Judo Capital Holdings Ltd Flags 30% Profit Growth Amid Credit Pressure

Judo Bank flags 30% profit growth despite emerging asset quality pressure

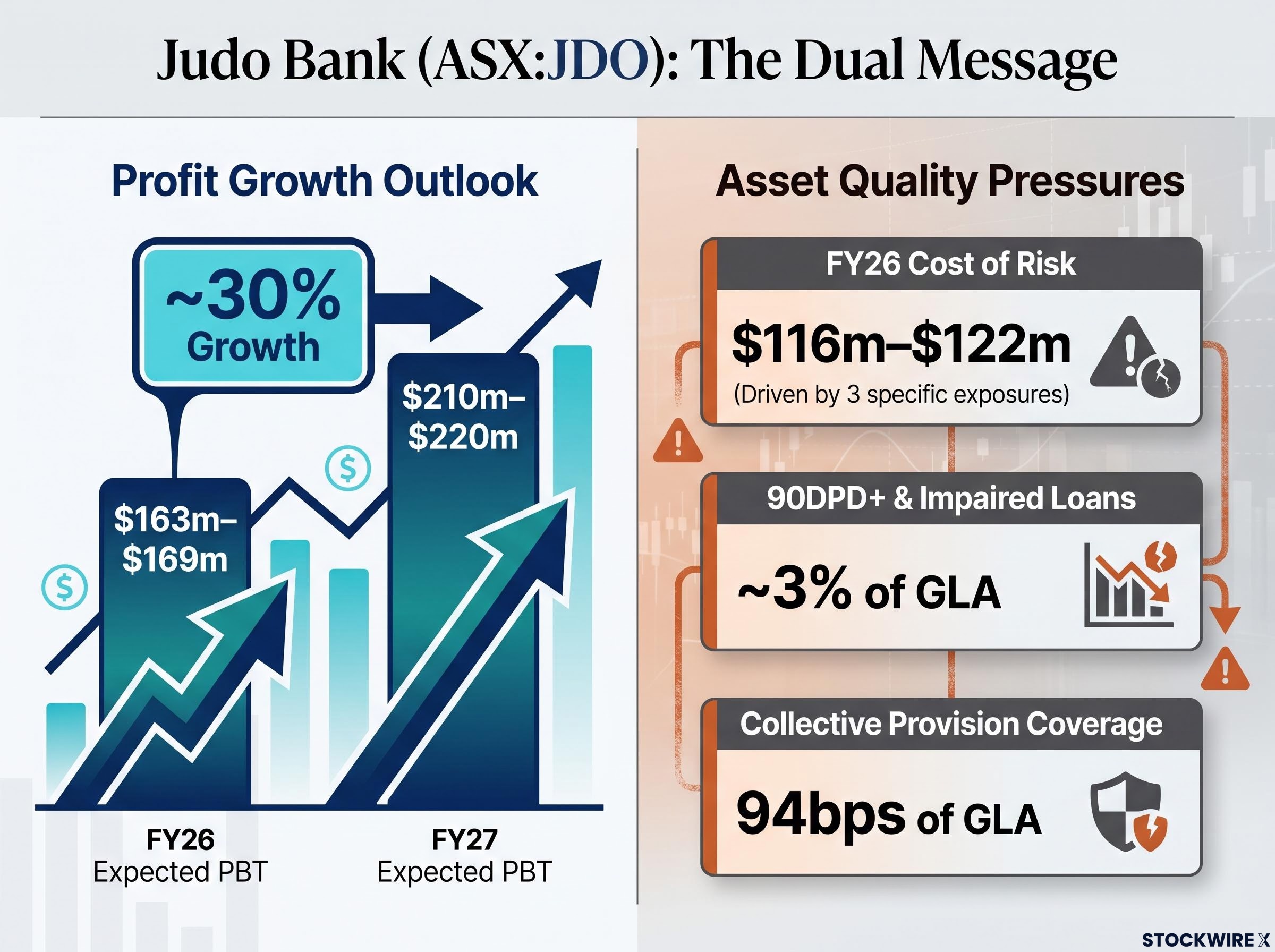

Judo Capital Holdings Limited (ASX:JDO) has updated the market on its FY26 trading and asset quality position, with expected profit before tax (PBT) now at $163m–$169m, representing approximately 30% growth on FY25, while flagging a higher cost of risk tied to three specific borrower exposures.

The update, issued 25 June 2026 ahead of the full FY26 result on 18 August 2026, presents a dual message. Underlying lending momentum and margins remain strong, yet recent credit developments across a small number of customers have pushed the FY26 cost of risk to an expected $116m–$122m.

Management framed the credit events as isolated rather than systemic. Profit growth guidance for both FY26 and FY27 remains intact, with FY27 PBT now expected at $210m–$220m, again reflecting around 30% growth.

When big ASX news breaks, our subscribers know first

Asset quality update — three exposures drive higher cost of risk

The increase in cost of risk has been driven primarily by specific provision increases for three exposures spread across different sectors. According to Judo, these emerged as a result of customer-specific developments that surfaced after the customer-by-customer review undertaken in the third quarter.

Note that the term “specific provisions” includes both individually-assessed and collective provisions for impaired assets. Judo now expects 90-days-past-due (90DPD+) and impaired loans to be approximately 3% of GLA as at 30 June, inclusive of the three exposures.

Collective provision coverage at 30 June is expected to remain broadly in line with the Q3 trading update, at 94bps of GLA (or 1.09% of standardised credit risk weighted assets). Provisioning levels include a management overlay for sectors impacted by the uncertain macroeconomic environment.

The Q3 collective provision top-up, which lifted coverage 5 basis points to 94bps of gross loans, was flagged at the time as a precautionary response to macroeconomic uncertainty rather than evidence of credit deterioration, making the three specific exposures disclosed in June a distinct and more acute development.

Key asset quality figures include:

- Cost of risk: $116m–$122m

- 90DPD+ and impaired loans: ~3% of GLA

- Collective provision coverage: 94bps of GLA

- Through-the-cycle cost of risk maintained at 50bps of average GLA

CEO Chris Bayliss

“We continue to see strong underlying momentum in the business. Recent credit outcomes have been driven by a small number of customers, who we are actively working with. These exposures have deteriorated subsequent to the customer-by-customer review undertaken in the third quarter and reflect recent, borrower-specific developments. While today’s update is partly a result of the macro environment, it is nevertheless disappointing. Regardless, we remain confident in the strength of our underlying business and the quality of the portfolio. We have a proven customer value proposition, are profitable and well capitalised, and have a clear path to achieving a return on equity in the low-to-mid teens.”

Trading performance — lending momentum and margin strength

Beneath the credit headwind, Judo’s operational story heading into Q4 FY26 has remained solid. Gross Loans and Advances (GLA) stood at over $14.4bn as of 24 June, expected to reach $14.6bn–$14.7bn by 30 June 2026.

Net interest margin (NIM) is now expected to be over 3.2% for 2H26, above the prior guidance of approximately 3.15%, supported by favourable term deposit costs. Front book and blended lending margins were stable at 4.2% over 1-month BBSW across April and May.

The AAA lending pipeline (applications, approved and accepted) was robust at $2.4bn, carrying a margin of 4.3% at the end of May. The blended cost of deposits was 62bps over 1-month BBSW over April and May, while new term deposits were originated at 76bps over BBSW in Q4 FY26 to date, largely due to swap rate movements.

On costs, the cost-to-income (CTI) ratio for 2H26 is on track to be below 1H26 (48.5%), in line with existing guidance. Judo confirmed it remains on track to achieve its existing FY26 guidance for GLA, NIM and CTI.

| Metric | Prior Position | Updated FY26 Position | Investor Read |

|---|---|---|---|

| PBT growth | — | $163m–$169m (~30%) | Profit growth intact |

| Cost of risk | — | $116m–$122m | Higher on three exposures |

| NIM (2H26) | ~3.15% | Over 3.2% | Margin uplift |

| GLA | Over $14.4bn (24 Jun) | $14.6bn–$14.7bn by 30 Jun | Lending momentum maintained |

| CTI (2H26) | 48.5% (1H26) | Below 1H26 | Cost discipline on track |

FY27 outlook and capital position

For FY27, Judo expects to deliver PBT of between $210m–$220m, representing growth of approximately 30%. The guidance takes into account the uncertain macroeconomic and geopolitical environment, while continuing to demonstrate the Bank’s ability to deliver strong growth and operating leverage.

On capital, Judo expects to have a CET1 ratio of approximately 12.4% at 30 June 2026, including the impact of its recent capital relief term securitisation transaction. The Bank will transition to operating with a management CET1 target range of 11.0%–12.0% in normal operating conditions.

The capital relief securitisation, which was upsized to $750m on strong investor demand and priced at a weighted average of 171bps over 1-month BBSW, lifted Judo’s pro forma CET1 ratio to 13.2% before settling back toward the 12.4% figure reported here after accounting for lending growth and other capital movements.

According to Judo, the securitisation “demonstrates that the Bank has multiple levers to actively manage capital, providing increased optionality, including the potential to consider capital management initiatives in due course.” Bayliss reiterated a clear path to achieving a return on equity in the low-to-mid teens.

For investors, a strong capital position combined with a lower CET1 target range signals confidence, alongside potential optionality for future capital management.

The next major ASX story will hit our subscribers first

Key dates and what comes next

Judo hosted an investor and analyst briefing at 10.00am AEST on 25 June 2026, with a live webcast made available. The full FY26 result is scheduled for 18 August 2026.

Upcoming milestones:

- Investor and analyst briefing — 25 June 2026

- FY26 financial year close — 30 June 2026

- FY26 result announcement — 18 August 2026

Stay Ahead on ASX Finance and Fintech News

Big News Blast delivers FREE breaking ASX news straight to your inbox within minutes of release, complete with in-depth analysis already done. Join 20,000+ subscribers who never miss a market-moving update. Click the “Free Alerts” button at StockWire X to start receiving alerts the moment ASX announcements drop.