How $4B in Fuel Costs Erased American Airlines’ Record Q1

18 mins ago

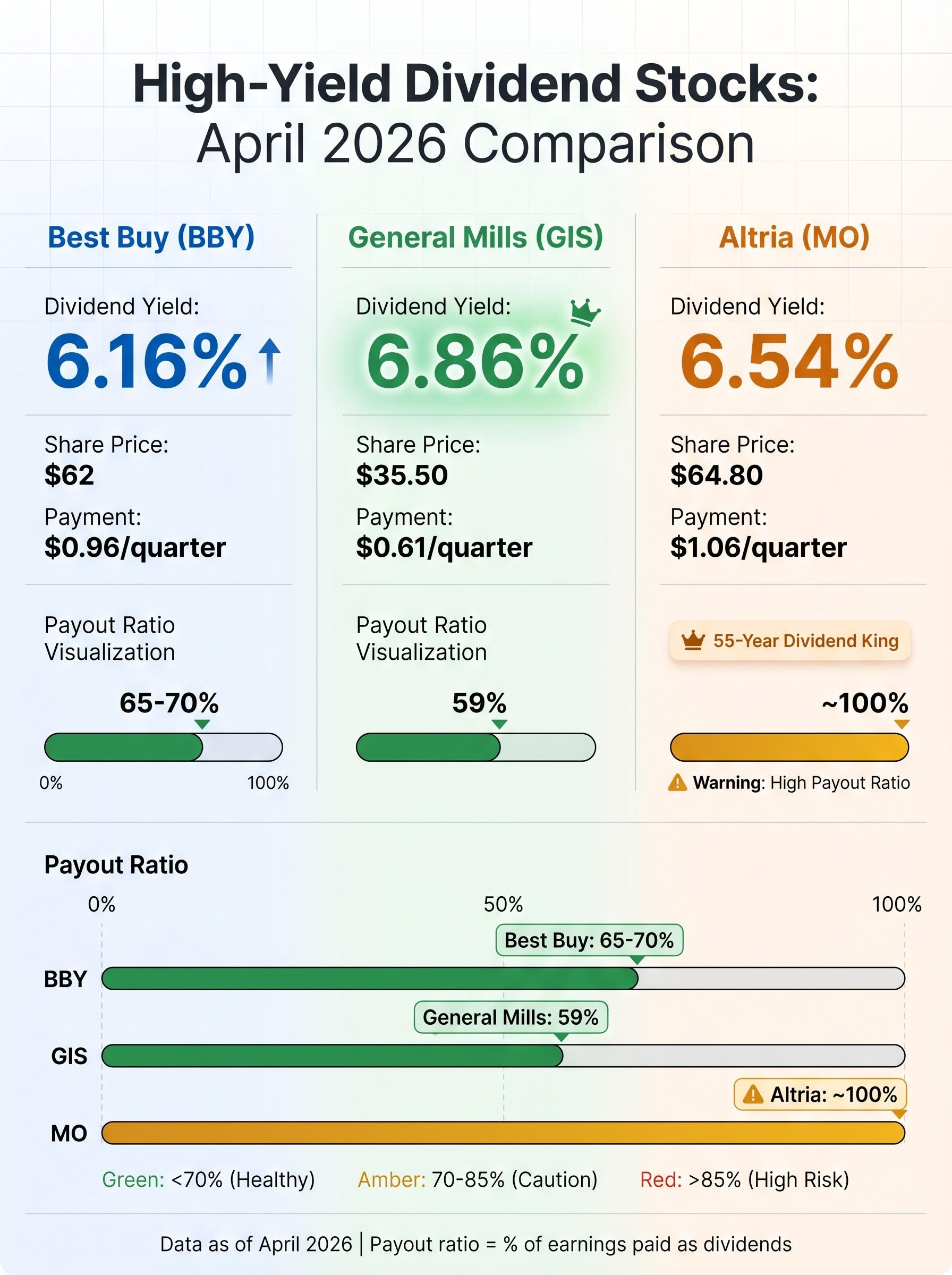

Three U.S. dividend stocks now offer yields above 6% with analyst-backed sustainability credentials, outpacing the typical consumer staples sector average of under 2% by a factor of three or more. Best Buy delivers 6.16%, General Mills 6.86%, and Altria 6.54%, each supported by payout ratios that suggest ongoing dividend capacity rather than near-term risk of cuts.

In April 2026, with the Federal Reserve signaling potential rate cuts totaling 75 basis points through the year, income-focused investors face a pivotal allocation question. High-yield dividend stocks present a compelling alternative to fixed income, but separating sustainable payers from dividend traps requires systematic evaluation. The anticipated lower-rate environment could enhance the relative appeal of these yields, yet sustainability depends on payout ratio discipline and sector-specific resilience.

This analysis examines the current high-yield landscape, breaks down sector dynamics shaping dividend durability, assesses risk profiles from conservative to elevated, and provides a framework for evaluating whether these income vehicles belong in your portfolio.

Best Buy closed near $62 in mid-April 2026, delivering a forward yield of 6.16% with quarterly payments of $0.96 per share. The most recent distribution landed on 14 April, reflecting a 1% increase from prior levels and supporting annual payouts totaling approximately $801 million in fiscal 2026. The payout ratio sits in the 65-70% range, providing cushion for both dividend continuity and share repurchases.

General Mills trades around $35.50, offering 6.86% with quarterly payments of $0.61 per share. The ex-date fell on 10 April 2026, with payment scheduled for 1 May. The company’s payout ratio runs at approximately 59% of earnings, well above the consumer staples sector average yield of roughly 1.8-2% but sustainable given the stable food production base and strong brand portfolio.

Altria, with shares near $64.80, provides 6.54% backed by its 55-year Dividend King status. Quarterly payments of $1.06 per share were declared on 26 February 2026, payable 30 April. The payout ratio has recently approached 100% of earnings, though management targets 80% of adjusted earnings and maintains a commitment to mid-single-digit annual dividend growth through 2028.

Altria has delivered dividend increases for 55 consecutive years, maintaining its Dividend King status despite sector headwinds and elevated payout ratios.

These three stocks contrast sharply with ultra-high yield securities appearing in screeners at 40-50% yields. Examples include entries with last payments in late March 2026 but lacking clear corporate identities, sustainability data, or established dividend growth track records. These often represent return of capital distributions or volatile micro-cap entities rather than analyst-endorsed picks, flagging them as potential traps rather than income opportunities.

| Stock | Current Yield | Payout Ratio | Recent Dividend | Share Price |

|---|---|---|---|---|

| Best Buy (BBY) | 6.16% | 65-70% | $0.96/share (14 April 2026) | ~$62 |

| General Mills (GIS) | 6.86% | 59% | $0.61/share (ex-date 10 April 2026) | ~$35.50 |

| Altria (MO) | 6.54% | ~100% (target 80%) | $1.06/share (payable 30 April 2026) | ~$64.80 |

The three featured stocks occupy distinct sector positions, each with structural factors that influence yield sustainability and risk profiles.

General Mills exemplifies the consumer staples defensive anchor, with its 6.86% yield standing three to four times above the sector average of 1.8-2%. The company’s brand portfolio spans established food categories where demand remains resilient through economic cycles. Stable food production and essential product positioning provide the earnings consistency that supports a 59% payout ratio without straining dividend coverage. Analysts highlight long-term payout growth backed by resilient demand for staples, a structural advantage in uncertain macroeconomic environments.

Altria carries the tobacco sector’s dual characteristics: a 55-year dividend growth track record paired with structural headwinds from declining smoking rates and regulatory pressures. The company has diversified into alternative products to offset conventional cigarette volume declines, but consumption trends remain a persistent drag on organic growth. The 6.54% yield compensates investors for accepting these sector-specific risks, while the Dividend King status signals management’s commitment to maintaining payouts through varied conditions. The payout ratio near 100% of recent earnings, though targeting 80% of adjusted figures, reflects this balance between yield delivery and earnings pressure.

Best Buy’s 6.16% yield is high for the retail sector, where dividend policies typically prioritise growth reinvestment over income distribution. The company’s omnichannel strategy and stable consumer electronics focus provide earnings support that has allowed consistent quarterly payments of $0.96 per share through fiscal 2026. Strong fiscal 2026 performance underpins the $801 million in annual dividends alongside share repurchases, a dual capital return profile that signals management confidence in cash generation capacity. The 65-70% payout ratio leaves room for both dividend continuity and operational flexibility, distinguishing Best Buy from retail peers with more capital-intensive expansion plans.

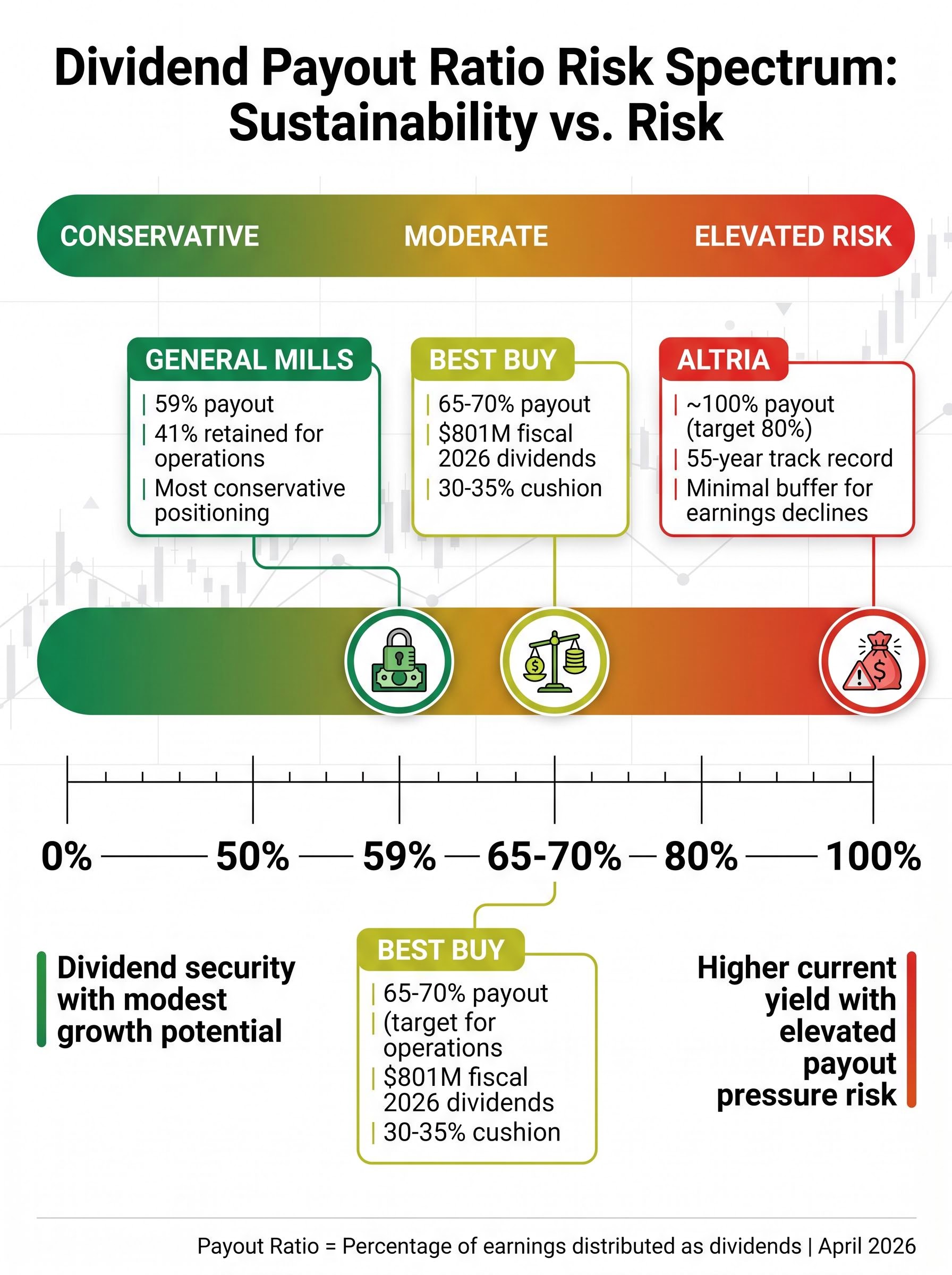

Payout ratio measures the percentage of earnings a company distributes as dividends, serving as the clearest indicator of whether a dividend can be maintained or increased through varying conditions. The metric reveals the buffer each company retains to absorb earnings volatility without cutting payouts.

Altria management has committed to mid-single-digit annual dividend growth through 2028, relying on adjusted earnings expansion to support payout increases while maintaining the target 80% payout ratio.

The payout ratio spectrum from 59% to 100% reflects different investor value propositions: General Mills and Best Buy offer dividend security with modest growth potential, while Altria delivers higher current yield with elevated risk that the payout may face pressure if earnings decline.

While Best Buy, General Mills, and Altria operate with payout ratios between 59% and 100%, investors seeking more conservative positioning may look at dividend policy frameworks targeting 20-30% payout ratios, which provide substantially larger earnings buffers for both operational flexibility and growth reinvestment.

The Federal Reserve maintained steady interest rates following its March 2026 meeting but signaled a pivot toward potential easing, with market expectations pricing in cuts totaling approximately 75 basis points throughout the year. This macroeconomic backdrop directly affects the relative attractiveness of high-yield dividend stocks versus fixed income alternatives.

Lower interest rates reduce borrowing costs for companies, easing debt service burdens and potentially expanding profit margins. For dividend payers like Best Buy, General Mills, and Altria, this translates to improved cash flow available for distributions. The mechanism also operates through investor positioning: as bond yields decline with rate cuts, equities offering 6%+ yields become more compelling on a risk-adjusted basis, particularly for income-focused portfolios.

Market expectations incorporate potential Federal Reserve cuts totaling approximately 75 basis points through 2026, which could enhance the relative appeal of high-yield dividend stocks.

Consumer staples and defensives benefit specifically from this environment. General Mills and Altria, with their stable cash flows and established payout histories, serve as bond proxies for investors seeking yield without full equity market volatility. If the Fed follows through on easing expectations, capital rotation from fixed income into dividend equities could compress yields (raising stock prices) while maintaining absolute income delivery, providing both income and capital appreciation potential.

Analysts emphasise monitoring inflation data for any policy reversals. If inflation resurges and forces the Fed to delay or abandon rate cuts, the relative appeal of dividend stocks diminishes as bond yields remain elevated. The 75 basis point easing scenario depends on inflation continuing to moderate, making inflation prints through Q2 and Q3 2026 critical data points for dividend stock positioning.

The 75 basis point easing scenario depends on inflation continuing to moderate, with oil price movements affecting Fed policy expectations serving as a critical variable. If crude prices sustain elevated levels through Q2 2026, the anticipated rate cuts could be delayed or abandoned entirely.

Each featured stock occupies a distinct position on the risk spectrum, driven by payout ratio discipline, sector dynamics, and earnings stability.

Best Buy carries lower risk with stability ratings equivalent to a B-grade. The 65-70% payout ratio provides a cushion that allows the company to maintain dividends even if consumer electronics demand softens modestly in coming quarters. Strong fiscal 2026 earnings backstop current payouts, and the omnichannel strategy positions the company to capture sales across physical and digital channels. Investors should watch Q2 2026 earnings reports for any signals of consumer spending weakness that could affect forward guidance, but the current setup suggests dividend security absent a severe retail downturn.

General Mills shares the lower-risk profile with B-grade equivalent stability. The 59% payout ratio is sustainable given stable fiscal 2026 earnings from essential food products. Consumer staples demand typically holds through economic cycles, providing earnings resilience that supports dividend continuity. The company’s strong brand portfolio and defensive sector positioning reduce vulnerability to discretionary spending pullbacks. Q2 2026 reports merit attention for any volume or pricing pressure, but the structural position favours dividend maintenance.

The stability ratings assigned to Best Buy and General Mills reflect defensive stock evaluation methodologies that prioritise earnings consistency and payout sustainability over growth potential, a framework increasingly relevant as investors rotate toward income in uncertain markets.

Altria operates in the moderate-high risk category despite its 55-year Dividend King status. The payout ratio near 100% of recent earnings, even with an 80% target on adjusted figures, leaves minimal buffer for earnings declines. Tobacco sector headwinds include regulatory scrutiny, declining smoking rates, and shifting consumer habits toward alternatives. The company’s diversification efforts into non-combustible products provide some offset, but the core business faces structural pressures. The Dividend King streak signals management’s commitment to maintaining payouts, yet the elevated ratio means any earnings miss could force a reassessment of dividend sustainability.

| Stock | Risk Level | Key Risk Factors | Mitigating Factors |

|---|---|---|---|

| Best Buy (BBY) | Lower Risk | Consumer spending shifts, electronics demand cycles | 65-70% payout ratio cushion, omnichannel strategy, strong fiscal 2026 results |

| General Mills (GIS) | Lower Risk | Input cost inflation, volume pressure | 59% payout ratio, defensive staples positioning, established brands |

| Altria (MO) | Moderate-High Risk | Declining smoking rates, regulatory pressure, ~100% payout ratio | 55-year Dividend King status, alternative product diversification, mid-single-digit growth plan through 2028 |

Ultra-high yield securities offering 40%+ returns often lack sustainability data, clear corporate identities, and established dividend track records. These represent potential dividend traps rather than analyst-endorsed income opportunities.

Ultra-high yields appearing in screeners at 40-50% contrast sharply with the three featured stocks. These often lack the corporate transparency, sustainability analysis, and Dividend King status that characterise Best Buy, General Mills, and Altria. Investors encountering such yields should verify the source of distributions (return of capital versus earnings), assess the issuer’s financial health, and determine whether the yield reflects genuine income opportunity or signals distress.

Investors evaluating high-yield dividend stocks can apply a structured framework that converts the analysis into portfolio action.

The yield threshold screening process in step 1 mirrors earnings screening methodologies that differentiate sustainable from unsustainable metrics, applying quantitative filters before qualitative assessment of sector dynamics and management track records.

Monitoring calendar items for ongoing evaluation:

This framework applies beyond the three featured stocks, providing evaluation criteria for any high-yield candidate that emerges in screening processes.

Best Buy, General Mills, and Altria deliver yields above 6% with varying risk profiles, supported by analyst endorsement and established dividend histories ranging from consistent quarterly payments to a 55-year Dividend King streak. The anticipated lower-rate environment, with potential Federal Reserve cuts totaling approximately 75 basis points through 2026, could enhance their relative appeal versus fixed income alternatives. Sustainability depends on payout ratio discipline, with General Mills’ 59% and Best Buy’s 65-70% providing more conservative positioning than Altria’s elevated ratio near 100%.

Review these stocks against your income requirements and risk tolerance. Consider starting with lower-risk positions in General Mills or Best Buy, with Altria as a yield-enhancing addition for those comfortable with tobacco sector dynamics and willing to monitor the elevated payout ratio closely. Watch Q2 2026 earnings reports for signals affecting forward guidance, and track Federal Reserve policy developments that could shift the relative attractiveness of high-yield equities versus bonds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

High yield dividend stocks are shares in companies that pay dividend yields significantly above market averages, often 5% or more, providing investors with regular income distributions funded by company earnings. The sustainability of these payouts depends on the company's payout ratio, sector stability, and earnings consistency.

Best Buy (6.16%), General Mills (6.86%), and Altria (6.54%) are three analyst-endorsed U.S. stocks offering yields above 6% in April 2026, each supported by established dividend histories and payout ratios that analysts consider sustainable.

Payout ratios below 70% are generally considered conservative and signal strong dividend security, while ratios between 70% and 85% carry moderate risk requiring earnings monitoring, and ratios above 85% demand closer scrutiny of earnings trends and management commentary.

When the Federal Reserve cuts interest rates, bond yields decline, making high yield dividend stocks more attractive on a risk-adjusted basis and potentially driving capital rotation from fixed income into dividend equities, which can raise stock prices while maintaining income delivery.

Sustainable dividends are typically backed by transparent financials, established payout histories, analyst endorsement, and payout ratios supported by consistent earnings, while dividend traps often feature ultra-high yields of 40% or more, lack corporate transparency, and may represent return of capital rather than genuine earnings distributions.