More than USD 6.5 billion in pharmaceutical M&A flowed into one narrow corner of oncology between late 2023 and 2025. The companies writing those cheques were not startups chasing speculative science; they were Novartis, Eli Lilly, and Bristol-Myers Squibb. Targeted nuclear medicine, a field that pairs radioactive isotopes with precision-guided molecules, has moved from a specialist imaging niche into a strategic priority for large-cap pharma. Yet most investors encounter the sector through individual stock screens rather than a coherent framework for understanding why the opportunity exists and what shapes it. This article builds that framework, explaining what radiopharmaceuticals physically do, why their clinical properties translate into a defensible investment thesis, and how the sector’s structure, from supply chains to acquisition dynamics, determines which companies are positioned to compound their advantages over time.

What radiopharmaceuticals actually are (and why they behave differently from conventional drugs)

A radiopharmaceutical is a compound built from two components: a targeting molecule (typically a peptide or antibody fragment) and a radioactive isotope. The targeting molecule locks onto a specific cell type, most commonly a cancer cell expressing a known receptor. The isotope delivers its radiation dose directly at that site, concentrating the destructive energy on the tumour rather than distributing it systemically through the bloodstream the way conventional chemotherapy does.

The isotope determines the function. Three broad categories define the field:

- Technetium-99m (Tc-99m): The dominant SPECT imaging isotope by clinical volume, used across cardiac, bone, and oncological diagnostics.

- Gallium-68 (Ga-68): A PET diagnostic isotope used in agents such as Telix Pharmaceuticals’ Illuccix for prostate cancer imaging.

- Lutetium-177 (Lu-177): The therapeutic backbone across most current pipeline agents, including Novartis’s Pluvicto (lutetium-PSMA-617), the established commercial reference point for radioligand therapy.

The theranostic model: one target, two applications

The same biological target can be addressed by both a diagnostic and a therapeutic radiopharmaceutical. The PSMA receptor on prostate cancer cells, for example, is targeted by Illuccix for imaging and by Pluvicto for treatment. The targeting molecule stays the same; only the isotope changes.

This structural feature compresses development risk in a way that single-use drugs cannot replicate. Imaging data from the diagnostic agent informs patient selection for the therapeutic, reducing the clinical trial failure rates that arise when patient populations are too heterogeneous. One biological insight produces two commercial products and a built-in mechanism for identifying which patients are most likely to respond.

When big ASX news breaks, our subscribers know first

Why the clinical profile creates a structural investment thesis

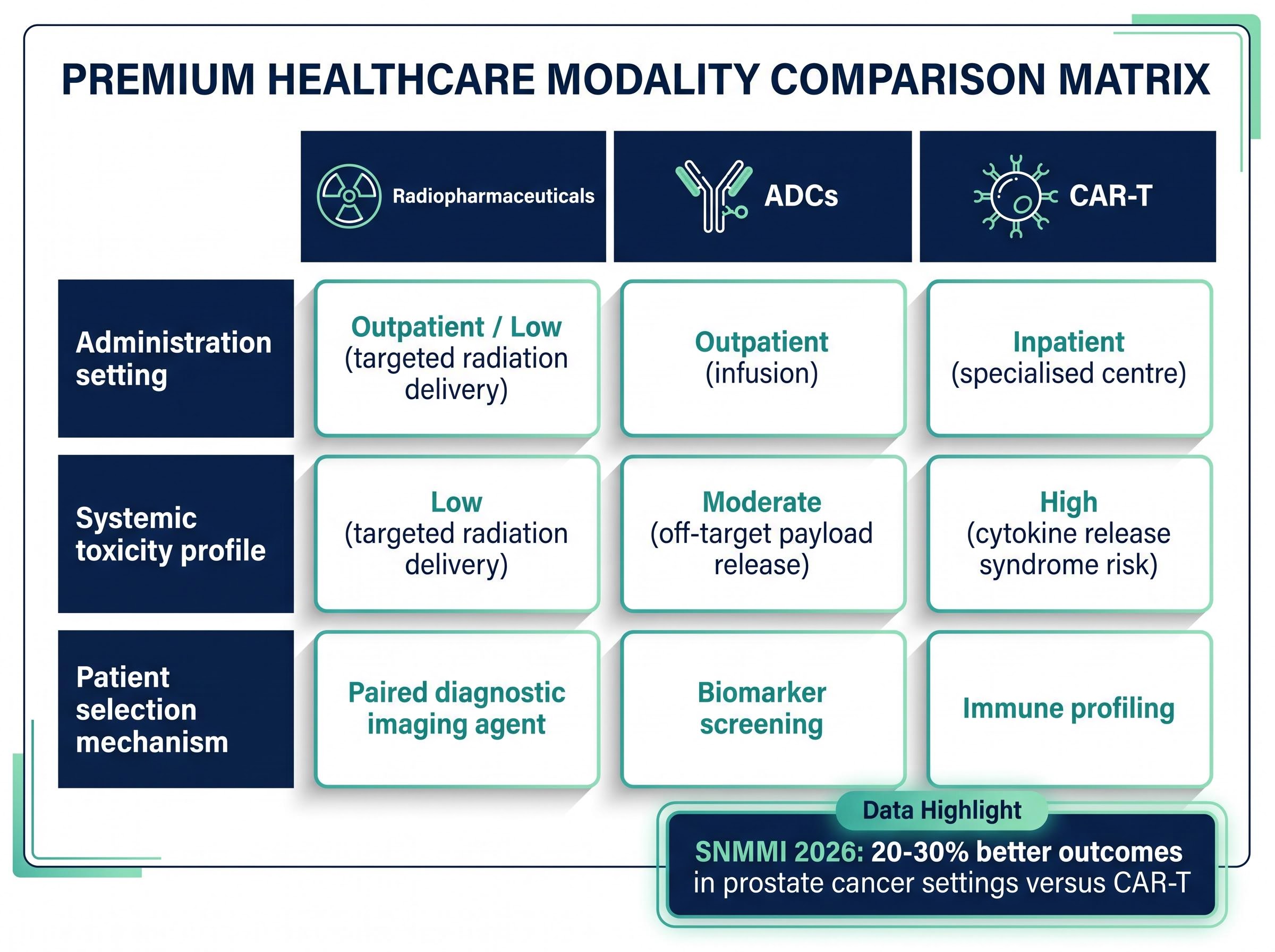

Radiopharmaceuticals compete with two primary modalities for metastatic cancer treatment: antibody-drug conjugates (ADCs) and CAR-T cell therapies. The clinical comparison is not about efficacy alone; it is about the properties that affect commercial deployment at scale.

| Modality | Administration setting | Systemic toxicity profile | Patient selection mechanism |

|---|---|---|---|

| Radiopharmaceuticals | Outpatient | Low (targeted radiation delivery) | Paired diagnostic imaging agent |

| ADCs | Outpatient (infusion) | Moderate (off-target payload release) | Biomarker screening |

| CAR-T | Inpatient (specialised centre) | High (cytokine release syndrome risk) | Immune profiling |

Outpatient administration is a structural advantage that extends beyond patient convenience. CAR-T therapies require inpatient infrastructure and are associated with significantly higher per-treatment economics, which limits both the number of eligible treatment centres and the breadth of patient access. Radiopharmaceuticals, by contrast, can be administered in standard nuclear medicine departments.

Outpatient administration depends on more than clinical protocol; it requires nuclear medicine infrastructure capable of handling radiopharmaceutical receipt, preparation, and same-day administration, a network that the US hospital system is still building out at scale.

Expert commentary from the SNMMI 2026 conference highlighted radiopharmaceuticals’ superior targeting for metastatic cancers relative to ADCs and lower systemic toxicity compared to conventional antibody therapies. Health economics data presented at the conference indicated 20-30% better outcomes in prostate cancer settings versus CAR-T, attributed to outpatient delivery and favourable tolerability profiles, though the direct study parameters should be confirmed before drawing definitive conclusions.

The targeted delivery mechanism reduces off-target exposure, which influences both patient tolerability and the breadth of eligible patient populations. A larger addressable patient pool, combined with a theranostic platform that compresses development timelines through built-in patient selection, creates the commercial durability that explains why large acquirers have been willing to pay strategic premiums.

The acquisition wave: what USD 6.5 billion in M&A tells investors about sector conviction

The consolidation started in late 2023 and accelerated through 2024 and into 2025. What matters is not just the capital deployed but the sequence: three of the world’s largest pharmaceutical companies moved within a twelve-month window, each targeting a different layer of the radiopharmaceutical value chain.

| Acquirer | Target | Deal value | Completion | Strategic rationale |

|---|---|---|---|---|

| Bristol-Myers Squibb | RayzeBio | USD 4.1B | February 2024 | Targeted radiotherapeutic pipeline |

| Eli Lilly | POINT Biopharma | USD 1.4B | 2024 | Next-generation radioligand therapy |

| Novartis | Mariana Oncology | USD 1B + up to USD 750M milestones | May 2024 | Pipeline extension beyond Pluvicto |

| Curium | Eczacibasi-Monrol | Not disclosed | March 2025 | Lu-177 capacity and PET footprint |

The transactions fall into three strategic categories:

- Pipeline assets: BMS and Eli Lilly acquired clinical-stage companies whose therapeutic candidates addressed unmet oncology targets with radioligand approaches.

- Platform extension: Novartis, already commercially established through Pluvicto, acquired Mariana Oncology to extend its radiopharmaceutical franchise into new tumour targets.

- Supply chain infrastructure: Curium’s acquisition of Eczacibasi-Monrol was not a pipeline play. It was a manufacturing and distribution play, securing Lu-177 production capacity and PET diagnostic infrastructure.

The fact that strategic capital flowed into manufacturing alongside clinical assets signals that sophisticated acquirers view the supply chain as a competitive bottleneck worth owning, not merely contracting.

The supply chain constraint most investors overlook

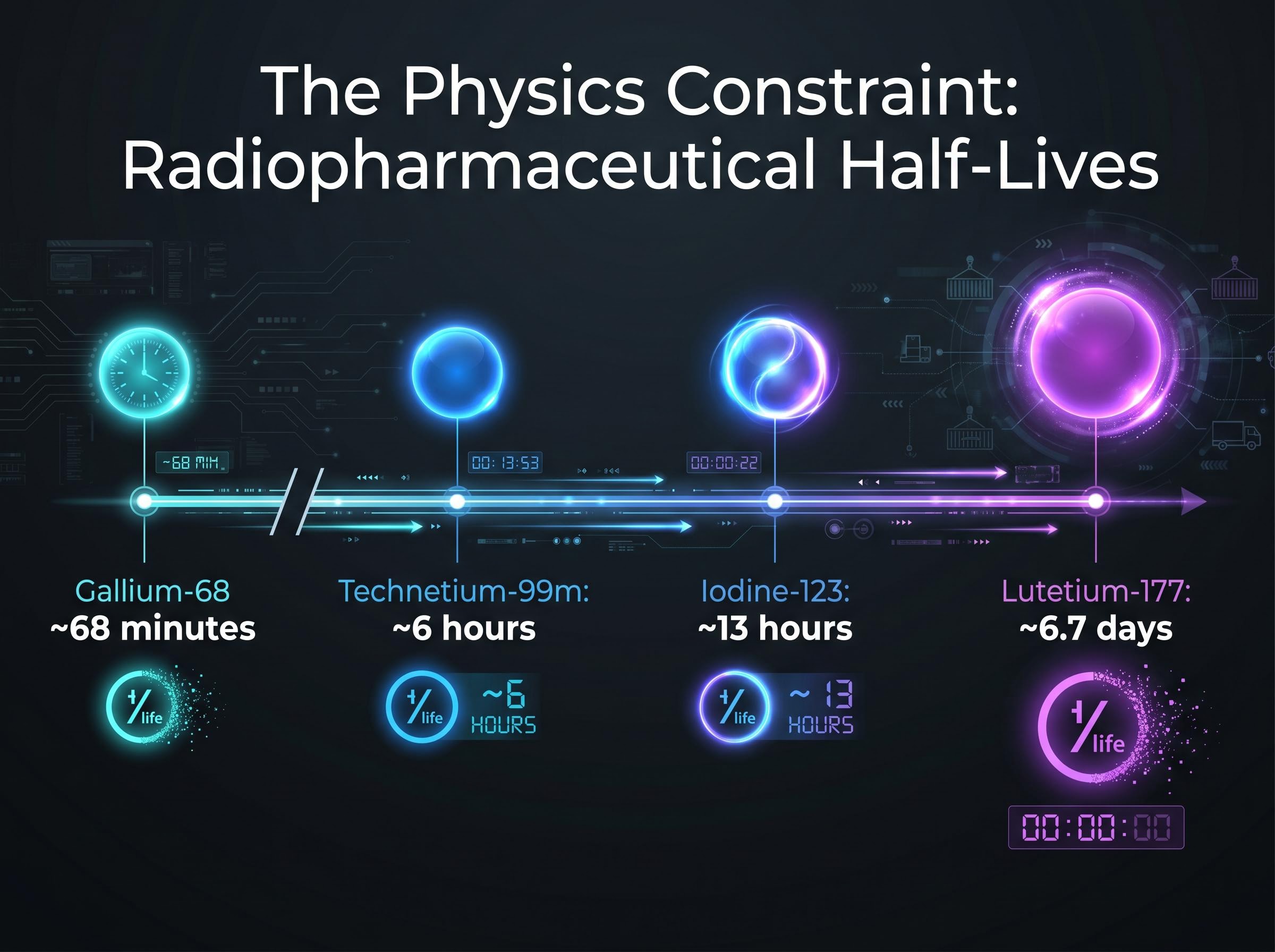

Radiopharmaceuticals cannot be stockpiled. They cannot be shipped through conventional pharmaceutical distribution networks. The isotopes that make them work are radioactive, and radioactivity decays on a fixed schedule that no logistics optimisation can override.

The half-lives tell the story:

- Gallium-68: Approximately 68 minutes. Must be produced and administered on the same day, at or near the clinical site.

- Technetium-99m: Approximately 6 hours. Regional distribution is possible; intercontinental shipping is not.

- Lutetium-177: Approximately 6.7 days. The most logistically flexible therapeutic isotope, but still requires specialised cold-chain transport and dose preparation within a tight window.

- Iodine-123: Used in SPECT diagnostics with a half-life of approximately 13 hours, constraining its distribution radius.

Copper-64’s 12.7-hour half-life occupies a distribution window sitting between gallium-68 and lutetium-177, and the strategic response to that window is visible in how Clarity Pharmaceuticals has constructed its copper-64 supply chain across four manufacturing partners, securing approximately 650,000 patient doses annually ahead of anticipated FDA approval.

This physics-driven constraint means that manufacturing facilities must be located near major clinical centres. A company with a promising molecule but no production infrastructure within reach of its target hospitals faces a bottleneck that clinical trial data alone cannot solve.

Why geography is a competitive advantage in nuclear medicine

Proximity to nuclear reactors (for Lu-177 production) and cyclotrons (for Gallium-68) determines which companies can reliably supply clinical-grade material to major hospital networks. Vertical integration into isotope production, or long-term supply contracts with reactor operators, functions as a strategic asset analogous to proprietary manufacturing in conventional biologics.

This is the lens through which the Curium/Eczacibasi-Monrol acquisition makes sense. Curium was not buying a drug candidate. It was buying geography: reactor access, established distribution routes, and the regulatory licences that take years to replicate.

Telix Pharmaceuticals as a case study in competing without Big Pharma’s balance sheet

Telix Pharmaceuticals is the most commercially advanced independent radiopharmaceutical company of Australian origin, operating in a sector otherwise dominated by US and European multinationals. Its trajectory illustrates a viable strategic path for companies building a theranostic platform without the balance sheet of a Novartis or an Eli Lilly.

The strategy is imaging-first. Telix’s approved commercial products, Illuccix and Gozellix (both PSMA-targeted PET imaging agents for prostate cancer), have generated a revenue base that funds the therapeutic pipeline without dilutive capital raises or partnership concessions. 2025 revenue reached USD 803.8 million, representing 56% year-over-year growth. Q1 2026 revenue came in at USD 230 million, an 11% rise on the prior quarter.

Telix’s full-year 2026 revenue guidance of USD 950 million to USD 970 million signals a commercial trajectory that positions the company to self-fund its therapeutic pipeline through cash generation rather than external financing.

Telix’s Regeneron partnership, which secured USD 40 million upfront with up to USD 2.1 billion in potential milestones, illustrates a further strategic dimension: treating manufacturing platform as a commercial asset that generates licensing revenue independently of the company’s proprietary pipeline, a model that adds a non-dilutive capital stream alongside product sales.

The company holds a dual listing on the ASX and Nasdaq, broadening investor access across capital markets.

Telix’s approved portfolio now spans three asset categories:

- Commercial imaging products: Illuccix and Gozellix (PSMA-targeted PET agents for prostate cancer).

- Companion diagnostic: Pixclara (TLX101-CDx), approved by the FDA in April 2026 for brain cancer imaging.

- Therapeutic pipeline: TLX591 (ProstACT), in Phase 3, with positive interim progression-free survival data presented at ASCO 2026.

From imaging to therapy: the Telix theranostic roadmap

Telix’s PSMA imaging franchise targets the same receptor that its therapeutic pipeline candidate TLX591 addresses. This directly mirrors the Novartis model where Illuccix (imaging) and Pluvicto (therapy) share the same biological target, PSMA, on prostate cancer cells.

Positive ProstACT Phase 3 interim data positions TLX591 for a potential regulatory submission, which could move Telix from a diagnostics-weighted revenue mix to a true theranostic commercial profile. That transition, if realised, would represent a shift from a company valued primarily on imaging volumes to one valued on the combined economics of diagnosis and treatment within a single platform.

The FDA label expansion for Pluvicto in early 2025 confirmed that regulators are willing to broaden approved indications as clinical evidence matures, a pattern that pipeline companies targeting the same PSMA receptor, including those building theranostic platforms around TLX591, are tracking closely as they design their own submission strategies.

What the sector’s trajectory means for investors approaching it in 2026

The radiopharmaceutical investment thesis rests on the convergence of four structural factors: clinical differentiation that is documented and durable rather than theoretical; theranostic platform economics that generate two revenue streams from a single biological insight; supply-chain barriers to entry that compound over time rather than eroding as generic competition emerges; and demonstrated Big Pharma acquisition appetite that has validated the thesis with disclosed capital.

Market forecasts reflect the breadth of credible growth scenarios. Future Market Insights projects the sector reaching USD 10.3 billion by 2036 at a 3.4% compound annual growth rate (CAGR), while InsightAce Analytic forecasts USD 22.88 billion by 2035 at a 13.4% CAGR. The spread reflects differences in market definition and modality coverage rather than fundamental disagreement about directional growth.

The FDA’s sustained regulatory engagement with radiopharmaceutical approvals across the 2024-2026 period provides an additional risk-reduction signal for pipeline assets approaching submission.

The PSMA receptor dominates current commercial activity, but the theranostic model is being tested against a broader target landscape; HER2-targeted radioligand therapy represents one of the more clinically significant expansions, with Radiopharm Theranostics reporting meaningful tumour uptake and no dose-limiting toxicities in its first-in-human HEAT trial evaluation of 177Lu-RAD202.

Investors evaluating any opportunity in this sector can apply a consistent set of questions derived from the structural dynamics this article has outlined:

- Does the company control or have contracted access to its isotope supply?

- Does it operate a paired diagnostic and therapeutic programme targeting the same receptor?

- What is its regulatory runway, and are its lead assets approaching submission milestones?

- Is its manufacturing infrastructure located within logistical reach of its target clinical centres?

- Does its revenue model fund pipeline development, or is it dependent on external capital?

Against the thesis, three risk dimensions require honest assessment: isotope supply reliability remains concentrated among a limited number of reactor operators; clinical trial failure rates in late-stage therapeutic assets carry binary outcomes; and the competitive pressure from Novartis’s established Pluvicto franchise in the PSMA-targeted space raises the bar for any new entrant.

Given that more than USD 6.5 billion in M&A has already been deployed, the pipeline of acquirable independent assets has narrowed. Remaining independents carry either higher acquisition premiums or higher standalone execution risk.

Targeted medicine’s next decade will be won in the supply chain as much as the lab

Radiopharmaceuticals’ clinical differentiation is real and documented across multiple modalities and tumour types. The Big Pharma acquisition wave has validated the investment thesis with disclosed capital at scale. And the structural supply-chain moat, rooted in isotope physics and geographic infrastructure, means competitive advantages compound over time rather than dissipating as the market matures.

The forecast spread, USD 10.3 billion to USD 22.88 billion by the mid-2030s, reflects definitional differences in how analysts scope the market rather than fundamental disagreement about growth direction. Both endpoints represent material expansion from today’s base.

The framework this article has built, covering clinical mechanism, theranostic economics, supply-chain position, and the acquisition landscape, is the lens through which any individual radiopharmaceutical opportunity should be evaluated. Investors who apply it consistently are better positioned to distinguish between companies with durable structural advantages and those whose clinical promise outpaces their ability to manufacture and deliver at scale.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Market forecasts are subject to revision, and past performance does not guarantee future results.