Why the US-Iran Deal Won’t Cut Oil Prices Overnight

1 hr ago

Macquarie Group shares hit a fresh all-time intraday high of A$250.54 on the morning of 17 June 2026, capping a 23% year-to-date run that has left every other ASX 200 bank stock behind. The record comes without a price-sensitive announcement to explain it, which raises a sharper question for investors: is this a fundamentals-driven re-rating of a genuinely superior franchise, or is momentum now running ahead of what the earnings can justify?

What follows unpacks the forces behind the Macquarie Group share price rally, where the broker consensus sits relative to today’s print, and what the risk-reward looks like for investors holding or considering MQG shares right now.

The path to A$250.54 was not a straight line. Macquarie pulled back alongside the broader ASX bank cohort during late February and March, recovered sharply through April, then pushed to a previous all-time high of A$249.49 in May. The 17 June intraday print cleared that mark by just over a dollar.

Key milestones in the 2026 share price sequence:

No price-sensitive disclosures have been released since Macquarie’s FY26 results. The continued buying appears driven by positioning and growth expectations rather than fresh news flow, which is itself informative: the market is bidding the stock higher on conviction, not catalysts.

The 23% year-to-date gain places Macquarie well clear of Commonwealth Bank, Westpac, NAB and ANZ, all of which have underperformed in 2026. This is not a broad bank sector rally lifting all boats. It looks more like a deliberate relative trade, with institutional capital rotating toward a globally diversified earnings profile that the big four simply cannot offer.

The contrast between MQG’s year-to-date outperformance and the deliberate underperformance of CBA, Westpac, NAB and ANZ is sharpened by the fact that professional investors have built record short positions against the big four, a positioning dynamic that reinforces the view that the relative trade between Macquarie and domestic mortgage lenders is being expressed with institutional conviction rather than passive sector rotation.

The 12-month gain of approximately 18% reinforces the same pattern: sustained outperformance over multiple timeframes, not a single-week spike.

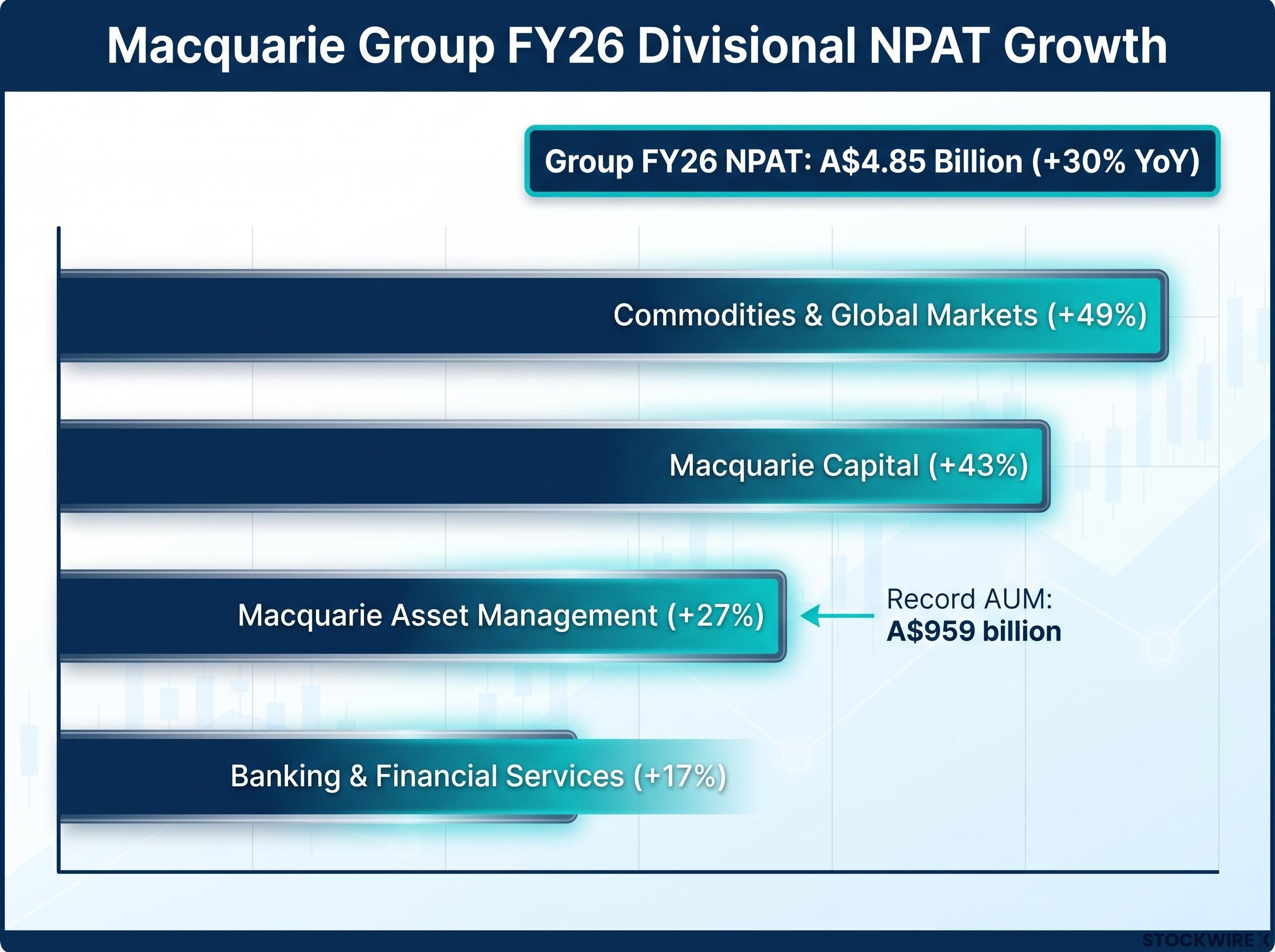

Macquarie reported FY26 net profit after tax of approximately A$4.85 billion, up roughly 30% year-on-year, with return on equity of 14.0%. The headline figure is strong. What sits underneath it is stronger.

All four divisions delivered double-digit profit growth:

| Division | FY26 NPAT Growth | Primary Driver |

|---|---|---|

| Commodities & Global Markets | +49% | North American power, gas and emissions trading; OnStream sale |

| Macquarie Capital | +43% | Advisory and deal activity; OnStream sale contribution |

| Macquarie Asset Management | +27% | Record AUM of A$959 billion; infrastructure revaluations |

| Banking & Financial Services | +17% | Loan book growth and deposit franchise |

This breadth matters. A result propped up by a single division, particularly one exposed to volatile commodity markets, would warrant scepticism about durability. Four divisions all contributing double-digit growth is a qualitatively different signal about earnings quality.

One caveat investors should factor in: the OnStream sale contributed to both Commodities & Global Markets and Macquarie Capital earnings. That gain is non-recurring. Forward projections need to account for its absence. The February 2026 trading update had already signalled the earnings inflection, triggering an intraday share price jump of up to 4% at the time, but the full-year result still exceeded the upgraded forecasts that followed.

Comparing Macquarie to CBA or Westpac on a price-to-earnings basis invites a category error. The businesses are structurally different, and the market prices them accordingly.

Approximately two-thirds of Macquarie’s group earnings come from international operations, a ratio that inverts the domestic mortgage-heavy orientation of Australia’s big four banks.

That international tilt is not diversification for its own sake. It provides exposure to structural growth themes that domestic banking simply does not offer:

Management flagged North American energy markets as a source of ongoing strength, and the Commodities & Global Markets result bears that out.

BloombergNEF analysis of North American gas markets highlights how weather-driven demand spikes from phenomena such as the polar vortex and La Nina have sustained elevated price volatility across the 2025-2026 period, providing the trading environment in which Macquarie’s Commodities and Global Markets division recorded its 49% profit increase.

Capital discipline reinforces the growth narrative rather than contradicting it. Macquarie ended FY26 with a CET1 ratio (a measure of a bank’s core capital relative to its risk-weighted assets) of 12.8%, well above regulatory minimums. For investors seeking combined financials, infrastructure and energy transition exposure in a single ASX-listed vehicle, Macquarie occupies a position that no peer replicates.

APRA’s APS 110 Capital Adequacy standard sets the minimum CET1 ratio for Australian authorised deposit-taking institutions at 4.5%, which means Macquarie’s reported 12.8% sits nearly three times the regulatory floor and signals substantial capacity for both growth investment and continued shareholder returns.

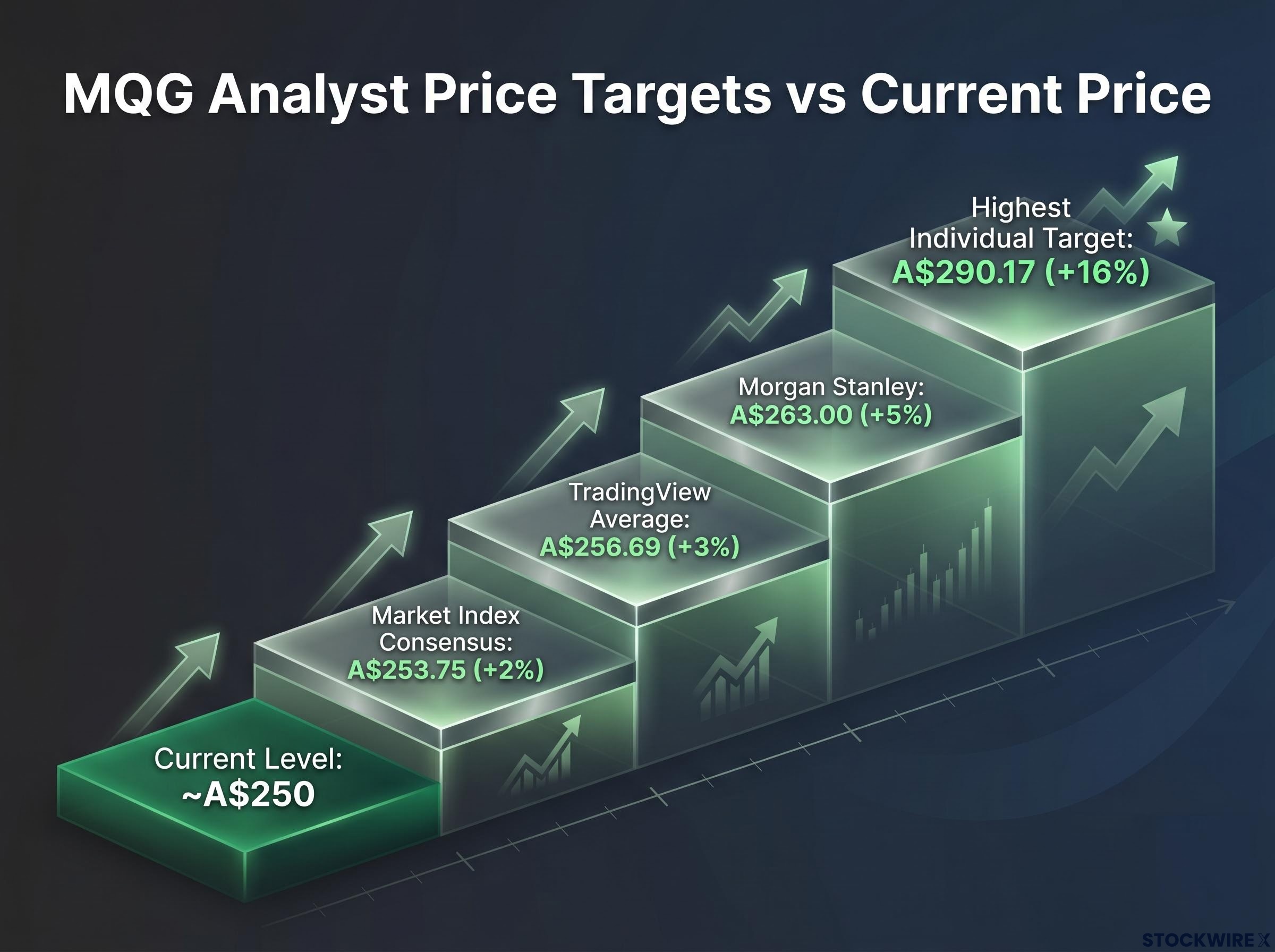

With the share price at record levels, the natural question is whether brokers see further upside. The answer is yes, but not by much on average, and the spread between bulls and bears is wide enough to warrant attention.

| Source | Price Target (A$) | Implied Move from ~A$250 |

|---|---|---|

| Market Index consensus | $253.75 | Approximately +2% |

| TradingView aggregated average | $256.69 | Approximately +3% |

| Morgan Stanley (buy rating) | $263.00 | Approximately +5% |

| Highest individual analyst target | $290.17 | Approximately +16% |

Morgan Stanley holds a buy rating with a price target of A$263, placing it among the more constructive voices on the stock and implying mid-single-digit upside from current levels.

Nine of 15 analysts tracked via TradingView hold either a buy or strong buy recommendation. Sentiment is constructive, but the consensus average clusters only 2-3% above the current price. Different data feeds produce different averages, reflecting which analysts are included and when targets were last updated. That modest gap tells investors something: at these levels, near-term upside requires either a material earnings beat or further multiple expansion.

On valuation, Macquarie trades at approximately 19x trailing FY26 earnings, based on earnings per share of roughly A$12.77. The forward price-to-book ratio sits at approximately 2.5x (this figure is approximate and sourced from aggregated data). Neither metric screams overvaluation for a franchise of this quality, but neither leaves a wide margin of safety.

The bull case rests on franchise quality and secular growth:

The bear case centres on valuation and cyclicality:

One dimension of downside risk that the headline valuation multiples do not capture is Macquarie’s debt-to-equity sensitivity: a debt-to-equity ratio above 250% means that movements in interest rates and tightening credit conditions transmit materially to earnings and equity value, amplifying the downside at any given entry price.

For existing shareholders, the record validates the thesis. The focus shifts from questioning the franchise to managing position size and cyclical risk. The FY26 final dividend of A$4.20 per share, fully franked and payable in early July 2026, provides a near-term income consideration.

For prospective buyers, the calculus is different. The easy re-rating has occurred. Average consensus targets sit only modestly above today’s price. The long-term case remains intact if Macquarie continues compounding earnings in infrastructure, asset management and global markets, but entry price matters more at this stage of the cycle than it did twelve months ago.

Macquarie’s all-time high is underpinned by genuine earnings quality, with all four divisions contributing to a 30% profit increase, a record asset base, and structural growth exposures that no ASX peer replicates. This is not a speculative spike.

At approximately 19x trailing earnings and with consensus targets only 2-3% above the current price, near-term risk-reward is more balanced than it was entering 2026. The investment case from here depends less on multiple expansion and more on Macquarie’s ability to sustain above-consensus earnings growth through the infrastructure, energy transition and commodities cycles that have driven the re-rating so far.

For investors who want to move beyond the consensus price target range and build their own view of MQG’s risk-adjusted return, our comprehensive walkthrough of ASX bank stock stress-testing covers discount rate sensitivity, credit cycle scenario analysis, and a qualitative due diligence checklist that applies to Macquarie’s infrastructure and commodities earnings as readily as it does to traditional lenders.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements are subject to market conditions and various risk factors.

Macquarie shares reached A$250.54 on 17 June 2026 without a price-sensitive announcement, suggesting the move was driven by institutional positioning and conviction in the company's globally diversified earnings profile rather than a specific news catalyst.

Macquarie reported FY26 net profit after tax of approximately A$4.85 billion, up roughly 30% year-on-year, with all four divisions delivering double-digit profit growth and return on equity of 14.0%.

Consensus targets range from approximately A$253.75 (Market Index) to A$256.69 (TradingView aggregated average), implying only 2-3% upside from the A$250 level, with Morgan Stanley holding a buy rating and a A$263 target.

Approximately two-thirds of Macquarie's earnings come from international operations, giving it exposure to global infrastructure investment, energy transition financing, and North American commodities trading that domestic mortgage-focused banks like CBA and Westpac cannot offer.

The main risks include a valuation of approximately 19x trailing earnings that leaves limited margin for disappointment, the non-recurring contribution from the OnStream asset sale in FY26, and a debt-to-equity ratio above 250% that amplifies sensitivity to interest rate movements and tighter credit conditions.