JB Hi-Fi’s share price sat nearly 40% below its 52-week high as of May 2026, yet the same company posted $10.55 billion in sales and grew net profit to $462.4 million in FY25. That gap between what the market is paying and what the business is producing is the kind of tension that rewards closer inspection.

Australian discretionary retailers have absorbed prolonged headwinds: cost-of-living pressure, elevated interest rates, and a post-pandemic demand hangover in consumer electronics. JB Hi-Fi has not escaped that sentiment. Yet its FY25 result delivered 10.0% revenue growth and 5.4% net profit after tax (NPAT) growth, a combination that sits uncomfortably against a share price near multi-year lows. For investors searching the ASX for quality businesses trading at depressed levels, the question is genuine: does the discount reflect a mispricing or a warning?

What follows is a structured examination of the financial metrics that matter for a cost-leadership retailer, the operating reality behind the numbers, and the specific assumptions an investor would need to hold to act in either direction.

What a 40% pullback actually signals for a retailer like JB Hi-Fi

A 39.9% decline from a 52-week high is a number that demands investigation, not a conclusion that invites action. The mid-$40s share price range referenced in the Australian Financial Review (22 May 2025) and the Sydney Morning Herald (1 May 2025, “just under $46”) places JB Hi-Fi well below levels the market was willing to pay within the preceding twelve months. The question is why.

Three broad categories of explanation apply to any large price gap in a consumer-facing stock:

- Macro and sentiment driven: Interest rate expectations, consumer confidence data, and broad risk-off rotations away from discretionary sectors

- Sector level: Weak category spending across electronics and household goods, validated by ABS and RBA data, dragging valuations for the entire peer group

- Company specific: Deteriorating competitive position, margin compression, or structural earnings decline unique to the business

Each demands different evidence and leads to a different investment conclusion.

“Spending on discretionary goods, particularly household furnishings, electronics and recreational goods, remains weak as households adjust to higher mortgage and rental costs.” — Reserve Bank of Australia, Statement on Monetary Policy, February 2025

The RBA’s assessment confirms the macro headwind is real. ABS Retail Trade data through 2024-25 showed household goods retailing flat to slightly negative in real terms. The environment has been genuinely difficult. Whether the price gap is an overreaction to that environment, or a correct reading of structural deterioration, requires examining the specific business behind the ticker.

When big ASX news breaks, our subscribers know first

The business JB Hi-Fi actually runs, and why the model matters

JB Hi-Fi operates three segments: JB Hi-Fi Australia, JB Hi-Fi New Zealand, and The Good Guys. Founded in 1974, the company grew into one of Australia’s largest consumer electronics and home entertainment retailers. The acquisition of The Good Guys in 2016 extended the model into whitegoods and home appliances, and the years since have involved deeper integration of buying, logistics, and back-office functions to extract scale efficiencies.

The operating model centres on cost leadership. Management has consistently emphasised “everyday low prices” and “low cost of doing business” as core strategic pillars across FY24 and 1H FY25 presentations. In practice, this means high inventory turnover, disciplined store-level cost control, and pricing power derived from scale rather than brand premium. The business wins by being cheaper to run than competitors, then passing part of that cost advantage to consumers as lower prices.

That distinction matters because cost-leadership retailers should not be evaluated with the same lens applied to mature, yield-focused blue chips.

Choosing the right metrics for the right business model

For a growth-oriented cost leader, the metrics that carry the most weight are revenue growth, profit growth, and return on equity (ROE) tracked over several years. Dividend yield and debt-to-equity ratios, while relevant for income-focused holdings, are secondary indicators for a business whose value proposition rests on reinvesting operational efficiency into market share.

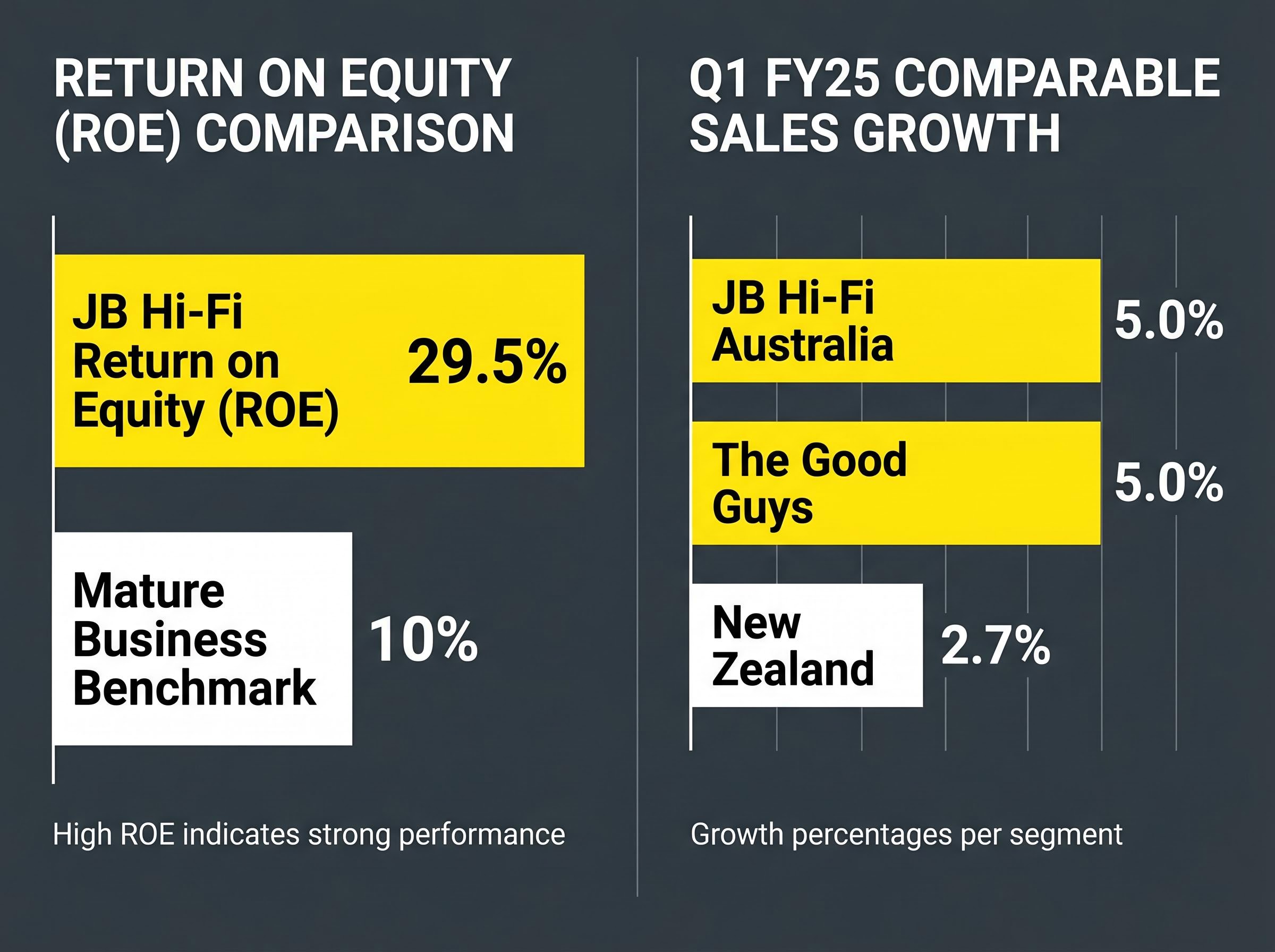

JB Hi-Fi’s most recently reported ROE stood at 29.5%. The general benchmark for a mature business is typically around 10%. A figure nearly three times that benchmark demands attention, even during a cyclical downturn. It signals a business generating outsized returns on shareholder capital. Whether that return is defensible through the cycle, however, requires examining the earnings trajectory across multiple years, not a single snapshot.

What the numbers actually show across FY23, FY24, and FY25

The three-year arc tells a more complete story than any single result.

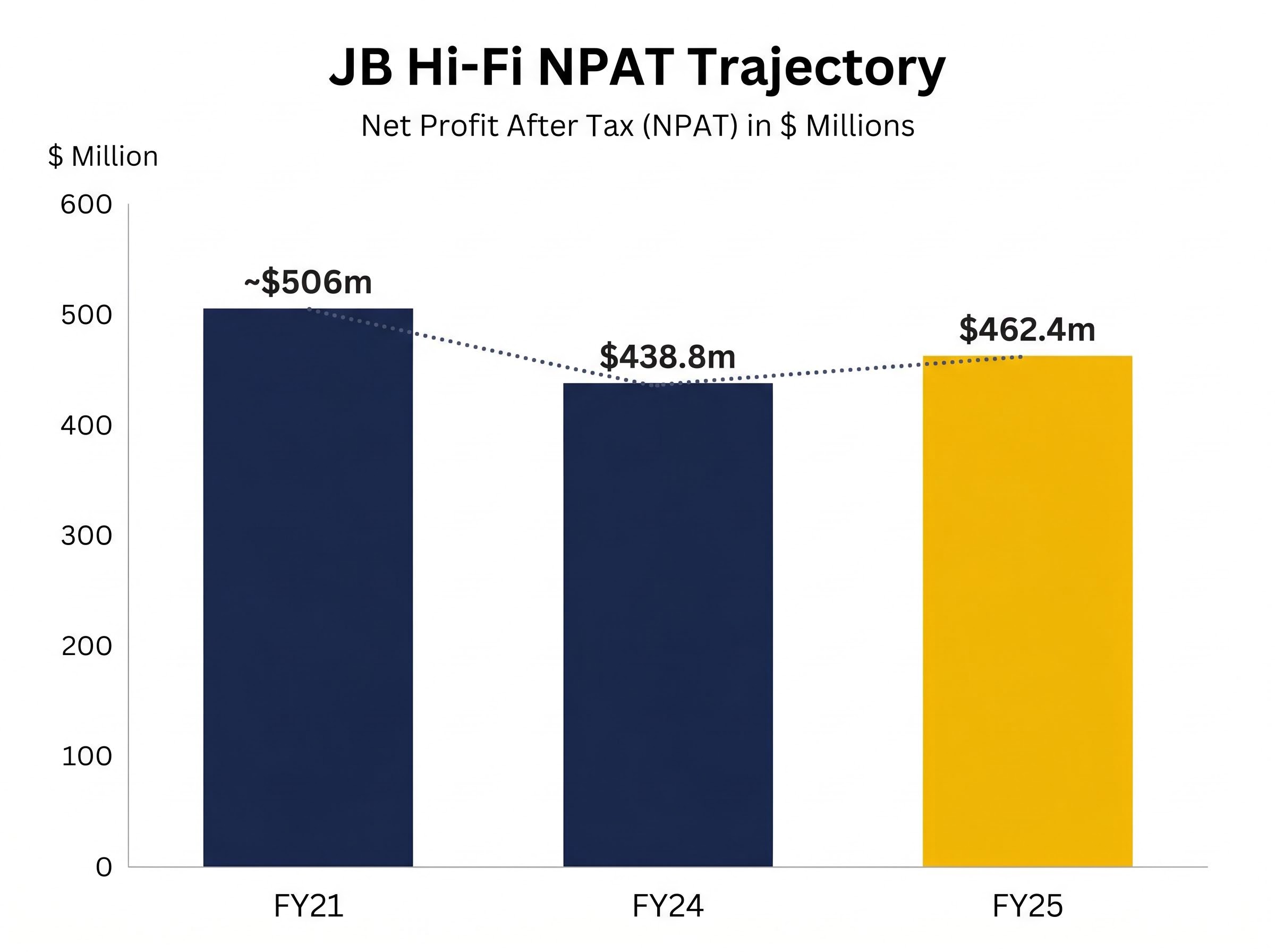

$10,554.8 million in sales, NPAT of $462.4 million, both growing. — JB Hi-Fi FY25 Full Year Results, ASX announcement, 11 August 2025

In FY24, JB Hi-Fi reported group revenue of $9,592.4 million and NPAT of $438.8 million, according to its ASX announcement on 12 August 2024. That result reflected a multi-year moderation from peak pandemic-era earnings, with net profit declining from approximately $506 million (FY21 reference point; this figure has not been independently confirmed) to $438.8 million over the three years to FY24. Average annual revenue growth over that period was approximately 2.5%.

Then FY25 arrived. Total sales reached $10,554.8 million, up 10.0% on FY24. EBIT grew 7.3%. NPAT rose to $462.4 million, a 5.4% increase, with earnings per share also up 5.4%. The Q1 FY25 trading update (31 October 2024) had already signalled the shift: JB Hi-Fi Australia comparable sales grew 5.0%, The Good Guys comparable sales grew 5.0%, and New Zealand posted 2.7% comparable growth.

| Financial Year | Revenue | NPAT |

|---|---|---|

| FY24 | $9,592.4M | $438.8M |

| FY25 | $10,554.8M | $462.4M |

The pattern is not a collapse followed by a dead-cat bounce. It is a demand cycle navigated by a structurally sound business: a peak, a trough, and a recovery. FY25’s result was meaningfully stronger than the cautious tone embedded in mid-2025 broker commentary, which is a distinction that matters for valuation.

The competitive and cost pressures testing the model’s durability

Appreciation of the earnings recovery needs to be weighed against the forces working to erode it. Two competitive threats stand out, each attacking a different dimension of the cost-leadership model:

- Harvey Norman has intensified promotional activity, launching aggressive discount campaigns across consumer electronics and appliances. Its half-year results to 31 December 2024 (ASX announcement, 26 February 2025) confirmed margins under pressure from discounting. The Australian Financial Review (5 March 2025) characterised the dynamic as a “discount war.” This compresses the price differentials that underpin JB Hi-Fi’s positioning.

- Amazon Australia has expanded its branded electronics range and increased Prime-style promotions, according to The Australian (3 December 2024). The AFR (7 May 2025) reported that electronics retailing continues to move further online as consumers chase bargains, forcing bricks-and-mortar retailers to maintain sharp online pricing while absorbing delivery and logistics investment costs.

IBISWorld’s March 2025 industry report described consumer electronics sales as “subdued,” with volume declines moderated only by promotional discounting.

Cost pressures that do not reverse when consumer sentiment improves

Wage inflation and store occupancy costs are structural headwinds that persist regardless of demand cycles. JB Hi-Fi’s 1H FY25 results (10 February 2025) cited higher wage costs and store occupancy expenses as ongoing pressures, partially offset by productivity initiatives. The RBA’s February 2025 statement reinforced the backdrop of solid wage growth and elevated rental costs, both directly relevant for labour-intensive, store-based retailers.

Investment in e-commerce platforms and data analytics adds to the cost base before it delivers margin benefit. That creates a short-term drag the market may be overweighting in its current pricing. The FY25 full-year result demonstrated the model withstood these pressures in the near term, but the question of multi-year durability remains open.

Where broker consensus sits and what the valuation debate hinges on

Broker targets from early to mid-2025 clustered around neutral-to-hold ratings with price targets in the mid-$40s. The dominant characterisation was fair value on current earnings with limited near-term upside.

| Broker | Rating | Price Target | Key Assumption |

|---|---|---|---|

| Macquarie | Neutral | $47.50 | Fairly valued on mid-cycle earnings |

| Morgan Stanley | Equal-weight | $48.00 | Resilient but fully priced |

| UBS | Sell | $42.00 | Expensive relative to peers on P/E |

| Ord Minnett | Hold | $45.00 | Worst of slowdown may have passed |

All four targets predate the FY25 full-year result (11 August 2025). Subsequent analyst revisions are not captured in the available press references.

ROE: 29.5%, nearly three times the 10% benchmark typically applied to mature businesses. A company sustaining that level of return on shareholder equity through a cyclical downturn complicates any “fairly valued” assessment.

The assumption that separates the bull and bear cases is specific: whether the FY25 recovery establishes a new earnings baseline or represents a one-year bounce within an ongoing structural pressure environment. UBS, rating the stock a Sell at $42.00, weighted the latter view. Ord Minnett, upgrading from Lighten to Hold, leaned toward the former. The ROE figure sits at the centre of that debate; a business generating 29.5% returns on equity for a sustained period typically commands a valuation premium, but only if the return is defensible through the full cycle.

The next major ASX story will hit our subscribers first

A 40% discount demands a 40% reason: what investors should weigh before acting

The analytical arc traced through this article surfaces a genuine tension. On one side: a 29.5% ROE, a successful FY25 earnings recovery to $462.4 million in NPAT, and a cost-leadership model that has proven durable through a prolonged demand downcycle. On the other: weak discretionary macro conditions validated by the RBA and ABS, intensifying competition from Amazon Australia and Harvey Norman, and a share price that brokers characterised as fairly valued before the stronger FY25 result was known.

The forward question hinges on specific assumptions:

- The bull case requires: FY25 establishing a new earnings floor rather than a cyclical peak; structural cost pressures (wages, rent, digital investment) proving manageable within the existing margin structure; and the market re-rating the stock to reflect a quality business priced at a discount

- The bear case requires: Amazon’s long-term pricing power permanently compressing industry margins; wage and occupancy inflation continuing to erode operating efficiency faster than productivity gains offset them; and the FY25 result proving to be a one-year bounce rather than sustainable growth

From approximately $506 million (FY21 reference) to $438.8 million (FY24 trough) to $462.4 million (FY25 recovery): the earnings trajectory describes a cycle, not a decline.

At the Macquarie Australia Conference (7 May 2025), management characterised Q4 FY25 early trading as “broadly consistent” with 1H FY25 trends. The correct evaluative lens remains multi-year revenue growth, profit growth, and ROE trend, not any single quarter’s trading update or a static price-to-earnings multiple.

The data has a case to make, but the macro still holds the gavel

JB Hi-Fi’s fundamentals are stronger than a 40% price gap from highs implies. That gap is not, however, simply a pricing error waiting to be corrected. It reflects real macro headwinds, real competitive intensification, and real uncertainty about whether FY25’s recovery marks a turning point or a temporary respite.

The practical question for Australian retail investors is not “is this cheap?” but whether the quality of this business justifies ownership at this price through the next full cycle. Updated broker notes following the FY25 result, ABS retail trade data releases through FY26, and any shifts in the RBA’s rate trajectory represent the most material inputs for revisiting the thesis.

Rather than reacting to weekly share price movements, investors may find more value in monitoring the metrics that define this business: revenue growth trend, NPAT trajectory, and ROE maintenance, assessed on an annual results basis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.