Challenger merges Fidante into $150 billion funds management powerhouse

Challenger Limited has entered a binding agreement to merge its multi-affiliate funds management business, Fidante, with Channel Capital, creating Channel Group — positioning the combined entity as one of Australia’s leading active funds management platforms with approximately $150 billion in assets under management.

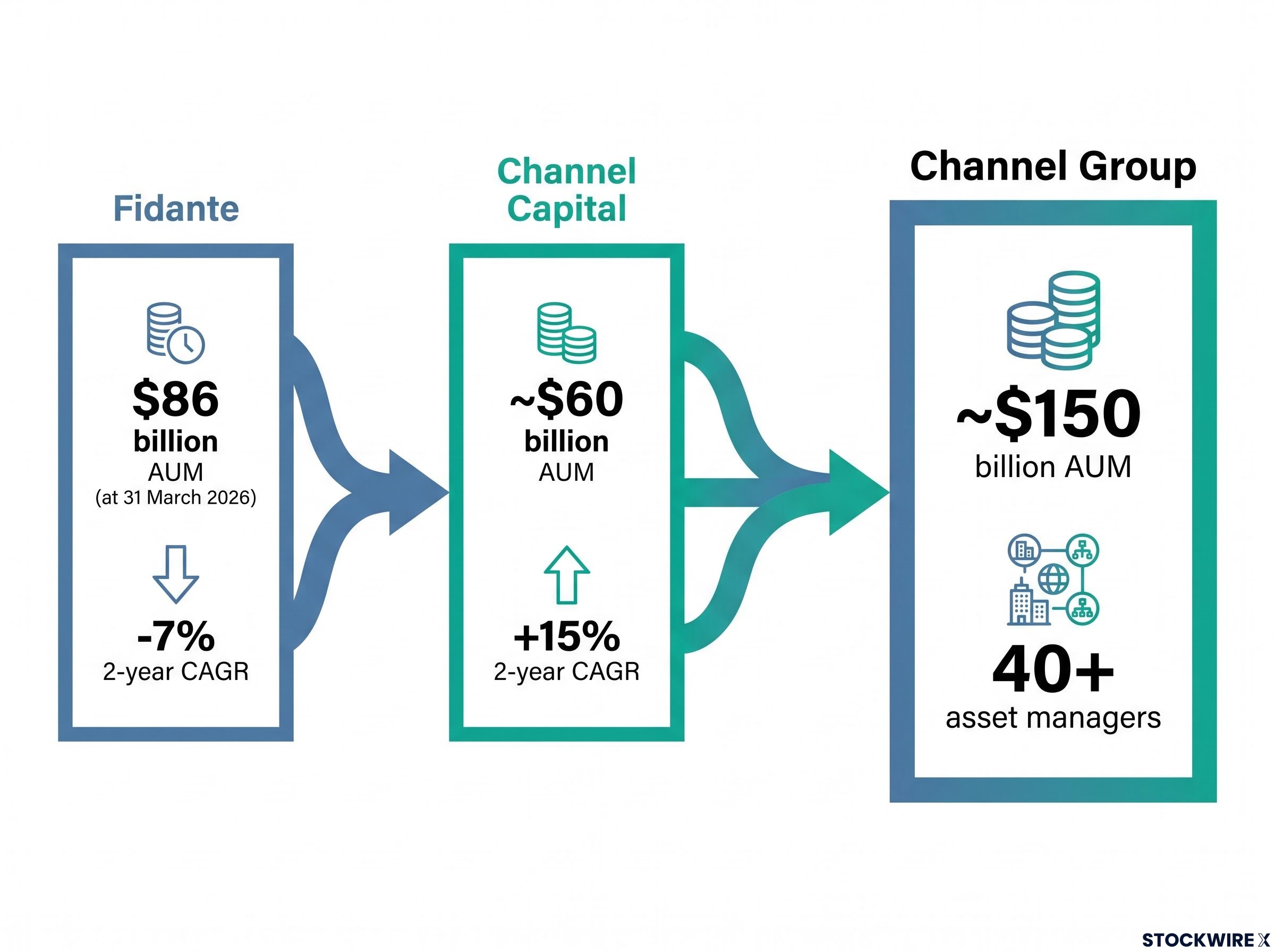

The merger brings together Fidante, which currently manages $86 billion (as at 31 March 2026), with Channel Capital’s approximately $60 billion in assets. Fidante will continue to operate as a standalone brand within the larger platform.

Glen Holding, current Channel Capital Managing Director, has been appointed Managing Director and CEO of Channel Group.

When big ASX news breaks, our subscribers know first

What is a multi-affiliate funds management model?

A multi-affiliate structure is a platform that partners with multiple independent investment managers rather than running a single in-house investment team. This model allows boutique asset managers to access distribution networks, administration services, and operational infrastructure while retaining full autonomy over their investment decisions.

Scale matters in this model because larger platforms can offer affiliates broader distribution reach, lower operational costs through shared services, and access to institutional investor networks that smaller managers would struggle to access independently.

Channel Group will support 40+ asset managers and global partners across public and private market strategies. The multi-affiliate model generates diversified fee income across multiple managers, reducing reliance on any single strategy’s performance or market cycle.

Transaction structure delivers cash and ongoing equity exposure

Challenger will own 45% of Channel Group equity, while existing Channel Capital shareholders and management will own 55%. The structure is designed to deliver both immediate value realisation and ongoing strategic exposure to the combined platform’s earnings.

Challenger is positioned to receive up to $172 million in cash payments subject to certain conditions. The company expects to recognise approximately $100 million in pre-tax gain on sale in FY27, with separation and transaction costs of $5 million to $8 million also expected in the same financial year.

The structure allows Challenger to retain strategic exposure to funds management earnings without consuming additional capital, converting a wholly-owned business into a minority stake in a scaled platform with improved growth prospects.

| Transaction Element | Detail |

|---|---|

| Challenger equity stake | 45% of Channel Group |

| Channel Capital/management ownership | 55% of Channel Group |

| Cash payments | Up to $172 million (subject to certain conditions) |

| Pre-tax gain on sale | Approximately $100 million (FY27) |

| Separation/transaction costs | $5-8 million (FY27) |

| Expected completion | First half FY27 (July-December 2026) |

Complementary capabilities across asset classes and investor channels

The two businesses bring distinct strengths to the combined platform. Fidante has established scale in equities and fixed income with award-winning retail and institutional distribution networks. Channel Capital contributes private markets expertise and extensive reach across high net worth, wholesale, family office, and adviser channels.

Performance trajectories differ markedly between the two platforms. Fidante has experienced a -7% two-year compound annual growth rate in assets, while Channel Capital has delivered +15% asset growth over the same period. The merger addresses Fidante’s recent headwinds by adding Channel’s faster-growing alternative strategies and wholesale distribution capability.

The combined platform demonstrates significant diversification across asset classes:

- 29% equities

- 27% fixed income

- 24% alternatives

- 20% other strategies

Channel Group’s pro forma EBIT is approximately $175 million. The business benefits from 85%+ recurring revenue streams and 35%+ EBIT margins (excluding cost synergies).

Key capability contrasts:

- Fidante: Specialists in equities, fixed income, liquid alternatives; award-winning retail and institutional distribution; Responsible Entity and full administration services; annuity-style RE revenues

- Channel Capital: Specialised in private markets and alternatives; extensive HNW, wholesale, family office and adviser reach; global partnerships across public and private strategies; majority staff-owned with equity incentivisation

Growth thesis centres on distribution expansion and alternatives

The strategic rationale for growth focuses on leveraging combined distribution networks to expand reach across retail, institutional, and offshore investor segments. Management identified clear opportunities that neither business could capture independently.

Channel Capital’s private equity, private credit, and infrastructure strategies will be distributed through Fidante’s broader platform, addressing a gap in Fidante’s product suite. Conversely, Fidante’s established institutional relationships will provide Channel’s boutique managers with access to larger investor networks.

The combined entity maintains a global footprint with 7 offices across Australia, the UK, the US, and the Cayman Islands, supported by 50+ distribution specialists. This international presence positions Channel Group to serve both Australian investors seeking global strategies and offshore investors seeking Australian market access.

The business operates with an “owner mindset” — majority staff ownership and equity incentivisation align employee interests with long-term platform growth. This structure is designed to retain talent across both businesses while maintaining the boutique culture that attracts independent asset managers to the platform.

Management commentary signals strategic alignment

Challenger Managing Director and CEO Nick Hamilton framed the transaction as a deliberate path to ensuring Fidante’s next stage of growth within a larger, more diversified platform.

Nick Hamilton, Managing Director and CEO, Challenger Limited

“We have been deliberate in our decision to pursue a merger with a strategically and culturally aligned business that will deliver strong outcomes for shareholders, affiliates and our employees. The merger delivers scale and opportunities for Fidante, which will benefit our affiliates and clients.”

Hamilton emphasised the strategic partnership model underlying the transaction, noting Challenger’s excitement about Channel Group’s broader geographic reach, wider investor base, and opportunities for employees.

Glen Holding, Channel Capital Managing Director, positioned the combination as creating a distinctive platform that supports boutique Australian managers while providing global investment managers with a trusted gateway into the Australian market.

“Bringing together the strength and expertise of Channel Capital and Fidante will result in a highly diversified and resilient platform with the ability to invest through market cycles,” Holding stated.

The management commentary underscored cultural alignment and a shared objective of supporting boutique asset managers, maintaining the brands and relationships that sit at the centre of client engagement.

Governance and independence maintained through board structure

Channel Group will operate with an independent Chair jointly appointed by Challenger and Channel Capital, ensuring balanced representation at the board level. The governance structure reflects the ownership split while providing both parties with strategic influence.

Four directors will be appointed by Channel Capital and two appointed by Challenger. This composition aligns with the equity distribution while ensuring Challenger retains meaningful board representation despite holding a minority stake.

The structure ensures alignment between key stakeholders while providing Challenger with ongoing influence over strategic direction. Importantly, Challenger Investment Management (Challenger IM) remains 100% owned by Challenger, separate from this transaction.

Timeline and regulatory pathway to completion

The merger is expected to complete in the first half of FY27 (July to December 2026), subject to regulatory approvals and satisfaction of customary closing conditions. The transaction requires several regulatory clearances before proceeding:

- Foreign Investment Review Board (FIRB) approval

- Australian Competition and Consumer Commission (ACCC) clearance

- Overseas regulatory approvals

Challenger will enter into a Transitional Services Agreement to provide technology and operational services for up to 24 months following completion of the merger. This arrangement ensures continuity of critical systems and processes during the integration period while the combined entity establishes its independent operational infrastructure.

The binding agreement establishes firm commitments from both parties, with completion contingent on standard transaction closing conditions and the regulatory approvals outlined above.

Investment implications for Challenger shareholders

The transaction delivers both immediate financial benefit and ongoing strategic exposure to a scaled funds management platform. The approximately $100 million pre-tax gain on sale (subject to completion accounts at close) provides near-term earnings uplift in FY27, partially offset by $5-8 million in separation and transaction costs.

Challenger’s 45% equity stake in Channel Group provides ongoing exposure to a larger, faster-growing platform with diversified fee streams across 40+ asset managers and global partners. The structure converts a wholly-owned business experiencing recent headwinds into a minority stake in a scaled platform with improved growth prospects.

The capital efficiency is notable: Challenger will receive up to $172 million in cash payments subject to certain conditions while retaining a 45% equity stake in Channel Group, without deploying additional capital. The combined entity’s 85%+ recurring revenue profile and 35%+ EBIT margins (excluding cost synergies) provide a quality earnings stream.

The Fidante merger is one of several simultaneous strategic moves by Challenger, with its alternative credit expansion through a $3.7 billion equipment finance acquisition from Bank of Queensland signalling the company is deliberately diversifying earnings streams across funds management, secured lending, and annuities in parallel.

The structure addresses the cyclical pressures facing Fidante’s -7% asset growth trajectory by combining it with Channel Capital’s +15% growth rate, creating a more diversified platform across asset classes, distribution channels, and investor segments.

Want the Next Financial Sector Breakthrough in Your Inbox?

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with in-depth analysis. Big News Blast delivers market-moving announcements from finance, tech, healthcare and beyond straight to your inbox. Click the “Free Alerts” button to get ahead of the next major sector shift.