies and lower-speed services.

“The operational leverage from increased scale is expected to improve capital efficiency and support stronger returns over time.”

The CEO’s comments emphasise operational execution and strategic positioning, highlighting the company’s ability to complete complex transactions while maintaining organic growth momentum.

Near-term catalysts for investors include the completion of the AGL Telco migration in Q2 FY27 (October-December 2026) and the release of FY26 full-year results on 24 August 2026. The results release will provide clarity on the financial impact of completed transactions and updated guidance for FY27.

Don’t Miss the Next Communications Breakthrough

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to start receiving telecommunications sector alerts the moment market-moving announcements hit the wire.