Australia has not entered a technical recession. That fact has become the centrepiece of a resilience narrative that has shaped how many investors think about their domestic equity exposure. The problem is that avoiding recession and operating in a healthy economy are not the same thing, and the gap between those two ideas is where portfolio risk is building.

VanEck’s latest assessment puts the distinction in blunt terms. The firm describes the domestic economy as “shaky,” characterises GDP as having “stalled,” and warns of a “very real prospect of a hard landing” if conditions deteriorate further. The forward-looking indicators give substance to that concern: business hiring plans are losing momentum, consumer sentiment has yet to recover, and trimmed mean inflation is still sitting above the Reserve Bank of Australia’s (RBA) target band. None of that reads like an economy investors should be building around with passive confidence.

Here is the analytical framework for separating the economic headline from the investment reality, and for understanding which parts of a portfolio carry the most exposure to a decelerating domestic environment.

The gap between Australia’s resilience story and what the data actually shows

The Australian economy managed to absorb the pandemic shock, the steepest interest rate tightening cycle in a generation, and prolonged cost-of-living pressure, all without tipping into negative growth territory. That is a legitimate achievement, and it gives the resilience narrative a real foundation.

The issue is what investors have done with that narrative since. VanEck’s published assessment reframes the achievement sharply: the absence of a recession tells you little about the underlying vitality of the economy. Their language is deliberately pointed. The economy is “shaky.” GDP has “stalled.” Leading indicators, including softening hiring plans, subdued private investment, and chronically weak household sentiment, point to an economy losing speed rather than building it.

VanEck explicitly warns against “irrational exuberance” and acknowledges the “very real prospect of a hard landing” if conditions worsen.

The backward-looking “no recession” milestone tells investors where the economy has been. The forward-looking indicators tell them where it is going. For portfolio construction, the second set of data matters more. Anchoring to the resilience story without accounting for current deceleration signals means building a portfolio on assumptions that applied to a different period.

Australia’s aggregate headline GDP figure obscures the per capita recession already running beneath it, with output per person falling approximately 0.7% across 2025 even as total growth registered positive, corporate insolvencies reaching their highest level since 1990-91, and real wages declining as wage growth failed to keep pace with CPI.

When big ASX news breaks, our subscribers know first

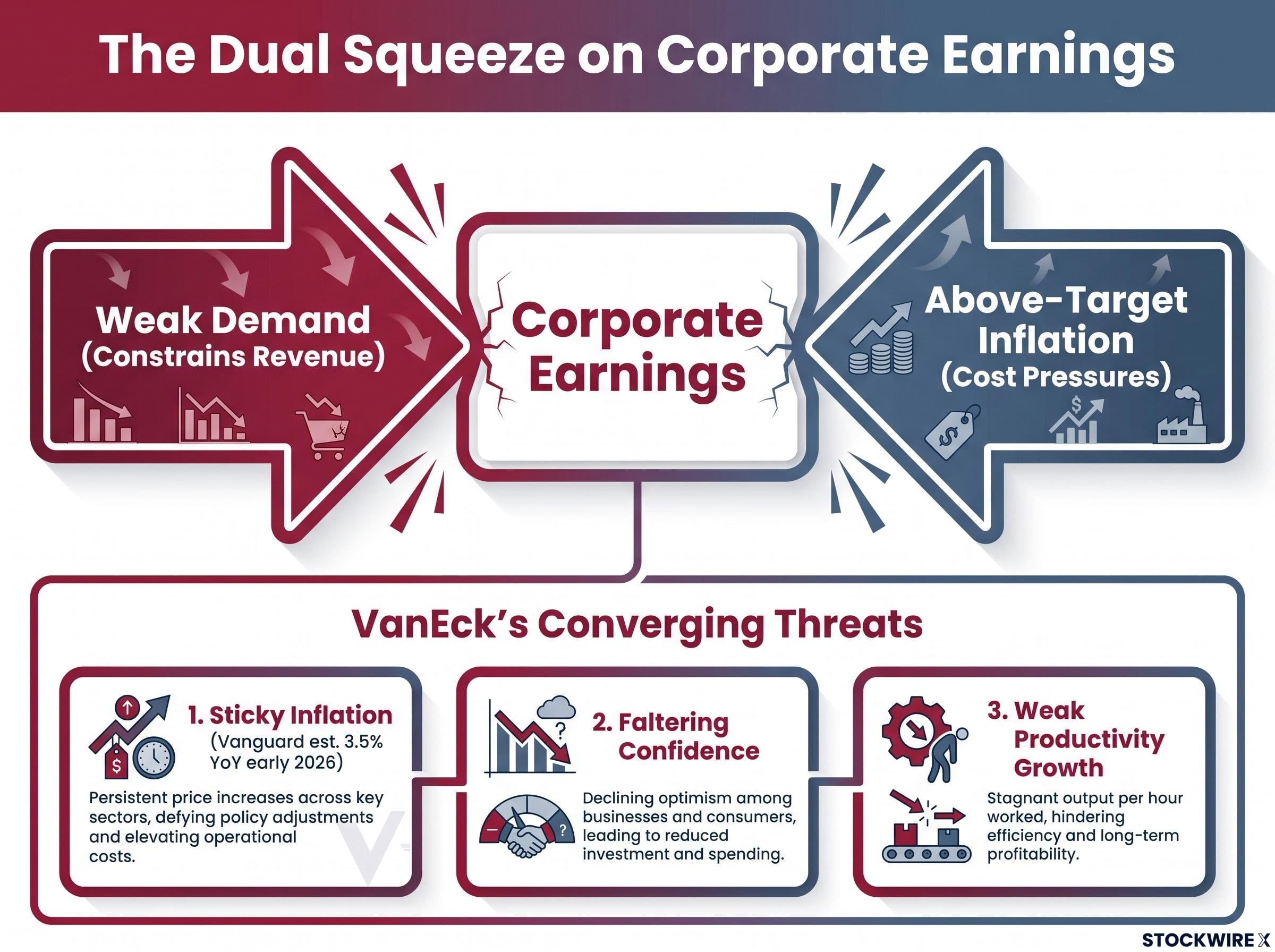

What slowing growth and sticky inflation actually mean in combination

Either of these conditions alone is manageable. Slowing growth in isolation typically triggers rate cuts that cushion earnings and support asset prices. Above-target inflation in isolation is uncomfortable but tolerable when revenue growth is strong enough to absorb cost pressures.

The problem is what happens when they arrive together. VanEck identifies three converging threats in the current environment:

- Sticky inflation that refuses to fall cleanly to the RBA’s target

- Faltering consumer and business confidence

- Weak productivity growth across the economy

This combination operates as a dual squeeze on corporate earnings. Weak demand constrains revenue from one side. Above-target inflation sustains cost pressures on margins from the other. Real household disposable incomes are being eroded, and consumer spending is described as “stalling.”

Vanguard’s outlook estimated trimmed mean inflation at approximately 3.5% year-on-year in early 2026, still above the RBA’s target band. The Organisation for Economic Co-operation and Development (OECD) has stated that monetary policy “should remain restrictive until underlying inflation is clearly on track” to target.

The RBA’s May 2026 Statement on Monetary Policy confirmed trimmed mean inflation at 3.5% in the March quarter of 2026, still materially above the target band, with the assumed cash rate path holding elevated through the end of the year.

Why the RBA’s hands are tied

Above-target inflation means rate cuts would risk reigniting price pressures. The RBA cannot deploy the stimulus tool that has historically cushioned downturns. That policy constraint is the part of this story that most directly limits relief: the earnings pressure from slowing demand does not have a rate-cut offset waiting in the wings.

Understanding the ASX 200’s structural vulnerability to a domestic slowdown

The S&P/ASX 200 is not a diversified snapshot of the global economy. It is structurally concentrated in two sectors, financials and resources, with limited exposure to the technology, healthcare, and industrial innovation sectors that have driven global equity returns over the past decade.

ASX 200 concentration risk is more severe than the 200-stock label implies: financials and materials together account for more than 50% of the index by market-cap weight, and VanEck research shows two stocks alone have historically represented approximately 22% of a typical cap-weighted Australian equity portfolio.

That concentration means the index amplifies domestic economic risk rather than diversifying it. When Australia decelerates, the ASX 200’s largest positions decelerate with it.

| Sector | Key vulnerability | Macro channel |

|---|---|---|

| Financials (major banks) | Household financial stress, slowing credit growth | Higher rates and living costs squeeze borrowers; weak confidence reduces demand for new credit |

| Resources | Domestic cost inflation, cyclical commodity volatility | Wages, energy, and regulatory costs rise while commodity prices remain subject to global cycles |

The major banks are particularly exposed. They sit at the intersection of household stress and credit demand; both deteriorate when confidence weakens and real incomes fall. Resources companies face a different version of the same problem: global commodity cycles can help, but domestic cost pressures from wages, energy, and regulation are harder to manage when inflation stays above target.

For investors who believe they are diversified because they hold a broad ASX index fund, the structural reality is that broad domestic exposure and genuine diversification are not the same thing in a slowing economy.

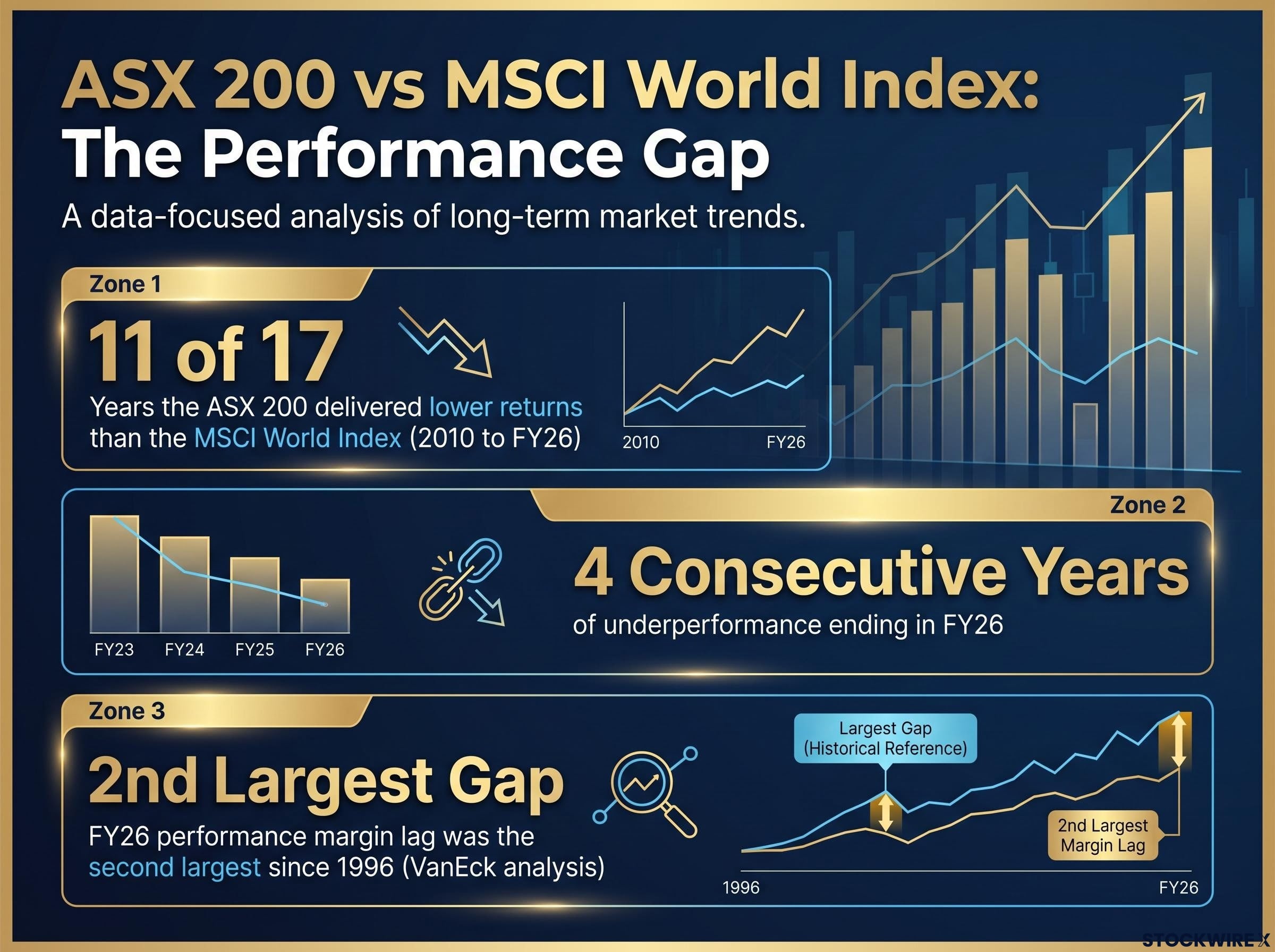

How the ASX 200 has performed against global markets over the long run

The structural argument has a performance record attached to it, and VanEck’s analysis quantifies the cost:

- Over the 17 financial years from 2010 to FY26, the ASX 200 delivered lower returns than the MSCI World Index, which measures performance across global developed markets, in 11 of those years

- The stretch of underperformance extended to four consecutive financial years by the end of FY26

- The margin by which the ASX 200 lagged in FY26 ranked as the second largest recorded since 1996

The FY26 performance gap between the ASX 200 and the MSCI World Index was the second largest on record since 1996, according to VanEck’s analysis.

This is not a short-term anomaly. The sectors that have driven global returns over the past 15 years, technology, healthcare, and industrial innovation, are systematically underrepresented in the ASX 200. The structural reasons for that underperformance do not change simply because Australia avoided a technical recession.

The long-run performance gap between Australian and global equities has compounded into dramatically different terminal wealth outcomes: the S&P 500 returned 16.03% per year in Australian dollar terms over 15 years to April 2026, compared to just 8.62% for the ASX 300, with financials and materials anchoring the domestic index to regulated lending growth and commodity cycles rather than technology-led reinvestment.

For investors whose portfolios carry a heavy home bias, this performance record means that defaulting to the ASX 200 as a core long-term holding has, for most of the past 15 years, meant accepting lower returns than a globally diversified alternative. Combined with the macro headwinds already outlined, there is no structural reason for that pattern to reverse while the index remains concentrated in domestic financials and resources.

The next major ASX story will hit our subscribers first

What a quality and diversification tilt actually looks like in practice

Moving from diagnosis to response, three portfolio adjustment principles are worth considering in the current environment:

- Quality tilt. VanEck’s recommended orientation focuses on companies with stable earnings, high return on equity (ROE), which measures how effectively a company generates profit from shareholder funds, and low leverage. In a slow-growth, sticky-inflation environment, companies that can sustain margins without relying on cheap credit or booming demand are better positioned to deliver consistent returns.

- Global diversification. Increasing exposure to international markets provides access to the technology, healthcare, and global industrial sectors that are structurally underweight in Australia and have driven the bulk of developed-market equity returns over the past decade. This is a structural adjustment, not a short-term trade.

- Tail-risk hedging. VanEck recommends considering assets such as gold and gold miners as part of a portfolio strategy designed for a more uncertain, still-inflationary environment. In fixed income, the principle favours investment-grade credit over high-yield in a slow-growth backdrop where default risk rises before rate relief arrives.

This orientation is not a defensive retreat from equities. It is a recalibration of where within equities the risk-reward proposition looks most credible given where the Australian economy currently sits.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

What the deceleration signal changes, and what it does not

The analysis does not call for abandoning Australian equities. It calls for questioning whether passive, home-biased reliance on the ASX 200 is the right default in an economy that is decelerating, still grappling with above-target inflation, and structurally concentrated in the sectors most exposed to both.

The portfolio actions the evidence supports are specific: a quality tilt, greater global diversification, and explicit risk management through defensive allocations. The actions it does not support are equally specific: a wholesale exit from domestic equities or a panic-driven reallocation based on a single quarter’s data.

VanEck’s framing is measured but firm. The case is not to flee Australia; it is to avoid complacency and manage concentration risk deliberately.

For investors wanting to explore the structural case in full, our deep-dive into cutting ASX home bias examines four compounding headwinds including an ROE deficit versus US markets, an iron ore demand ceiling, and stagflationary domestic conditions, covering why the ASX 200’s underperformance is structural rather than cyclical.

The question the analysis leaves every investor with is personal: does my current portfolio reflect where the Australian economy is going, or where it has been? The resilience narrative was earned. But avoiding recession and operating in a growth-generating environment are not the same thing, and portfolio construction should reflect that difference.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.