Betashares ERTH ETF: Macro Tailwind Meets Real Volatility Risk

4 hrs ago

Parsons Corporation released its first-quarter 2026 financial disclosure on Wednesday, 29 April 2026, arriving amid heightened scrutiny of United States defence contractors and escalating Middle East regional risks. The immediate data presented a striking contrast for market participants. The company reported a 4% drop in total quarterly sales, yet simultaneously achieved the highest adjusted profit margins in its corporate history.

Operational efficiency has become a key metric for investors evaluating government contractors. This detailed breakdown of the latest Parsons earnings report outlines how the firm engineered a profitability beat during a top-line revenue contraction. The company also secured a historic $9.3 billion backlog, a figure that signals sustained forward momentum.

The ensuing data unpacks the specific mechanisms behind the margin expansion. It also clarifies a classified contract anomaly that obscured underlying business growth, offering a clearer picture of the defence sector outlook.

The immediate financial reality for Parsons presents an analytical tension between contracting sales volumes and record-setting profitability. The company reported total first-quarter sales of $1.5 billion, representing a 4% annual drop. Top-line revenue misses often trigger immediate market sell-offs, yet the underlying margin expansion protected shareholder value.

Parsons delivered an adjusted earnings per share of $0.70, beating the Wall Street consensus expectation by a clear margin. The profitability metrics outpaced the volume contraction. Adjusted EBITDA reached $151 million, yielding a record 10.1% margin that widened by 50 basis points compared to the prior year.

Capital efficiency also improved significantly during the three-month period. According to estimates, management minimised operational cash utilisation to just $4 million, a marked improvement from the negative $12 million recorded in the first quarter of the prior year. Investors evaluating this print are seeing a demonstration of how cost control and margin expansion can shield corporate health during temporary volume dips.

| Metric | Q1 2026 Actual | Market Expectation / YoY Change |

|---|---|---|

| Adjusted EPS | $0.70 | According to estimates, beat by $0.10 (Est. $0.69) |

| Total Revenue | $1.5 billion | Down 4% |

| Adjusted EBITDA Margin | 10.1% | Up 50 basis points |

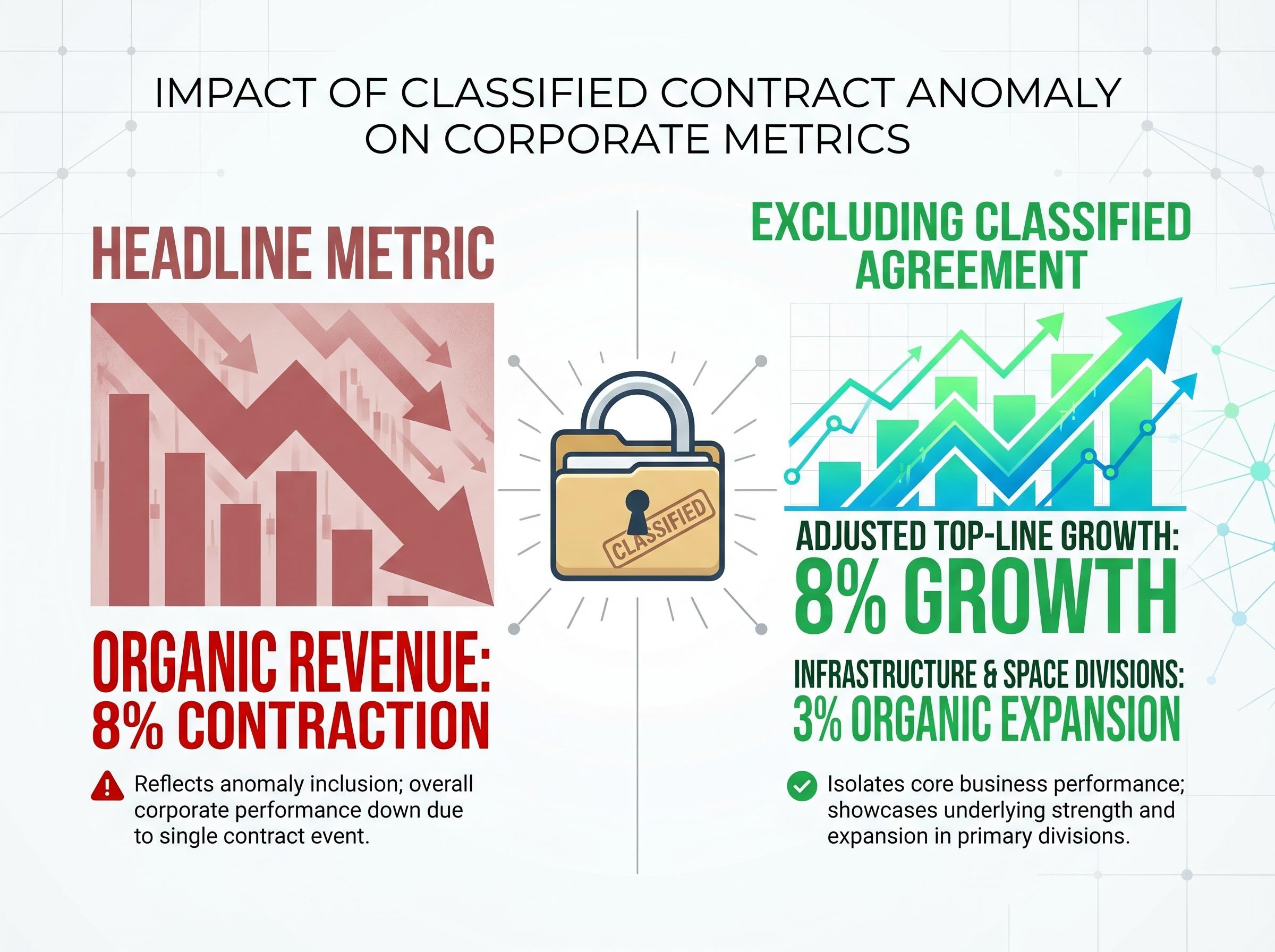

Defence financials frequently carry opaque variables due to confidential government projects. The headline numbers show that Parsons experienced an 8% organic revenue contraction, alongside net income falling 20% to $53 million. However, this top-line miss masks the underlying operational growth when the mechanics of government procurement are isolated.

A single fixed-price classified agreement heavily skewed the overall corporate organic growth metrics. Fixed-price defence contracts establish a set payment regardless of the contractor’s costs or the pacing of the work. When volume on a major fixed-price project lowers during a specific quarter, it drags down the aggregate revenue and operating income figures, even if the rest of the portfolio is expanding.

Beyond massive classified programs, the defense department is actively funding solutions for structural supply chain gaps, particularly where legacy components are no longer available from original equipment manufacturers.

Removing this specific confidential contract from the ledger clarifies the mathematical difference in performance. Without the classified agreement, Parsons actually generated an adjusted 8% top-line growth and, according to estimates, a 3% organic expansion across its critical infrastructure and space divisions.

CEO Commentary “Our first quarter results highlighted the resilience of our business and our team’s high level of execution, as we delivered our highest adjusted EBITDA margin ever, reached record levels for both total and funded backlog, achieved a book-to-bill ratio of 1.4x in both segments, and generated record first quarter cash flow.” – Carey Smith, Chief Executive Officer.

Smith further noted that revenue performance aligned with internal expectations, with strategic acquisitions continuing to drive long-term value. By unpacking this specific anomaly, the true organic expansion rate becomes visible to market participants.

Attention shifts from past performance to future capital security. Government contractors rely on their order pipelines as a strategic shield against immediate market volatility. Parsons secured $2.1 billion in fresh orders during the three-month period, demonstrating an ability to lock in future revenue streams.

Once a vendor qualifies for a military platform, they often develop incredibly sticky customer relationships that result in reliable follow-on orders across multiple financial years.

This order influx generated a 1.4x book-to-bill ratio across both operational divisions. The book-to-bill metric is a standard health indicator in government contracting, measuring the ratio of new orders received to completed billed work. A ratio above 1.0x confirms that demand is outstripping current fulfillment capacity, providing guaranteed long-term revenue visibility.

This forward-looking security is quantified in the company’s unfulfilled order pipeline. The funded backlog now represents the highest volume of financed future work since the company’s 2019 initial public offering.

Fresh orders acquired during the quarter: $2.1 billion Book-to-bill ratio across all divisions: 1.4x Cumulative pending orders: $9.3 billion Financed segment of unfulfilled orders: $6.6 billion

This massive funded backlog reassures investors that the company holds a guaranteed pipeline of future capital, offsetting concerns regarding current quarter volume contractions.

Markets rarely digest complex earnings reports with uniform sentiment. Retail trading optimism frequently clashes with institutional caution, and Parsons experienced this exact divergence early on Wednesday. The immediate pre-market equity response leaned heavily positive as traders reacted to the margin expansion and EPS beat.

Prior to the opening bell, Parsons stock traded at $53.45, reflecting a jump of approximately 3.1% from the previous close. Pre-market trading volume was notably heavy, with approximately 1.3 million shares changing hands before regular hours began. This early momentum suggested the broader market was willing to reward the profitability metrics while ignoring the top-line contraction.

The morning rally contrasted sharply with a cautious pre-earnings downgrade issued by KeyBanc analysts. The financial institution downgraded Parsons to a “Sector Weight” rating just prior to the earnings release. This institutional caution offers a counterweight to the retail buying pressure.

Analysts cited lingering concerns regarding escalating Middle East risks and a limited growth outlook for the upcoming periods. Presenting both the pre-market rally and the institutional downgrade gives a realistic view of the varying market sentiments surrounding the defence contractor.

Investors exploring how geopolitical conflicts are directly translating to contractor order books will find our detailed coverage of Middle East defence procurement outlines how regional tensions are accelerating counter-drone and weapon system demand across the sector.

Management chose to sustain its forward-looking financial targets for the remainder of the fiscal year, holding steady despite the first-quarter top-line miss. According to reports, Parsons maintained its full-year top-line projections, forecasting a range from $6.5 billion to $6.8 billion. This guidance provides a definitive benchmark for evaluating corporate performance in the upcoming quarters.

According to estimates, the $6.65 billion median of this corporate sales forecast falls just under the $6.665 billion broader market expectation. However, the company’s record backlog positions it strongly to navigate these forecasted revenue ranges. The secured financing acts as a buffer against potential geopolitical disruptions.

Meeting these elevated sales forecasts will require defense firms to secure ongoing development contracts that inform future US Army procurement programmes, ensuring a steady transition from prototype work to full-rate production.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Parsons achieved record 10.1% adjusted EBITDA margins through strong operational efficiency and cost control, which shielded corporate health even during a 4% revenue contraction.

A single fixed-price classified agreement heavily skewed Parsons' reported 8% organic revenue contraction; excluding it, the company achieved 8% adjusted top-line growth.

The $9.3 billion backlog, including $6.6 billion funded, represents the company's highest since its 2019 IPO and signals a strong, guaranteed pipeline of future revenue streams.

Pre-market trading showed a 3.1% jump in Parsons stock due to strong profitability, though KeyBanc analysts issued a pre-earnings downgrade to "Sector Weight."

Yes, management maintained its full-year revenue projections of $6.5 billion to $6.8 billion, with the record backlog supporting these targets despite the Q1 top-line miss.