Steadfast Group receives $6.00 per share acquisition offer from Amwins-Dragoneer Consortium

Steadfast Group has received a conditional, non-binding, indicative offer from US-based Amwins Group and Dragoneer Investment Group to acquire 100% of the company’s outstanding share capital at $6.00 per share in cash via a scheme of arrangement. The proposal values Steadfast at approximately $7.7 billion on an enterprise value basis.

The offer, announced on 10 June 2026, follows a period of negotiation during which the consortium submitted earlier indicative proposals at $5.50 and $5.83 per share. Under the proposed structure, Dragoneer would acquire Steadfast’s retail brokerage business whilst Amwins would acquire the underwriting agency division.

A scheme of arrangement is a court-supervised transaction that requires approval from 75% of votes cast and a majority of shareholders voting. If approved, all shareholders receive identical consideration, providing deal certainty unavailable under traditional takeover structures where acquirers can end up with partial ownership.

To progress the proposal, Steadfast entered into a Process Deed on 10 June 2026, granting the consortium eight weeks of due diligence access (automatically extended for successive two-week periods unless Steadfast provides written notice at least five days prior to expiry that it no longer wishes to pursue the transaction). The company has confirmed it will continue to update shareholders in accordance with continuous disclosure obligations as the process advances.

Based on Steadfast’s 1,114.5 million fully diluted shares on issue (inclusive of 2.5 million performance rights), net debt of $733 million and non-controlling interests of $253 million as at 31 December 2025, the proposal represents a significant premium to recent trading levels.

When big ASX news breaks, our subscribers know first

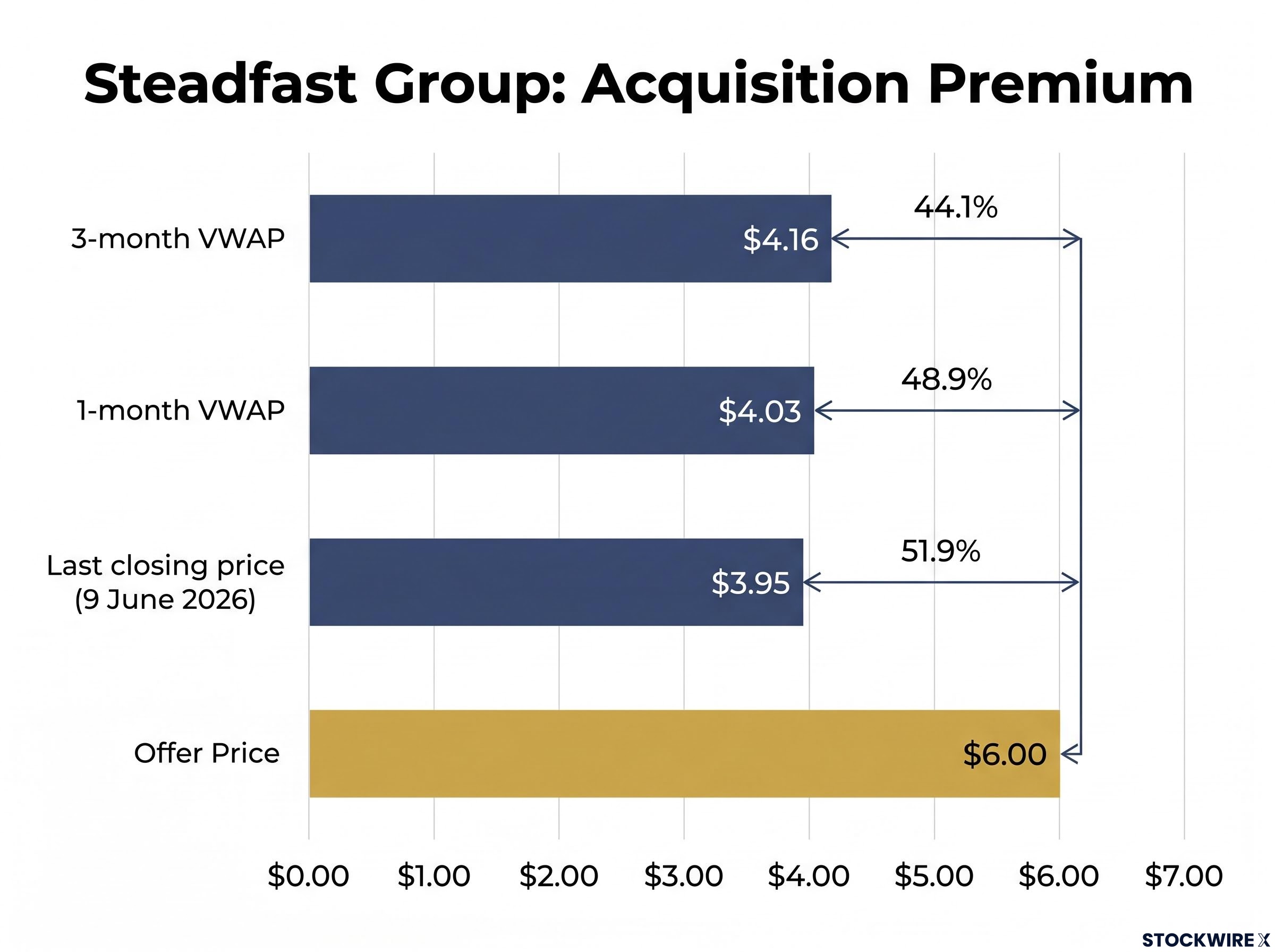

Premium analysis shows substantial upside to recent trading levels

The $6.00 per share offer represents a material premium across multiple reference points. Steadfast shares closed at $3.95 on 9 June 2026, the last trading day before the announcement.

| Metric | Reference Price | Offer Price | Premium |

|---|---|---|---|

| Last closing price (9 June 2026) | $3.95 | $6.00 | 51.9% |

| 1-month VWAP | $4.03 | $6.00 | 48.9% |

| 3-month VWAP | $4.16 | $6.00 | 44.1% |

A premium of approximately 50% to recent trading levels indicates the consortium sees material value in Steadfast’s franchise and market position beyond current market pricing. The offer price must be reduced by any dividends or distributions declared or paid by Steadfast after 5 June 2026.

Board intends to recommend the transaction

Steadfast’s Board has determined it is in shareholders’ best interests to enter into the Process Deed and progress discussions with the consortium. The Board has confirmed it intends to unanimously recommend the transaction, subject to three conditions:

- Agreement on acceptable terms of a binding scheme implementation deed

- Absence of a superior proposal

- Independent expert concluding (and continuing to conclude) that the offer is in shareholders’ best interests

Each Steadfast director has also indicated they intend to vote shares they own or control in favour of the scheme, subject to the same conditions. This alignment between Board recommendation and director voting intentions provides clarity on the Board’s view of the proposal’s merits.

The Process Deed grants the consortium access to confidential information and due diligence materials to enable them to assess the transaction and work towards a binding offer.

Key conditions and regulatory approvals required

The proposal remains subject to satisfactory completion of due diligence and execution of a binding scheme implementation deed. Multiple regulatory approvals must be obtained before any transaction can complete:

- Satisfactory completion of due diligence by the consortium

- Execution of a binding scheme implementation deed

- Unanimous Board recommendation (subject to conditions outlined above)

- Foreign Investment Review Board (FIRB) approval

- Australian Competition & Consumer Commission (ACCC) clearance

- New Zealand Overseas Investment Office approval

The ACCC will assess whether the acquisition raises competition concerns in Australian insurance broking or underwriting agency markets. FIRB approval is required as the consortium comprises foreign entities acquiring an Australian company above monetary thresholds. The New Zealand approval reflects Steadfast’s operations across the Tasman.

Completion is not guaranteed and shareholders should understand the regulatory approval process may take several months. The absence of a financing condition precedent (confirmed in the Key Terms) removes one common hurdle in acquisition transactions.

Exclusivity arrangements and deal timeline

The Process Deed grants the consortium eight weeks of due diligence access from and including the business day after 10 June 2026, unless extended by agreement. During this exclusivity period, Steadfast is subject to “no shop” and “no talk” restrictions that prevent the company from soliciting or engaging with competing bidders.

The exclusivity period is structured in two phases. The first four weeks constitute a “hard exclusivity” period during which no fiduciary exception applies. The consortium must provide written confirmation by the end of this period that due diligence is progressing satisfactorily and they remain committed to the transaction.

Hard exclusivity vs soft exclusivity

Following the hard exclusivity period, the remaining term becomes a “soft exclusivity” period during which the Board may respond to unsolicited superior proposals if legal advice indicates fiduciary duty requires it. This structure balances deal certainty for the consortium with appropriate protections for shareholders if a materially better offer emerges.

If Steadfast receives an unsolicited competing proposal during the soft exclusivity period that the Board determines could be a superior proposal, the company must notify the consortium within 24 hours and provide five business days for the consortium to submit a matching counterproposal. This matching right mechanism ensures the consortium has opportunity to respond to competitive pressure.

Who are the acquirers?

Amwins Group

Amwins is a leading international wholesale insurance distribution business headquartered in the United States. The company places over US$49 billion of premium annually and maintains relationships with more than 36,000 retail agency relationships and 1,300 carrier and MGA relationships.

Under the proposed structure, Amwins would acquire Steadfast’s underwriting agency business, which provides specialist insurance products in niche market segments to the open market through a portfolio of majority-owned underwriting agencies.

Dragoneer Investment Group

Dragoneer is a US-based investment firm. Under the proposed structure, Dragoneer would acquire Steadfast’s retail brokerage business, which operates insurance broker and agency networks in Australia, New Zealand, Singapore and the United States.

The consortium’s structure suggests they see distinct value in Steadfast’s two operating segments and have strategic plans to develop them independently. This separation mirrors Steadfast’s own operational structure and may facilitate focused management strategies post-acquisition.

Previous offers and negotiation history

The $6.00 per share proposal follows a period of engagement during which the consortium submitted two earlier indicative offers. The first proposal valued Steadfast at $5.50 per share in cash (less any dividends or distributions declared or paid by Steadfast). The consortium subsequently increased this to $5.83 per share in cash (less any dividends or distributions declared or paid by Steadfast) before arriving at the current $6.00 offer.

The progression from $5.50 to $5.83 to $6.00 demonstrates active price discovery and negotiation between Steadfast’s Board and the consortium. The 9.1% increase from first offer to final proposal suggests the Board has extracted improved terms through the negotiation process.

Minimum holding buy-back terminated

Steadfast has terminated the proposed minimum holding buy-back announced on 12 May 2026. This is a standard step when a company enters into a takeover or scheme process, as proceeding with the buy-back would complicate the capital structure and potentially affect the transaction mechanics and pricing.

The termination ensures all shareholders remain on the register during the exclusivity and due diligence period, maintaining a clean share register if the transaction progresses to implementation.

What shareholders should do now

Shareholders do not need to take any action at this stage. The $6.00 per share proposal is indicative, conditional and non-binding. No shareholder vote has been scheduled and the consortium is currently conducting due diligence to assess whether to proceed to a binding offer.

If the transaction progresses, Steadfast will convene a scheme meeting and shareholders will receive a comprehensive scheme booklet containing:

- Full details of the proposed transaction and its terms

- An independent expert’s report assessing whether the scheme is in shareholders’ best interests

- Reasons for the Board’s recommendation

- Information about how to vote and attend the scheme meeting

The due diligence period and regulatory approval processes will determine whether a binding offer eventuates. Steadfast will continue to update shareholders in accordance with continuous disclosure obligations as material developments occur.

Advisers appointed

Steadfast has assembled an advisory team to support the Board through the evaluation and negotiation process:

- J.P. Morgan and Citigroup act as joint financial advisers

- Insight Capital Advisors serves as independent adviser

- Mallesons provides legal advice

The appointment of dual financial advisers alongside an independent adviser reflects the scale and complexity of the proposed transaction.

Want the Next Financial Sector Takeover in Your Inbox?

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with in-depth analysis. Major M&A moves like this $7.7 billion Steadfast offer arrive in your inbox the moment they’re announced. Click the “Free Alerts” button at Big News Blast to get ahead on market-moving financial sector news.