HighCom Pushes Armour Revenue to FY27 as H2 Loss Narrows to $1.2M-$1.6M

HighCom revises H2 FY26 outlook as armour revenue shifts to FY27

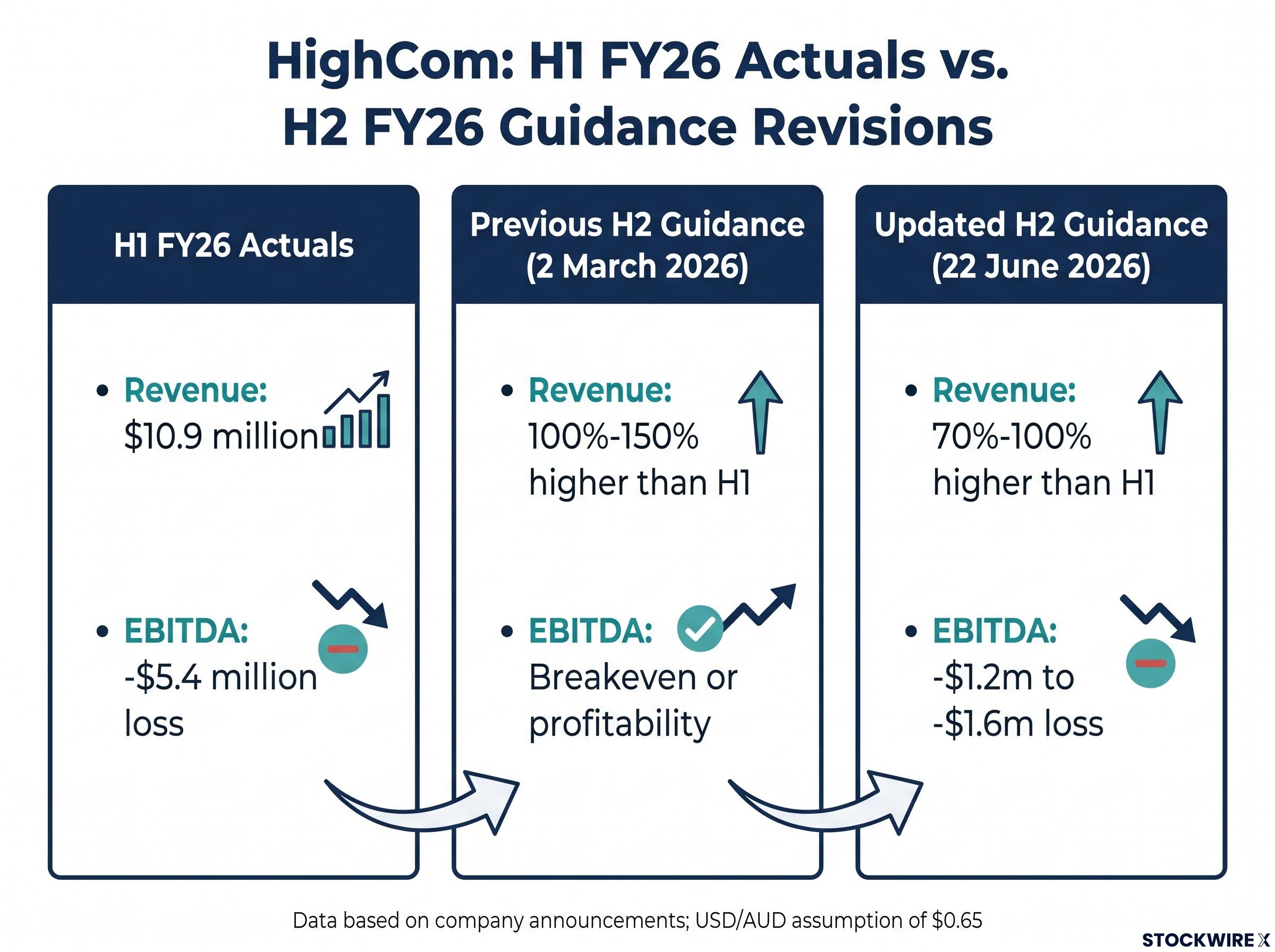

HighCom Limited has updated its half-year guidance, now expecting an EBITDA loss for H2 FY26 of between -$1.2 million and -$1.6 million, compared to the -$5.4 million loss recorded in H1 FY26. Revenue for the second half is expected to come in 70%-100% higher than H1 FY26 revenue of $10.9 million, marking a significant operational improvement despite missing the company’s previous breakeven target. The updated guidance, announced 22 June 2026, supersedes projections provided on 2 March 2026.

Whilst the revision represents a departure from previous expectations of breakeven or profitability, the company has characterised the shortfall as primarily timing-driven rather than reflecting deterioration in underlying financial performance or order book health.

What drove the guidance revision

Management cited three principal factors behind the updated outlook: timing of revenue recognition, a change in expected product mix for H2 FY26, and the deferral of certain armour orders into FY27. These headwinds were partially offset by stronger-than-expected performance from the company’s technology business.

The announcement updates guidance provided on 2 March 2026, when HighCom projected H2 revenue would be 100%-150% higher than H1, with the business expected to reach breakeven or profitability. The company has explicitly stated that “timing, rather than underlying financial performance, is the principal driver” of the variance from previous guidance.

The previous H2 FY26 guidance, issued on 2 March 2026, projected revenue 100%-150% above H1 levels and a return to breakeven or profitability, with US government procurement normalisation and XTclave armour technology cited as key drivers of the anticipated recovery.

| Metric | Previous Guidance (2 March 2026) | Updated Guidance |

|---|---|---|

| H2 Revenue Growth vs H1 | 100%-150% higher | 70%-100% higher |

| H2 EBITDA | Breakeven or profitability | -$1.2m to -$1.6m loss |

| H1 EBITDA (actual) | — | -$5.4m |

The company noted that both the previous and updated guidance incorporate a USD/AUD exchange rate assumption of $0.65.

When big ASX news breaks, our subscribers know first

Understanding EBITDA guidance and why timing matters for defence contractors

EBITDA — Earnings Before Interest, Taxes, Depreciation, and Amortisation — measures a company’s operating performance by isolating cash-generating activities from financing and accounting decisions. For investors, it provides a clearer view of operational profitability than net profit, which can be influenced by tax arrangements and capital structure.

Defence and armour contracts create inherently lumpy revenue patterns. Large orders involve extended production cycles, with revenue recognised only when specific delivery milestones are met. A single shipment delay or contract timing shift can materially affect reported results for a given quarter or half-year, even when the underlying order book remains intact.

For project-based defence suppliers like HighCom, this means half-yearly results can swing significantly based on delivery schedules without necessarily reflecting changes in competitive position, contract pipeline, or long-term financial health. The company’s updated guidance underscores this dynamic — revenue has been deferred rather than lost.

Cash position and capital requirements

The company has explicitly confirmed it holds adequate available cash on hand. Management stated the updated guidance “does not materially affect its forward cash position or its need to raise capital”, providing direct reassurance to investors regarding liquidity.

This statement takes on particular significance in the context of wider-than-expected losses. By proactively addressing capital adequacy, management signals confidence that existing cash resources can support operations through FY27 whilst deferred armour orders are recognised.

Technology business provides bright spot

Whilst armour revenue faced timing delays, the technology division delivered stronger-than-expected performance, partially offsetting the deferral impact. HighCom Technology supplies Australian Defence and Security Agencies with Small Uncrewed Aerial Systems (SUAS), sensor payloads, systems integration, maintenance, and logistics support.

The technology segment’s outperformance in H2 was underpinned by specific contract wins, including a counter-drone contract win worth A$9.81 million from the Australian Department of Defence, which marked HighCom Technology’s entry into the C-UAS market and was scheduled for delivery and payment within FY26.

The technology segment’s resilience demonstrates the benefit of operating across two distinct defence verticals. When one segment experiences contract timing delays, outperformance in the other can provide earnings stability — a structural advantage that may become increasingly relevant as the company scales.

Armour revenue deferred, not lost

The company clarified that certain armour orders have been deferred into FY27 rather than cancelled, distinguishing pushed-out revenue from lost contracts. HighCom Armor designs and manufactures personal protection ballistic products for military, law enforcement, and first responder customers globally.

The armour business spans three core product categories:

- Body Armour

- Ballistic Helmets

- Composite Armour Panels and Platform Structures

The distinction between deferred and cancelled revenue matters materially for investors. Deferred revenue implies the order book remains intact and these shipments will flow through in FY27, whereas cancelled contracts would signal demand erosion or competitive displacement. Management’s framing suggests backlog health has been preserved despite the timing setback.

The next major ASX story will hit our subscribers first

What investors should watch next

The guidance is based on unaudited management accounts and remains subject to final contract timing through 30 June 2026. HighCom has flagged that inventory carrying value assessments and other accounting matters remain under review as part of the year-end audit process, indicating the potential for further adjustments when audited accounts are released.

Key monitoring points for investors include:

- FY26 audited accounts release

- FY27 armour order recognition timing

- Continued technology segment momentum

- Any capital position updates

The audit process may result in revisions to preliminary figures, particularly around inventory valuations. Management’s decision to flag this explicitly suggests a disciplined approach to year-end accounting assessments rather than attempting to defer difficult adjustments.

Don’t Miss the Next Defence Sector Move

Join 20,000+ investors receiving FREE breaking ASX news delivered within minutes of release, complete with in-depth analysis. HighCom’s guidance revision highlights how quickly defence sector dynamics shift—stay ahead by clicking the “Free Alerts” button at Big News Blast to get real-time alerts the moment market-moving announcements break.