How to Choose Between VAS and A200 for Your Portfolio

Jul 1, 2026

Most investors spend their careers hunting for the next ten-bagger. They scan newsletters, follow fund managers on social media, and wait for the next hot tip. What they rarely do is examine the eight unglamorous disciplines that separate managers who actually compound at 20% annualised from those who merely talk about it.

Ben and Luke of Senica Financial Solutions are small-cap, ASX-focused practitioners who report approximately 20% annualised returns since inception. Their lessons are not academic theory. They are practitioner-derived, and most of them run against the grain of standard retail investing advice.

Here is the framework, reconstructed from their experience, that you can apply to your own process starting now.

Most small-cap commentary is a blend of verifiable data and salesmanship. The professional edge is knowing which is which in real time, not after the price has already moved.

The hierarchy matters. Not all sources carry equal weight, and ranking them changes the quality of every decision downstream:

Your information diet is the single most controllable variable in your edge. Switching from secondary commentary to primary documents is a free upgrade available right now, and it costs nothing but attention.

The ASX announcement feed is the foundation of disciplined small-cap stock research, delivering primary source material before any newsletter or podcast adds interpretation; fund manager monthly reports and broker summaries are, by the time they reach you, a lagging record of conclusions someone else drew from documents you could have read directly.

Consider the Vulcan Energy Resources example. Senica took an early-stage placement at approximately 40 cents per share, partly on the strength of observing founder Francis’s authentic behaviour in unscripted contexts outside formal investor presentations. That kind of management assessment does not show up in broker notes. It comes from prioritising primary observation over polished pitch decks.

By the time an investment idea appears in a newsletter or fund manager monthly report, you are already late. The edge erodes in the gap between the original insight and the published commentary. That is not a quality problem. It is a timing problem.

The route back to being early runs through specific primary-source behaviours:

Senica identified a special dividend opportunity by reading management incentive structures in company announcements to determine probable timing. That insight was simply unavailable to anyone relying on secondary sources.

Every hour you spend reading another manager’s monthly report is an hour not spent reading the underlying ASX announcement that manager read six months ago. The maths on that trade-off is not close.

Optionality accumulates in low-expectation environments. The situations most investors filter out are precisely where asymmetric access to information and relationships tends to emerge.

Ben and Luke’s professional partnership itself began at a broker presentation that neither expected to be worthwhile. A seemingly unproductive lunch turned into the foundation of a firm reporting 20% annualised returns.

The principle extends directly to stock selection. Unloved sectors, thinly attended roadshows, and low-multiple names are the structural equivalent of that low-expectation meeting. Your filter for “worth attending” is almost certainly set too high. The next meaningful opportunity is more likely to come from a situation you almost skipped than from one you were excited about.

Most retail investors screen for conviction before committing time. This lesson inverts that logic: the commitment of time without certainty of return is itself the edge-generating behaviour.

This is the single most psychologically difficult skill in small cap investing, and no amount of reading about it replaces the experience of living through it.

The distinction is conceptually simple. Price pain means the position is down but the thesis remains intact. Thesis failure means the facts have changed or the original assumptions are broken. In practice, telling them apart during a drawdown is brutally hard.

| Company | Adverse price move | Outcome |

|---|---|---|

| Mineral Resources | ~$70 to ~$15 | Recovered to ~$60-$70 |

| HMC Capital | Peak above $10, fell to ~$2.50 (below co-investment and NTA value) | Medium-term target of $6-$8 |

| Arcadium Lithium | Held through broadly negative lithium sentiment | Acquired by Rio Tinto at a significant premium |

James Carse’s finite versus infinite games framework applies directly here. The objective is not to win or lose on any single position. It is to remain continuously active in the game. Selling a position because the price hurts, when the thesis remains intact, takes you out of the game permanently on that name.

The practical discipline is specific: write down your original thesis with explicit invalidation criteria before you buy. That is the only reliable way to distinguish price discomfort from genuine thesis failure in the heat of a drawdown.

Maintaining conviction through a drawdown requires more than belief in the thesis; it requires a pre-written document that specifies, before the price falls, exactly which facts would invalidate your original investment case, because in the heat of a multi-month decline that document becomes the only reliable separation between disciplined reassessment and panic.

Being roughly right on the key drivers beats being precisely wrong on dozens of minor inputs. This lesson has a cost attached to learning it the hard way.

| Company / asset class | Key variable | Lesson |

|---|---|---|

| Promedicus | Misidentified; detailed model at ~$310 did not prevent stock trading to ~$120 | Precision without correct variable identification is expensive |

| XRF Scientific | Sample volume trends in the most profitable division | One metric can be the entire monitoring framework |

| REITs (as a class) | Prevailing interest rate direction | Macro variables can overwhelm fundamental modelling entirely |

The Promedicus case is instructive because the analyst’s model was both thorough and granular, yet the stock fell from around $310 to around $120 regardless. The model failed not through lack of effort but because it was anchored to the wrong drivers. Getting the key variables right matters far more than the sophistication of the surrounding analysis.

Your next investment review task is not adding more model inputs. It is removing them. Name the one to three variables that will determine whether your thesis is right, and monitor only those.

Once the research work on a high-conviction thesis is done, that cost is largely fixed. Finding additional vehicles to express it raises the return on that fixed cost, and the range of available expressions is wider than most investors realise:

A royalty structure lets you capture revenue-linked upside on an underlying asset without taking on the operator’s balance sheet or leverage risk.

Red Hill Minerals holds a royalty over a project associated with Mineral Resources, providing revenue-linked exposure without the leverage risk of the operating company. Digico Infrastructure REIT, listed at approximately $5.00 per unit and subsequently trading at approximately $2.40, was cited as a potential catalyst opportunity. HMC Capital was identified as the preferred vehicle for a broader thesis encompassing Home Co Daily Needs REIT, HCW, and Digico, with nuanced views held on each component.

ASX REIT valuation through a five-test framework, covering stress-tested net tangible assets, yield spread, price-to-FFO versus peers, implied cap rate against transaction evidence, and a balance-sheet filter, is the analytical layer that distinguishes a genuinely mispriced vehicle from one that is cheap because writedowns are pending.

Take your single strongest current conviction and list every ASX-listed vehicle that provides exposure to the same underlying thesis. Identify which expressions you hold and which you are missing.

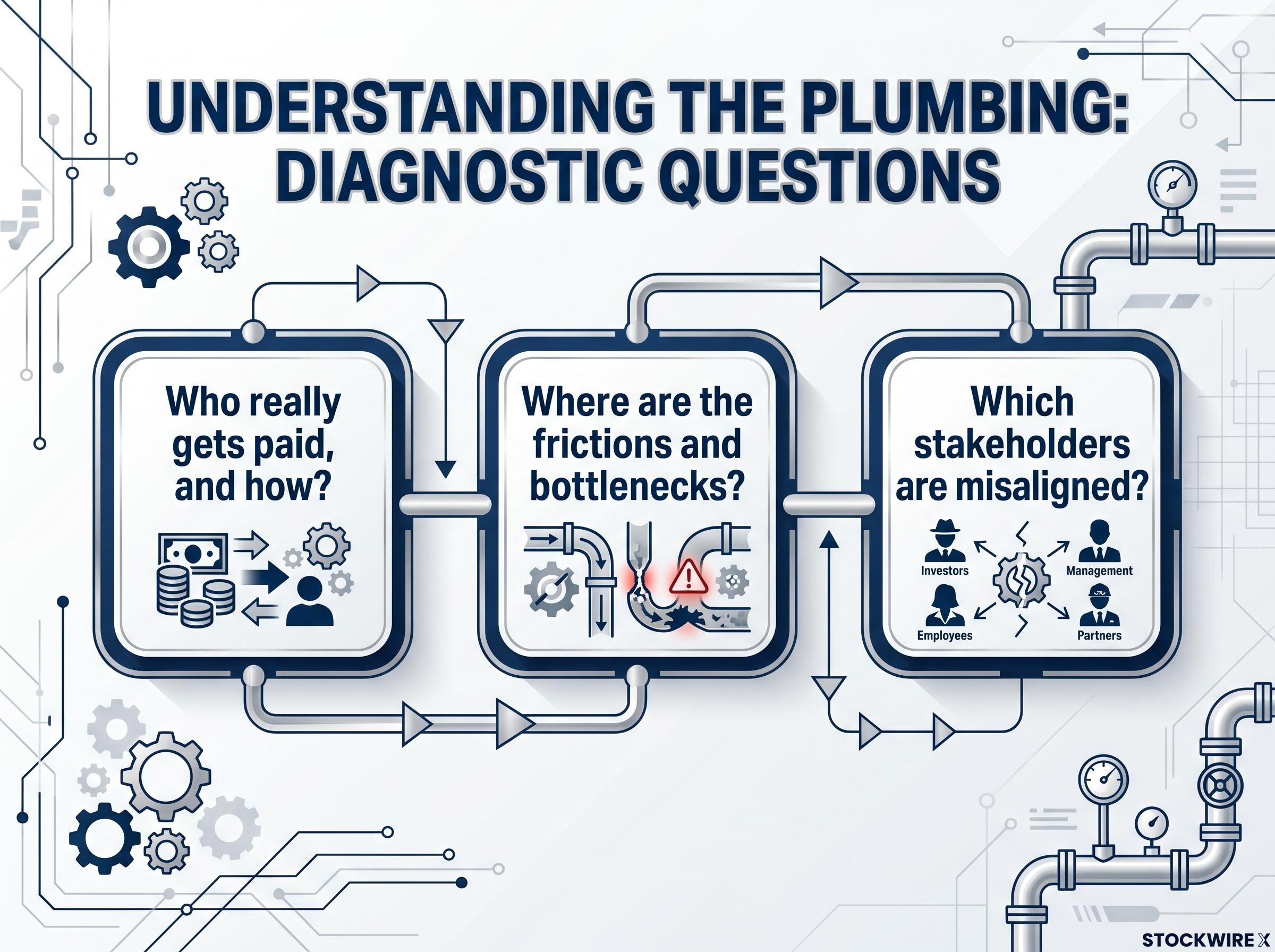

A colleague identified as JB originally called this “understanding the plumbing,” and the metaphor is precise. Mapping the full chain, from share issuance through custodial ownership, from revenue through to cashflow, from regulation through to incentives, reveals mispricings that surface-level analysis cannot surface.

The diagnostic questions are specific and repeatable:

Few practitioners can walk through the full mechanics of a share transaction, from the moment a company issues shares all the way through to how they sit inside a custodial arrangement. Investors who can trace that chain see structural features that everyone else cannot. Larger financial advice businesses can develop incentive misalignments as a byproduct of regulatory and administrative complexity, and structural understanding is what makes those misalignments visible.

Add those three diagnostic questions to every investment review. They turn management assessment from an art into a repeatable analytical process, and they surface risks that earnings models alone will miss.

Reverse-engineering a famous fund manager’s portfolio is not a strategy. It is a set of positions without a thesis. Successful investors operate from professional backgrounds, networks, and temperaments that are not transferable. Imitation lacks the foundational context that produced their results.

Ophir Asset Management, managing in excess of $1 billion across a closed-end fund and a listed vehicle trading under the ticker OP, is a useful calibration reference for what differentiated positioning at scale looks like. But it is a reference, not a template.

The structural small-cap quality dynamics shaping ASX-adjacent markets deserve attention before building a small-cap process, because broad passive index exposure systematically dilutes the size premium by including unprofitable and speculative names, and the AQR research cited across global markets confirms the premium is real but concentrated in higher-quality businesses.

The practical audit is specific: map your genuine strengths (sector familiarity, professional background, pattern recognition, temperament under stress) and design a process that fits those strengths. Ben and Luke cite their frequent internal disagreement as a deliberate and productive feature of their process, not a weakness. That is temperament-aligned process design.

Before adopting any element of another manager’s approach, check whether the underlying conditions that make it effective for them are actually present in your own situation. If they are not, you inherit the method without the structural advantages that make it work.

If the answer is no, the imitation carries the liability without the structural advantage that made the original work.

Four structural themes run through all eight lessons, and they reinforce each other:

These are not a checklist to tick off individually. They are a compounding system. Practitioners who apply all four simultaneously have a different quality of process than those who apply one or two in isolation.

The lessons are practitioner-derived from ASX small-cap experience specifically. For Australian retail and self-directed investors, they are directly applicable without translation. The question is not whether the framework makes sense. It is whether you will do the work.

Morningstar analysis of ASX small-cap returns against the S&P/ASX 200 benchmark shows the small-cap premium in Australia is real but historically inconsistent, confirming that the process discipline described throughout this framework is what separates practitioners who capture it from those who do not.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Nothing in this article constitutes financial advice.

—

Small cap investing on the ASX involves buying shares in smaller listed companies that typically have higher growth potential but also greater volatility than large-cap stocks; the small-cap premium in Australia is real but historically inconsistent, meaning process discipline is what separates investors who capture it from those who do not.

Price pain means the position is down but your original investment case remains intact, while thesis failure means the underlying facts have changed or your original assumptions are broken; the most reliable way to distinguish them is to write down explicit invalidation criteria before you buy, so you have a pre-written document to consult when the price falls.

By the time an investment idea appears in a newsletter or fund manager monthly report, the original insight has already been acted on by earlier readers; reading ASX announcements as they are released puts you at the top of the information hierarchy and allows you to form your own thesis before the interpretation layer is added.

Expressing a thesis across multiple vehicles means identifying every ASX-listed instrument, including operators, royalties, REITs, and adjacent beneficiaries, that provides exposure to the same underlying idea, so the fixed research cost generates returns across more than one position; Red Hill Minerals holding a royalty over a Mineral Resources-associated project is a concrete example of this approach.

The goal is to name the one to three factors that will determine whether your thesis is correct and monitor only those, rather than building increasingly complex models; the Promedicus case illustrates the risk of precise modelling anchored to the wrong drivers, with the stock falling from around $310 to around $120 despite a thorough detailed model.