Delivery Hero Shareholders Reject Uber’s €33 Bid, Demand €40+

10 mins ago

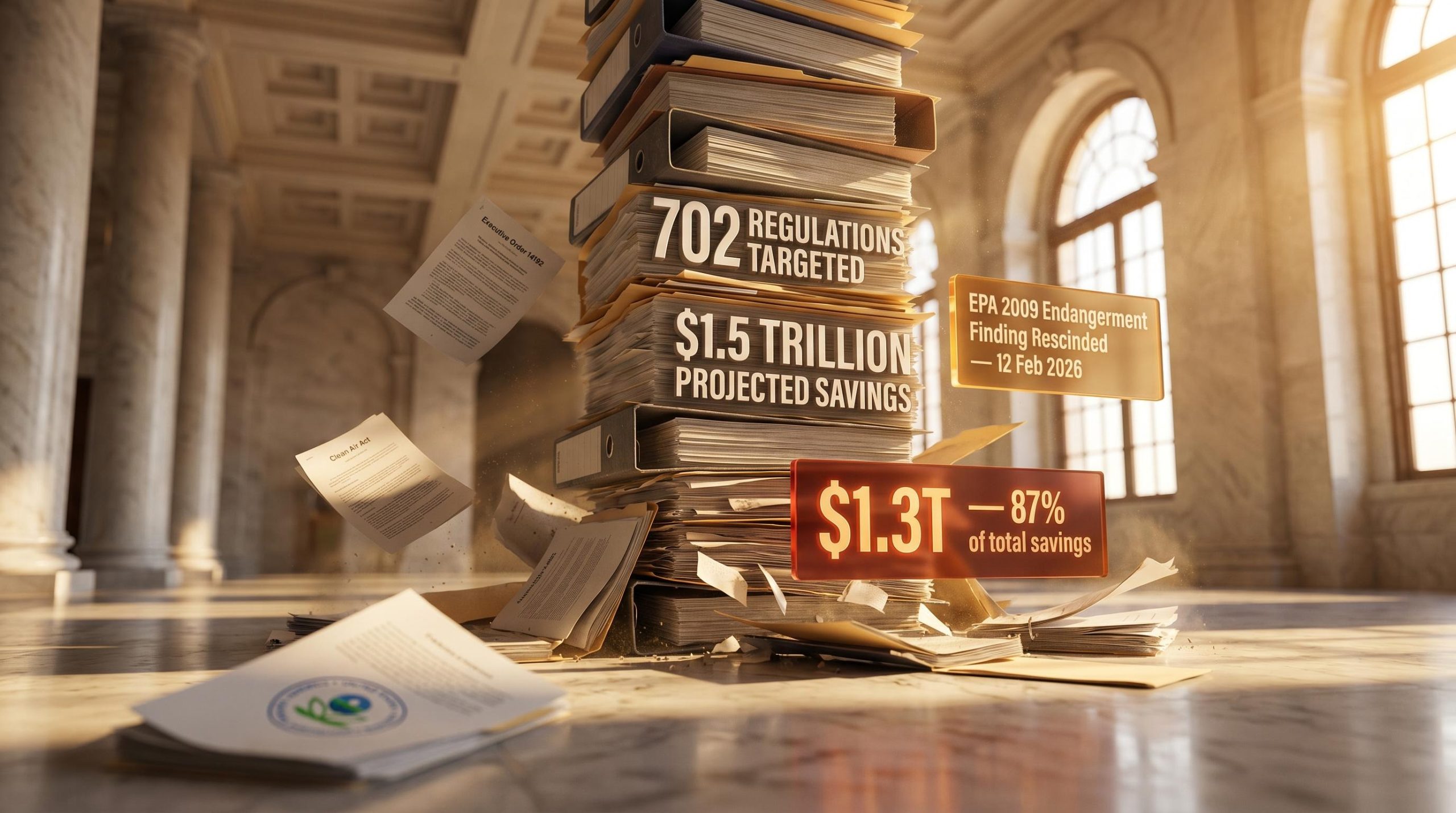

On Independence Day, the Trump administration revealed an ambitious deregulatory agenda targeting 702 federal regulations for elimination, with projected economic savings of up to $1.5 trillion before the end of the fiscal year in September. More than $1.3 trillion of that total traces to a single action: the February rescission of the EPA’s 2009 endangerment finding.

The scale here is structurally significant, not just political. The endangerment finding was the legal foundation for decades of federal greenhouse gas regulation, covering vehicle emissions, power plant limits, methane rules, and cross-sector climate policy. Its removal does not simply reduce one agency’s workload; it strips the statutory anchor from a wide range of rules built on top of it. Businesses and investors now face a period where compliance costs are falling sharply on paper, but the regulatory ground beneath those projections is actively contested in federal appellate courts.

Here is what is actually in the 702-rule proposal, why the EPA rescission dominates the numbers, where the savings projections fall short as a decision-making tool, and what the near-term and long-term implications look like by sector.

Bloomberg reports that the 702 proposed eliminations set a new high-water mark for deregulatory scope within a White House semiannual regulatory agenda, surpassing any previous such package. The categories of rules put forward for repeal include:

These are proposals, not outcomes. Each must clear formal rulemaking, public comment periods, and potential judicial review before taking effect. For anyone tracking regulatory risk, the 702 figure is the opening bid of a multi-step legal and administrative process, not a completed rollback.

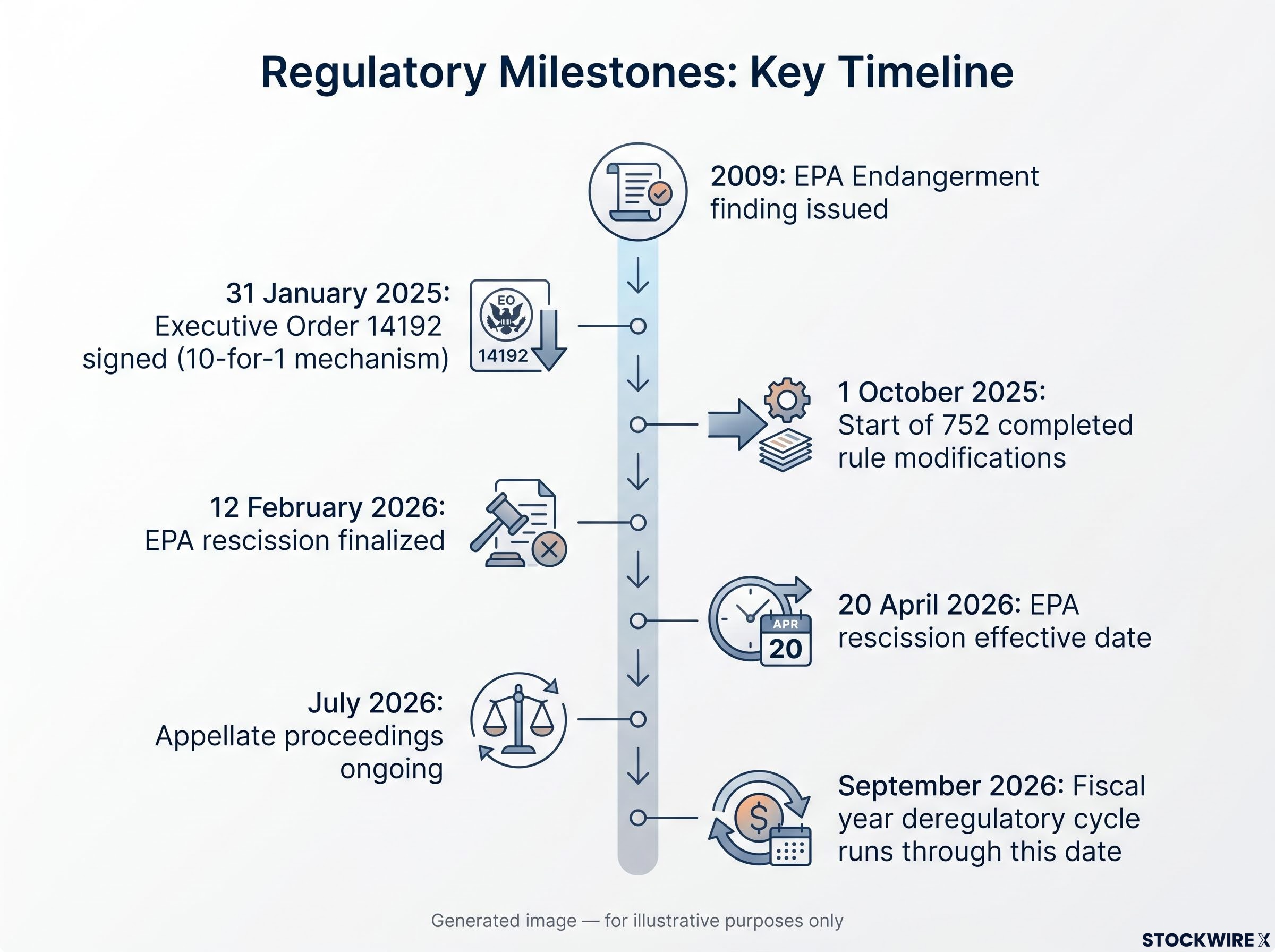

A further 752 rule modifications had been brought to completion prior to this announcement, having been finalised or fully executed since 1 October 2025, which means the current package sits within a broader pattern of ongoing regulatory activity rather than representing an isolated event.

The deregulatory push operates under Executive Order 14192, signed 31 January 2025, which requires ten existing regulations removed for every new rule adopted. Hundreds of actions under this directive have delivered over $200 billion in estimated savings for fiscal year 2025.

Executive Order 14192, published in the Federal Register on 6 February 2025, establishes the 10-for-1 deregulatory requirement as a standing policy directive, meaning each future regulatory cycle will continue generating new elimination proposals until a subsequent administration revokes or modifies the order.

The 702 count is not a one-time event. It is the current cycle’s output of that standing policy. Future regulatory cycles will continue generating deregulatory proposals, which means the 702 is an instalment, not a ceiling.

The 2009 endangerment finding was issued under the Clean Air Act following the Supreme Court’s Massachusetts v. EPA decision. It established that greenhouse gases endanger public health and welfare, and it became the legal predicate for every subsequent federal GHG regulation. Vehicle emissions standards, power plant and industrial limits, methane rules for oil and gas, cross-sector climate guidance: all of it was built on this single finding.

The EPA rescinded the finding on 12 February 2026, with an effective date of 20 April 2026.

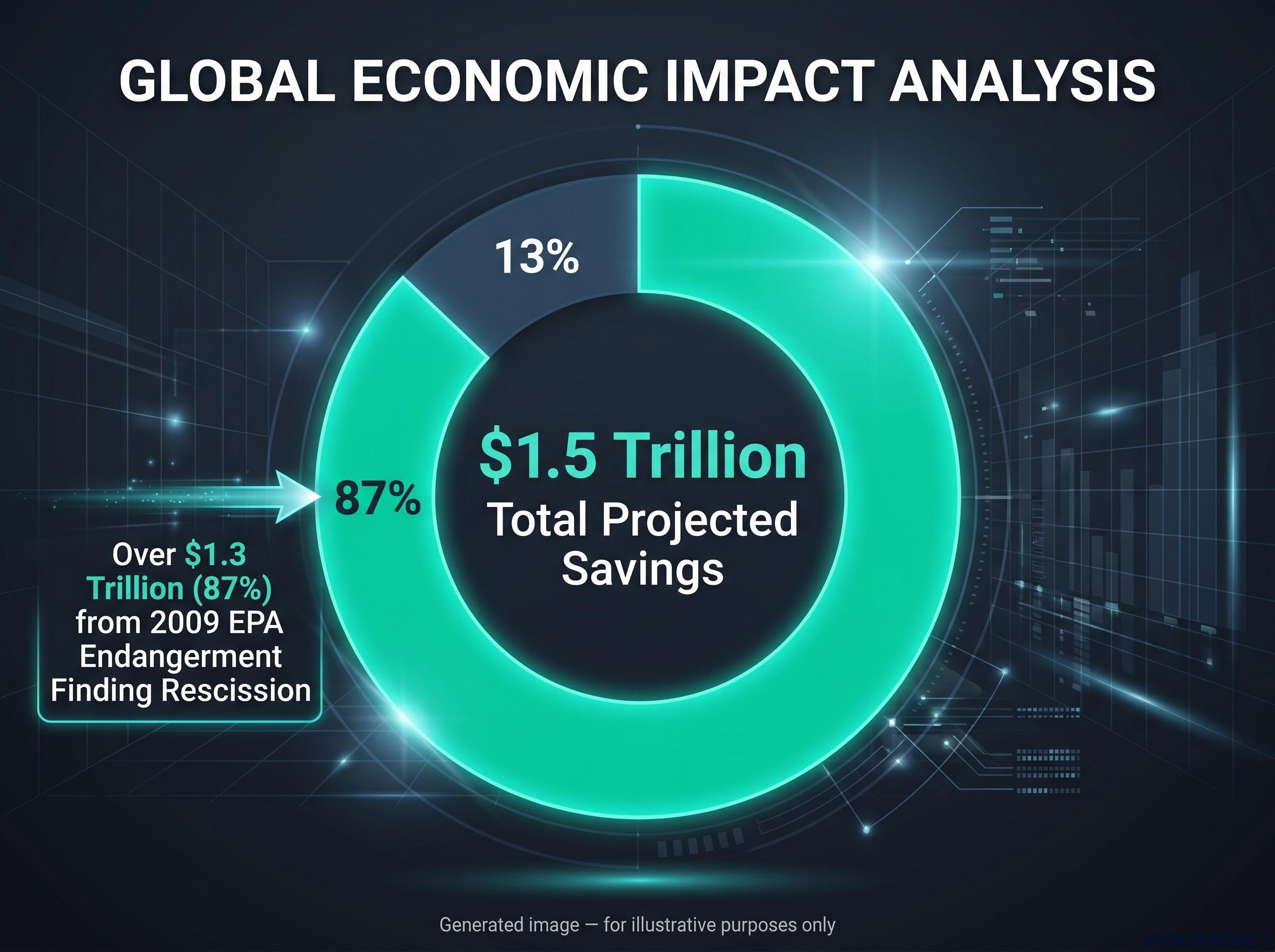

The EPA estimates the endangerment finding rescission alone saves over $1.3 trillion, representing the dominant share of the administration’s total $1.5 trillion savings projection.

Because so many downstream rules were legally anchored to this one finding, its removal does not just cut one regulation. It creates uncertainty across an entire architecture of environmental compliance. The categories now weakened or stripped of their statutory basis include:

For investors in energy, industrial, and transportation sectors, understanding that 87% of the administration’s savings claim rests on a single, actively litigated action is the most important context for weighting those projections.

The $1.5 trillion figure is a cost-side number only. It measures reduced compliance and capital expenditures for regulated entities. It does not represent a net economic benefit.

Standard regulatory analysis compares compliance costs against quantified benefits: avoided premature deaths, reduced illness, climate damage averted, and consumer efficiency savings. The administration’s estimate omits that entire side of the ledger. The accurate interpretation is that this is a cost-shifting exercise, where burdens move from regulated businesses toward households, governments, and future economic output, rather than a creation of free economic value.

| What the $1.5 trillion counts | What it omits |

|---|---|

| Reduced compliance costs for regulated industries | Economic value of avoided premature deaths and illness |

| Lower capital expenditure on emissions controls | Climate damage costs shifted to households and governments |

| Reduced reporting and documentation burdens | Consumer savings from energy efficiency standards |

| Faster permitting timelines for energy projects | Litigation exposure and reinstatement risk for businesses |

For any investor using the $1.5 trillion headline to project sector earnings upside, the correct adjustment is to treat it as a gross compliance cost reduction with an offsetting, unquantified liability side that includes litigation exposure, physical climate risk, and the cost of potential future reinstatement.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

| Sector | Near-term benefit | Primary risk |

|---|---|---|

| Energy, oil and gas, pipelines | Faster permitting, lower compliance costs, extended asset life for higher-emitting facilities | Policy whiplash if a future administration reinstates rules; ESG financing pressure from large asset managers |

| Utilities and power generation | Carbon-intensive generators (coal, older gas) gain breathing room from reduced retirement pressure | Renewable developers lose regulatory tailwind; utilities doubling down on fossil without a transition hedge face long-term stranding risk |

| Automotive and transportation | Weakened legal backing for fuel economy standards lowers near-term compliance costs | OEMs have already invested heavily in EV platforms; global markets (EU, China) still demand lower emissions, limiting strategic reversal |

| Industrials and manufacturing | Improved capex flexibility and margins from rolled-back efficiency mandates | Higher energy use increases operating costs if fuel prices rise or carbon pricing returns in any form |

The deregulatory regime creates a divergence trade. Companies that can generate cash under loose rules while remaining viable under tighter future rules are structurally better positioned than those whose business models only function at the current regulatory minimum. That distinction matters for portfolio construction: sector exposure to this cycle is highly uneven, and the near-term margin benefit in some industries carries tail risks that are not yet priced into current valuations.

These statements involve forward-looking projections and are subject to change based on market developments, regulatory outcomes, and company performance.

The endangerment finding rescission was finalised on 12 February 2026 with an effective date of 20 April 2026, but it faces active appellate litigation. The 702 proposed rule eliminations remain at the proposal stage, each requiring formal rulemaking, public comment, and potential judicial review.

The appellate risk surrounding the endangerment finding rescission sits within a broader pattern of judicial limits on executive authority: federal courts have already dismantled the broadest statutory pillars of executive tariff power within a single three-month window, demonstrating that the administration’s unilateral regulatory toolkit is actively being tested and narrowed by the courts.

Three outcomes are possible for the endangerment finding challenge:

Regardless of which federal outcome prevails, some states are already tightening their own environmental rules in response to federal rollbacks, creating a patchwork regulatory environment that multi-state businesses cannot plan around by assuming uniform deregulatory relief. This state-level floor persists no matter what the appellate courts decide.

For companies making capital allocation decisions on the assumption that today’s deregulatory environment is durable, the appellate timeline and state-level patchwork represent the variables that should be stress-tested before committing long-horizon capex.

The administration’s $1.5 trillion projection is best treated as an upper-bound scenario that requires three legal and political conditions to be maintained simultaneously: appellate courts upholding the endangerment finding rescission, states declining to fill the regulatory gap, and the 2026 and 2028 electoral cycles producing continuity. A planning framework that hedges against partial delivery is more durable than one that banks the full savings.

The practical directives split cleanly between corporate operators and investors:

The investment quality signal in a deregulatory cycle is this: companies that can operate profitably under both stricter and looser regulatory regimes represent structurally stronger positions than those whose models only work at the current regulatory minimum.

Appellate proceedings are ongoing as of July 2026. The fiscal year deregulatory cycle runs through September 2026. The window for action is open, but the ground beneath it is still moving.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Trump administration unveiled a plan to eliminate 702 federal regulations, projecting economic savings of up to $1.5 trillion before the end of fiscal year September 2026, operating under Executive Order 14192 which requires ten regulations removed for every new rule adopted.

The 2009 endangerment finding was the legal foundation for all federal greenhouse gas regulation, covering vehicle emissions, power plant limits, and methane rules; its rescission in February 2026 eliminates the statutory anchor for an entire architecture of compliance requirements, which the EPA estimates saves over $1.3 trillion on its own.

It measures only reduced compliance and capital expenditure costs for regulated businesses; it does not account for the offsetting economic value of avoided premature deaths, climate damage costs shifted to households, consumer savings from efficiency standards, or litigation and reinstatement risk.

Energy, oil and gas, pipelines, and carbon-intensive power generators see the most immediate near-term relief from lower compliance costs and faster permitting, while automotive OEMs face limited strategic reversal given prior EV investment and global emissions demand, and all sectors carry tail risk if appellate courts overturn the endangerment finding rescission.

Yes; the endangerment finding rescission faces active appellate litigation and could be upheld in full, narrowed in scope, or struck down entirely, which would force businesses that assumed permanent rollback to absorb sudden re-compliance costs, and several states are already tightening their own environmental rules regardless of the federal outcome.