Equity indices are at or near new highs. Corporate earnings have largely beaten expectations. On the surface, mid-2026 looks like a market doing exactly what it should. The problem is what the surface is hiding.

Major institutional strategists, including those at Morgan Stanley, J.P. Morgan, and Robeco, are describing the current advance in terms that should give investors pause: narrow leadership, assumption-dependent gains, and structural vulnerabilities building in segments that headline index data simply does not capture. A market that looks calm is not necessarily a market that is calm.

Here is a clear analytical framework for reading this environment accurately, including why strong earnings are not moving prices, what professional investors mean when they call a rally fragile, and where the accumulating risks actually sit. These are the tools for making sense of a market that rewards careful reading right now.

Why the rally looks stronger than it is

The rebound has been real. Equity markets have lifted to new highs through the first half of 2026, and the headline numbers tell a story of recovery, momentum, and renewed confidence. That story is incomplete.

Morgan Stanley has noted that the gains driving those new highs are concentrated in a small cohort of AI-linked large-cap names rather than distributed broadly across the market. J.P. Morgan’s 2026 outlook goes further, explicitly characterising the current environment as one in which risk and resilience coexist, a condition the bank describes as “fragile.”

Record market concentration data from Wolfe Research shows five companies now controlling roughly 30% of total US equity capitalisation, a level that exceeds the dot-com peak and means passive index holders are carrying this narrow-leadership risk by default, without having made an active decision to do so.

J.P. Morgan’s 2026 outlook explicitly describes the current market environment as “fragile,” emphasising that risk and resilience coexist and that investors must navigate a delicate balance between the two.

The concentration dynamic is the structural feature that separates this rally from a healthy broad advance. Three characteristics define it:

- Concentrated leadership: A handful of AI-linked names are responsible for the bulk of index-level gains, while the majority of listed companies are not participating in the advance.

- Assumption-dependency: The rally holds as long as benign rate expectations and AI capital expenditure growth projections hold, and not a moment longer.

- Low tolerance for negative surprises: When a small number of stocks carry the index, a single macro disappointment can produce outsized index-level damage.

What this means in practice is that a broadly positive index return may be masking flat or negative performance across most of your portfolio’s individual holdings. The headline number and your actual exposure may be telling very different stories.

When big ASX news breaks, our subscribers know first

What “fragile” actually means in practice

The word gets used loosely. In the institutional context, fragility does not mean a crash is imminent. It means the rally’s tolerance for negative surprises is unusually low relative to the index levels at which it is trading. The market can absorb good news comfortably. It cannot absorb bad news proportionally.

That distinction matters because it shifts fragility from a prediction (something will break) to a structural condition (the system is less resilient than it appears). The second framing is more useful. It tells you to monitor, not to panic.

The cross-asset signals worth watching

The mechanism by which corrections appear sudden is worth understanding. Indices absorb small shocks one at a time, a disappointing data print here, a minor geopolitical flare there, while underlying positioning, leverage, and sentiment become progressively more brittle. Nothing visibly breaks until a threshold is crossed and the accumulated pressure releases rapidly. The correction looks sudden. The fragility was not.

J.P. Morgan and Morgan Stanley both describe this coexistence of surface resilience and background instability as a defining feature of the current cycle. Robeco frames it more directly, characterising the broad asset price inflation since 2025 as an “everything rally” that has created pockets vulnerable to a sharp reality check, with private debt flagged as a potential flash point.

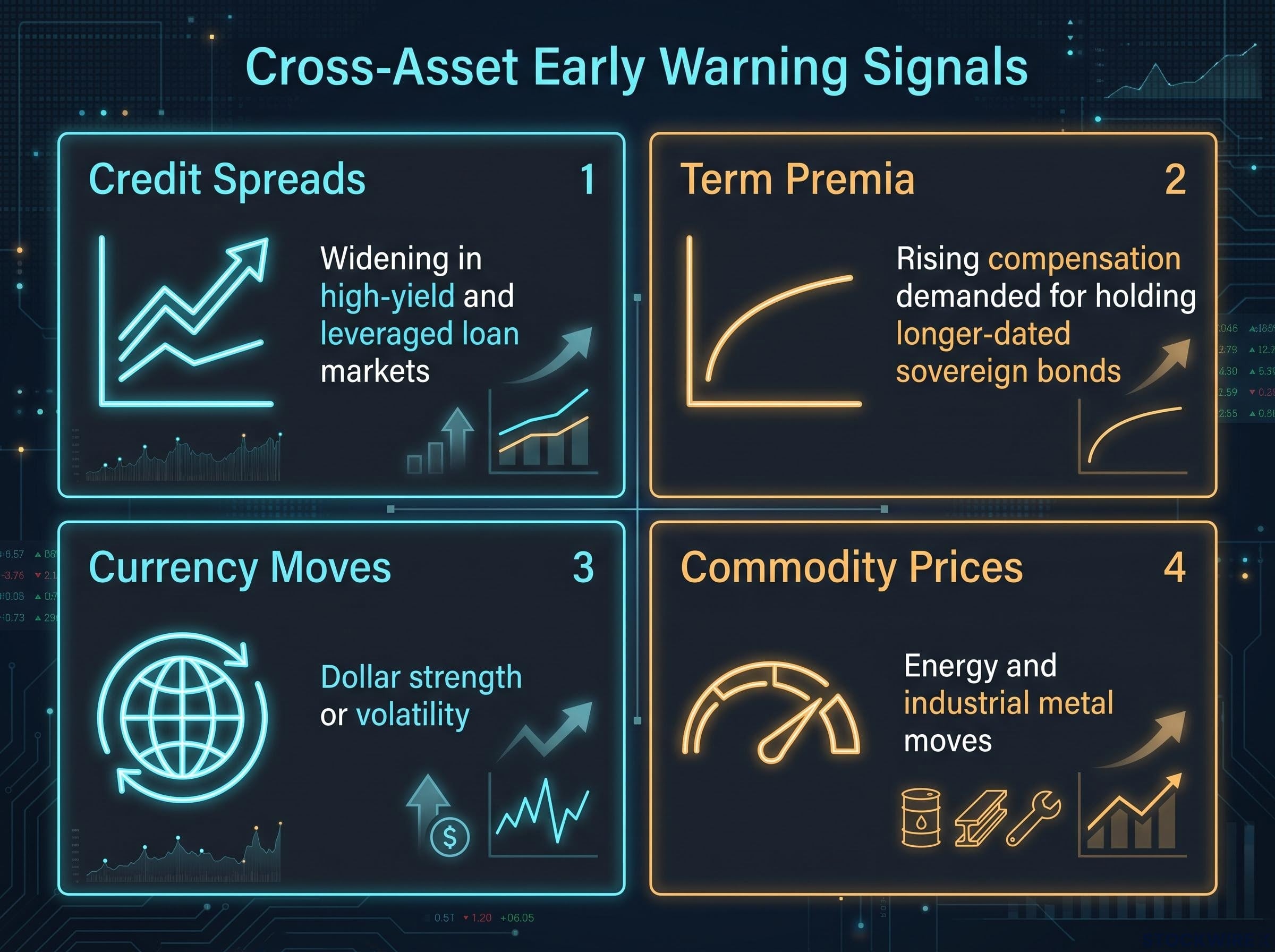

The practical implication is that monitoring only index-level price action provides a false sense of security in this environment. The real signal sits in cross-asset indicators that accumulate before the threshold is crossed:

- Credit spreads: Widening in high-yield and leveraged loan markets signals stress before equity prices adjust.

- Term premia: Rising compensation demanded for holding longer-dated sovereign bonds indicates shifting rate expectations.

- Currency moves: Dollar strength or volatility disrupts multinational earnings and emerging-market funding conditions.

- Commodity prices: Energy and industrial metal moves feed directly into inflation expectations and central bank responses.

These signals work precisely because they operate in markets with different participant bases and shorter feedback loops than listed equities. They move first.

When earnings beats stop translating into price gains

Here is the puzzle. Corporate earnings in mid-2026 have largely beaten consensus expectations. Historically, beats produce price gains. This cycle, they are not.

The disconnect is not one thing. It is three forces operating simultaneously, and they are worth ranking in order of analytical weight:

- Forward guidance is carrying more weight than backward-looking results. In an uncertain macro setting, strategists consistently stress that the quality and confidence of forward guidance outweighs what happened last quarter. Companies delivering strong historical numbers but issuing cautious or ambiguous outlooks are being penalised, not rewarded.

- Expectations were already priced in. The “buy the rumour, sell the news” dynamic is playing out across multiple sectors. Market participants had already incorporated anticipated beats into prevailing valuations before results were published, leaving little incremental upside to be realised on announcement.

- Macro variables are overwhelming company-specific positives. Rates, term premia, energy prices, and geopolitical developments are frequently overriding what would otherwise be share-price-positive earnings prints.

In a macro-dominant environment, the revision trajectory in forward guidance is where the actual information content sits, not the comparison between reported results and pre-announcement consensus.

Beneath the index surface, composition is shifting. Investors are rotating toward defensives and non-US markets, a repositioning that index-level stability obscures. If you are using headline earnings beats as a signal for adding exposure, you are looking at the wrong data point. The forward guidance revision trend is the signal that matters right now.

AI optimism, IPO signals, and the valuation compression risk

Artificial intelligence remains the dominant market narrative of the cycle, and the gains it has produced are real. The question is whether the assumptions embedded in current valuations are equally real.

Concentrated AI-linked leadership has driven index-level performance while compressing the margin of safety for investors entering at current prices. Major banks and asset managers have warned that near-term AI-linked earnings optimism may be overstated, given that recent margin strength in AI-adjacent sectors partly reflects pricing power rather than fully proven productivity gains. The extrapolation of AI capital expenditure benefits into durable, economy-wide margin expansion has not yet been empirically validated at scale.

Markets are pricing in AI productivity benefits before those benefits have been empirically validated at scale, compressing the margin of safety for investors entering at current valuations.

The SK Hynix US IPO in July 2026 offers a concrete illustration. The South Korean memory chip maker brought in approximately $26.5 billion, a figure that placed the transaction among the largest listings ever recorded, with demand from investors reportedly running at more than seven times the available allocation. When sophisticated holders with deep informational advantages choose to crystallise value at prevailing valuations through a transaction of that scale, it is analytically reasonable to ask what that signals about the risk-reward for incoming buyers.

More broadly, large-scale technology and AI-adjacent IPOs through 2026 reflect a pattern of well-informed holders willing to monetise aggressively at current valuations. Combined with unvalidated productivity extrapolation, the specific warning indicators are worth tracking:

- Concentrated gains in a narrow cohort of AI-linked names

- Pricing-power-versus-productivity ambiguity in reported margins

- Capex extrapolation risk as markets assume linear translation from investment to economy-wide returns

- Large-scale insider monetisation activity signalling informed holders are comfortable selling at these levels

This combination is not a sell signal on its own. But it is a signal to stress-test the assumptions embedded in your AI-linked positions before the validation data arrives.

Where the hidden risks are actually accumulating

The risks most likely to produce a sudden correction are precisely the ones that do not show up in equity market volatility readings until after the threshold has been crossed.

| Risk Category | Where It Is Accumulating | Mechanism for Market Impact |

|---|---|---|

| Private credit | Segments inflated by the post-2025 “everything rally,” where valuations are extended and liquidity is thin | A liquidity crunch forces selling into public markets, creating sudden cross-market pressure not predictable from equity volatility alone |

| Geopolitical tail risks | Energy supply chokepoints (e.g., Strait of Hormuz), trade policy escalation | Rapid re-ignition of inflation expectations pushes sovereign yields higher and compresses risk sentiment across asset classes simultaneously |

| Term premia | Sovereign debt markets, where structural instabilities are building while risk assets still perform on the surface | Rising compensation demanded for duration risk reprices the discount rate applied to equity valuations, particularly long-duration growth stocks |

Robeco has flagged private debt specifically as a potential flash point within the “everything rally” dynamic. The concern is straightforward: when broad asset price inflation inflates segments with limited liquidity, a forced-selling event in those segments spills into public markets with little warning.

Robeco’s January 2026 market monitor uses the term ‘everything rally’ explicitly to characterise post-Liberation Day asset price inflation, identifying private debt as the segment where systemic risks have been rising most materially within that dynamic.

Geopolitical tail risks follow a different but equally dangerous mechanism. A scenario such as renewed Strait of Hormuz disruptions could quickly re-ignite inflation expectations, push yields higher, and compress risk sentiment across asset classes simultaneously, overwhelming what appear to be stable macro backdrops.

Why equity volatility is the wrong early-warning system

Volatility indexes measure realised and near-term implied volatility in listed equity markets, which is precisely the segment that absorbs isolated shocks most efficiently. Structural risks in private credit, sovereign debt, and geopolitics build without producing immediate volatility spikes. That is why cross-asset monitoring, tracking credit spreads, term premia, and commodity prices alongside equity data, is the more reliable diagnostic tool. Relying on equity volatility alone in this environment is monitoring the last instrument that will sound the alarm.

The ECB’s modelling of European private credit exposure illustrates the cross-market spillover mechanism: a severe shock in private credit segments generates second-round losses through equity portfolio revaluations that can exceed the initial direct credit hit, a dynamic that operates well before equity volatility indexes register any signal.

The next major ASX story will hit our subscribers first

Positioning for a market that rewards careful reading

The current environment is not an obvious bear case. Nor is it an obvious bull case. Morningstar Australia’s Q3 2026 US equities outlook characterises the market as one where risks are evenly weighted and opportunities exist on a sector-by-sector basis, rather than through broad participation. Several other large research providers use comparable language.

That symmetry favours selectivity over momentum-driven broad-index positioning. In practical terms, five positioning disciplines are consistent with the analytical framework developed across this analysis, ranked in priority order:

- Reassess concentration risk. Review your exposure to the narrow AI-linked leadership cohort. If your portfolio’s performance is tracking the index only because of those same few names, you are carrying the same concentrated risk the index is carrying.

- Prioritise forward guidance over backward-looking beats. The information content in the current earnings cycle sits in the revision trajectory, not in the historical comparison.

- Treat rallies as review moments. Positive price action in a fragile environment is a prompt to rebalance, not a signal to add broad exposure.

- Monitor cross-asset signals. Credit spreads, term premia, currency moves, and commodity prices are providing more reliable early-warning information than equity volatility alone.

- Maintain liquidity. Preserving optionality to act during volatility has a higher expected value than being fully invested in a symmetric risk environment.

Institutional consensus suggests that elevated US large-cap valuations leave limited upside relative to risk in AI-adjacent segments, while select non-US markets and value-tilted or income-oriented segments offer comparatively more attractive risk-reward.

For investors wanting to convert this analytical framework into concrete portfolio actions, our comprehensive walkthrough of portfolio crisis preparation covers the four specific steps, including sizing a liquidity buffer and running a written drawdown stress test, that improve resilience regardless of whether a downturn arrives.

The conditions that characterise a fragile rally, positive headline performance and recent price momentum, are precisely the conditions that most reliably suppress the alertness needed to respond to it.

The behavioural dimension is the hardest part. Narrative consistency, the tendency to interpret new information in ways that confirm an existing market story, is particularly dangerous when concentrated leadership means most market experience for most participants is positive. The discipline of trimming and rebalancing on rallies has a higher expected value than it intuitively feels like in the moment. Recognising that is the first step toward acting on it.

What changes and what does not when the narrative shifts

Headline index performance and underlying structural fragility can coexist for extended periods. That has been the defining feature of mid-2026, and the inability to predict timing does not reduce the value of understanding the conditions. The diagnostic shift this analysis argues for, from backward-looking earnings and index levels as the primary inputs toward forward guidance quality, cross-asset stress signals, and concentration monitoring, remains the more information-rich framework regardless of which direction the next move takes.

You are now better placed to hold the contradictory evidence simultaneously: a market at new highs and a market where the foundation beneath those highs is narrower and more assumption-dependent than the headline suggests. That is not a comfortable position, but it is an honest one, and honest readings are what protect capital when the narrative eventually shifts.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

—