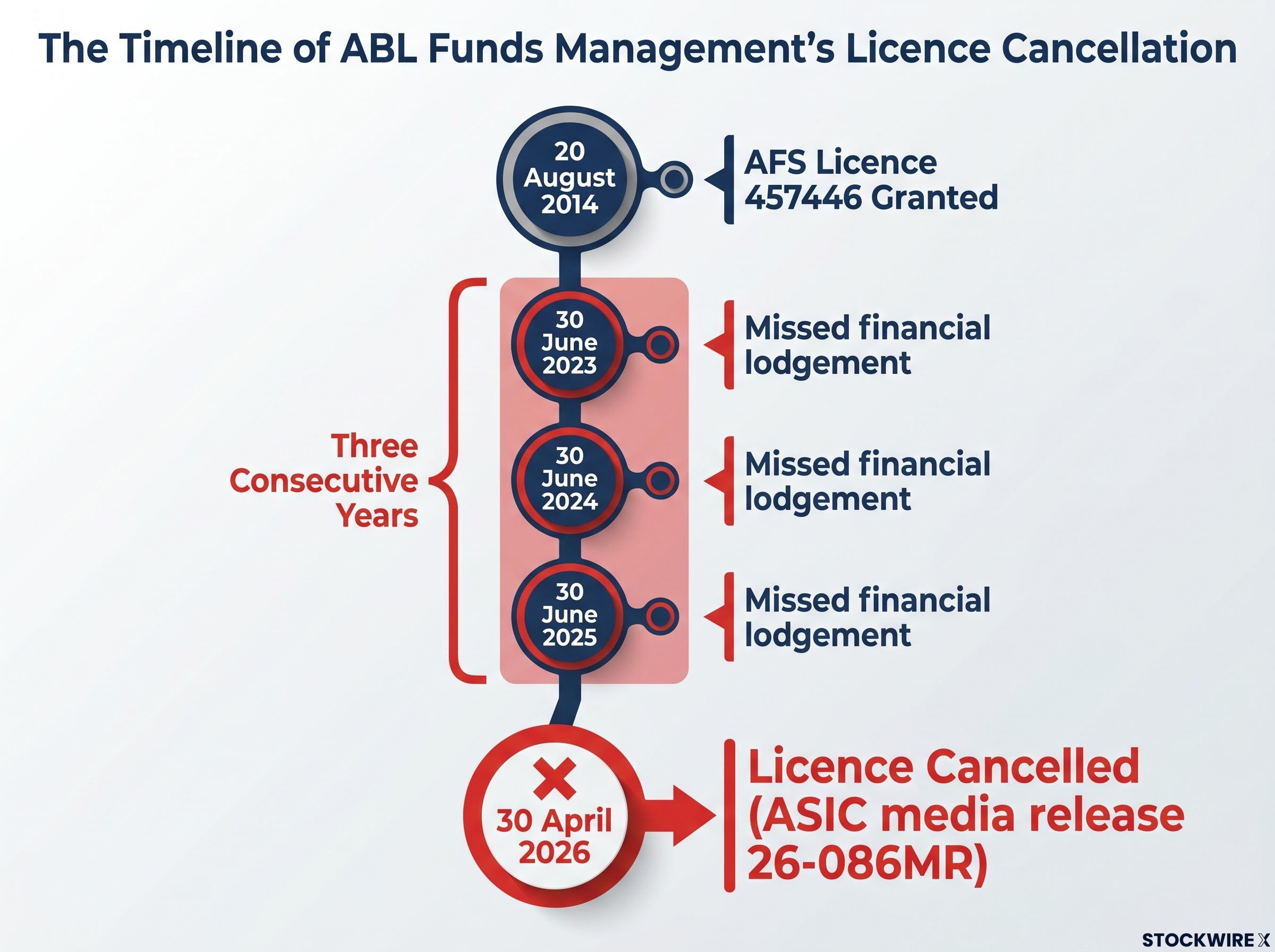

In April 2026, ASIC cancelled the Australian Financial Services licence held by ABL Funds Management Pty Ltd. The firm had failed to lodge required financial statements and audit reports for three consecutive years. One enforcement action, three missed reporting cycles, and the licence that authorised the firm to operate simply ceased to exist.

For Australian fund managers and their clients, AFS licence cancellation is not a fine, a warning, or a condition attached to ongoing operations. It is the termination of the legal authorisation to provide financial services, and it carries immediate, practical consequences for every mandate the affected firm holds. The ABL case, announced via ASIC media release 26-086MR on 30 April 2026, offers a concrete lens through which to understand how cancellations work, what statutory obligations trigger them, what happens to clients when a fund manager loses its licence, and what appeal rights exist for affected firms.

The authorisation that makes fund management legal in Australia

An AFS licence is issued by ASIC under the Corporations Act 2001 (Cth) and is the legal authorisation required to carry on a financial services business in Australia. Without one, a firm cannot lawfully provide financial product advice, deal in financial products, or hold client assets. The licence is the entry point, but obtaining it is only the beginning.

What the licence authorises versus what holding it requires

ABL’s licence, AFS Licence 457446, was granted on 20 August 2014. It authorised the firm to provide general financial product advice, deal in financial products, and provide custodial and depository services, all limited to wholesale clients only. Those authorisations defined what ABL could do. The obligations attached to the licence defined what ABL had to keep doing to retain the right.

Holding an AFS licence is an ongoing regulatory relationship with continuing obligations, not a one-off approval. The core requirements include:

- Financial resources: Maintaining adequate capital and liquidity to support the services covered by the licence

- Risk management and compliance: Operating appropriate systems to identify, manage, and monitor risks

- Reporting and audit lodgement: Preparing audited financial statements and lodging them with ASIC within prescribed timeframes

Each of these obligations applies for as long as the licence is held. A firm that meets them at the point of application and then allows them to lapse has not satisfied the regulatory bargain. That distinction, between a licence as a static approval and a licence as a living obligation, is what makes cancellation a logical consequence rather than a bureaucratic surprise.

When big ASX news breaks, our subscribers know first

What ASIC’s power to cancel actually looks like in practice

ASIC’s authority to suspend or cancel an AFS licence sits in section 915B of the Corporations Act 2001 (Cth). The provision sets out several grounds on which the regulator may act. The key grounds that can lead to cancellation include:

- The licensee has failed to comply with its obligations under the financial services laws

- The licensee does not meet its financial reporting and audit obligations

- The licensee has ceased to carry on a financial services business

- ASIC has reason to believe the licensee will not comply with its obligations in the future

In ABL’s case, the ground was specific and well-documented. The firm failed to lodge audited financial statements and audit reports for three consecutive financial years.

The ABL cancellation arose from sustained non-compliance, but s 915B also contains a mandatory cancellation ground that operates differently: once ASIC is satisfied a licensee has ceased carrying on a financial services business, it must cancel the licence regardless of whether any misconduct is involved.

The core factual trigger: ABL failed to lodge audited financial statements and audit reports for the financial years ending 30 June 2023, 30 June 2024, and 30 June 2025, a sustained pattern of non-compliance spanning three full reporting cycles.

Three consecutive years of non-lodgement is not a single administrative slip. It represents a sustained breakdown in the most basic compliance obligation a licensee owes to its regulator. That pattern is what placed the matter within the scope of outright cancellation rather than a softer regulatory response such as a warning or licence condition.

The cancellation has been publicly recorded on ASIC’s Professional Registers Search, meaning anyone can verify ABL’s current licence status.

Why financial reporting obligations carry so much regulatory weight

Lodged, audited financial statements are not paperwork. They are a surveillance mechanism that serves three distinct audiences simultaneously, and when a licensee stops lodging them, all three lose visibility at once.

| Audience | What Lodgements Provide | Consequence of Non-Lodgement |

|---|---|---|

| ASIC | Ability to assess solvency, capital adequacy, and whether the licensee is operating within its authorisations | Complete loss of monitoring visibility; the regulator cannot verify the firm’s financial soundness |

| Wholesale clients | One of the few external indicators of a manager’s financial stability and governance quality | Clients have no independently audited evidence that their manager remains solvent and properly controlled |

| Broader market | Integrity of ASIC’s registers and reliability of the licensed population | Market participants cannot trust that all registered licensees meet baseline standards |

From ASIC’s perspective, a three-year lodgement gap amounts to an information blackout. The regulator has no audited data on which to assess whether the firm meets capital requirements, is solvent, or is operating within its licence authorisations. That is not a technical gap. It is a substantive failure in the regulatory architecture.

ASIC Regulatory Guide 166 sets out the specific financial requirements AFS licensees must satisfy on an ongoing basis, including the capital adequacy and liquidity standards that underpin ASIC’s ability to assess whether a licensee remains financially sound across successive reporting periods.

ABL is not an isolated case. Eden Asset Management had its licence cancelled after the firm entered liquidation, and Ballast Financial Management lost its licence after ceasing to carry on a financial services business. Across these matters, the enforcement pattern is consistent: where basic compliance obligations break down over an extended period, ASIC treats licence cancellation as the appropriate response.

What licence cancellation means for the clients left behind

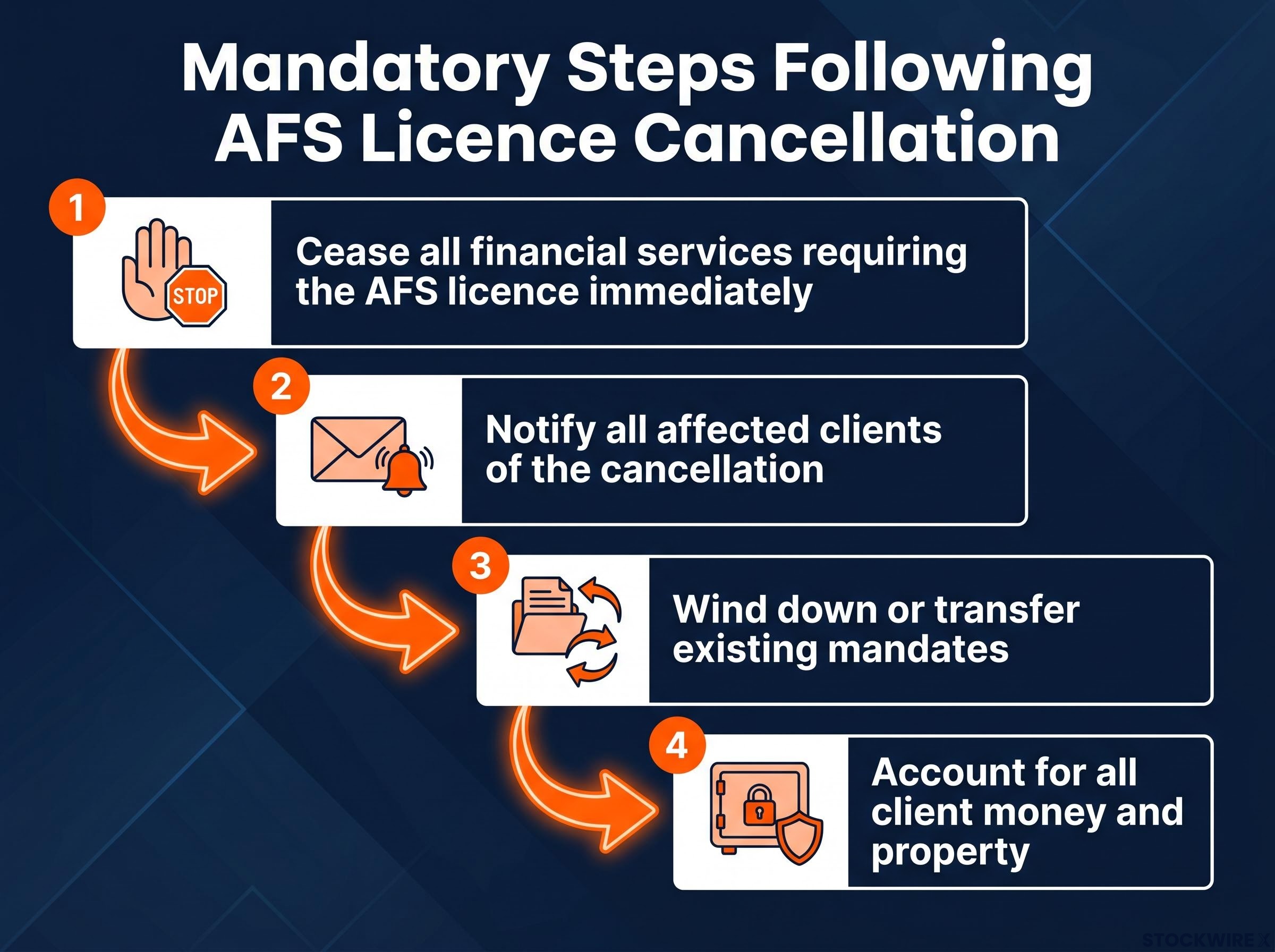

Once an AFS licence is cancelled, the firm must immediately cease providing any financial services that require that licence. Continuing to do so constitutes unlicensed conduct under the Corporations Act 2001 (Cth), exposing the firm and its officers to civil and potentially criminal liability.

The sequence of steps that must follow a cancellation is specific and non-discretionary:

- Cease all financial services that require the AFS licence, effective immediately

- Notify all affected clients of the cancellation and its implications for their mandates

- Wind down or transfer existing mandates and investment management agreements, either terminating them or novating them to another appropriately licensed firm, subject to contract terms and client consent

- Account for all client money and property, ensuring that obligations under contract and general law are discharged even though the licence no longer exists

The firm retains ongoing obligations to clients under contract and general law even after losing its licence. Cancellation removes the right to provide financial services; it does not extinguish the duty to properly account for client assets.

The wholesale client experience in practice

ABL’s clients were exclusively wholesale clients: institutions, professional investors, and high-net-worth individuals. These investors are generally better positioned to navigate a manager transition than retail consumers. They typically have legal and financial advisers, undertake ongoing due diligence, and may hold contractual protections such as termination rights triggered by licence loss or changes in regulatory status.

The disruption is operationally significant regardless of sophistication. Mandates must be reassigned. Reporting lines change. Investment strategies may need to be reviewed or re-tendered with a replacement manager. For wholesale clients holding illiquid or complex positions, the transition timeline can stretch well beyond the initial cancellation date.

Not every financial licence cancellation follows the enforcement pathway seen in ABL’s case; the in1Bank matter in May 2026 demonstrated that an orderly licence exit under APRA supervision can return every depositor’s funds before the licence is formally revoked, a contrast that illustrates how the outcome for clients depends heavily on whether the exit is structured and supervised or forced by regulatory action.

Review rights and what ABL can do next

ASIC’s cancellation is not necessarily the final word. The regulator has explicitly stated that ABL may apply to the Administrative Review Tribunal (ART) for a merits review of the decision, under the Administrative Review Tribunal Act 2024.

The practical points for any firm in this position are worth understanding clearly:

- What a merits review is: The Tribunal can reconsider the facts and the law and decide what the correct or preferable decision should be, not merely whether ASIC followed the correct process

- What the Tribunal can do: It may affirm, vary, or set aside ASIC’s decision entirely

- When it must be filed: Review applications must generally be lodged within a prescribed timeframe (commonly around 28 days from notification in many federal review regimes), though the exact limit should be confirmed for the specific matter

- What happens to the licence during the review: ASIC’s cancellation continues to operate unless and until the Tribunal makes a specific order, such as a stay of the decision

A merits review differs from a judicial review. In a judicial review, a court examines whether the decision-maker followed the correct legal process. In a merits review, the Tribunal steps into the shoes of the original decision-maker and determines what the right decision should have been on the facts. The distinction matters: a merits review offers a broader path to reinstatement, but the licence remains cancelled while the review proceeds.

Filing a review application does not pause the cancellation. A firm cannot treat its licence as effectively reinstated by the act of lodging the application. Until the Tribunal makes an order, the firm remains unlicensed.

Five compliance lessons every AFS licensee should take from ABL

The ABL matter is a single case, but the lessons it produces apply to every AFS licensee, particularly smaller or wholesale-only firms that may underestimate ongoing compliance obligations.

- Reporting obligations apply even in quiet or difficult years. Even if a business is dormant, restructuring, or winding down, statutory financial reports and audits must be prepared and lodged on time unless and until the licence is properly surrendered or cancelled. Operational inactivity does not suspend the obligation.

- Non-lodgement is a substantive breach, not a minor administrative issue. ASIC allowed three full financial years of non-compliance to accumulate before cancelling ABL’s licence, which suggests earlier opportunities for the firm to engage and remediate were not taken. Treating a missed lodgement as trivial is a serious mistake.

- Wholesale-only status does not reduce regulatory expectations. ABL dealt exclusively with wholesale clients. That did not spare it from enforcement. ASIC expects wholesale managers to meet the same core licence standards as retail-focused firms, particularly around financial reporting and audits.

What clients and counterparties should do

- Check ASIC registers as part of basic due diligence. ASIC maintains public, searchable registers of current and cancelled AFS licences, and the cancellation of ABL’s licence is recorded there. ASIC’s Professional Registers Search is freely accessible, and checking a manager’s current licence status takes minutes. Clients, counterparties, and advisers should make this a routine check before and during any investment relationship.

- Engage ASIC early if compliance is under strain. For firms facing resource constraints, governance problems, or impending closure, proactive engagement with ASIC, and if necessary, voluntary variation or surrender of the licence, is preferable to allowing multiple years of non-compliance to accumulate and invite enforced cancellation. The pattern across ABL, Ballast Financial Management, and Eden Asset Management confirms that ASIC treats this as a consistent enforcement approach, not an isolated action.

Licence cancellation is one tool in ASIC’s enforcement arsenal; the regulator also holds director disqualification powers under Section 206F of the Corporations Act, which allow it to ban individuals from managing any corporation for up to five years without a court order, a sanction that can be applied to officers of failed or non-compliant entities independently of what happens to the entity’s licence.

When the regulator runs out of patience, only the licence pays the price

AFS licence cancellation is the outcome of sustained, not isolated, non-compliance. In ABL’s case, three years of missed lodgements produced one cancellation and a firm that can no longer operate until the position is resolved through review or remediation.

The enforcement message from ASIC is consistent across recent cases: every AFS licensee, regardless of size, client type, or operational activity level, is expected to meet basic governance and reporting discipline. The consequences of not doing so are public, immediate, and operationally disruptive, for the firm and for every client relying on the licence that no longer exists.

Investors wanting to understand how ASIC pursues enforcement beyond the licensing regime will find our full explainer on the Nuix disclosure appeal, which examines how ASIC is challenging the Federal Court’s treatment of prospectus revenue forecasts, continuous disclosure obligations, and materiality thresholds for ASX-listed companies.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.