How Australia’s Largest CFD Penalty Exposed a Broken Model

3 hrs ago

SpaceX is set to begin trading on Nasdaq today under the ticker SPCX at an implied valuation of US$1.77 trillion, making it potentially the largest IPO in stock market history by capital raised. The listing has generated enormous retail interest. Yet for the Australian investors most eager to buy in, the structural realities of this particular debut, a tiny free float, institutional allocation advantages, and a timezone that puts the opening auction in the middle of the night, mean that day-one trading conditions bear almost no resemblance to buying an established stock.

Listing day is not the same as “getting in at the IPO price.” The mechanics of how SPCX will actually open, who already holds shares at what price, and what happens to orders placed before bed are questions that matter far more than the headline valuation number. What follows breaks down exactly how the SpaceX debut will unfold, what risks are specific to today versus the longer term, and what practical steps an Australian investor should take before placing any order.

The scale is genuine. SpaceX is offering 555.6 million shares at US$135 each, raising approximately US$75 billion and surpassing Saudi Aramco’s 2019 debut (approximately US$29 billion) as the largest IPO on record by deal size. The implied market capitalisation of US$1.77 trillion would place the company among the ten largest US-listed entities from day one.

The core listing facts:

Those numbers, though, embed assumptions most retail investors have not stress-tested.

SpaceX reported 2025 revenue of US$18.7 billion against a net loss of US$4.9 billion, attributed largely to xAI investment and Starship development expenditure. The valuation rests almost entirely on forward growth expectations rather than current earnings.

The offer price of US$135 is the other figure worth contextualising. That price was set through the bookbuild process and allocated primarily to institutional investors. Most retail buyers will never trade at US$135. They will trade at whatever price the opening auction and subsequent volatility produce.

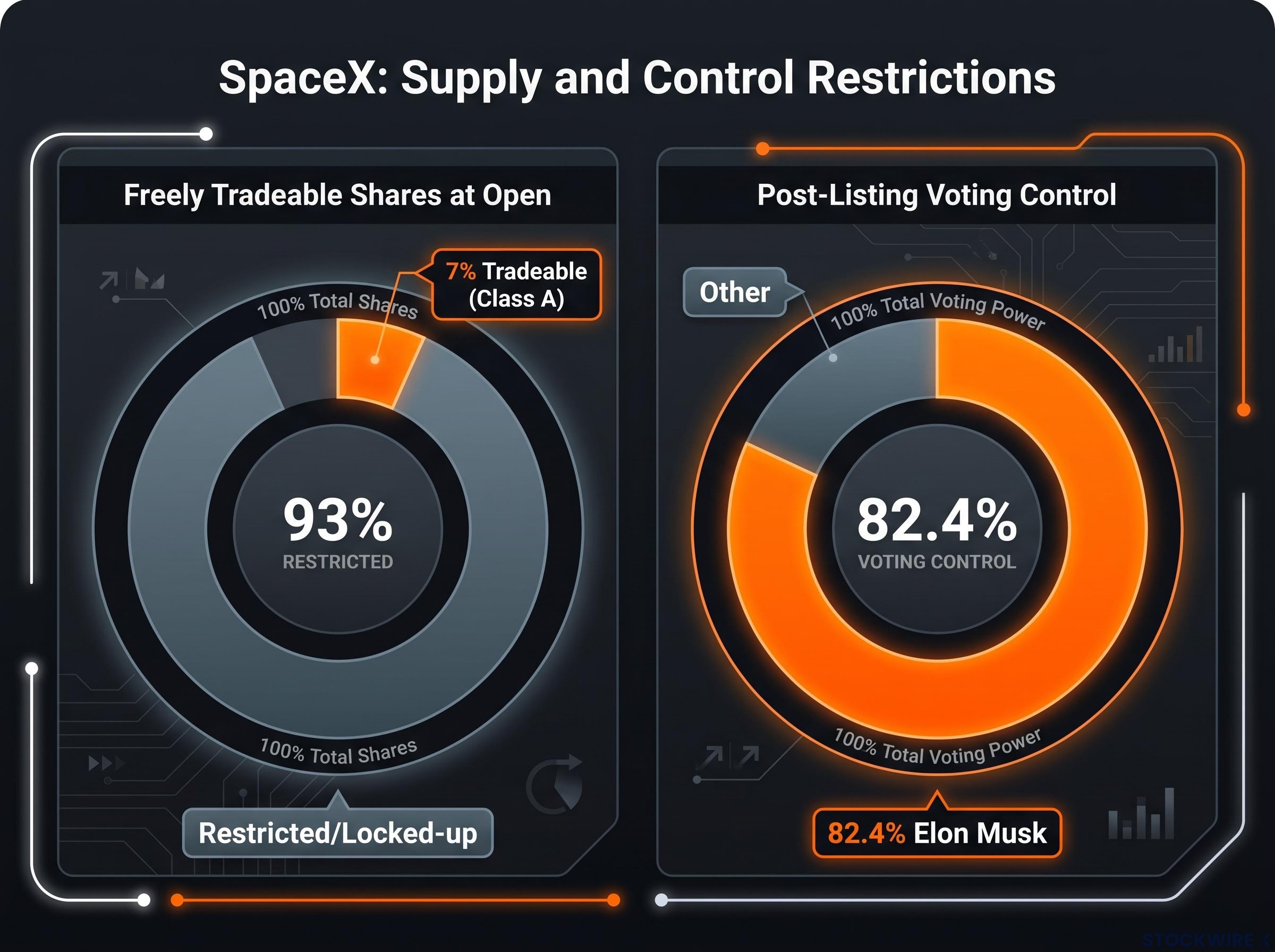

Free float refers to the portion of a company’s shares that are actually available for public trading. Shares held by founders, employees, and early investors who are contractually restricted from selling (typically through lock-up agreements) sit outside the float. They exist on paper but cannot enter the market.

For SPCX, approximately 7% of Class A shares are expected to be freely tradeable at open. The remaining majority is locked up. Elon Musk is expected to retain approximately 82.4% of voting control post-listing, with his holdings forming the largest block of restricted shares.

Nasdaq float rules define unrestricted publicly held shares in a way that excludes affiliate-held shares, locked-up shares, and unregistered holdings, which is precisely why a company with a US$1.77 trillion market capitalisation can simultaneously have only 7% of its shares available for public trading on debut day.

A 7% float on a company valued at US$1.77 trillion means the tradeable pool of shares is extraordinarily thin relative to the demand chasing it. Three practical consequences follow directly:

Constrained-float volatility is not theoretical. Virgin Galactic surged during the 2021 meme-stock period before declining more than 98% from its peak. The free float figure is the single most important structural fact for any investor considering a day-one trade.

For a mega-IPO like SPCX, the open will not resemble a normal 9:30 a.m. bell. The sequence unfolds in stages:

The Nasdaq IPO Halt Cross process governs exactly how the opening auction for a new listing is conducted, including the conditions under which Nasdaq can extend the matching period, pause trading on volatility imbalances, and reset the auction before a first print is recorded.

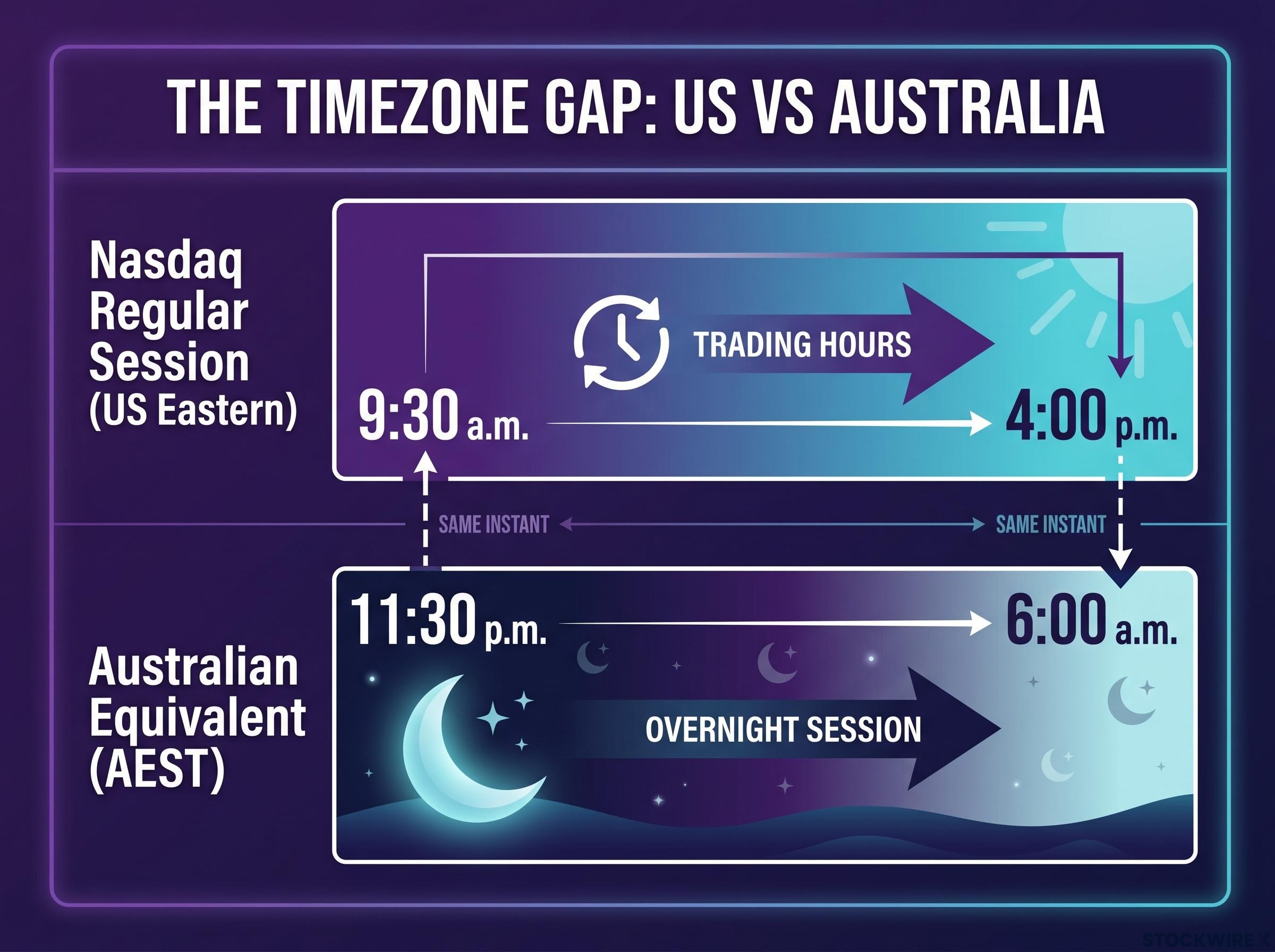

Nasdaq’s regular session (9:30 a.m. to 4:00 p.m. US Eastern) maps to approximately 11:30 p.m. to 6:00 a.m. AEST, meaning most Australians will be asleep for the opening auction on day one.

The practical implication is direct: an Australian investor placing an order before bed may find it fills hours later, at a price shaped by conditions they never saw, during a halt they could not respond to. Orders placed during a halt remain queued and will execute when trading resumes. Without active monitoring, there is no way to intervene.

The SpaceX IPO is, structurally, a two-stage market. The first stage happened before today. Through the bookbuild and roadshow process, large fund managers, banks, and pension funds received share allocations at the fixed offer price of US$135. A portion of allocations also went to select retail participants, though the majority went to institutions. These buyers are inside the deal.

IPO allocation mechanics consistently favour institutional participants: fund managers, pension funds, and underwriting banks receive shares at the fixed offer price through the bookbuild, while retail investors are left to buy in the open market after that price advantage is already locked in.

Anyone buying SPCX in the open market today is in the second stage. They are not buying at US$135. They are buying at whatever price the opening auction and subsequent trading produce, which, given the structural conditions already described, could be materially higher.

Academic research on IPOs consistently finds that first-day price appreciation disproportionately accrues to those who received the initial allocation. By the time a stock opens for public trading, much of any opening “pop” is already captured by allocated holders.

| Attribute | IPO allocation buyer | Secondary market buyer (day one) |

|---|---|---|

| Price paid | US$135 (fixed offer price) | Opening auction price (unknown until it clears) |

| When allocated | Before listing, through bookbuild | After listing, through open market |

| Information advantage | Access to roadshow, management meetings | Public information only |

| Who they are | Institutions and select retail participants | Any investor with a brokerage account |

Understanding that distinction, that buying in the open market today means buying as a secondary participant, not an IPO participant, is the foundational mindset shift that prevents overpaying in the opening minutes of a hyped listing.

Australian investors need a broker with US market access to trade SPCX. The basic setup and order placement sequence:

SelfWealth charges a flat US$9.50 brokerage fee per trade regardless of transaction size, with a 60 basis point foreign exchange conversion fee applied when transferring funds into or out of a USD account. The platform provides access to more than 5,000 US-listed equities and over 3,000 US ETFs. SPCX is expected to be available in the same manner as other Nasdaq-listed securities, though some platforms may require a few additional days post-listing before enabling trading in a new ticker.

Two platform-level restrictions directly affect day-one risk. Most brokers, including SelfWealth, disable pre-market and after-hours trading for new IPOs, limiting exposure to regular Nasdaq hours only. And the timezone reality means that if a queued order is sitting in the book when a trading halt clears at 2:00 a.m. AEST, the investor cannot intervene.

Limit orders, not market orders, are especially important when bid-ask spreads are wide and price discovery is still in progress. A limit order sets the maximum price a buyer is willing to pay; a market order accepts whatever price is available, which in a thin, volatile debut can be far from expectations.

The chaos of the debut session is temporary. The structural questions are not.

Pre-IPO shareholders, including founders, employees, and early venture capital investors, are typically restricted from selling for 90 to 180 days post-listing under lock-up agreements. These agreements are the direct reason the free float is only 7% at open. They are also a known future event: when lock-ups expire, a large additional pool of shares becomes eligible for sale, and that incoming supply can create downward pressure if demand does not match it.

Institutional investors track lock-up expiry dates closely in their positioning. This does not guarantee a price decline when the restriction lifts; if demand is strong enough, the market can absorb additional supply. But it is a structural factor that long-established companies do not face in the same way.

| Risk factor | Practical takeaway |

|---|---|

| Free float (~7% at open) | Thin markets amplify price swings; even modest orders move the stock |

| Lock-up expiry (90-180 days) | A large increase in tradeable shares is a known future supply event |

| Valuation vs. financials | US$1.77T on US$18.7B revenue with a US$4.9B net loss implies very optimistic growth expectations already priced in |

| Key-person and governance risk | Elon Musk holds ~82.4% of voting control; outcomes are highly sensitive to one individual’s decisions |

A US$1.77 trillion valuation on US$18.7 billion in revenue, with a US$4.9 billion net loss in 2025, implies that very optimistic growth expectations are already embedded in the offer price. The market is not pricing SpaceX as it is today. It is pricing SpaceX as investors expect it to become over the next decade and beyond.

Long-term IPO underperformance is a structural pattern in the data rather than an outcome unique to any individual listing: newly listed companies have underperformed comparably sized established peers by an average of 3.3% per year over their first five years, a drag that compounds into a material dollar difference over a typical holding period.

Capital intensity is a structural feature of this business, not a temporary condition. Rockets and satellite constellations require sustained heavy investment. Starship development expenditure was a major contributor to the 2025 net loss, and that spending is expected to continue.

The governance structure adds another layer. SpaceX will operate under a dual-class share arrangement similar to Tesla, with Elon Musk retaining approximately 82.4% of voting control following the listing. For minority public shareholders, this concentrates strategic decision-making in a single individual and creates key-person risk that extends well beyond the debut session.

The structural realities are worth restating plainly. Approximately 7% of Class A shares will be tradeable at open. The opening auction is expected to extend into late morning or early afternoon US Eastern Time, which corresponds to the middle of the night in Australia. Institutions received their allocations at US$135 through the bookbuild; secondary market buyers will pay whatever price emerges from a chaotic and delayed auction. Lock-up expiries in 90 to 180 days represent a material future supply event.

None of this means SpaceX is a poor business. It means that trading its stock on debut day, under these specific conditions, carries risks that are distinct from a considered investment decision made after price discovery has stabilised.

Before placing any order, five steps are worth completing:

SPCX will still be there next week, and next month. The debut session, with its thin float, delayed auction, wide spreads, and timezone mismatch, will not.

For readers who want US market exposure but prefer a more diversified approach than a single high-valuation debut, our dedicated guide to international ETFs for Australian investors covers how broad-market US ETFs like IVV provide access to hundreds of large American companies, including established technology and aerospace names, without the concentration risk of a single IPO position.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

SpaceX is listing on Nasdaq under the ticker SPCX at an offer price of US$135 per share, implying a market capitalisation of approximately US$1.77 trillion and raising around US$75 billion, which would make it the largest IPO in stock market history by capital raised.

Australian investors need a broker with US market access, such as Stake or SelfWealth, and must complete a W-8BEN tax form, convert AUD to USD, and place a limit order during regular Nasdaq hours (9:30 a.m. to 4:00 p.m. US Eastern Time), which correspond to approximately 11:30 p.m. to 6:00 a.m. AEST.

A 7% free float means only a small fraction of SpaceX shares are available for public trading at open, which creates conditions for large price swings from modest orders, unusually wide bid-ask spreads, and significant slippage risk for anyone placing market orders during the debut session.

The US$135 offer price was set through the bookbuild process and allocated primarily to institutional investors before listing; anyone buying SPCX in the open market on debut day will pay whatever price emerges from the opening auction, which could be materially higher depending on demand and volatility.

Pre-IPO shareholders are typically restricted from selling for 90 to 180 days post-listing, which is why only 7% of shares are tradeable at open; when lock-ups expire, a large additional pool of shares becomes eligible for sale, representing a known future supply event that could create downward price pressure.