Barclays Warns of Prolonged Market Volatility Under New Fed Reality

1 hr ago

Australia’s May inflation print delivered exactly the wrong combination for the Reserve Bank of Australia (RBA): the number that households see fell, and the number that policymakers track rose.

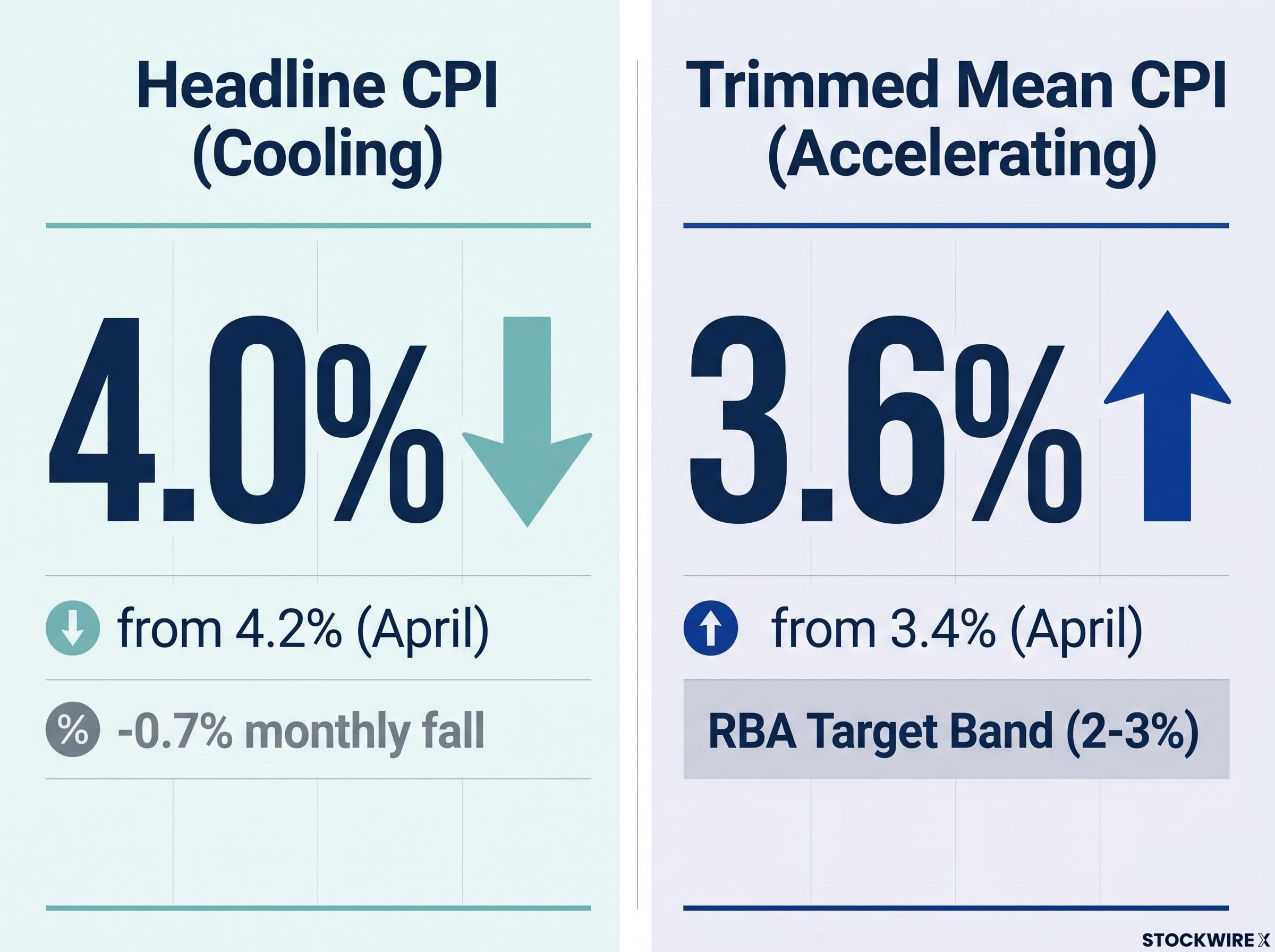

Today’s Australian Bureau of Statistics (ABS) data showed headline Consumer Price Index (CPI) easing to 4.0% annually, below market consensus, while the trimmed mean measure the RBA uses to judge underlying price pressure surprised to the upside at 3.6%, its highest reading since September 2024. That divergence does not simplify the rate outlook. It complicates it.

Here is what each measure is telling you, why the split matters for RBA rate decisions, what drove the Australian dollar below US70¢, and which two data events in the coming days will do more to settle the rate debate than today’s print did.

The headline number looked encouraging. The May annual CPI reading of 4.0% represented a step down from 4.2% in April and landed well short of the 4.3-4.4% consensus. Prices declined 0.7% on a monthly basis, a result roughly twice as large as the 0.3-0.4% fall the market had pencilled in. It is the softest annual reading since February 2026.

Then the trimmed mean told a different story. The RBA’s preferred measure of underlying inflation rose to 3.6% year-on-year, up from 3.4% in April and above the 3.5% consensus forecast. The monthly trimmed mean print of 0.4% exceeded the 0.3% that forecasters had anticipated. That 3.6% sits 0.6 percentage points above the top of the RBA’s 2-3% target band.

These two measures are not telling the same story. The headline is cooling. The underlying measure that guides monetary policy is accelerating. For investors, the trimmed mean’s movement above the RBA’s target band is the number to anchor to, not the headline softness that might otherwise suggest the inflation problem is resolving.

| Measure | April result | May consensus | May result |

|---|---|---|---|

| Headline CPI (annual) | 4.2% | 4.3-4.4% | 4.0% |

| Headline CPI (monthly) | — | -0.3% to -0.4% | -0.7% |

| Trimmed mean CPI (annual) | 3.4% | 3.5% | 3.6% |

| Trimmed mean CPI (monthly) | — | 0.3% | 0.4% |

The RBA cannot pivot toward cuts on this data. Trimmed mean inflation at 3.6% is 1.1 percentage points above the central bank’s 2.5% target midpoint, and it is moving in the wrong direction. That alone tells the board its inflation fight is not finished.

Equally, the RBA is not forced into an immediate hike. The headline undershoot and below-consensus result reduce urgency, and raising rates while the number most visible to households is falling creates a communication problem no central banker wants.

“Headline miss and core beat, the worst combination for the RBA’s communication task.” , Investing.com

The practical meaning of this bind for investors holding Australian rate-sensitive assets is straightforward: uncertainty is the operative condition. The RBA has neither the cover to ease nor a clean trigger to tighten, which extends the period where rate risk remains elevated in both directions. Based on today’s data, the board’s options are:

Rate markets continue to price a non-trivial probability of at least one further hike this year, but nothing about today’s print turned that probability into a certainty.

The trimmed mean CPI is a measure of underlying inflation that removes the most volatile price movements from both ends of the distribution. If a handful of items spike or crash in a given month, the trimmed mean strips those out and calculates what inflation looks like once the noise is removed.

The RBA’s target band is 2-3%, with a 2.5% midpoint. In May, the trimmed mean printed at 3.6%, its highest reading since September 2024, while headline CPI fell to 4.0% from 4.2% in April.

When the trimmed mean is accelerating while the headline is cooling, the underlying inflation problem is not resolving; it is being masked by short-term factors. For you, that distinction changes how to interpret any apparent easing in the top-line number. A falling headline does not mean the inflation fight is being won if the persistent component is getting worse.

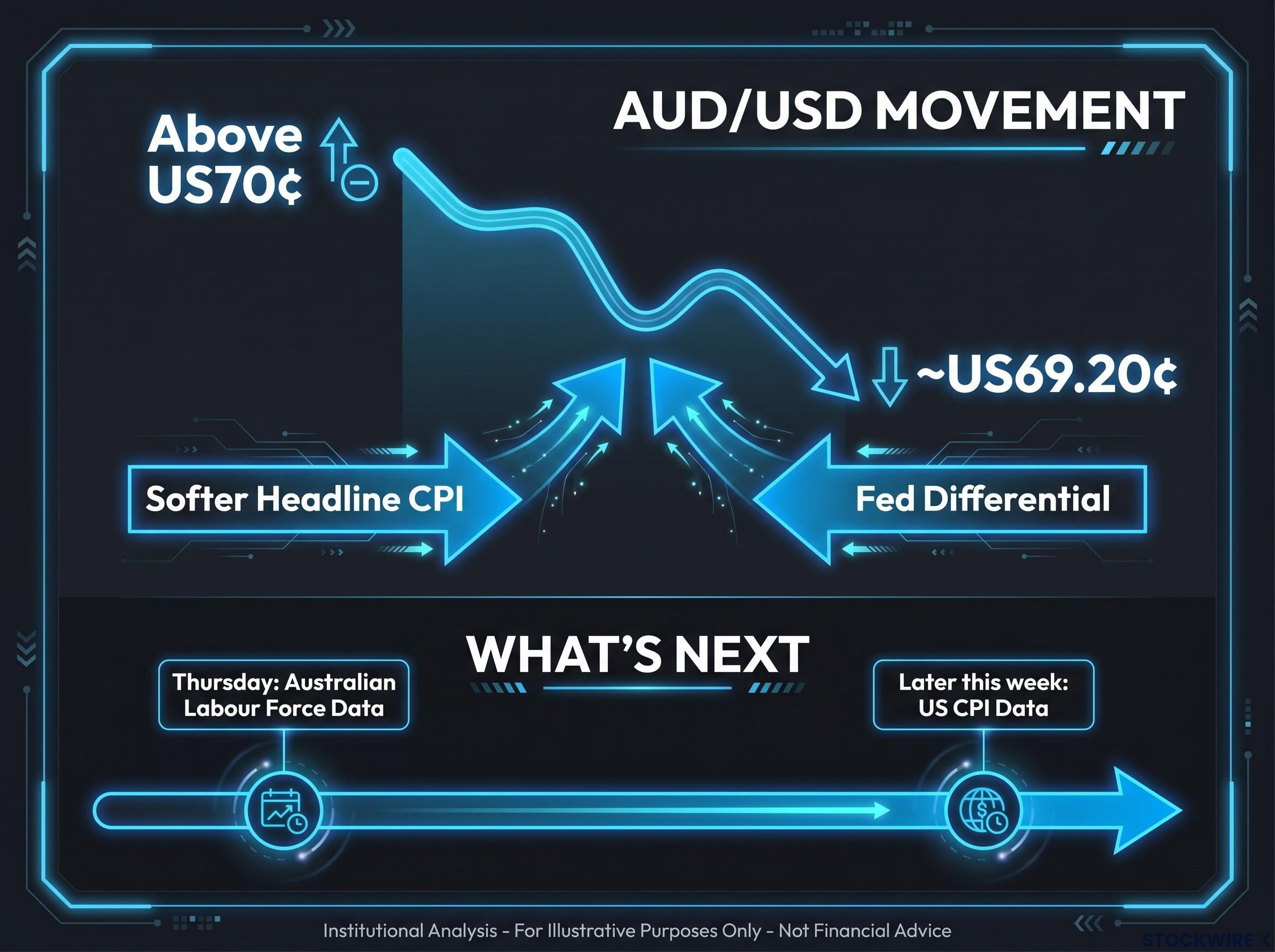

Overnight, the Australian dollar slid from above US70¢ to settle near US69.20¢, a decline driven by two distinct forces that happened to point in the same direction at the same time.

The softer-than-expected headline CPI reduced confidence that the RBA would aggressively tighten from here. When the market sees a below-consensus inflation print, even one accompanied by a trimmed mean overshoot, it trims the odds of near-term rate hikes. Lower expected rates mean a less attractive yield on Australian assets, and that feeds directly into a weaker currency.

The trimmed mean overshoot prevents a full repricing toward easing. But it does not fully offset the headline drag on hike expectations, and that half-step is enough to pressure the Australian dollar.

The other half of the equation sits in Washington. The US Federal Reserve’s higher-for-longer expectations have widened the expected interest rate spread in favour of the US dollar. When the Fed is perceived as relatively more hawkish than the RBA, capital flows toward USD-denominated assets, and the AUD/USD pair drops.

AUD/USD fell to approximately US69.20¢ overnight, with the immediate reaction to the CPI print itself described as muted to modestly negative before the broader rate differential trade took over.

For investors with AUD exposure, the signal here is that the currency is vulnerable not because of Australian data alone but because of the relative rate story between the RBA and the Fed. US data events now matter as much as domestic releases for AUD/USD direction.

Today’s CPI offered a split verdict. The two releases that will break the tie are already on the calendar, and each has a clear reaction function.

These two releases, not today’s CPI, are where the near-term RBA rate call will be made by the market. Investors who position ahead of them need to understand the asymmetry: the Australian labour data shapes the domestic rate outlook, while the US print shapes the currency environment those rates operate in. Together, they carry more weight for August meeting pricing than any single inflation reading.

Today’s May CPI data neither resolved the rate debate nor eliminated either direction. Trimmed mean inflation at 3.6%, above target and accelerating, is the persistent underlying pressure the RBA cannot dismiss. The AUD at approximately US69.20¢ is where the market has priced the current state of uncertainty.

What changes from here depends on Thursday’s Labour Force data and the US CPI print later this week. Those two events will update the probability distribution before the August RBA meeting, and they will do so with more force than any single inflation number could.

For investors with exposure to Australian assets or currency markets, the framework is clear: the rate path is genuinely open, event risk is elevated into Thursday, and the direction hinges on data that is not yet known.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results.

Trimmed mean CPI strips out the most volatile price movements from both ends of the distribution, isolating persistent inflation trends rather than short-term noise. The RBA uses it as its primary policy guide because it is more predictive of where inflation is heading than the headline figure, which can swing on energy prices and one-off policy changes.

Headline CPI fell to 4.0% annually, below the 4.3-4.4% consensus, while the trimmed mean rose to 3.6%, above both the 3.5% forecast and April's 3.4% reading. The divergence means the headline number is cooling but the underlying inflation measure the RBA targets is accelerating.

The softer-than-expected headline CPI trimmed near-term RBA rate hike expectations, reducing the yield appeal of Australian assets and pushing AUD/USD down to approximately US69.20 cents. The Federal Reserve's higher-for-longer stance widened the rate differential in favour of the US dollar, compounding the pressure.

Thursday's Australian Labour Force data and the US CPI print later this week carry more weight for August meeting pricing than the May CPI reading. Strong Australian jobs data keeps hike odds elevated, while a hot US print strengthens the USD and adds further downside pressure to the AUD.

No. With trimmed mean inflation at 3.6%, sitting 1.1 percentage points above the RBA's 2.5% midpoint target and moving in the wrong direction, the board cannot credibly pivot toward cuts on this data. The headline undershoot reduces urgency to hike but does not remove the option.