ASX Sector Rotation: Why FY25 Leaders Became FY26’s Worst

4 mins ago

Australia’s financial system was deliberately subjected to more stress than it has experienced in half a century of banking history. Not because regulators feared an imminent collapse, but because they needed to see what happens when banks and superannuation funds pull against each other at the same moment.

The Australian Prudential Regulation Authority’s (APRA) 2025 cross-sector stress test was the first exercise of its kind in this country, covering the four major banks and six large superannuation funds simultaneously. Superannuation has grown into a force capable of both stabilising and destabilising the financial system, depending on how funds behave under pressure. Regulators needed evidence of which way it would go.

Here is what the results actually found, where the fault lines sit, and what it all means for the safety of Australian deposits and retirement savings. The system held up. It also revealed specific vulnerabilities that will not fix themselves, and your super fund’s behaviour in a crisis now matters to the entire economy.

APRA has historically tested banks and super funds in isolation. The 2025 exercise changed that, marking the first time both sectors were tested together in a single integrated scenario. The aim was not to pass or fail individual institutions on their capital buffers; it was to observe how their behaviours interact when everything goes wrong at once.

The scenario combined three simultaneous stressors:

The scenario subjected banks to funding pressures beyond anything their large Australian counterparts had faced across the prior 50 years. For superannuation funds, the modelled member outflows and switching activity were substantially more severe than what the sector recorded during the COVID-19 period.

Ten institutions participated: the four major banks and six large super funds, representing approximately 70 per cent of the banking industry and 45 per cent of APRA-regulated superannuation funds. The exercise assumed no change in government policy or exceptional support.

This was an exploratory scenario, mirroring system-wide exercises used by the Bank of England. Phase 1 findings were published on 20 November 2025. Phase 2 results are due by mid-2026.

The severity of the scenario is the point. APRA was not testing for likely conditions but for extreme ones. That makes the resilience finding more meaningful, and the remaining vulnerabilities far more telling.

Confidence-sensitive funding dynamics are not new to financial crises: the Panic of 1907 demonstrated that a contained loss in a single commodity trade could cascade into system-wide collapse precisely because trust companies relied on short-duration, confidence-dependent funding with no central backstop, a structural parallel to the liquidity amplification the 2025 stress test was specifically designed to stress.

Every one of the 10 participating institutions proved capable of honouring their financial commitments and rebuilding their liquidity buffers throughout the scenario. For depositors and superannuation members, the headline is genuinely reassuring: in APRA’s modelled crisis, the institutions holding your savings did not fail.

That reassurance, though, has limits.

The same exercise that confirmed resilience simultaneously exposed structural fault lines that do not disappear simply because the scenario stopped short of institutional failure. APRA identified four specific categories of vulnerability:

Both sectors were found to require further investment in their stress-testing frameworks. APRA-supervised institutions collectively hold approximately $9.8 trillion in assets on behalf of depositors, policyholders, and superannuation members. The fault lines identified tell you where future stress could be most damaging if these gaps are not addressed before the next real shock arrives.

Superannuation balance benchmarks contextualise what is at stake in the regulatory discussion: the average Australian aged 50-54 holds approximately $198,400, already more than $430,000 below the ASFA comfortable retirement threshold, meaning any amplification of losses through poor crisis-period behaviour lands on a member cohort with limited runway to recover.

Superannuation now accounts for a large and growing share of Australia’s financial system. A small number of very large funds wield significant influence over markets and counterparties. APRA Chair John Lonsdale has noted that as superannuation’s share of the financial system continues to grow, gaining a clearer picture of how funds are likely to behave during severe stress, and the knock-on effects those decisions could have on other parts of the system, has become a central regulatory concern.

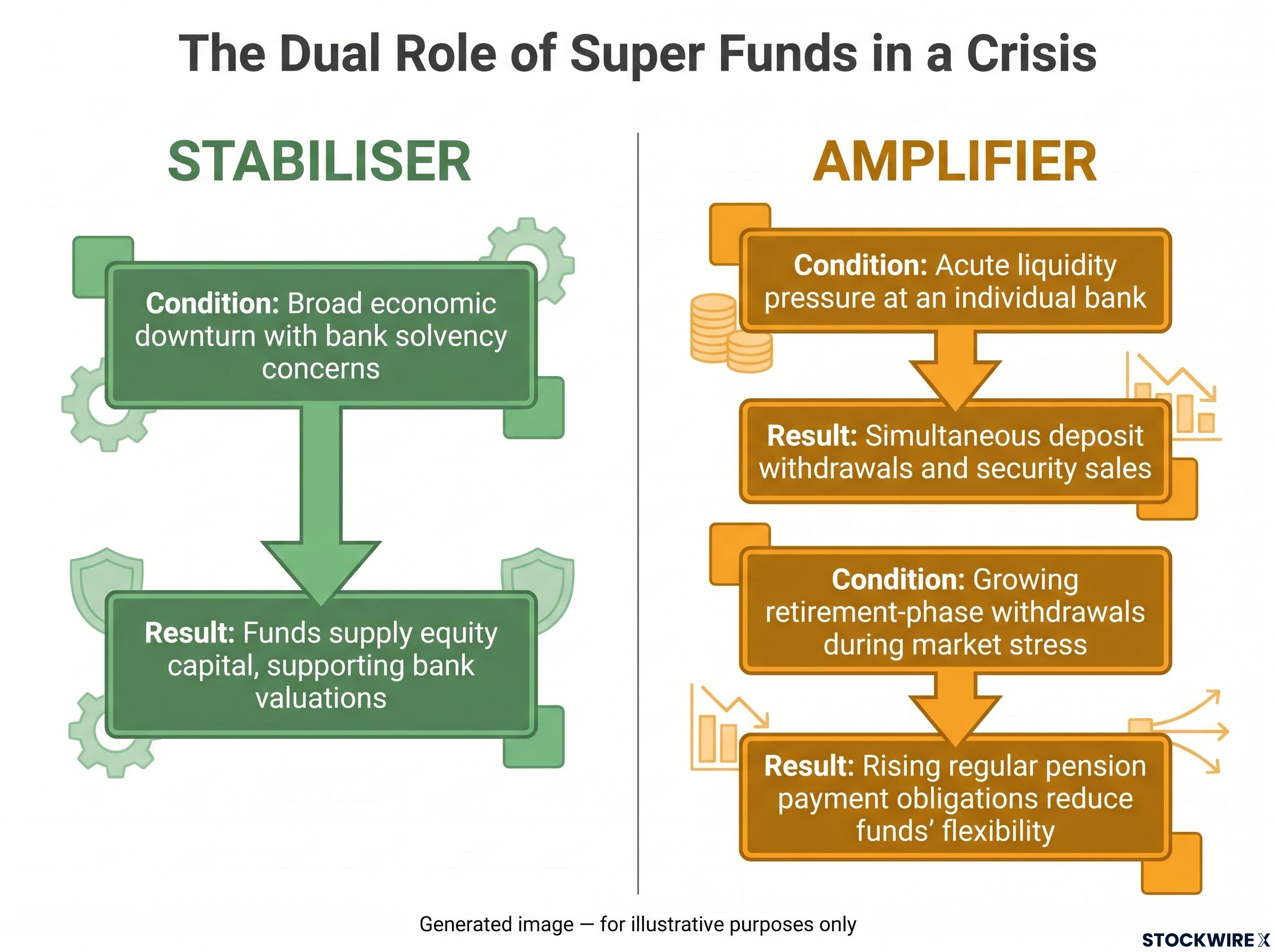

The complication is that super funds play two opposing roles under stress, and which one dominates depends entirely on the nature of the crisis.

During periods of broad economic deterioration and bank solvency stress, large super funds can serve as a source of equity capital when other investors withdraw. Their long investment horizons allow them to absorb bank shares that shorter-term investors are offloading, which helps to steady bank valuations and reduce the spread of systemic risk.

When a single bank comes under intense liquidity pressure, the dynamic reverses. When numerous super funds each independently reduce their exposure to that bank, through deposit withdrawals or security sales, those individually cautious decisions combine to deepen the institution’s funding difficulties. Each fund is acting prudently. The aggregate effect is destructive.

| Stress condition | Super fund role |

|---|---|

| Broad economic downturn with bank solvency concerns | Stabiliser: funds supply equity capital, supporting bank valuations and containing systemic risk |

| Acute liquidity pressure at an individual bank | Amplifier: simultaneous deposit withdrawals and security sales by multiple funds intensify the bank’s funding crisis |

| Growing retirement-phase withdrawals during market stress | Amplifier: rising regular pension payment obligations reduce funds’ flexibility to maintain exposures |

When members move from the accumulation phase into retirement, funds face growing obligations to pay pensions regularly and meet higher volumes of withdrawals, which shifts their liquidity profile away from patient, long-term investing toward a schedule of ongoing outflows. That shift means your fund’s crisis-response behaviour now carries consequences well beyond your own account balance, extending to the stability of the banks holding your mortgage or savings.

The cross-sector design surfaced something that no single-sector stress test could: the crisis plans of banks and super funds are, in specific scenarios, directly contradictory.

Some banks’ internal stress models assumed that large super funds would maintain their funding and deposits through a shock. Those same super funds had plans to reduce their exposures to stressed institutions in the very same scenario.

This mismatch is not a marginal finding. It is a structural gap. If a bank’s liquidity planning assumes counterparty funding will hold steady, and the counterparty’s own risk framework dictates withdrawal, the bank’s actual resilience is weaker than its internal models suggest.

APRA flagged this divergence in behavioural assumptions as a central finding, observing that as the financial system grows more interconnected, actions taken within one sector can ripple through to institutions in other sectors and to the service providers they share. The cross-sector methodology was specifically designed to surface these discrepancies.

The implication is direct: the financial system’s resilience depends not just on what individual institutions hold in reserve, but on whether their crisis plans are compatible with each other. Being well-capitalised individually is insufficient if your counterparties’ plans are pulling in the opposite direction from your assumptions.

APRA has signalled that the stress test findings will drive concrete policy changes, not just supervisory guidance. The three reform tracks, in order of immediacy, are:

Shared service provider risk extends beyond the operational disruption scenario modelled in the 2025 test: APRA’s April 2026 supervisory letter identified AI vendor concentration across banks, insurers, and superannuation trustees as a distinct externally-originating threat, where a failure cascading through a dominant provider could simultaneously impair fraud detection, credit decisioning, and compliance monitoring across multiple institutions.

APRA indicated it would take proposed bank liquidity amendments to public consultation within 12 months of the November 2025 System Risk Outlook, a concrete timeline that signals the urgency regulators attach to these findings.

Phase 2 results, due mid-2026, will extend the analysis further. For savers, the regulatory response is itself a signal: APRA considers these vulnerabilities serious enough to require structural rule changes, which is the most direct evidence that the fault lines identified are material, not theoretical.

The test confirms something meaningful. Australia’s major banks and large super funds held up under a scenario more severe than any real-world shock the banking system has faced in half a century. Operating without any assumed government support, every one of the 10 institutions demonstrated it could honour its obligations and rebuild its liquidity position. That is a result worth acknowledging.

What the test does not change is equally important:

Phase 2 results, due mid-2026, and the regulatory consultation process already underway represent the next observable signals for anyone following this space. APRA’s framing is clear: resilience will increasingly hinge on cross-sector coordination, liquidity management, and operational planning, not just the capital buffers of individual institutions.

The 2025 cross-sector findings confirm resilience against domestically-generated shocks, but imported systemic risks from geopolitical transmission channels and offshore private credit exposures operate through pathways that domestic scenario design was not built to fully stress, a distinction APRA’s May 2026 System Risk Outlook makes explicit.

The $9.8 trillion in APRA-supervised assets is a reminder of the scale at stake. The stress test result is not a clearance certificate for the financial system. It is a calibration point, showing where the system is strong and, more precisely, where it is not.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The APRA stress test is a regulatory exercise designed to assess whether financial institutions can withstand severe economic shocks. The 2025 cross-sector version was Australia's first to test banks and superannuation funds simultaneously, covering the four major banks and six large super funds across three combined stressors: severe market deterioration, intense liquidity outflows, and an operational disruption at a major shared third-party service provider.

All 10 participating institutions demonstrated they could honour their financial commitments and rebuild liquidity buffers throughout the scenario, which was more severe than any real-world shock Australian banks have faced in 50 years. However, APRA simultaneously identified four structural vulnerabilities, including liquidity amplification dynamics and behavioural mismatches between sectors, that the result does not eliminate.

When a bank faces acute liquidity pressure, multiple super funds independently reducing their exposure to that institution through deposit withdrawals or security sales can collectively deepen the bank's funding crisis, even though each fund is acting prudently in isolation. This amplification effect is the opposite of the stabilising role super funds play during broad economic downturns, where their long investment horizons allow them to absorb bank shares that shorter-term investors are offloading.

APRA announced a public consultation in March 2026 on proposed enhancements to bank capital adequacy and liquidity requirements, including consideration of a new Pillar 2 liquidity framework, committing to put these changes out for consultation within 12 months of the November 2025 System Risk Outlook. Supervisory activities targeting super fund stress-testing capability and liquidity management will also increase, and shared service provider risk is now treated as a systemic concern requiring cross-sector operational resilience standards.

The test result is reassuring at the headline level: in APRA's modelled crisis, every institution holding deposits and retirement savings remained solvent and met its obligations without any assumed government support. The unresolved vulnerabilities, particularly the mismatch between banks' funding assumptions and super funds' planned withdrawal behaviour in the same crisis scenario, mean the result is a calibration point rather than a clearance certificate.