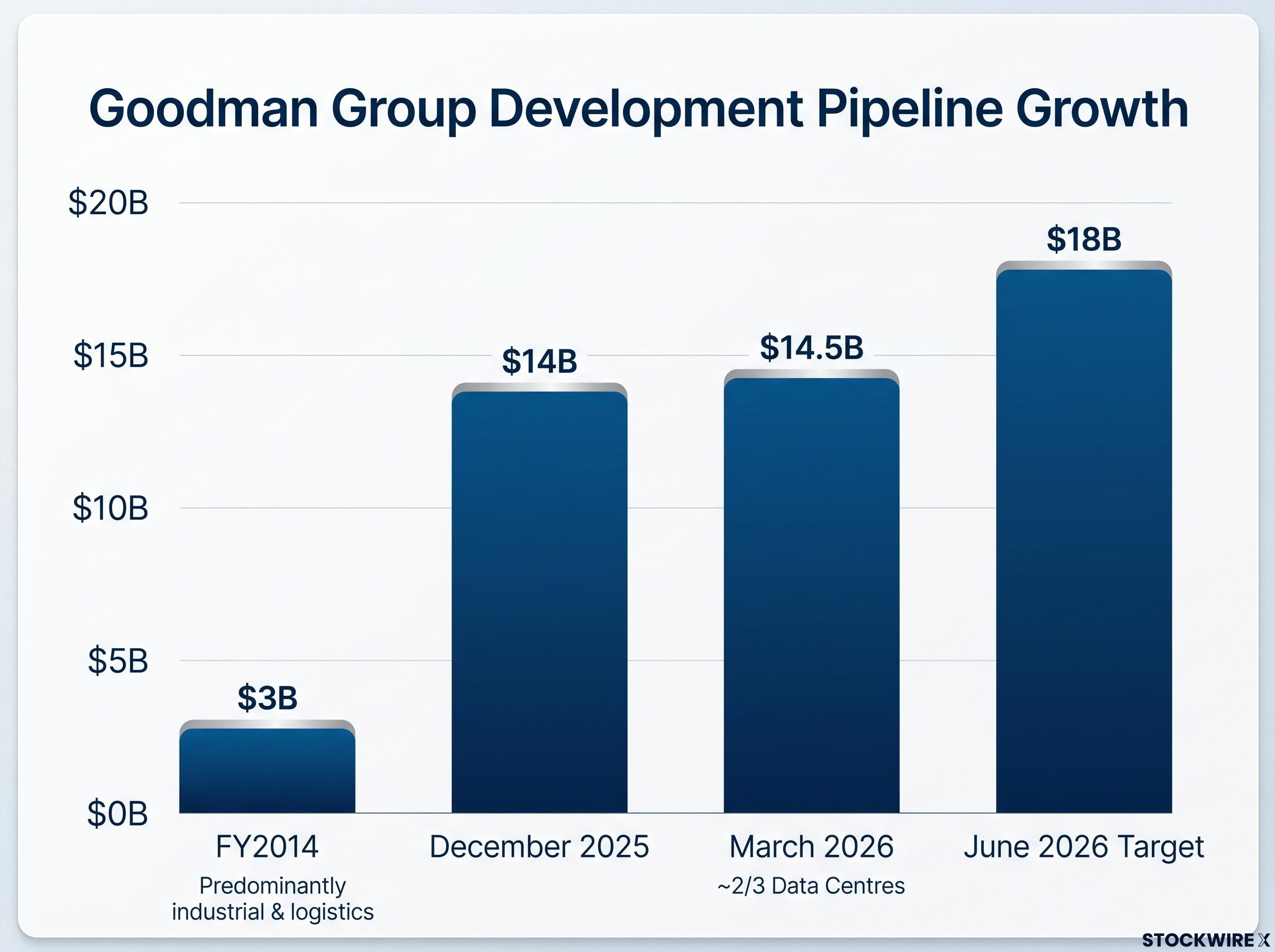

Goodman Group’s development pipeline has grown from $3 billion in fiscal year 2014 to $14.5 billion as of March 2026, with an $18 billion target due within weeks. Not a single major lease has been signed for the data centre projects that now make up two-thirds of that pipeline. With $3.5 billion in data centre commencements planned for June 2026 and delivery windows stretching to 2028-2029, the group is placing one of the largest speculative bets in Australian listed real assets, timed to coincide with surging institutional and retail investor interest in AI infrastructure exposure on the ASX.

This analysis unpacks how Goodman’s build-first, lease-later strategy works, why it diverges from industry norms, what Morningstar and the broader market see in the demand risk it introduces, and what investors should watch between now and the 2028-2029 delivery window.

From logistics landlord to data centre developer: the scale of Goodman’s strategic shift

The numbers tell the story of a company that has quietly re-engineered itself. A decade ago, Goodman Group operated a $3 billion development pipeline anchored to industrial and logistics assets across Australia, Asia, and Europe. By December 2025, that figure had reached $14 billion. By the end of March 2026, it stood at $14.5 billion, with an $18 billion target set for the close of June 2026.

Pipeline growth: From $3 billion in FY2014 to $14.5 billion at March 2026, a near five-fold increase in a decade, with data centres now accounting for approximately two-thirds of the total.

The composition of that pipeline has shifted just as sharply as its size. Data centres now account for roughly two-thirds of the pipeline by value, displacing the industrial and logistics properties on which the group built its reputation.

- FY2014: $3 billion pipeline, predominantly industrial and logistics

- December 2025: $14 billion pipeline; total assets under management reach $87 billion

- March 2026: $14.5 billion pipeline; data centres represent approximately two-thirds

- June 2026 target: $18 billion pipeline

With total assets under management at $87 billion as of December 2025, roughly triple the level from a decade earlier, and management reaffirming at least 9% operating earnings growth for fiscal year 2026, the pipeline composition carries real weight. Goodman’s earnings trajectory is now structurally tied to data centre delivery and lease-up in a way it was not three years ago.

The investor appeal of ASX AI infrastructure exposure is partly structural: colocation operators, property developers like Goodman, and network services providers each sit at different points in the same capital cycle, offering distinct risk profiles within a single macro theme that has accelerated sharply since 2023.

When big ASX news breaks, our subscribers know first

What the build-first, lease-later strategy actually means in practice

The label sounds straightforward. The mechanics are not. Goodman breaks ground on data centre projects without securing tenant pre-commitments, using its own balance sheet and third-party capital partners to fund construction through to near-completion. The rationale, as management has articulated, is twofold: lock in construction costs early while positioning to achieve higher lease pricing as assets approach delivery, when supply scarcity should be most acute.

This approach sits well outside the industry norm. Large-scale data centre developers, including Digital Realty and Equinix, typically require anchor tenant pre-leasing of approximately 50-70% before proceeding with full build-out. Speculative shell construction is used selectively in markets with proven demand and tight power, but interior fit-out is generally tied more closely to signed contracts.

| Attribute | Goodman Group | Industry norm (Digital Realty, Equinix) |

|---|---|---|

| Pre-commitment requirement | None as of March 2026 | Approximately 50-70% pre-leased |

| Primary risk mitigation tool | Third-party capital partners | Anchor tenant agreements |

| Construction start trigger | Strategic site and power readiness | Pre-leasing threshold met |

| Lease pricing timing | Negotiated closer to completion | Locked in before or during build-out |

For Goodman’s own non-data-centre portfolio, high pre-commitment levels alongside long-duration leases have historically been a standard requirement. The data centre approach is a conscious strategic departure, not an extension of existing practice.

Third-party capital as the risk buffer

Instead of tenant pre-commitment, Goodman brings institutional capital partners into its development structures. The own-develop-manage model means completed assets are typically transferred into investment funds or joint ventures, distributing the risk across institutional balance sheets rather than concentrating it on the listed entity.

Goodman’s established relationships with institutions such as GIC and CPPIB in earlier structures illustrate the model. No post-March 2026 disclosure has confirmed a new capital vehicle or joint venture specifically for the current data centre pipeline, a gap that itself carries informational weight for investors.

Why Australian data centre conditions make speculative construction more defensible than it sounds

The strategy carries less risk in Australia than it might in a market with abundant power and land. Three structural factors underpin that distinction.

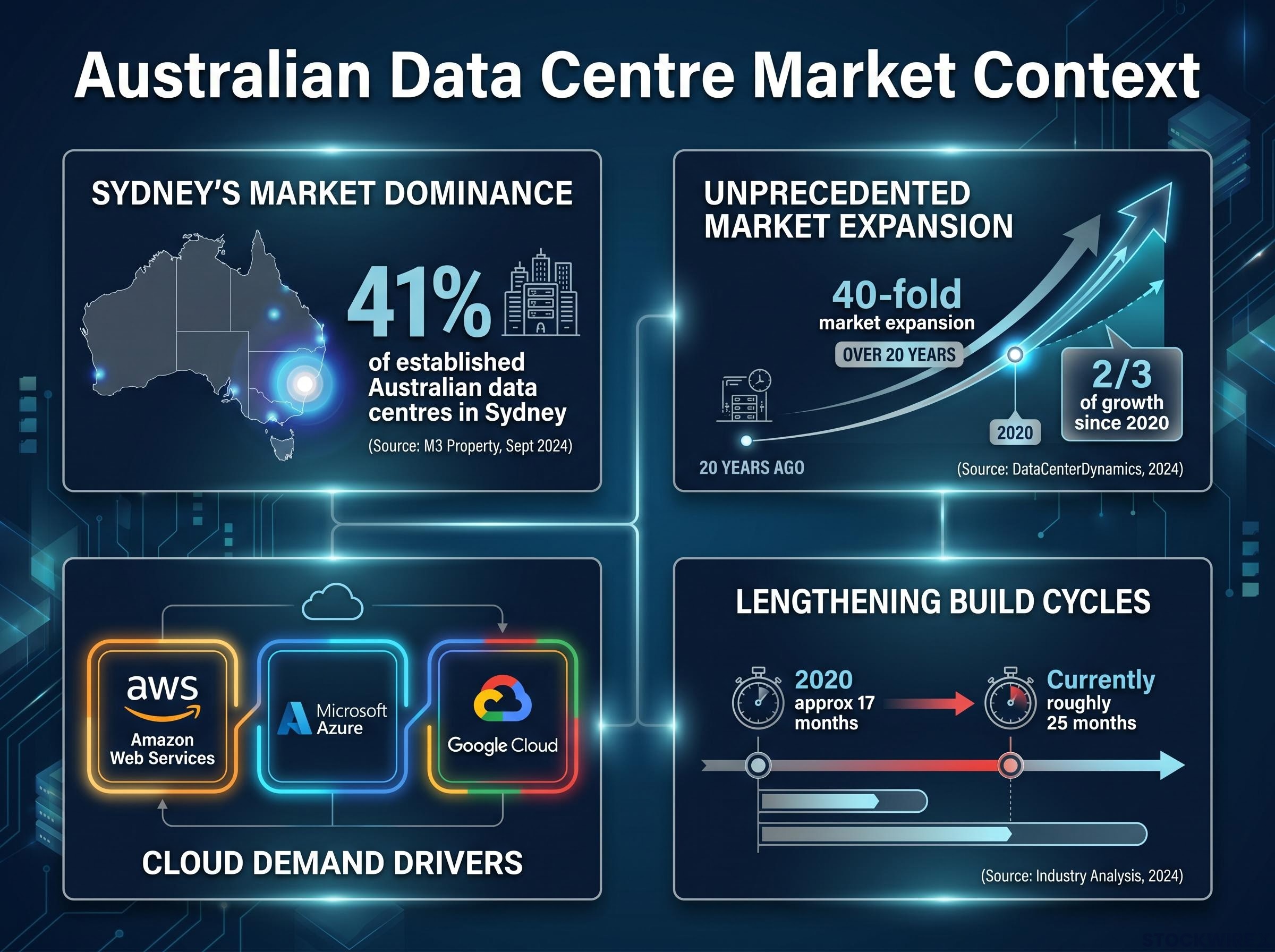

Sydney is the country’s primary hyperscale hub. According to M3 Property (September 2024), approximately 41% of established Australian data centres are concentrated in the city, with Western Sydney serving as the primary greenfield corridor for new capacity. The geographic concentration means hyperscaler demand is funnelled into a narrow set of corridors where Goodman already holds positions.

M3 Property’s Australian data centre report projects national capacity to more than double to 3,100 MW by 2030, with a potential supply gap of 0.7-1.7 GW by 2028, a structural shortfall that directly supports the case for speculative construction in a market where demand is outpacing committed pipeline.

According to DataCenterDynamics (using DC Byte research, 2024), Australia’s data centre market has expanded roughly 40-fold over 20 years, with two-thirds of that growth occurring since 2020.

Power availability, not zoning or land, is the binding constraint on new supply. Securing power connections and substation capacity in Sydney and Melbourne is increasingly difficult, favouring developers with pre-secured infrastructure regardless of lease status. A developer holding power-ready sites in a constrained corridor occupies a structurally advantaged position.

Power availability constraints in Australia’s main data centre corridors are now formally recognised by AEMO as a structural demand driver, with the Draft 2026 Integrated System Plan projecting nearly 10 TWh of additional electricity load by 2033-34 under an accelerated data centre growth scenario, a figure that reinforces why grid-ready site positions carry strategic value independent of leasing status.

The demand drivers reinforcing that position are threefold:

- Cloud adoption from AWS, Microsoft Azure, and Google Cloud, all of which have expanded their local presence

- AI workload growth, which has accelerated hyperscale capacity requirements since 2023

- Data localisation requirements, which keep a floor under domestic demand independent of global cycles

These conditions provide a structural buffer for speculative capacity. They do not, however, eliminate timing risk, particularly if multiple developers deliver simultaneously into the same corridors.

The risk Goodman is running: what analysts and the market see for 2028-2029

Morningstar analyst Yingqi Tan, in an assessment published 3 June 2026 (data as of 29 May 2026), offered a measured reading: the absence of signed leases does not signal weak demand for Goodman’s facilities, and leasing is likely to be achieved as projects approach their 2028-2029 completion dates. Goodman is reportedly in active discussions with several potential customers.

Morningstar’s view (Yingqi Tan, 3 June 2026): The lack of signed leases does not indicate weak demand. Leasing is expected to be achieved as projects approach completion in 2028-2029.

That assessment carries weight, but it rests on assumptions about demand arriving on schedule. The risk scenarios analysts and industry commentators flag are more specific than a generic “demand might not show up.”

The conditions that would make the risk materialise

Three variables determine whether Goodman’s speculative exposure becomes a headwind rather than a competitive advantage:

- Pace of competing supply delivery. If multiple developers, including other Australian REITs and global operators, complete large campuses simultaneously in Western Sydney and Melbourne’s main corridors, a period of elevated vacancy or discounted pricing during lease-up becomes possible.

- Power connection constraints. If regulatory or infrastructure changes ease power approvals faster than expected, the supply scarcity that currently limits competition could erode, widening the field of viable developers.

- Hyperscaler contract timing. Management has described leasing discussions as active but undisclosed. The timeline and scale of those conversations will determine whether capacity is absorbed before or after delivery.

Build cycles have also lengthened. Average project completion time has extended from approximately 17 months in 2020 to roughly 25 months currently, reflecting the higher concentration of data centre developments. With $3.5 billion in commencements planned for June 2026, a substantial tranche of this exposure will push into the 2028-2029 delivery window, concentrating lease-up risk into a relatively narrow period.

How Goodman’s strategy compares with how global listed peers manage the same trade-off

The contrast between Goodman’s approach and global best practice is a matter of degree, not of kind. Digital Realty and Equinix use speculative shell construction in select markets, but their large campus developments are typically structured in phases, with initial phases approximately 50-70% pre-leased before full fit-out proceeds. Interior fit-out spending is tied to signed contracts, limiting balance-sheet exposure to demand timing.

Goodman’s posture is materially different. As of March 2026, the data centre component of its $14.5 billion pipeline carried no anchor tenant agreements. The three structural differences are:

Pre-committed hyperscaler contracts of the kind CDC Data Centres secured in May 2026 — a 555MW deal that pushed its total contracted capacity past 1GW — illustrate the alternative model that Goodman has chosen to move away from: signed anchor agreements before construction proceeds rather than building to readiness and negotiating closer to completion.

- Commitment timing: Goodman begins construction without pre-commitments; global peers require partial pre-leasing before full build-out.

- Fit-out trigger: Goodman’s model funds construction through to near-completion on a speculative basis; peers typically phase fit-out spending alongside leasing progress.

- Risk allocation mechanism: Goodman distributes exposure through institutional capital partnerships and fund transfers; peers rely primarily on tenant contract security.

The own-develop-manage model and fund transfer mechanism mean the listed entity’s balance sheet does not carry the full weight of speculative exposure indefinitely. Institutional capital, including pension funds, sovereign wealth funds, and infrastructure funds, absorbs a share of the risk.

That said, institutional capital typically prefers phased fit-out spending tied to leasing milestones, and no public disclosure details how speculative risk is allocated in Goodman’s current data centre structures. For investors, that absence is itself a data point worth registering.

What the June 2026 commencement milestone means for investors tracking this story

The $18 billion pipeline target and the $3.5 billion commencement goal represent the first verifiable checkpoint in a multi-year thesis. If met, both figures signal execution capacity and management confidence. If deferred, they raise questions about demand visibility or capital availability that would warrant direct engagement with management.

The next event horizon is the FY2026 full-year results, which will provide the first definitive pipeline update after the June 2026 target and likely include updated commentary on leasing discussions. Four specific signposts will shape how the market reads Goodman’s data centre position through fiscal year 2027 and beyond:

- June 2026 pipeline confirmation: Does the pipeline reach $18 billion on schedule?

- FY2026 results commentary: Does management offer greater specificity on leasing discussions and tenant interest?

- Capital partnership announcements: Does Goodman disclose a new joint venture or capital vehicle specific to the data centre pipeline?

- First lease or pre-commitment signing: Does any anchor tenant agreement materialise before the 2028-2029 delivery window?

Goodman’s at least 9% operating earnings growth target for fiscal year 2026 provides a near-term performance floor. The longer-term trajectory, through FY2027 and into FY2028, is increasingly linked to whether hyperscaler demand validates the build-first bet on schedule.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The bet Goodman is making, and what has to go right

Goodman has chosen speed and cost certainty over demand certainty. The wager is that AI-driven hyperscaler appetite in Sydney and Melbourne will be sufficient to absorb a speculative pipeline of this scale by 2028-2029, and that locking in construction costs now will deliver stronger lease economics than waiting for pre-commitments that might never arrive on preferred terms.

The same power constraints and supply scarcity that make the strategy defensible also make execution harder and more capital-intensive than the group’s traditional logistics model. Delivery timelines are longer. Capital requirements are larger. The margin for error on lease-up timing is narrower than anything Goodman has managed at this scale before.

Investors who share management’s demand thesis have a clear set of milestones to evaluate. The June 2026 commencement target is the first checkpoint. What follows, whether leases materialise, capital partners are named, and competing supply arrives on time or late, will determine whether Goodman’s largest strategic bet becomes its most consequential success or its most expensive lesson.

Investors exploring the broader investment landscape around the Australian data centre build-out will find our full explainer on ASX electrical infrastructure stocks, which examines how companies such as Genus Plus and Southern Cross Electrical are capturing earnings growth as picks-and-shovels beneficiaries of the same AU$26 billion construction programme that is expanding Goodman’s pipeline.

Forward-looking statements regarding Goodman’s pipeline targets, leasing expectations, and delivery timelines are based on management commentary and analyst assessments. These are subject to change based on market developments and company performance. Past performance does not guarantee future results.