Vinyl Group Ltd Eyes First EBITDA Positive Year After Nominal Cost Deals

Vinyl Group outlines path to first profitable year after two strategic acquisitions

In its June 2026 investor presentation, Vinyl Group (ASX: VNL) detailed the acquisitions of Time Out Australia and Pedestrian Group and a forecast pathway to its first EBITDA-positive year. Both businesses were acquired for nominal consideration, lifting the company’s de-duplicated online audience reach to 55% of Australians online (Ipsos iris, All Categories).

Management outlined a forecast FY27 EBITDA of $3.5 million on forecast FY27 revenue of $37-$40 million, representing the company’s first profitable year on that measure.

The strategic angle is capital efficiency. By acquiring recognised brands at minimal cost, Vinyl is expanding national audience reach while keeping cash outlay low, positioning itself as what the presentation described as the leading acquirer of choice for “sub-scale publishers in Australia.”

When big ASX news breaks, our subscribers know first

Two recognised brands added at nominal cost

The presentation detailed two separate transactions, both struck at what management characterised as increasingly capital-efficient valuations and structures.

Time Out Australia

Time Out Australia was framed as one of the world’s most recognised urban culture brands. Vinyl acquired Time Out Australia for nominal consideration and separately entered into a long-term franchise agreement with Time Out England.

- Acquired for nominal consideration

- Long-term franchise agreement with Time Out England

- Currently profitable, with an expected positive EBITDA contribution in FY27

The company positioned the deal as confirmation of Vinyl as the leading partner for international cultural digital assets that want to maintain a presence in Australia.

Pedestrian Group

Pedestrian Group was described as one of Australia’s most recognised youth media businesses, acquired from Nine Digital Pty Ltd.

- Acquired from Nine Digital Pty Ltd for nominal consideration

- Rebalances the portfolio with original IP

- Forecast FY27 EBITDA contribution of $0.6m-$0.8m

The presentation noted the acquisition confirms Vinyl as the leading acquirer of choice for “sub-scale publishers in Australia.”

Both deals reflect minimal cash outlay against meaningful gains in audience scale and forecast EBITDA contribution, reinforcing the company’s stated ability to secure strategic acquisitions through capital-efficient structures.

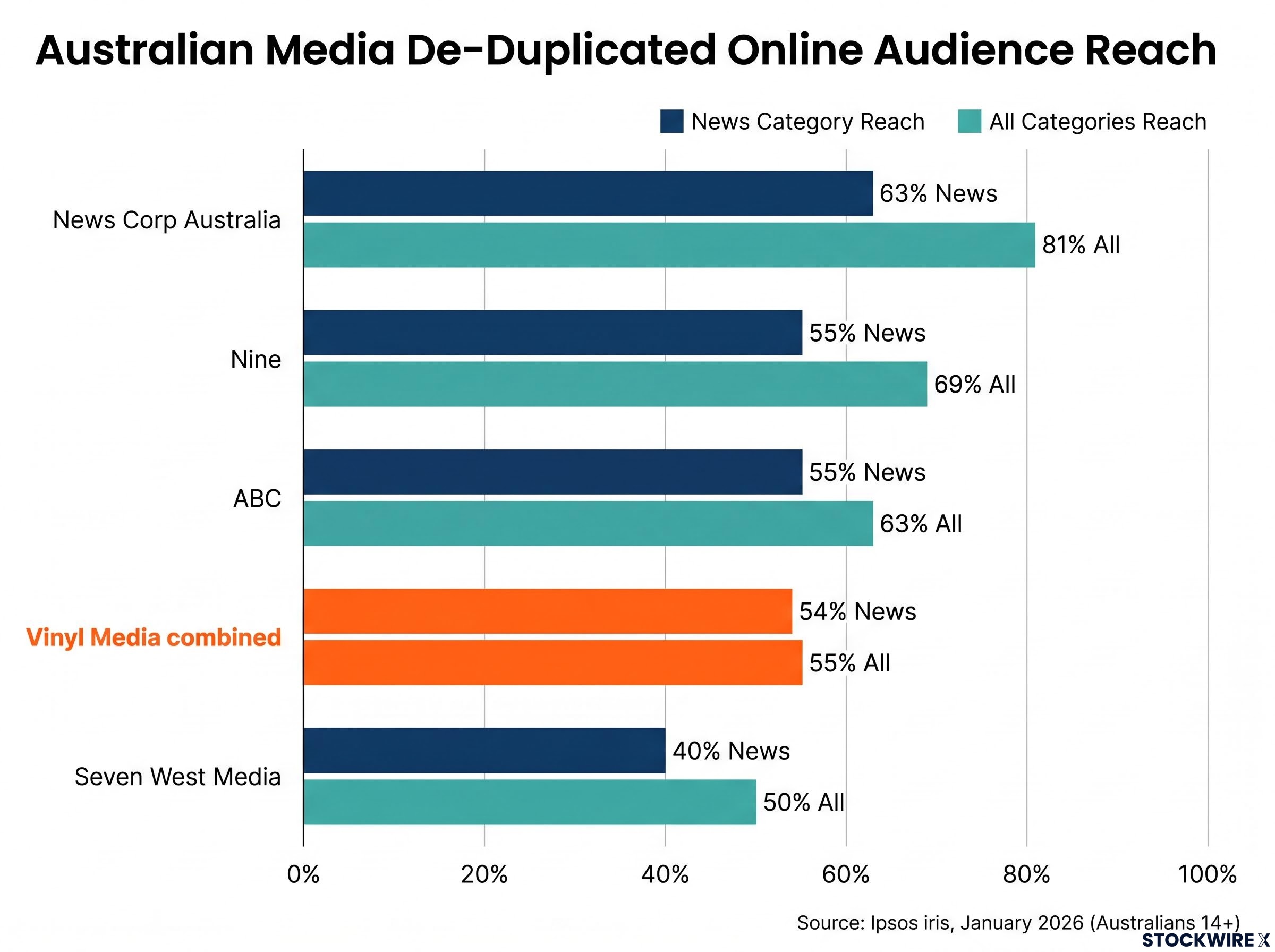

Combined audience now rivals Australia’s largest media players

The scale story sits at the centre of the strategic case. Using Ipsos iris figures, management compared Vinyl Media’s combined de-duplicated reach against selected Australian media organisations.

| Media Organisation | News Category Reach | All Categories Reach |

|---|---|---|

| News Corp Australia | 63% | 81% |

| Nine | 55% | 69% |

| ABC | 55% | 63% |

| Vinyl Media combined (VMD, Time Out & Pedestrian) | 54% | 55% |

| Seven West Media | 40% | 50% |

The figures are sourced from Ipsos iris, January 2026, measuring de-duplicated online audience reach across PC/laptop, smartphone and tablet for Australians aged 14+. The comparison is illustrative for contextual scale and does not represent an official Ipsos organisation ranking.

For investors, the proof point is clear: Vinyl now sits among the top tier of Australian digital media reach, despite acquiring its newest assets at nominal cost.

The Val Morgan Digital acquisition in March 2026 was the deal that first established this consolidation template, adding exclusive ANZ licences for BuzzFeed, Fandom, and Vox Media alongside a strategic partnership with The HOYTS Group that extended Vinyl’s advertising footprint into cinema and out-of-home channels.

What is “Adaptive Media” and why it matters

At the core of Vinyl’s model is what the presentation termed Adaptive Media, an integrated advertising model where cultural assets, technology and distribution work together to deliver meaningful brand connections at scale.

The presentation contrasted three distinct eras of advertising:

- Legacy Media: broadcast-based mass reach

- Social Media: platform algorithm-driven targeting

- Adaptive Media: advertising embedded within cultural assets

According to the presentation, advertisers value the model because it combines several outcomes in a single approach:

- Mass audience reach

- Niche targeting at scale

- Meaningful brand connections

This is Vinyl’s differentiation and pricing-power narrative. It explains how the company aims to translate scale into higher-margin advertising revenue rather than competing purely on volume.

Proof in the numbers — the Mentos case study

The presentation used the 2025 Mentos “Fresh Sounds” campaign as a concrete example of the model in action.

- 9.7M impressions and 7M reach, exceeding booked benchmarks

- 961 artist submissions versus 300 expected

- 19.6% video engagement versus a 5% target

Management noted that Vinyl delivered more than 300 Adaptive Media campaigns over the prior year, activating marquee brands including Spotify, McDonald’s, Samsung and Disney+.

A defensible, self-reinforcing business model

The presentation framed Vinyl’s model as a self-reinforcing flywheel, where each successful campaign compounds the value of the broader ecosystem.

- Combine premium cultural assets into an immersive ecosystem

- Grow audience reach through premium content and technology

- Attract brands with the scale of the ecosystem

- Deliver superior ROI for advertisers

- Acquire further assets, repeating the cycle

Management highlighted several factors that make the model difficult for competitors to replicate:

- Hard to replicate, given the difficulty of combining many cultural assets into one integrated ecosystem

- Requires scale to be profitable when delivering meaningful brand connections at a competitive price

- Technology as a core capability, supported by an internally developed AI publishing suite

- Not dependent on any single social media platform, publisher or algorithm

- A self-reinforcing flywheel where value compounds rather than resets each cycle

The framing positions Vinyl as the natural consolidator for sub-scale operators seeking an exit.

The next major ASX story will hit our subscribers first

Forecast points to first EBITDA-positive year in FY27

The financial centrepiece of the presentation was the FY27 forecast, which management presented as a turning point for the business.

Key Forecast

Forecast consolidated FY27 EBITDA of $3.5 million — Vinyl’s first EBITDA-positive year.

The supporting forecasts outlined in the presentation include:

- Forecast FY27 revenue of $37-$40 million, representing approximately 100% revenue growth

- Forecast FY27 EBITDA of $3.5 million, marking Vinyl’s first EBITDA-positive year

- A forecast assumption that some revenue duplication from overlapping assets, products and customers will work through during FY27

Management balanced this outlook with clear caveats. The presentation noted that advertising market conditions remain soft, impacted by geopolitical uncertainty and buyer hesitation. The profitability pathway was described as clear but not linear, with some expected integration and market-related volatility, amplified by seasonality.

This nuance matters for credibility. The forecast represents a target rather than a guaranteed outcome, and investors should weigh the integration risk and soft advertising backdrop against the projected growth.

Upcoming catalysts and the road ahead

The presentation set out a forward-looking timeline of strategic priorities.

- Q4 FY26: Integration of Val Morgan Digital, Time Out and Pedestrian

- 1H FY27: EBITDA-positive run-rate

- FY27: Focused technology investment to further enhance the flywheel

- FY27 and beyond: International growth through licensing, franchise and M&A opportunities

Management also flagged an “Agentic AI-first strategy under development,” with a comprehensive update set to accompany the FY26 results. This was positioned as a forward catalyst for investors to monitor.

Taken together, the strategic update points to a transition from growth-at-cost towards profitable scale. By pursuing audience reach through nominal-cost acquisitions while keeping cash outlay low, Vinyl is attempting to reach profitability without the heavy capital requirements typically associated with media consolidation.

For investors wanting a fuller treatment of both transactions, our deep-dive into the Time Out and Pedestrian acquisitions covers the deal terms, the agentic AI strategy update, and the assumptions underpinning the FY27 EBITDA guidance in detail.

No Target URL was provided. Please supply a Target URL so the CTA can be generated with a correctly embedded Markdown link.