Tasmea outlines ~A$75m JPS Group acquisition to expand into Australia’s LNG energy sector

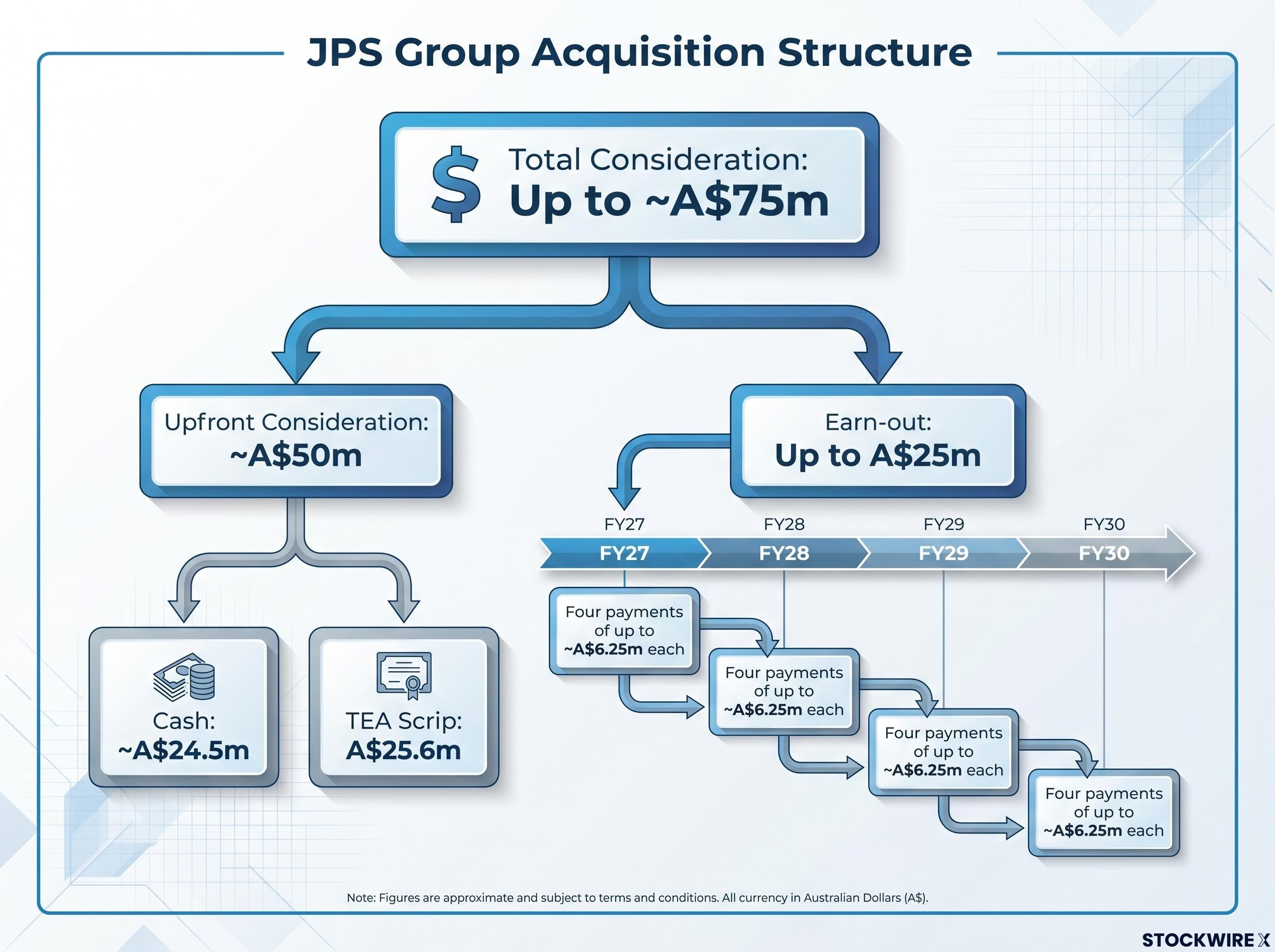

In its June 2026 investor presentation, Tasmea (ASX: TEA) outlined the acquisition of 100% of JPS Group, a specialist integrated services provider to the Australian energy sector. The presentation detailed total consideration of up to ~A$75m, comprising ~A$50m upfront at settlement plus an earn-out of up to A$25m payable across FY27–FY30.

Management highlighted that the transaction is forecast to be ~5% EPS accretive in FY26e (excluding synergies) and is fully funded. The Share Purchase Agreement (SPA) was executed 23 June 2026, with settlement targeted on or around 1 August 2026, subject to customary conditions precedent including ACCC approval under Australia’s new mandatory merger control regime.

The presentation reconfirmed FY26 guidance, including underlying EBIT of $117m and underlying NPAT of $72.5m. The strategic angle outlined positions the deal as a means of diversifying Tasmea’s earnings into the structurally growing LNG and gas market via an embedded, recurring-revenue services platform.

When big ASX news breaks, our subscribers know first

Inside the deal: how the JPS acquisition is structured

The presentation set out the key transaction terms, which were executed under the signed SPA.

| Term | Detail |

|---|---|

| Target | 100% of JPS Holdings Pty Ltd entities (JPS Management & Execution Pty Ltd and Safe Isolation Australia Pty Ltd) |

| Total consideration | Up to ~A$75m |

| Upfront consideration | ~A$24.5m cash (existing cash reserves & debt facility draw down) plus A$25.6m TEA scrip (3,011,750 new TEA shares at A$8.50 per share) |

| Earn-out | Four cash payments of up to ~A$6.25m each (up to A$25.0m total), payable 30 Sep 2027–2030, subject to JPS achieving Maintainable EBIT ≥A$12.0m each year |

| Leverage post-deal | ~0.85x net debt to pro forma FY26e EBITDA (within TEA’s target leverage) |

How the earn-out works

The presentation explained the performance-based mechanics designed to align vendor incentives with delivery:

-

For every $1 of EBIT below A$12m, the earn-out reduces by $2.

-

An EBIT floor of A$8.875m results in a nil earn-out for that year.

-

A cumulative catch-up payment is payable in cash if cumulative EBIT of A$48.0m is achieved across the four years.

This structure ties vendor consideration to ongoing performance, providing downside protection for Tasmea while rewarding the JPS founder-GMs for sustained delivery. The combination of upfront scrip and a multi-year earn-out reinforces alignment between the vendors and Tasmea shareholders.

What JPS Group brings: Tier-1 LNG clients and sticky recurring revenue

Management profiled JPS as a leading integrated services provider that embeds specialist workforces directly into energy asset operators, executing critical work scopes on Australian LNG and gas infrastructure.

-

~150 FTE specialist workforce, supported by a 600+ vetted specialist labour pool.

-

Brisbane-headquartered and founded in 2018, with 40+ projects delivered and 500,000+ safe-work hours.

-

Embedded clients including Chevron, ConocoPhillips, INPEX, Mitsui, Santos, Shell and Woodside.

-

More than 10 long-term Master Service Agreements (MSAs), with revenue visibility of >80% in FY27e and ~70% in FY28e.

-

FY26e underlying EBIT of ~$10m at specialist margins, with revenue forecast to double by FY29 (from an FY26e base).

-

A track record across APLNG, GLNG, QCLNG, Gorgon, Wheatstone, Pluto, Scarborough, Prelude FLNG, Ichthys, Darwin LNG and Varanus Island.

The presentation noted that all five Founder-GMs, with an average of 20+ years’ sector experience, are staying with the business, and the JPS brand is to be retained. The investment significance lies in a recurring, regulation-mandated revenue base operating within a high-barrier sector.

The SIA / DBB Saver edge

The presentation detailed JPS’s differentiated technology offering through Safe Isolation Australia (SIA), the sole Australian distributor and equipment services provider under a 5+5 year agreement with ValveTight.

The Double Block & Bleed (“DBB”) Saver Technology (ValveTight) creates a vacuum between passing valves via a nitrogen-driven Venturi pump, enabling 100% isolation at the point of work. This allows maintenance to proceed while the plant remains online, avoiding costly shutdown scope. Management positioned it as specialist-margin, recurring income with minimal cost of goods sold, a cross-sell gateway to new operators, and an offering with USA and Africa expansion opportunities identified.

Why LNG? The market backdrop investors should understand

The Australian LNG services market underpins the rationale outlined in the presentation. Understanding its structure helps explain why recurring maintenance demand exists.

-

10 producing LNG facilities operate across Western Australia, the Northern Territory and Queensland.

-

More than A$300bn has been invested in LNG project capex over the last 20 years.

-

Australian nameplate LNG capacity stands at 88 mtpa, around 20% of global capacity, ranking the country among the top three exporters.

-

Approximately 75% of capacity is sold on long-term contracts, with tenor running into the 2030s and 2040s.

These highly regulated assets require mandatory periodic shutdowns and statutory maintenance, while ageing infrastructure drives life-extension work. Together, these create a structural, repeatable services market. The presentation cited the Ichthys LNG facility in Darwin as an example, where a maintenance program exceeding A$200m saw the onshore workforce scale from 600 to 1,600+ during 2025. This demand engine underpins JPS’s revenue visibility and growth forecast.

The financial impact and strategic rationale for Tasmea

The presentation set out the pro forma FY26e impact of the combined acquisitions. These figures are forecasts and assume full 12-month ownership.

| Metric | TEA pro forma pre-M&A | Pro forma post-M&A (TEA, Maxim & JPS) |

|---|---|---|

| Underlying EBIT ($m) | 128 | 185 |

| Underlying NPAT ($m) | 78 | 113 |

| Underlying EPS (cps) | 29.8 | 40.9 |

| Gearing (net debt / pro forma EBITDA) | <0.50x | ~0.85x |

| EBIT contribution share | — | TEA 69% / Maxim 25% / JPS 6% |

It is important to note that the post-M&A figures incorporate both the Maxim Group acquisition (announced to the ASX on 2 June 2026) and JPS. The full uplift should not be attributed to JPS alone. The ~5% EPS accretion is JPS-specific and illustratively assumes full 12-month FY26e ownership.

The Maxim Group acquisition, announced to the ASX on 2 June 2026 for up to A$254 million, targets structural exposure to data centres, BESS, and major infrastructure, with pro forma FY26 Underlying EBIT rising from A$128 million to A$175 million before the JPS contribution is layered in.

The presentation detailed an upfront EV/EBIT multiple of ~5x FY26e (excluding the earn-out), a total enterprise value of ~$75m, and maintainable EBIT of ~$12m per annum.

Strategic fit and synergy upside

Management outlined the strategic case for combining JPS with the Tasmea Group:

-

Adds an embedded energy-services platform and Tier-1 LNG client base to the TEA Group.

-

Revenue synergies: cross-sell of Tasmea’s specialist trade streams (Electrical, Mechanical, Civil, Water & Fluid) into JPS’s energy client base.

-

Operational synergies: Tasmea Corporate Services and the WorkPac labour engine support JPS’s scaling.

-

Cost synergies: procurement at scale, systems rationalisation over time, and identified insurance savings.

The presentation also highlighted the quality of JPS’s earnings, characterised by an asset-light model with high cash conversion and organic growth funded internally.

The acquisition is positioned to diversify Tasmea’s revenues into the energy and LNG sector, adding recurring “sticky” revenue under more than 10 long-term MSAs while creating cross-sell opportunities across the wider Group.

What comes next

The presentation set out a defined roadmap and timeline for the transaction:

-

Settlement is targeted on or around 1 August 2026, subject to conditions precedent including ACCC approval.

-

The earn-out period runs across FY27–FY30, with payments scheduled on 30 September in 2027, 2028, 2029 and 2030.

-

International expansion is underway across the USA and Africa, including Chevron USA/Africa, Woodside USA and ConocoPhillips USA.

-

The deal forms part of Tasmea’s stated programmatic acquisition strategy, following the Maxim Group acquisition.

Tasmea’s programmatic acquisition strategy has accelerated sharply in 2026, with the Maxim deal targeting electrical infrastructure markets forecast to grow at double-digit CAGRs through 2030 and the JPS deal adding a recurring LNG services platform, together lifting pro forma underlying EBIT toward A$185 million.

For investors, the update presents clear catalysts and a defined value-creation runway anchored to the structurally growing LNG and energy services market.

Don’t Miss the Next ASX Industrials Mover

Big News Blast delivers FREE breaking ASX announcements directly to your inbox within minutes of release, complete with in-depth analysis. Over 20,000 subscribers are already getting the edge on market-moving news the moment it drops. Click the “Free Alerts” button at Big News Blast to make sure you never miss the next major ASX industrials update.