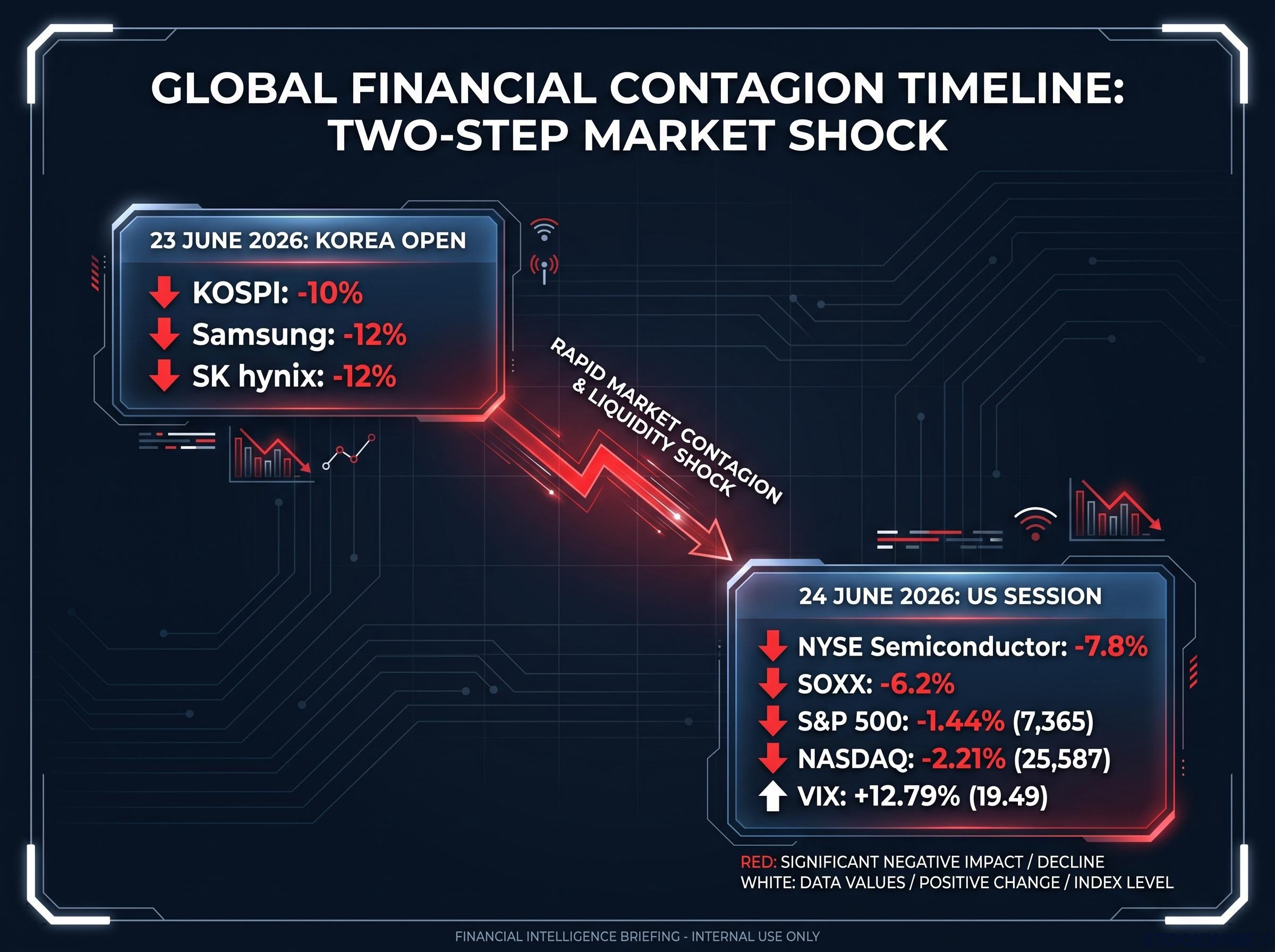

South Korea’s KOSPI plunged roughly 10% on 23 June 2026. Samsung and SK hynix each dropped more than 12% in a single session. Across the Pacific, Micron, a stock that had gained more than 300% year-to-date and crossed the $1 trillion market-cap threshold barely a month earlier, fell approximately 13-14% ahead of its own earnings call. The numbers alone are striking. What matters more is what they reveal about the trade underneath.

This was not a single-catalyst shock. Several forces that had been building for months, including extreme positioning in AI-chip names, leverage embedded in Korean structured products, and rising doubts about the linearity of AI data-centre demand, collided within a 48-hour window. The speed at which the selloff spread from Seoul to New York is itself part of the story: it tells you how interconnected the AI-chip trade had become, and how little slack existed when the unwind began.

What follows gives you a framework for reading the next set of catalysts, from Micron’s earnings to Big Tech capex commentary, against the two competing explanations for what just happened: a technical shakeout in a crowded trade, or an early signal that the semiconductor cycle is turning.

How a Korean chip complex sparked a global selloff

The chain of events moved fast. South Korea was the origination point, and for specific reasons: the combination of retail participation, structured products tied to chip indices, and concentrated semiconductor exposure made the Korean market uniquely vulnerable to a reversal. When prices turned, those products forced mechanical selling, amplifying what might otherwise have been a routine pullback into a cascading liquidation.

Then came the regulatory signal. South Korea’s financial regulator acknowledged the government moved too quickly in approving leveraged funds linked to chip stocks.

South Korea’s financial regulator indicated the government moved too quickly in approving leveraged funds linked to chip stocks, adding regulatory selling pressure on top of mechanical redemptions.

That admission is not a footnote. It tells you the amplification of this selloff was partly a policy misstep, which means the mechanical selling pressure was larger than the underlying fundamental concern alone would have justified.

Korea-originating chip selloffs are not a new pattern: a single Facebook post from a South Korean presidential aide about a proposed AI tax wiped more than $300 billion in market value intraday on 12 May 2026, with three government bodies issuing coordinated denials before the session closed, a precedent that helps explain why Korean political and regulatory signals now carry immediate cross-market weight.

The contagion followed a predictable path:

- 23 June, Korea open: KOSPI fell approximately 10%; Samsung and SK hynix each down more than 12%

- 24 June, US pre-market: Semiconductor futures indicated sharp losses as global investors repriced exposure

- 24 June, US session: The NYSE Semiconductor index shed 7.8%; SOXX closed 6.2% lower; the S&P 500 finished down 1.44% at 7,365; the NASDAQ declined 2.21% to 25,587; and the VIX climbed 12.79%, closing at 19.49

| Index / ETF | Single-session decline |

|---|---|

| KOSPI | ~10% |

| NYSE Semiconductor | 7.8% |

| SOXX | 6.2% |

| DRAM-focused ETF | ~14% |

| NASDAQ Composite | 2.21% |

When big ASX news breaks, our subscribers know first

The five forces that made the trade this vulnerable

The trigger was Korea. But the trigger is not the explanation. Five forces had been building for months, each one weakening the structural integrity of the AI-chip trade before the first redemption notice hit.

- Extreme positioning and valuation stretch. Micron joined the $1 trillion market-cap club in late May 2026. HBM (High Bandwidth Memory, the specialised memory chips used in AI accelerators) was sold out through calendar 2026. Gross margins had reached the mid-50s to mid-70s range, with peaks above 80%. This was a trade priced for perfection, with no cushion for disappointment.

- Open-source AI and efficiency fears. The bull case for AI hardware implicitly assumes demand comes from ever-larger, proprietary frontier models run on the densest hardware. If open-source models and more efficient architectures deliver competitive performance at lower compute footprints, long-dated HBM demand projections look too optimistic.

- Rising doubts about AI capex linearity. Broadcom’s guidance miss in early June served as the first concrete flashpoint. Analysts highlighted that hyperscaler CFOs are starting to scrutinise returns on massive AI capital expenditure, raising the risk that the pace of accelerator and HBM purchases moderates over the next couple of years.

- SK hynix HBM4 and DRAM mix chatter. Officially, SK hynix continues to guide to strong HBM3E and HBM4 demand, with approximately 70% HBM4 quota allocation for Nvidia’s Rubin platform. But market chatter suggested the company is selectively pushing more capacity toward conventional DRAM to exploit shifting relative profitability. Even unconfirmed, that kind of signal is exactly what a crowded market is primed to react to.

- Late-cycle memory pricing risk into 2027. Sell-side work specifically flagged potential memory price weakness for 2027 if capacity additions overshoot just as AI demand normalises. The memory industry’s boom-bust history means this risk is never purely theoretical.

None of these forces was, by itself, a catastrophic revelation. The problem was that they converged simultaneously in a trade where positioning left no room for doubt.

UBS and Citi had flagged crowded-trade positioning risks in AI-linked equities the morning before the selloff, citing the BofA June 2026 fund manager survey in which 80% of managers named long global semiconductors as the most crowded trade in the survey’s 12-year history, a concentration reading with no historical precedent.

What the rotation pattern tells you about market structure

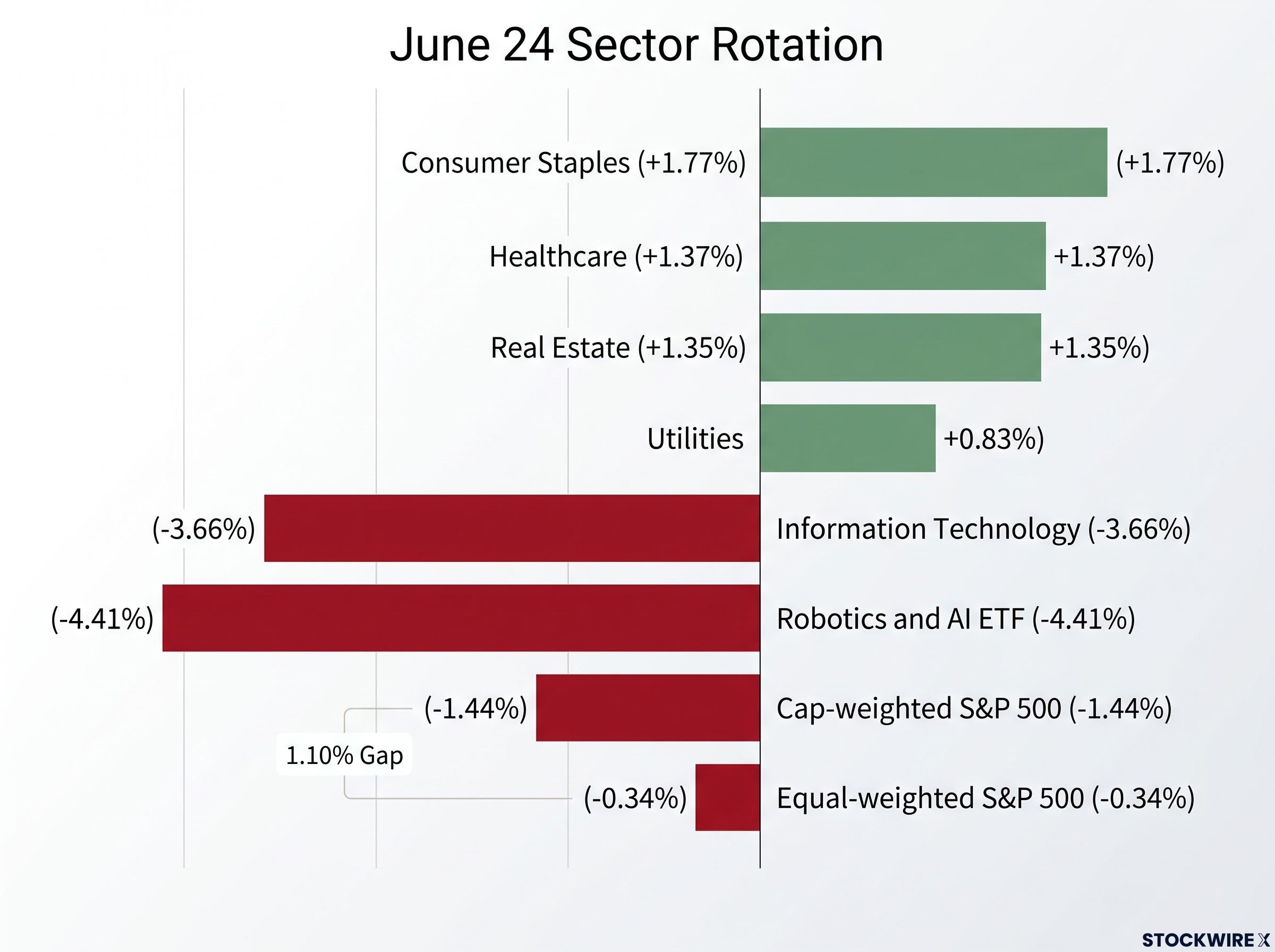

Consumer staples gained 1.77% on 24 June. Healthcare rose 1.37%. Real estate climbed 1.35%. Utilities added 0.83%. Information technology fell 3.66%. The Robotics and AI ETF dropped 4.41%.

That split is the clearest signal in the data. Capital did not leave equities. It rotated within them.

The confirmation comes from one number. The equal-weighted S&P 500 fell just 0.34%, while the cap-weighted S&P 500 declined 1.44%: a gap of approximately 110 basis points.

The 110-basis-point gap between the equal-weighted and cap-weighted S&P 500 shows that losses were concentrated in the names carrying the heaviest positioning. That pattern is consistent with leveraged unwinding rather than a broad-based reconsideration of market fundamentals.

The Dow Jones Industrial Average, less exposed to mega-cap semiconductor names, fell only 0.09%. The NASDAQ, heavily weighted toward the same AI-chip cohort, dropped 2.21%. The divergence captures concentration risk in a single comparison.

| Sector / Index | 24 June performance |

|---|---|

| Consumer Staples | +1.77% |

| Healthcare | +1.37% |

| Information Technology | -3.66% |

| Robotics and AI ETF | -4.41% |

| Equal-weighted S&P 500 | -0.34% |

Recognising this pattern helps you avoid two errors: panic-selling unrelated holdings because a headline number spooked you, or assuming chip names will bounce immediately because the wider market held up. Rotation is not collapse, but it is also not instant recovery for the sector that shed the capital.

Technical correction or structural shift? The case for each

Why this looks like a technical shakeout

- The speed and breadth of the move, concentrated within 48 hours across two continents, are characteristic of forced selling in levered positions rather than a gradual, fundamentals-led derating.

- Signs of mechanical selling were visible in specific products, including the Roundhill Memory ETF and leveraged Korean chip-linked funds, where redemptions and rebalancing drove indiscriminate selling pressure.

- There was no single catastrophic earnings miss or macro shock. A series of incremental worries hit a crowded trade simultaneously.

- Broader market breadth remained intact: the Russell 2000 lost only 0.96%, and the equal-weighted S&P 500 dropped a modest 0.34%, figures that point toward sector rotation rather than a broader, systemic flight from risk.

Why the structural risks deserve respect

- The AI data-centre capex curve is unlikely to be a straight line. As hyperscaler projects scale, CFOs and boards scrutinise return on investment more intensely, which can flatten or stagger deployment timelines.

- The memory industry’s history is one of booms followed by sharp corrections. The current supercycle narrative assumes AI is large enough to structurally dampen that cyclicality. If that assumption is even partly wrong, current multiples have limited cushion.

- Any sustained shift in the profitability balance between HBM and conventional DRAM, or any signal that HBM undersupply is less durable than expected, would force a reassessment of long-term earnings power for the major memory producers.

- If Micron’s HBM sold-out status through 2026 and gross margins above 80% represent peak conditions rather than a new baseline, the recovery from this selloff will be slower than bulls expect.

HBM supply constraints are more structurally durable than the selloff’s speed might suggest: SK Hynix projects a global DRAM shortage lasting through 2030, HBM inventory sits at just 3-4 weeks industry-wide, and the first meaningful output from new capacity commitments by Micron and SK hynix is not expected until 2027-2028, a timeline that makes the current undersupply condition difficult to resolve quickly even if AI demand moderates.

The most defensible synthesis: this is primarily a technical correction in an overextended trade, but occurring at a moment when genuine medium-term uncertainties are rising. Being right about “technical correction” does not mean being safe. A trade that was already pricing in perfection will be slow to recover if the next two or three data points are merely good rather than exceptional.

Micron as the market’s verdict on the AI memory thesis

Micron became the focal point for a reason. It is the most direct US-listed proxy for HBM demand, AI data-centre spending health, and memory pricing trajectory, all concentrated in a single earnings event scheduled for 24 June 2026.

By late May 2026, Micron had crossed the $1 trillion market-cap threshold, reflecting just how far expectations had stretched. A stock that appreciates more than 300% inside a year sets a demanding benchmark: even a genuinely strong quarterly result can fall short of what the share price has already priced in.

The 13-14% pre-earnings drop tells you the market was not waiting for a negative surprise. It was de-risking from a position that left no room for anything less than exceptional. That dynamic is as much about positioning as it is about any specific view on Micron’s actual results.

The earnings call functions as a binary test. If management reiterates multi-year HBM undersupply and strong 2027 pricing, it supports the technical-correction interpretation. If it introduces caution on forward guidance or flags memory pricing normalisation, it validates the structural-concern camp. Either way, Micron’s numbers will carry weight far beyond a single company’s quarterly results. They are the clearest near-term signal on whether the broader AI-chip thesis remains intact.

Four variables that will determine what comes next for chip stocks

The next 60-90 days will resolve what this selloff was. Four variables will do the work:

- Micron’s earnings guidance tone. If management reiterates that HBM is sold out through 2026 with strong 2027 pricing visibility, the bull case stabilises. If the call introduces caution on forward demand or margin sustainability, expect the structural-concern camp to gain conviction. Gross margins peaking above 80% need to look sustainable, not cyclical.

- Hyperscaler AI capex commentary. Upcoming Big Tech earnings are where the demand side of the equation gets tested. Evercore has argued that the upcoming round of earnings reports is likely to bring the technology sector back into favour with investors. Reaffirmed or increased multi-year AI capex envelopes would stabilise sentiment across the semiconductor complex. Any signal of delayed projects, stretched timelines, or reallocation toward software efficiency over raw hardware would pressure chip names further.

- Regulatory response to leveraged chip products. Korea’s financial watchdog has indicated that the approval process for leveraged funds tied to chip stocks moved faster than it should have. If regulators in other markets tighten rules around complex retail products tied to volatile sectors, it could reduce the amplitude of future swings, but also remove a source of incremental demand on the way back up.

- Volatility and breadth normalisation. The VIX closed at 19.49 after the selloff. A sustained decline in volatility and broader participation on the upside, rather than a narrow AI and semiconductor cohort leading, would signal that the worst of the forced de-leveraging has passed. Continued underperformance of the most AI-exposed names even as the broader market steadies would point to a more durable leadership transition.

Barclays and Stifel each lifted their S&P 500 year-end price target to 7,800, citing the strength of the broader earnings outlook, even as the index slid on the day. The broader market’s base case has not broken. What remains genuinely uncertain is whether chip stocks specifically will recover their leadership role or cede it to other growth sectors for the near term.

What the correction changes, and what it does not

The selloff that unfolded across these 48 hours reflects a trade that had become dangerously crowded, with leverage concentrated in Korean structured products and a regulatory misstep compounding the mechanical pressure, all against a backdrop where substantive questions about AI spending trajectories, the durability of HBM demand, and the memory industry’s inherent cyclicality were already accumulating. The technical and the fundamental are not separate stories here: they are intertwined.

What has changed: the trade is no longer “free money” for late entrants. The market has revealed that expectations were priced for perfection, and the regulatory and leverage dynamics in Korean chip products have been exposed for what they were. The crowd discovered, as it periodically does, that a crowded position exits through a narrow door.

What has not changed: Micron’s fundamental HBM position remains strong. SK hynix’s multi-year demand visibility has not been formally revised. Hyperscaler AI capex remains substantial, even if scrutiny is increasing. The structural demand story has not been disproved; it has been questioned, and those are different things.

The next 60-90 days of earnings and capex commentary will either confirm that this was a flush to buy, or reveal that the semiconductor cycle is earlier in a structural reset than bulls assumed. Until that evidence arrives, conviction in either direction is a guess dressed as a thesis.

For investors holding Samsung or SK hynix positions and weighing whether to act before the next catalyst window closes, our dedicated guide to holding chip stocks through volatile markets walks through the specific rules-based framework, including band-rebalancing triggers, single-stock concentration caps, and FINRA’s pre-trade checklist, that Jefferies, Barclays, and five major asset managers recommend for navigating late-stage chip rallies without reactive selling.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—