Ryman Healthcare Launches $150M Bond Offer at 5.6%+ to Refinance Debt

Ryman Healthcare launches up to NZ$100 million fixed rate bond offer (plus up to NZ$50 million oversubscriptions)

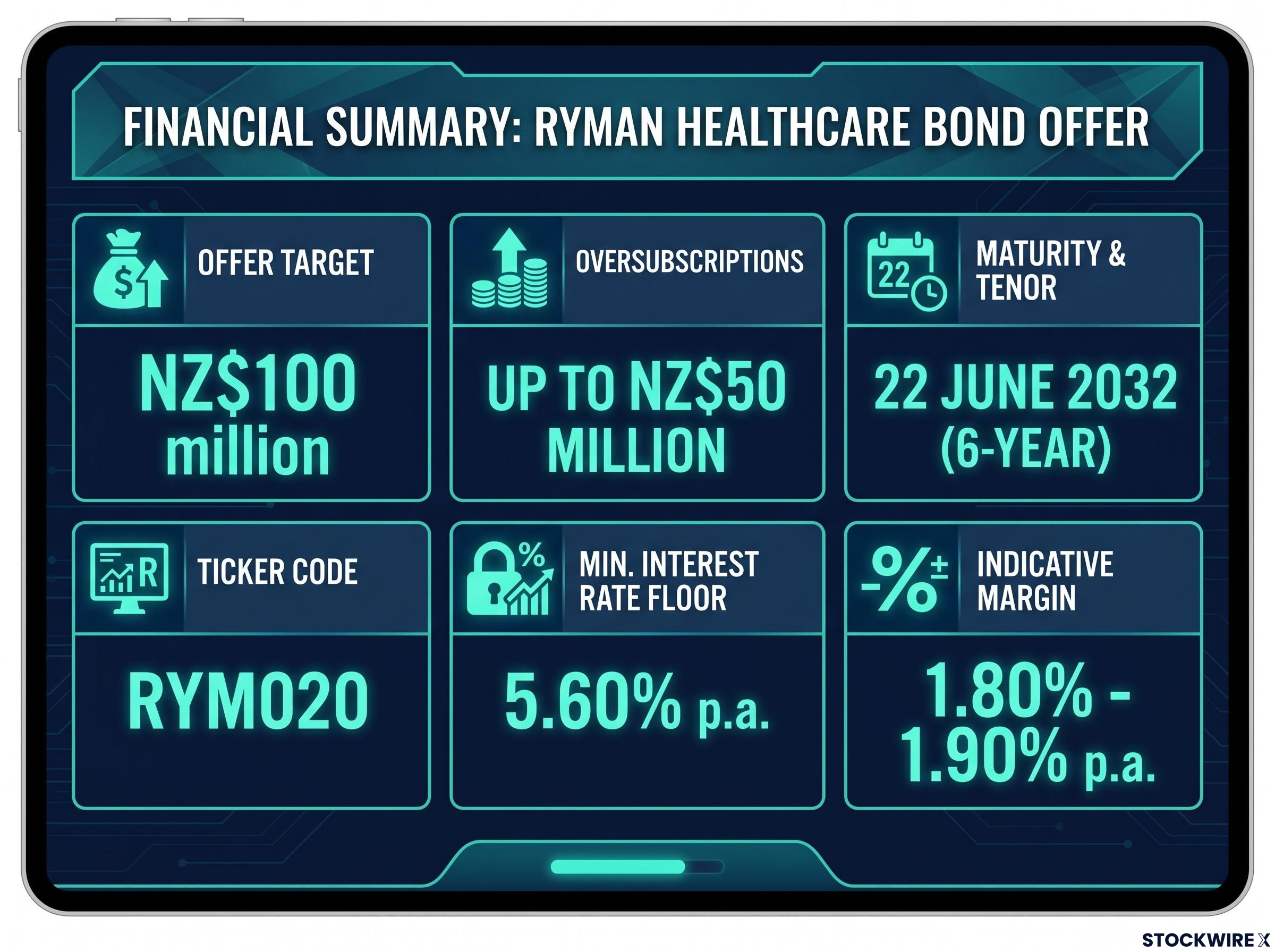

Ryman Healthcare Limited (ASX: RYM) has launched an offer of up to NZ$100 million in fixed rate bonds, with the ability to accept up to NZ$50 million in oversubscriptions at its discretion. The bonds mature on 22 June 2032, providing a 6-year tenor for investors seeking fixed income exposure to one of Australasia’s largest retirement village operators.

The offer opened on 8 June 2026 with expected quotation on the NZX Debt Market under ticker code RYM020 on 23 June 2026. The purpose of the raise is to diversify funding sources, repay existing bank debt, refinance existing RYM010 bonds, and provide capital for general corporate purposes.

Investment significance: This bond offer provides Ryman with capital flexibility while giving investors access to secured debt exposure to one of Australasia’s largest retirement village operators. The bonds are secured, unsubordinated, and rank equally with other senior debt obligations.

When big ASX news breaks, our subscribers know first

Understanding fixed rate bonds

Fixed rate bonds are debt securities where the issuer pays a set interest rate for the life of the bond, regardless of what happens to market interest rates. This contrasts with floating rate notes, where the interest rate adjusts periodically based on market benchmarks.

For investors, fixed rate bonds offer predictable income over the entire term. If market interest rates fall after you purchase the bond, you continue receiving the higher fixed rate, protecting your income stream from rate declines.

Ryman’s bonds are described as “secured” and “unsubordinated” in the offer documentation. Secured status means the bonds are backed by specific assets that bondholders can claim if Ryman defaults. Unsubordinated means these bonds rank equally with other senior debt in the repayment hierarchy.

Investment significance: For income-focused investors, fixed rate bonds offer certainty of returns regardless of future interest rate movements, while the secured status provides additional protection relative to unsecured debt.

Interest rate and pricing structure

The interest rate on the bonds is calculated as the Swap Rate plus the Issue Margin. Ryman has provided an indicative issue margin range of 1.80% – 1.90% per annum, with a minimum interest rate floor of 5.60% per annum.

The final issue margin (which may fall within, above, or below the indicative range) will be determined by Ryman in consultation with the Joint Lead Managers following a bookbuild process. The interest rate will be announced via NZX on or about 11 June 2026.

Interest is paid quarterly in arrear on 22 March, 22 June, 22 September, and 22 December each year (or the next business day if these dates fall on a non-business day). The first interest payment date is 22 September 2026. The issue price is NZ$1.00 per bond.

Key payment dates:

- 22 March (quarterly)

- 22 June (quarterly)

- 22 September (quarterly, first payment 2026)

- 22 December (quarterly)

Investment significance: The quarterly payment structure provides regular income, whilst the minimum interest rate floor of 5.60% per annum offers downside protection if the calculated rate would otherwise fall below this level.

Exchange mechanism for existing RYM010 bondholders

Holders of existing RYM010 bonds (NZ$150 million outstanding, 2.55% per annum, maturing December 2026) who hold through custodial accounts may exchange into the new RYM020 bonds. The exchange is on a one-for-one basis at NZ$1.00 face value, with no additional cash payment required for bonds obtained via exchange.

Custodial RYM010 bondholders who exchange will receive a final interest payment on their RYM010 bonds for the period up to the issue date. The exchange mechanism opens 11 June 2026 and closes at 5:00pm NZT on 17 June 2026.

As at 4 June 2026, the 20-day average market price of RYM010 bonds was NZ$0.9918 per bond. Exchanged RYM010 bonds will be purchased by Ryman on the issue date and cancelled, reducing the total amount of RYM010 bonds outstanding. This may impact trading of the RYM010 bonds on the secondary market.

The exchange mechanism is available only to custodial RYM010 bondholders who receive an allocation of the new bonds from a bookbuild participant and who have agreed the exchange with that participant. Holders of RYM010 bonds may choose to retain their existing bonds rather than participate.

Investment significance: This mechanism allows existing bondholders to roll their investment into a longer-dated instrument with a higher interest rate, avoiding transaction costs of selling and repurchasing. The exchange at face value compares to the current secondary market price of approximately NZ$0.99 per RYM010 bond.

Security structure and investor protections

Bondholders will share the benefit of the same security package as Ryman’s banks and other debt funding providers on a pro rata basis. This security is held by the Security Trustee and includes first ranking registered mortgages over land and buildings owned by NZ Guarantors (excluding certain village-specific land), and general security agreements granted by NZ and Australian Guarantors.

For NZ Guarantors that are not NZ Village Companies, the Security Trustee holds first ranking mortgages over all land and buildings owned by that entity, including bare land and land under development. For NZ Village Companies (entities that own and operate a retirement village registered under the Retirement Villages Act 2003), the Security Trustee holds first ranking mortgages only over land and buildings on separate legal titles to any land allocated for Units (excluding care centres that include Care Suites).

Separately, each NZ Village Company provides first ranking mortgages to the Statutory Supervisor over all land and buildings containing Units and land on which a care centre including Care Suites is located. Under the Security Sharing Deed, the Statutory Supervisor is entitled to proceeds of enforcement in priority to the Security Trustee to the extent that proceeds relate to a Unit, the land on which the Unit is located, or land on which a care centre with Care Suites is located. Remaining proceeds are shared between beneficiaries (including bondholders) on a pro rata basis.

For Australian Guarantors that operate retirement villages registered under the Retirement Villages Act 1986 (Vic), each resident has the benefit of a statutory charge over the land to secure the Australian Village Company’s obligation to repay the Australian Resident Loan. This statutory charge ranks ahead of the security interest held by the Security Trustee.

| Security Type | Scope | Ranking |

|---|---|---|

| Registered mortgages | NZ land and buildings (excluding village-specific land allocated for Units) | First ranking |

| General security agreements | NZ and Australian Guarantors | As described in Trust Deed |

| Statutory Supervisor arrangement | Village-related land/units | Priority for unit-related proceeds |

Investment significance: The multi-layered security structure provides bondholders with tangible asset backing, though investors should understand the priority waterfall in any enforcement scenario. The Statutory Supervisor’s priority for unit-related proceeds and the Australian residents’ statutory charges both rank ahead of the Security Trustee’s interests in specific circumstances.

Financial covenants

Two key financial covenants apply to the bonds, providing structural protection by limiting Ryman’s ability to over-leverage.

The Debt to Equity Covenant requires that Total Liabilities of the Ryman Group (after deducting the aggregate value of all Resident Occupancy Advances, Australian Resident Loans and Accommodation Bonds) to Net Tangible Assets must not exceed 1.0:1.0 at all times.

If this covenant is breached, Ryman has 6 months from the date of the 6-monthly compliance report to remedy the breach. If not remedied within 6 months, Ryman must give notice to the Bond Supervisor within 20 Business Days after such date of its plan to remedy the breach. If the breach is not remedied within 6 months of the date of that notice (or the date on which it should have been delivered, if earlier), an Event of Default occurs. This provides approximately 13 months total before a continued breach becomes an Event of Default.

The Guaranteeing Group Coverage Covenant requires that the Guaranteeing Group must represent at least 90% of Total Tangible Assets and Adjusted EBITDA of the Ryman Group for the last twelve months. A breach of this covenant is an Event of Default if it is not remedied within 30 days and is, or is likely to be, materially prejudicial to bondholders.

Under Ryman’s bank facility agreement, the company is not permitted to make distributions if the equivalent debt to equity covenant is breached, unless this restriction is waived by the relevant majority of beneficiaries. This distribution stopper operates independently of the bondholder covenants.

Investment significance: These covenants provide structural protection by limiting Ryman’s ability to over-leverage and ensuring the guarantor group maintains substantial coverage of group assets. The extended cure period for the Debt to Equity Covenant gives Ryman time to remedy a breach before it becomes an Event of Default.

Key dates and how to participate

All bonds, including oversubscriptions, are reserved for clients of the Joint Lead Managers, institutional investors, and invitees to the bookbuild. There is no public pool. Retail investors should contact their financial adviser or one of the Joint Lead Managers (ANZ, Craigs Investment Partners, Forsyth Barr, or Westpac NZ) for details on acquiring bonds.

The minimum application is NZ$5,000, with increments of NZ$1,000 thereafter. Brokerage of 0.40% plus 0.35% on firm allocations will be paid by Ryman. Neither Ryman nor the bonds are credit rated.

Indicative timetable:

- Opening Date: Monday, 8 June 2026

- Closing Date: Thursday, 11:00am NZT, 11 June 2026

- Interest Rate Set Date: Thursday, 11 June 2026

- Issue Date: Monday, 22 June 2026

- Expected Quotation: Tuesday, 23 June 2026

- Maturity Date: 22 June 2032

These dates are indicative and subject to change at Ryman’s discretion. The offer may open or close early, accept late applications, or extend the closing date without notice.

Investment significance: The closed nature of the offer means retail investors must work through primary market participants to acquire bonds. Prospective investors should contact advisers early to ensure allocations can be secured within the compressed timeline.

The next major ASX story will hit our subscribers first

Investment considerations

The bond offer suits investors seeking predictable income from a secured instrument with a defined 6-year horizon. Key attractions include secured debt exposure, fixed income with known maturity, and the exchange mechanism for existing RYM010 holders seeking to extend their investment tenor at a higher interest rate.

Neither bondholders nor Ryman are able to redeem the bonds before the maturity date, except in the event of an Event of Default. Transfer restrictions apply: bondholders must maintain a minimum holding of NZ$5,000, and transfers must be in NZ$1,000 multiples.

Ryman is not credit rated, meaning investors cannot rely on an independent credit assessment from a rating agency. Prospective investors should assess the company’s financial position independently by reviewing disclosures available on NZX at www.nzx.com/companies/RYM.

Ryman’s FY26 financial results reported free cash flow of $188.3m, the company’s first positive result in a decade, with gearing falling to 27.8% and $675m in liquidity headroom following a $2 billion bank facility refinancing.

The bonds are direct, secured, unsubordinated obligations of Ryman, ranking equally with all other unsubordinated obligations except indebtedness preferred by law. The security structure involves multiple layers, with certain claims (Statutory Supervisor for unit-related proceeds, Australian resident statutory charges) ranking ahead of the Security Trustee’s interests in specific enforcement scenarios.

Investment significance: The bond offer suits investors seeking predictable income from a secured instrument with a defined 6-year horizon, though the absence of a credit rating means additional due diligence is warranted. The inability to redeem early means investors must be comfortable locking in capital until 2032 unless they sell on the secondary market.

Want the Next Healthcare Investment in Your Inbox?

Join 20,000+ investors receiving FREE breaking ASX healthcare news within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to get market-moving announcements delivered straight to your inbox the moment they break.